- Private equity fund structures

- How are typical PE funds structured?

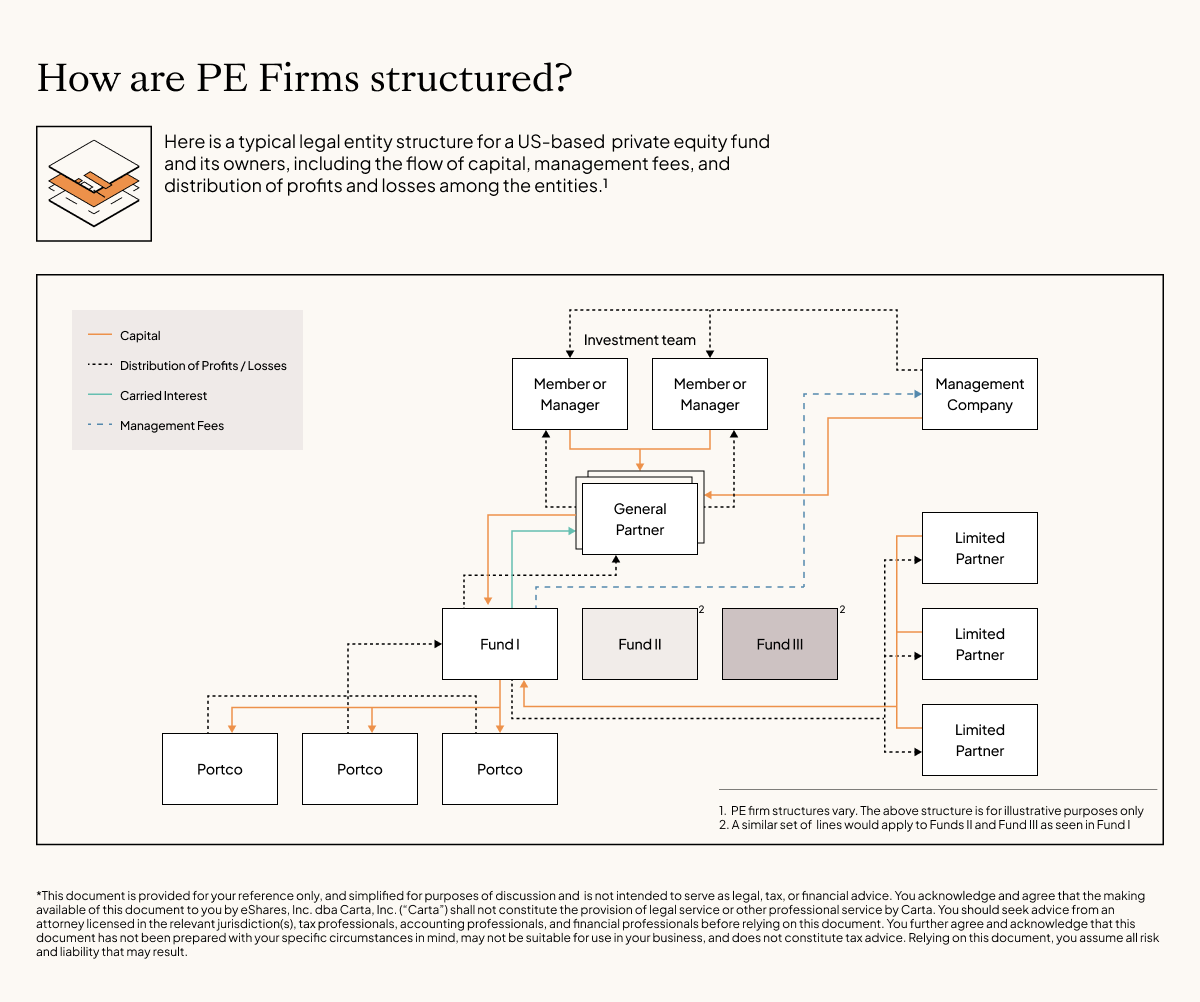

- Private equity fund structure diagram

- The components of the firm

- The general partner

- The management company

- The fund

- The portfolio companies

- Why are PE funds structured this way?

