- Carta Policy Insights: Decoding the Data | Startup job creation

- Startup job growth has been net positive in almost every state over the past year

- Despite dips, startups recover and consistently drive job growth

- Early-stage startups contribute significantly to job growth

- Unicorns are few in number but important job creators

- Policy as infrastructure

- Policy recommendations:

Startups and growth businesses consistently drive job creation in the U.S. economy. Startups, particularly companies less than five years old, have shown a net job creation rate of 15-20% annually over the last 40 years, much higher than the 0% or negative rates often seen with more mature companies. From traditional startup hubs like Silicon Valley to emerging entrepreneurial ecosystems across the country, these ventures are fueling employment opportunities, reshaping the American economy, and leading to our competitive edge.

To sustain and expand the important role of startups in driving job creation, pro-entrepreneurship policies are required that will drive capital and talent into the ecosystem and make it easier for founders and the funds that back them to raise capital.

Here is a closer look at the data that supports new policies favorable to the entrepreneurship economy.

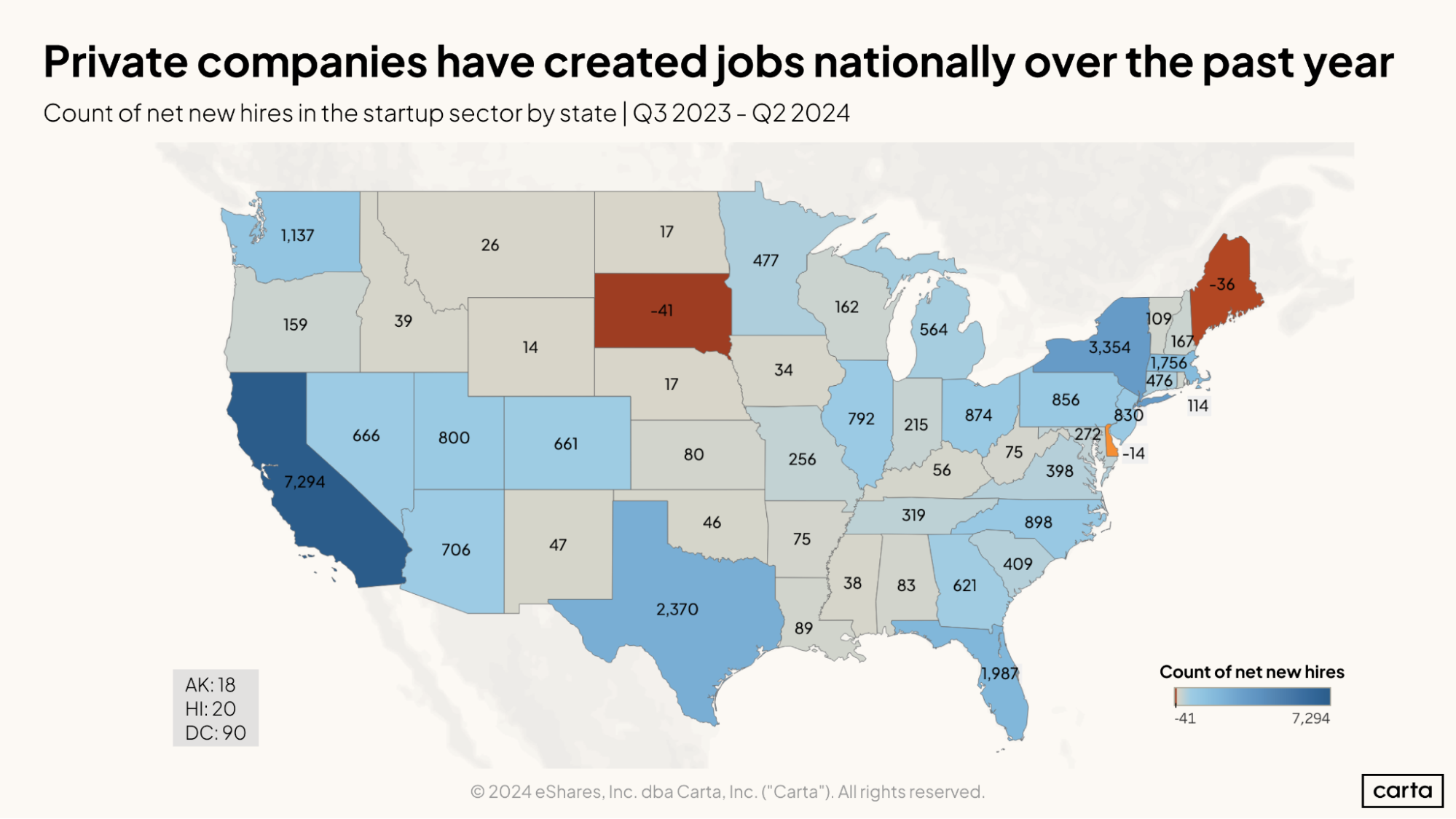

Startup job growth has been net positive in almost every state over the past year

Growth-stage companies have driven job creation across the country, and have been net new job creators in all but three states, as Carta data reveals (Q3 2023 to Q2 2024).

