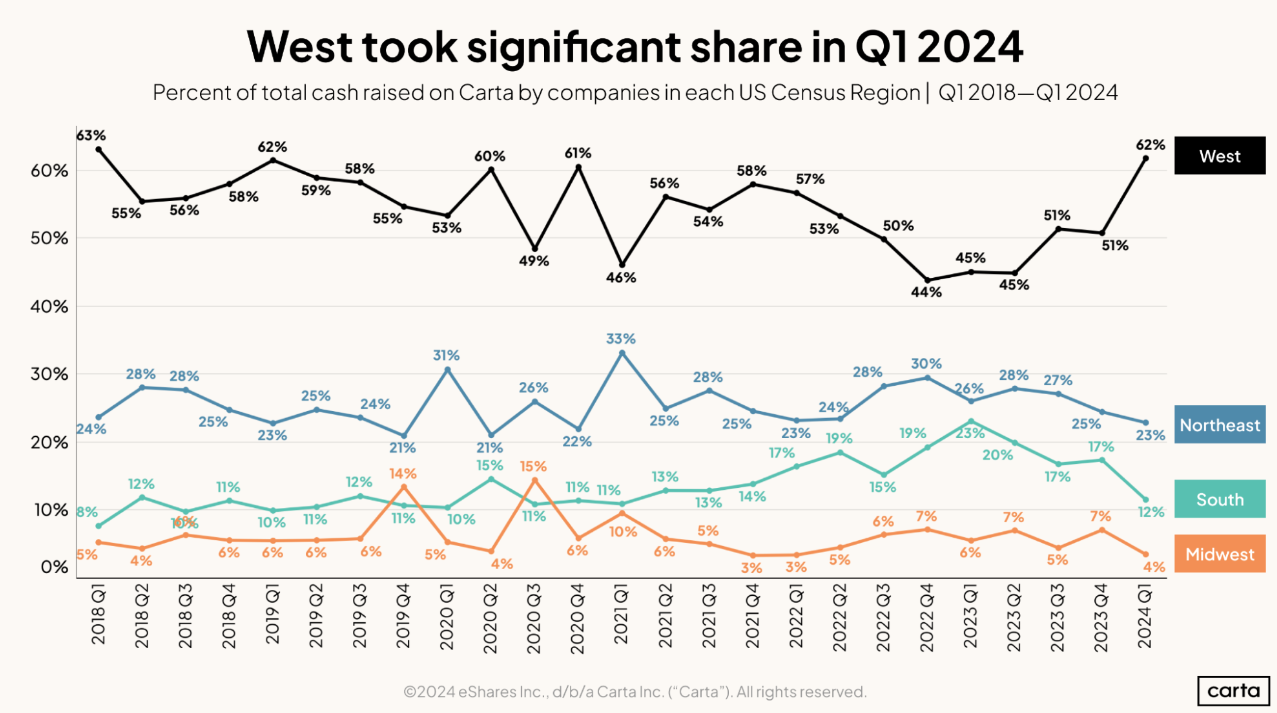

Startups based in the West census region raised 62% of all capital on Carta during the first quarter of 2024, the highest quarterly figure in more than three years. The other three census regions—the Northeast, the South, and the Midwest—all saw declines in their share of startup fundraising.

But what’s true across the entirety of the venture capital landscape is not always true in every niche. In some of the most common startup industries, the distribution of capital across the regions of the U.S. looks quite different.

Download the data addendum to see industry deal counts by regionHere’s a closer look at how venture capital funding was dispersed across the U.S. in four key industries in Q1—and at how Q1’s numbers compare to the full annual data in these industries over the previous five years.