- Operational flexibility

- Taxes

- Limitation of liability

- Regulatory compliance

- Tradition

A traditional U.S. private equity firm is an aggregation of entities that raises funds from private investors. Private equity firms are structured in such a way as to efficiently acquire, manage, and ultimately divest stakes in companies. The private equity funds’ structure allows fund managers to flexibly invest private capital by leveraging the fund manager’s expertise, with the intent of maximizing the returns to their investors.

This article was written in collaboration with Weil, Gotshal & Manges LLP.

How are typical PE funds structured?

The most common entity structure for a U.S. private equity fund is the limited partnership. A limited partnership is a business arrangement between at least one general partner (“GP”) and at least one limited partner (“LP”), where the GP controls the day-to-day operations of the fund’s business and assumes unlimited personal liability for the debts and obligations of the partnership.

Funds often have several LPs or “investors,” who contribute capital for the fund’s investments, which are made in accordance with the fund’s investment strategy. The LPs’ liability is typically limited to their capital commitment and contingent upon their obligation to make timely capital contributions in the amounts agreed upon in the fund’s operating agreement.

In addition to the GP and the LPs, most funds also have a “management company” or “manager,” which provides services to the fund pursuant to a contractual arrangement. For tax and regulatory reasons, the investment professionals who own the GP entity (sometimes called the “key persons”) often form a separate management company to manage the fund’s investments or its “portfolio,” as well as the investments or “portfolio” of any other funds that may be advised by the manager.

As shown in the diagram below, in the typical structure, the GP manages the funds, while the management company manages the fund’s investments, sometimes called “portfolio companies” (“PortCo(s)”).

Private equity fund structure diagram

The components of the firm

As noted above, the PE firm is made up of multiple entities that are structured to efficiently deploy private capital. Below, we’ll detail the responsibilities of each entity and how they interact with the other entities that encompass the larger firm.

The general partner

In many private equity fund structures, the GP entity typically sits on top of the fund, where they direct strategy, fundraise, and oversee the fund’s internal governance. The GP often makes a capital commitment to the fund, also referred to as “skin in the game.” The GP’s capital is usually invested on similar terms as the LPs’ capital (though usually the GP does not pay fees on its commitment), as outlined in the fund’s operating agreement and subscription agreements. In exchange for their services, the GP typically receives an agreed share of the fund’s profits. The GP’s receipt of a profit share is thus dependent on performance of the fund’s investments.

While called the general partner, the GP entity itself is often incorporated as a limited liability company (“LLC”). By assuming this structure, the owners of the GP entity can generally limit their personal liability to their capital contributions to the entity. Certain owners of the GP entity may become managers of the LLC, in addition to (or instead of) being members of the LLC, retaining the above-mentioned control levers over the fund.

The management company

Although the GP entity typically manages the fund, it doesn’t usually oversee the day-to-day investments of the fund. In the typical structure, the GP delegates the management of the fund’s assets—also called its portfolio—to the management company. The aggregate investments in various companies make up the fund’s portfolio, hence why these companies are called “portfolio companies.”

The management company is the operating entity that employs the people who actually deploy the fund’s capital, and manage its portfolio (i.e., the key persons and the investment team). The GP and management company are usually affiliated via shared ownership, with the practical and economic terms of their relationship commonly documented in a management agreement. Due to applicable securities laws, the management company and/or the GP are typically registered or licensed to provide investment management services to the fund.

In consideration for its services, the fund usually pays the management company an agreed fee.

The fund

The private equity fund is the collective investment entity that sits under the GP and management company. The fund is where LPs make their capital commitments, and direct and indirect investments into PortCos are made. Due to regulatory requirements, many funds restrict LP participation to accredited investors, depending on the investment strategy. There are also instances where the fund is required by applicable securities laws to limit LP participation to qualified purchasers and/or qualified clients. The fund is sometimes called a pooled investment vehicle, because the GP and LPs pool their capital to make investments together, as directed by the GP, and managed by the management company.

Funds are often structured as limited partnerships to limit the personal liability of the investing partners but, importantly, the structure also allows the LPs to each take their pro rata share of the gains and losses of the fund on their personal tax return.

Limited partnership agreements (LPA)

The fund entity has its own governing agreement (often called a "limited partnership agreement” or “LPA”), which sets out the rights and obligations of the partners, including procedures for funding, profit sharing, investment guidelines and key decisions. The fund’s LPA also stipulates the percentage of the fund’s profits that the GP will receive (the percentage being more commonly known as “carried interest” or “carry”).

