There are two main types of stock options that startups and other companies may offer as part of their employee compensation packages: incentive stock options (ISO) and non-qualified stock options (NSO). Companies may also offer different equity compensation types, like restricted stock awards (RSA) and restricted stock units (RSU). Each equity type is taxed differently by the Internal Revenue Service (IRS). This article covers everything you need to know about NSOs.

What are non-qualified stock options?

Non-qualified stock options (NSOs) are a type of stock option that grants employees, consultants, advisors, board members, and other service providers the right to purchase company stock at a fixed price, known as the strike price. Unlike incentive stock options (ISOs), NSOs do not qualify for special tax treatment under the Internal Revenue Code (IRC), making them a more flexible but less tax-advantaged form of equity compensation.

Like other types of stock options, NSOs typically follow a vesting schedule, which requires the option holder to remain with the company or meet certain milestones before they can be exercised.

Companies may favor NSOs because they can be granted to employees as well as a broader range of non-employee service providers like consultants and startup advisors. Companies also receive a tax deduction equal to the ordinary income recognized by the option holder at the time of exercise.

While NSOs provide recipients with the potential to financially benefit from the appreciation of company stock, option holders should evaluate their financial situation before exercising their options due to potential immediate tax liabilities upon exercise and potential investment risks if the share price declines.

How are non-qualified stock options taxed?

Taxation is a key difference between NSOs and ISOs. With NSOs, taxes may be owed at exercise and when the shares are sold, whereas ISOs are tax-deferred until sold (other than potential AMT). NSOs do not have the same tax benefits as other types of equity compensation.