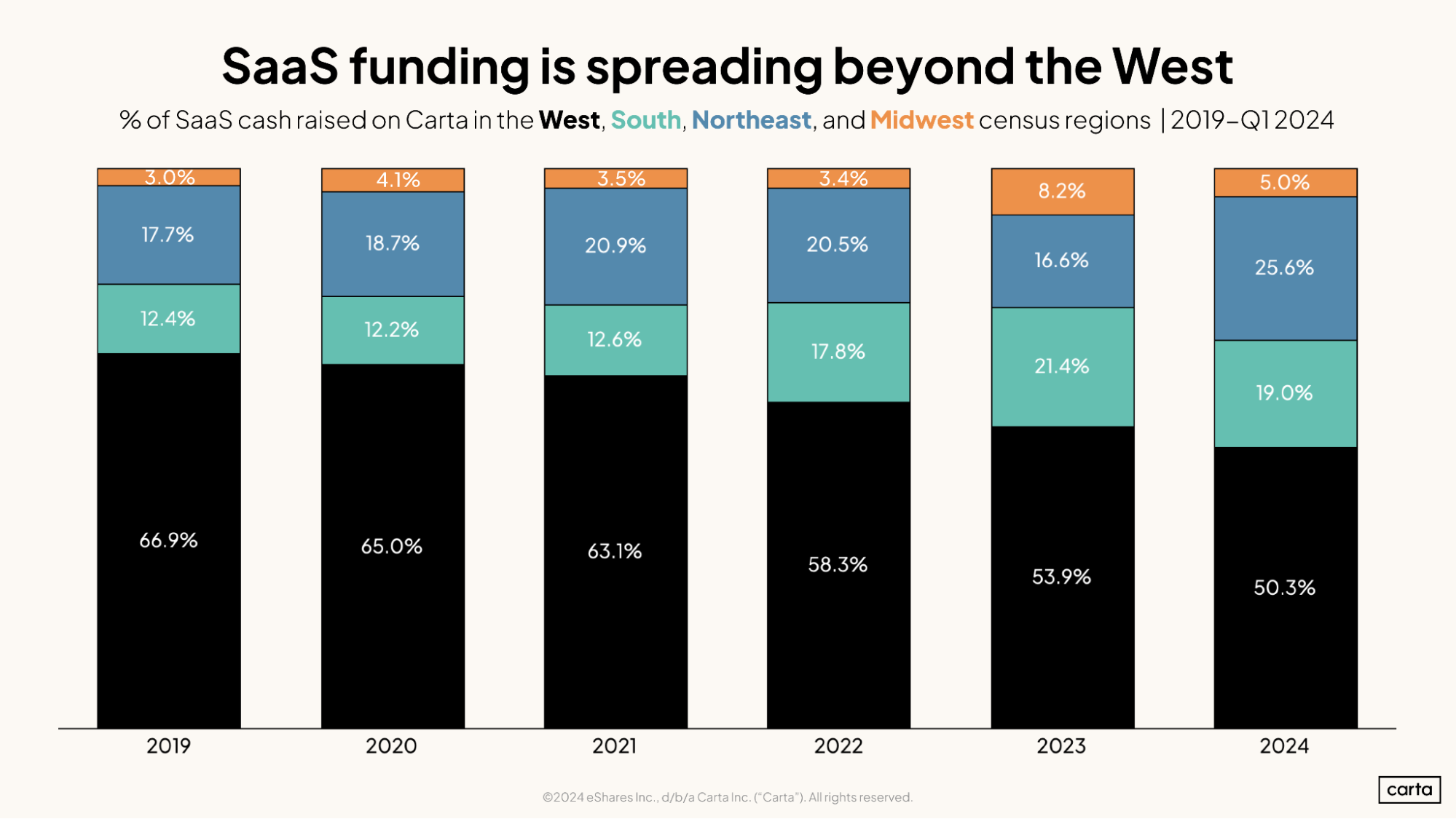

SaaS

In recent years, the West’s percentage of cash raised in the SaaS sector has been higher than its percentage of cash raised across all sectors. This makes sense given the Bay Area’s longtime role as the nation’s preeminent hub for software startups, as well as the contributions of other ecosystems with strong reputations for software development, such as Seattle and Salt Lake City.

In Q1 2024, however, this trend reversed: Startups in the West region raised 50.3% of all venture capital that went to software startups in the quarter, well below that 62% share of funding that the West captured across all sectors.

Startups in the Northeast claimed about a quarter of all cash raised in the SaaS industry in Q1, much higher than their typical share over the previous five years. This gave the region the second-highest share of SaaS funding in Q1, as has been the case in four of the previous five years. The lone exception was 2023, when startups from the South outraised Northeastern startups by nearly five percentage points.

The South’s share of investment in SaaS startups has climbed significantly since the end of 2021—part of a broader growth of Southern ecosystems during the 2020s. In 2019, SaaS startups in the West raised 5.4x more VC funding than SaaS startups in the South. By 2023, that ratio narrowed to just 2.5x.