Investment management agreements

The fund also enters into an investment management agreement (an IMA) with the management company that outlines, among other things, how the fund will compensate the manager for its provision of strategic and investment services to the fund. Such compensation fee structure typically includes the management fees that the fund will pay to the manager, as well as reimbursement of expenses incurred in connection with diligencing, managing, and monetizing the fund’s investments in the PortCos.

The portfolio companies

Portfolio companies are the companies in which a PE fund invests. Typically the GP sets the investment strategy, which dictates the types of companies the fund will invest in. The PortCos can be structured in any number of ways, and—up until the time of investment by the fund—are owned and managed separately from the fund.

The PortCos need capital to accelerate growth, so in exchange for the capital invested, a PortCo may give the fund preferential voting rights, distributions, and liquidation payouts.

Why are PE funds structured this way?

Private equity funds follow this structure for many reasons, including: operational flexibility, taxes, limitation of liability, regulatory compliance, and tradition.

Operational flexibility

The structure summarized above is among the most operationally flexible. The partnership structure allows GPs flexibility to accommodate the timing and participation preferences of a varied LP base. It also permits the GP to allocate profit and loss in accordance with varying degrees of participation in the underlying investments; for example, in the event one or more of the LPs require an excuse from one of the fund’s underlying investments.

Taxes

Most GPs, management companies and private equity funds that use the limited partnership structure are not subject to U.S. federal income tax at the entity level. Because the GP, management company and funds are generally structured as pass-through entities, the individual owners take recognized gains and losses on their individual tax returns. Subject to applicable tax laws, certain gains from PortCos held for more than three years may in some cases be taxable at the long-term capital gains rates, rather than ordinary income tax rates.

Private equity funds will often offer certain non-U.S. investors the ability to elect into alternative structures that include “blocker” corporations, intended to prevent non-U.S. investors from being required to file U.S. income tax returns or directly pay income tax on certain flow-through investments in the PortCos, commonly referred to as “ECI” deals. In these cases, the corporation pays the taxes, and the investors’ returns are reduced accordingly.

Limitation of liability

The limited partnership structure also affords passive LPs a liability shield, while still generating the operational and tax flexibility needed to accommodate the complex regulatory and tax positions of the various partners and the fund’s investment strategy. For example, in circumstances where the individual LP’s attributes require more complex structuring, the fund structure might be adjusted to create parallel funds or feeder funds.

Regulatory compliance

Regulatory compliance also informs PE fund structures. Depending on factors including the size of the fund, its investment strategy, and the identity of its investors, the management company and/or the GP may be required to register with the Securities and Exchange Commission, the Commodity Futures Trading Commission and/or other applicable federal, state or non-U.S. regulators. The separation of the fund and portfolio management functions can also help facilitate ongoing compliance with U.S. and non-U.S. regulators across various fund vintages.

Tradition

Last but not least, tradition and course of performance also play an important role in many fund structures. The governing agreements for many of today’s top performing funds have been carefully negotiated and refined across many vintages of funds, going back in some cases to the 1960s and 1970s. Over time, the limited partnership form has become well understood by GPs, LPs, counterparties, regulators and service providers. As the PE market continues to grow and evolve, we expect the limited partnership entity form to remain an important starting point, even as new structures continue to develop.

This article was written in collaboration with Weil, Gotshal & Manges LLP.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). Members of the Private Funds team at Weil, Gotshal & Manges LLP ("WGM") collaborated on this article but the views expressed do not necessarily reflect the views of its Private Funds team or of WGM. This communication is for informational purposes only, and contains general information only. Carta and WGM are not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta and WGM do not assume any liability for reliance on the information provided herein. © 2024 Carta. All rights reserved. Reproduction prohibited.

The contents of this article may contain attorney advertising under the laws of various jurisdictions. Prior results do not guarantee a similar outcome. By using this web site you understand and agree that no information is being provided in the context of any attorney-client relationship and that nothing herein is intended to constitute legal advice. This web site is solely informational in nature, not intended as a substitute for competent legal advice from a licensed and retained attorney in your jurisdiction, and should not be so used. IRS Circular 230 Notice: To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. tax advice contained in this article (including any attachments or images) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.