Concentration in established markets: Job creation is still concentrated in traditional startup hubs. While policy has helped to expand startup growth beyond the traditional hubs of California and New York, there is still work to be done.

Positive net new growth: Startups and growth-stage businesses continue to deliver job growth, creating economic opportunity wherever they are located.

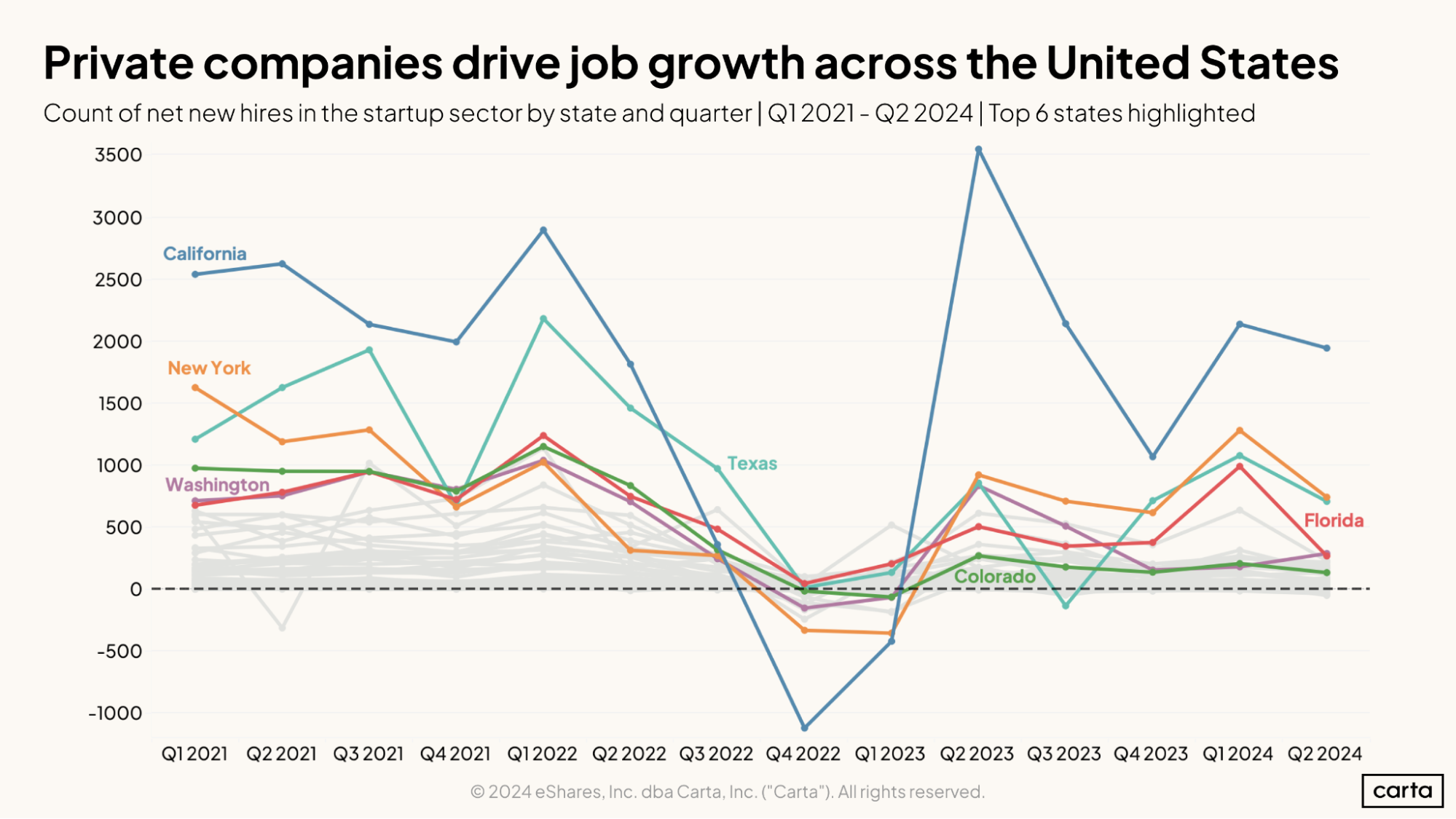

Despite dips, startups recover and consistently drive job growth

This chart highlights the net new hires in the startup industry across six key U.S. states—California, Texas, New York, Washington, Florida, and Colorado—from Q1 2021 to Q2 2024. These states created the most startup jobs over that time period.

Resiliency: Despite downswings, especially in late 2022 and early 2023, the overall trend remains positive for most U.S. states. This resilience is evident in the quick recoveries following downturns.