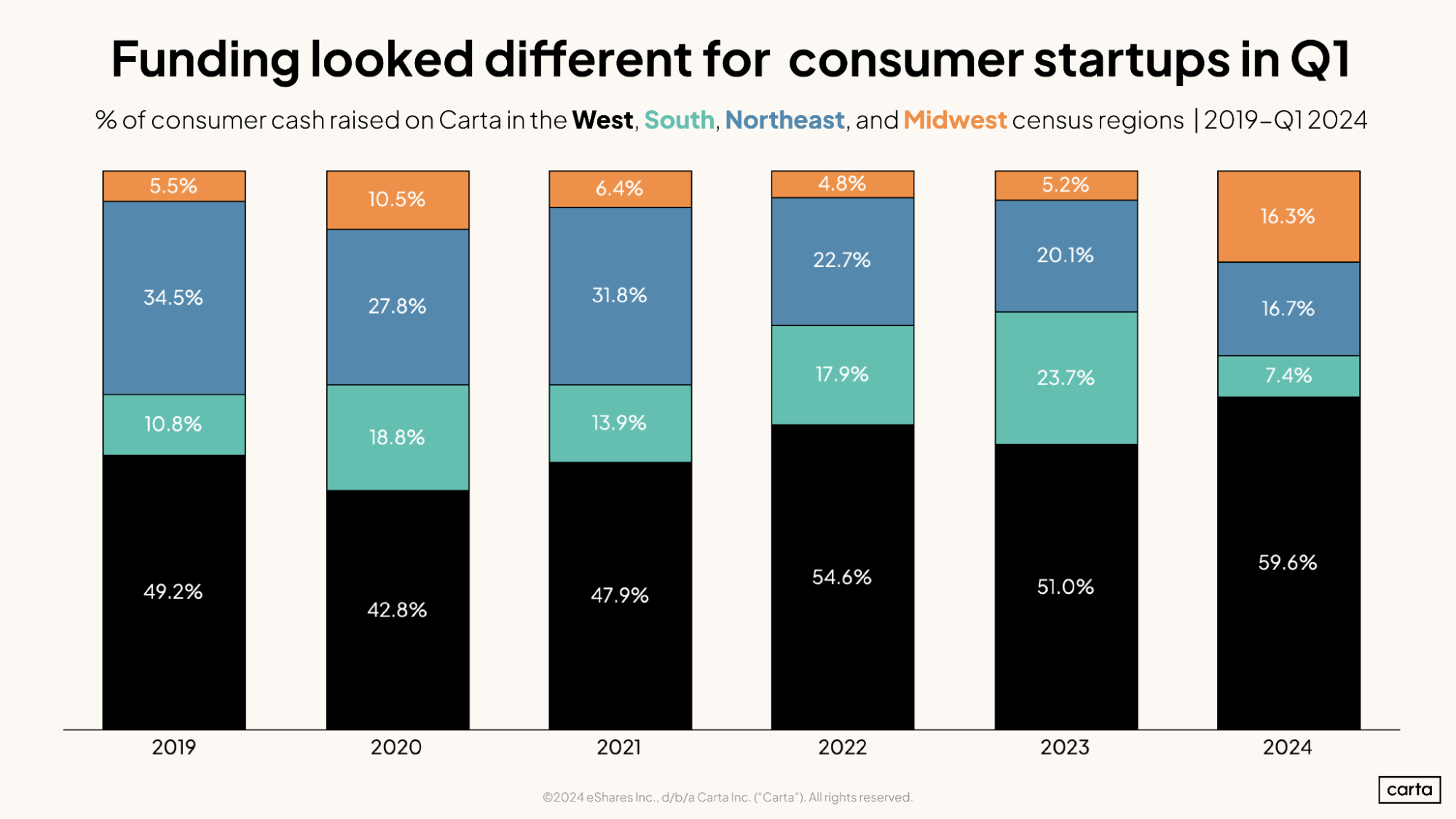

Consumer

In the consumer sector, startups from the West raised 59.6% of all VC funding in Q1. That’s nearly in line with the region's 62% share of funding across all sectors. But it’s a notable increase from the West’s share of consumer fundraising over the previous five years.

There were large shifts in market share across the board for consumer fundraising in Q1, with the Midwest’s percentage of cash raised jumping to 16.3% and the South’s falling to just 7.4%. This data may very well smooth out as the rest of the year unfolds: Since we’re comparing one quarter from 2024 to past full years, some of this change in Q1 may be noise. There were just 121 overall consumer deals on Carta in Q1, compared to 663 during all of 2023.

Check out our downloadable asset here for full data on quarterly deal counts in the consumer, SaaS, fintech, and health sectors over the past five years.