→ Learn more about how taxes work for stock options

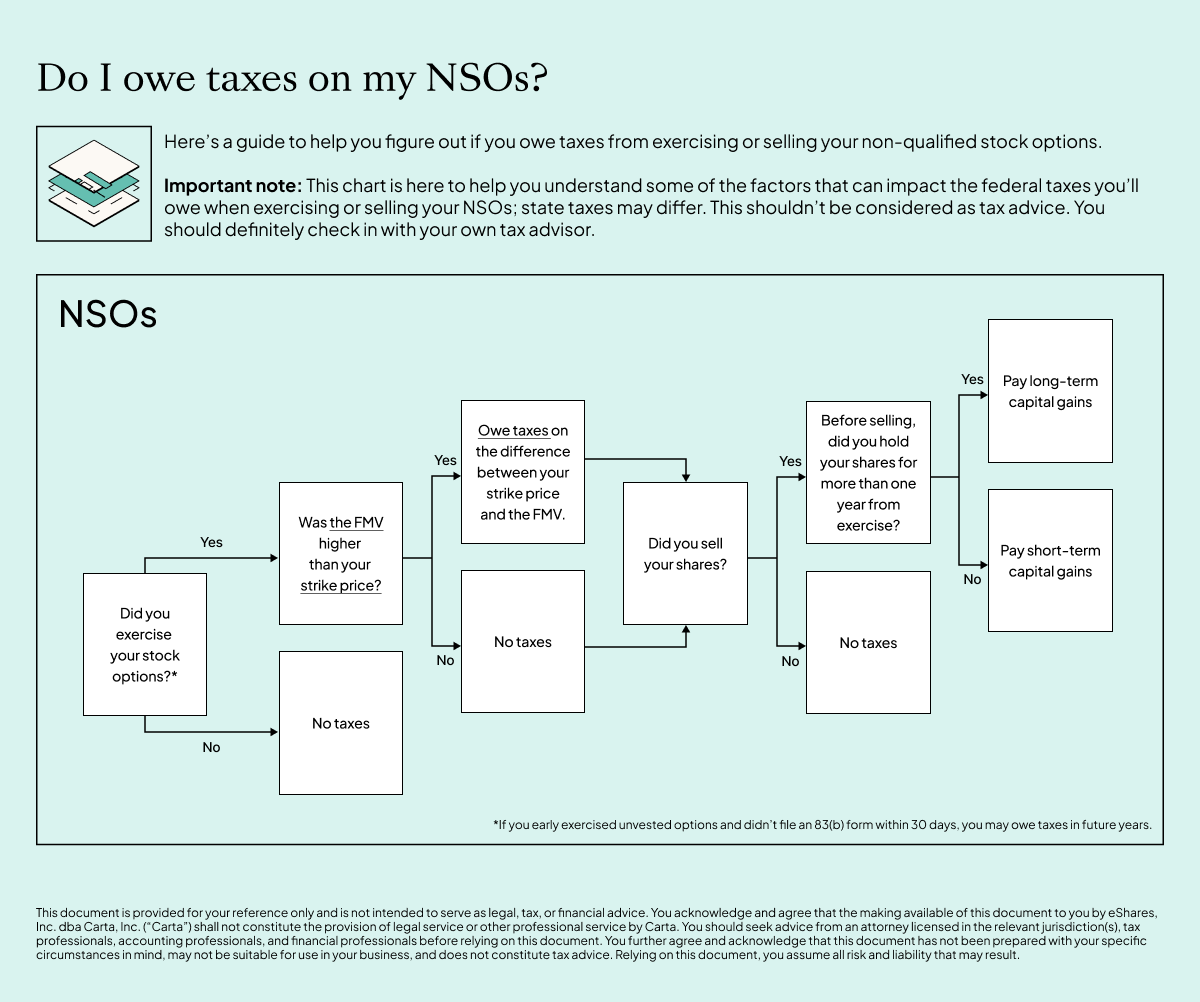

When you exercise

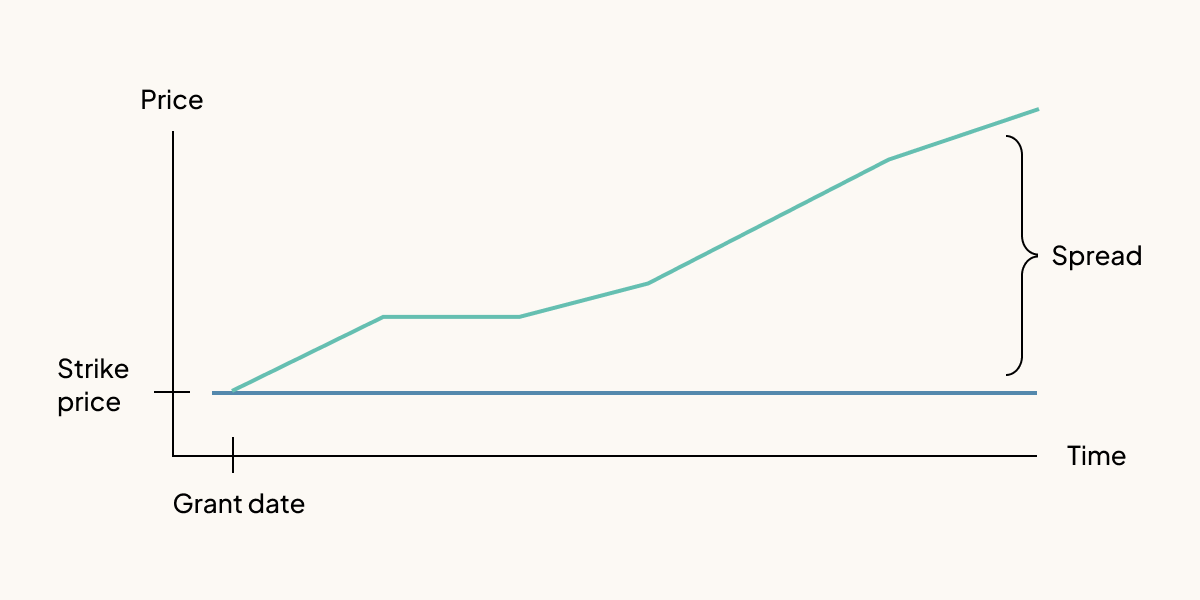

When you exercise your stock options, you’ll be taxed on the difference between your strike price (fixed purchase price) and the current FMV of those stock options. This difference is called the spread.

If you are an employee, your company will usually withhold ordinary income tax (which includes both payroll taxes and regular income taxes) on the spread when you exercise or may require you to pay the withholding tax out of pocket. If you are an independent contractor or other non-employee service provider, you will have to pay any applicable taxes directly to the IRS.

After exercising the NSOs, any additional gain realized from selling the shares is subject to capital gains taxes. If the shares are held for more than one year after exercise, they qualify for the lower long-term capital gains tax rate. If they are sold under one year from exercise, they are taxed as short-term capital gains.

For example, if you exercise 100 vested options at a grant price of $1 and the current value is $2, you’ll owe ordinary income tax on the $100 gain.

When you sell

After you exercise your options, you can either sell right away or hold onto your stock. If you sell right away at the current FMV of the stock, you will not have any capital gain and will only have to pay ordinary income tax on the spread.

If you sell your stock within a year of when you exercised your options, you’ll pay short-term capital gains tax on any increase in value since the exercise date. But if you hold onto your stocks for more than a year and then sell, you would pay long-term capital gains tax, which is typically a lower rate than the short-term capital gains tax rate.

The qualified small business stock exclusion

After you exercise NSOs and hold stock, it may be eligible for the qualified small business stock (QSBS) tax benefit. If you qualify for QSBS, you could potentially sell your stock without owing taxes at sale if you hold your stock for at least five years.

After the five-year holding period, you can potentially exclude up to 100% of capital gains from their federal taxes when you sell the QSBS stock in a liquidity event such as a tender offer, secondary transaction, or initial public offering (IPO).

Action | Tax implication |

You exercise your NSOs into stock | You’ll likely owe ordinary income tax on the difference between your strike price and the current FMV of the stock |

You exercise NSOs and sell your stock in one transaction | You’ll likely pay ordinary income tax on the difference between your strike price and the current FMV of the stock. If your sale price is higher than the company-determined FMV of the common stock, you could owe short term capital gains tax on the difference. |

You sell your stock within a year of exercising your NSOs | You’ll likely pay short-term capital gains taxes on the profit you made selling your options |

You sell your stock after holding it for over a year after exercising your NSOs | You’ll likely pay long-term capital gains taxes on the profit you made selling your options |

You sell your stock after holding it for over five years after exercising NSOs | You may be eligible for the QSBS exclusion and could potentially owe zero federal capital gains taxes on the profit you made when you sell (up to a $10M cap and depending on your company’s QSBS status at the time you exercised your option) |

When can I exercise non-qualified stock options?

Typically, you gain the ability to exercise your stock options on a set schedule as you work for a company over time. This is called vesting. You can exercise your NSOs as soon as they vest, but you can also choose not to exercise.

If you choose to exercise, you can either pay the strike price in cash or, if your company allows it, sell a portion of your shares to cover the cost of exercise, referred to as a cashless exercise. Check to see if your company allows cashless exercises.

If you leave your company, you’ll usually have a certain period of time—the post-termination exercise period (PTEP)—to exercise your vested NSOs. If you don’t exercise your options before this period ends, you’ll lose your opportunity to purchase them.

To maximize your potential profit after taxes, talk to a tax advisor before exercising and selling your non-qualified stock options. While advisors can’t predict your company’s future stock performance, they can help you understand your next steps and minimize your tax liability.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2026 Carta. All rights reserved. Reproduction prohibited.