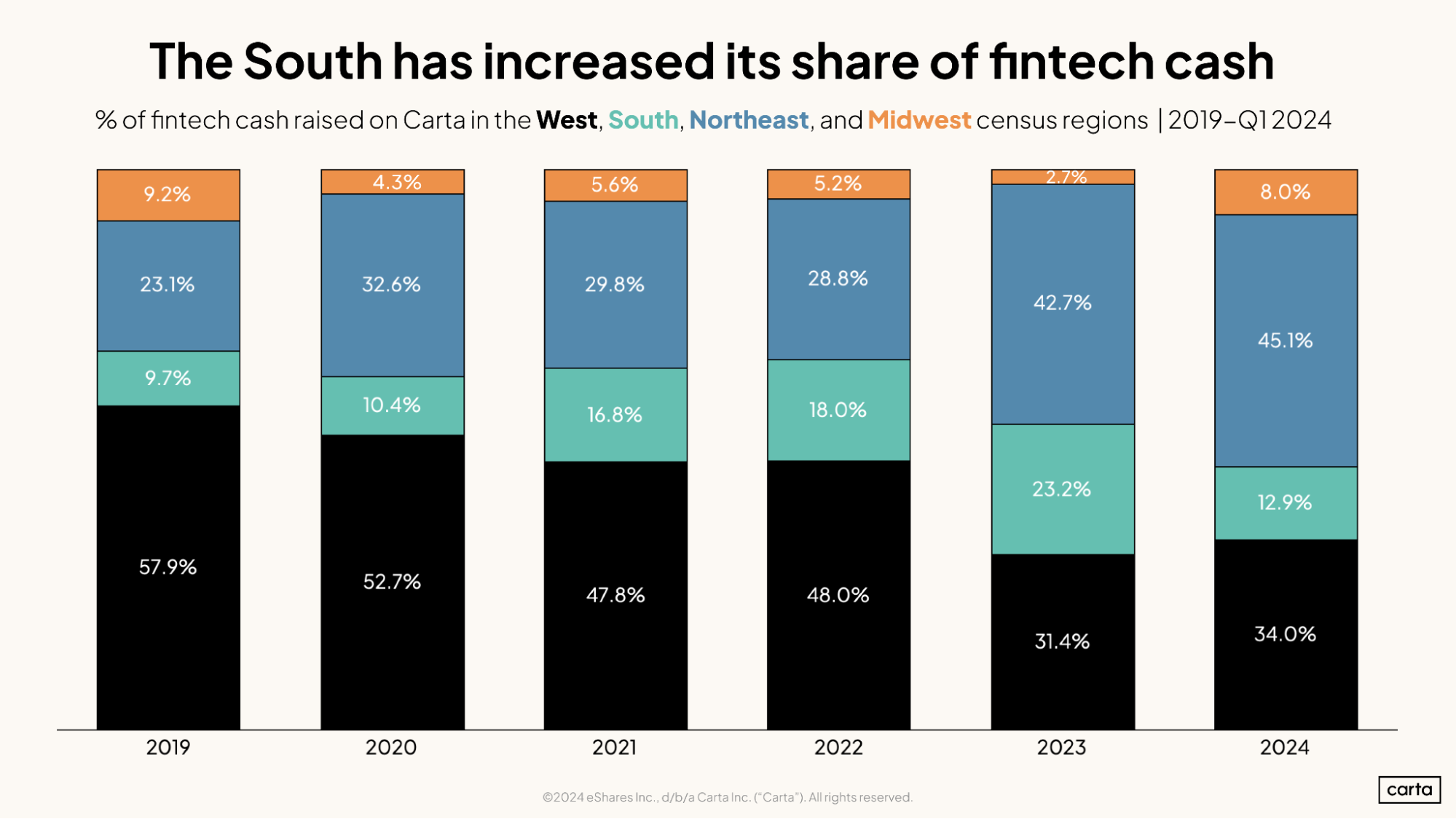

Fintech

The geographic divide of fintech funding looks quite different from the split of funding across all industries. In fintech, startups from the West raised just 34% of all VC in Q1 2024, about in line with a 33.1% share of fintech funding in 2023. That’s nearly half of the West’s 62% share of cash raised in all sectors.

The Northeast is the clear leader in this sector, claiming 45.1% of fintech cash raised in Q1, compared to 23% of total cash raised. The South started the year off slow, with 12.9% of fintech cash raised in Q1, comapred to 23.2% during 2023.

As is the case with both SaaS and consumer, the South has been steadily increasing its share of cash raised in the fintech industry over the past several years. Some of those gains have come at the expense of the West, which has claimed a much smaller share of all fintech funding from 2022 onward than in the preceding three years.

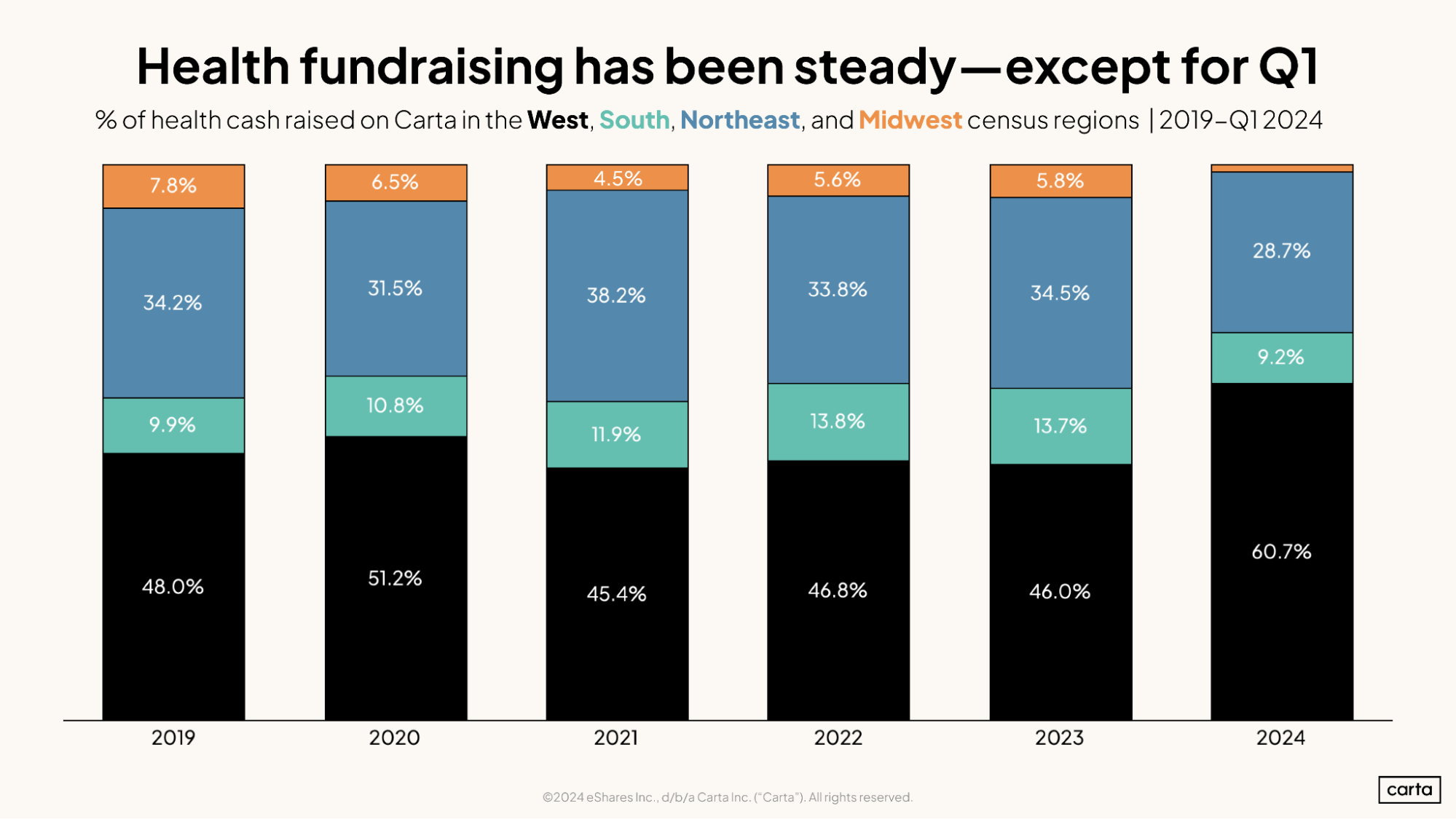

Health

The breakdown of fundraising in the health industry—comprising biotech, healthtech, and medical devices—is relatively similar to the overall breakdown of fundraising that’s served as our reference point. Western startups raised 60.7% of health funding in Q1, nearly equaling their overall 62% share. Northeastern startups raised 28.7% of all Q1 capital in healthcare, and Southern startups brought in 9.2%, compared to respective shares of 23% and 12% across all sectors.

Outside of Q1 2024, the split of health funding across these four census regions had been relatively consistent in recent years. This could be another instance where the relative size of the sample in Q1—health companies on Carta raised about $5.4 billion in Q1, compared to $19.1 billion over the course of 2023—makes it unwise to yet draw any long-term conclusions.

The breakdown of deal count between these regions in Q1, as opposed to cash raised, looks quite different. Startups in the West closed just 34.8% of new health investments in Q1, compared to a 60.7% share of cash raised. Startups in the Northeast finished Q1 with the same 34.8% of all deals closed.

Download additional data

The downloadable addendum to this story contains eight charts analyzing deal counts by industry and region.