California as an example: As the leading state, California exemplifies this pattern. California drives job creation; in a market downturn, it slows, but rebounds to prior levels, hitting its highest peak in Q2 2023.

Long-term trend: Despite short-term volatility, the long-term trend for all states remains net-positive.

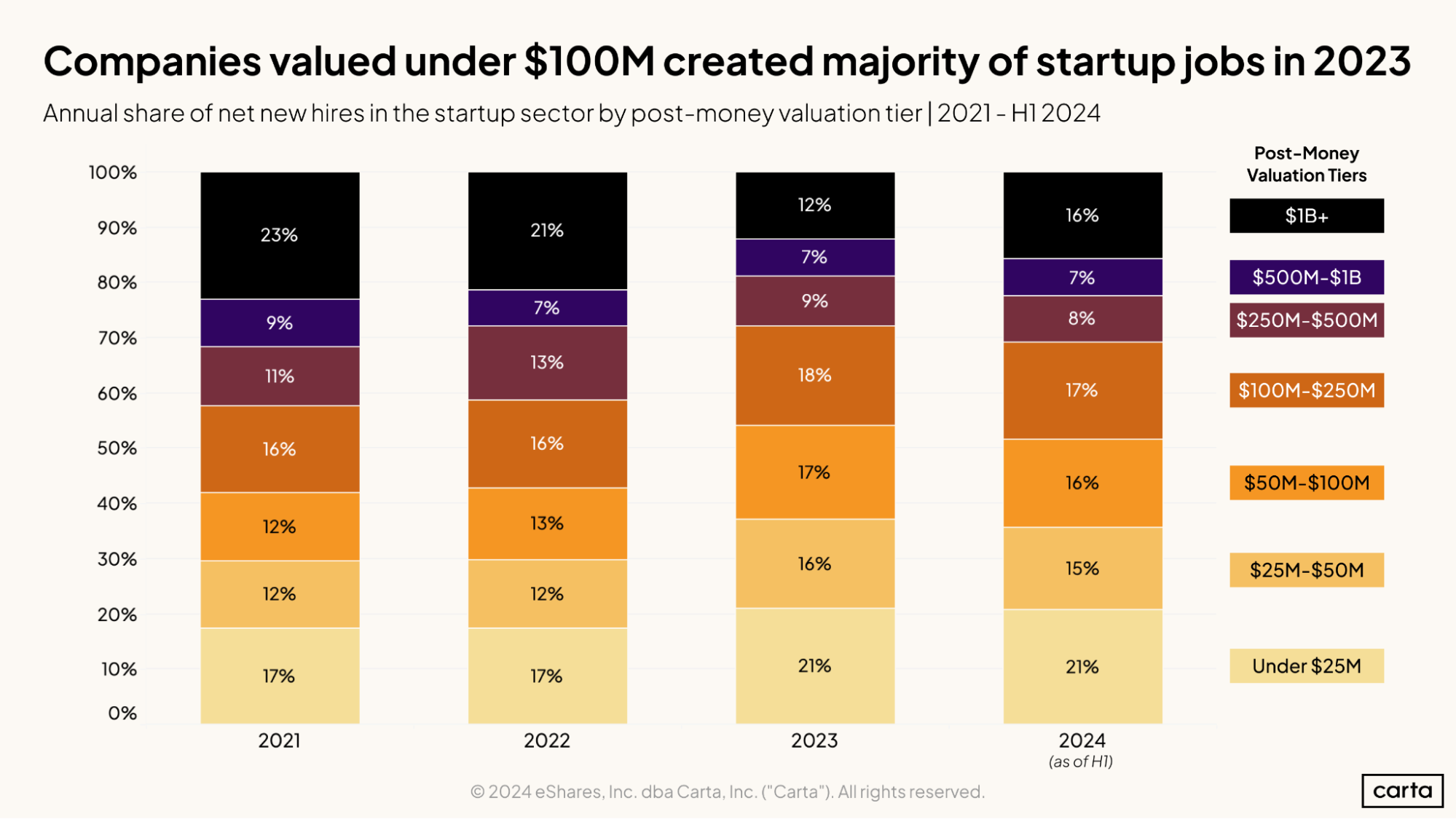

Early-stage startups contribute significantly to job growth

This chart looks at how much companies at different stages of growth in terms of valuation contribute to job creation.

Diverse job creation across valuation tiers: Startups across all valuation tiers contribute to job creation, from those valued under $25M to those over $1B. This diversity indicates a robust startup ecosystem that generates employment at various stages of company growth.

Large role of smaller startups in job creation: While jobs are generated at various stages of company growth, early-stage startups play a significant role in driving employment growth. In 2023, companies valued under $100M (the bottom three tiers) accounted for 54% of new hires in the startup sector.

Shift towards earlier-stage startups: There's a noticeable trend of increasing job creation share among earlier-stage startups valued under $25M, rising from 17% in 2021-2022 to 21% in 2023-2024, further revealing a growing importance of very early-stage startups in the job market.

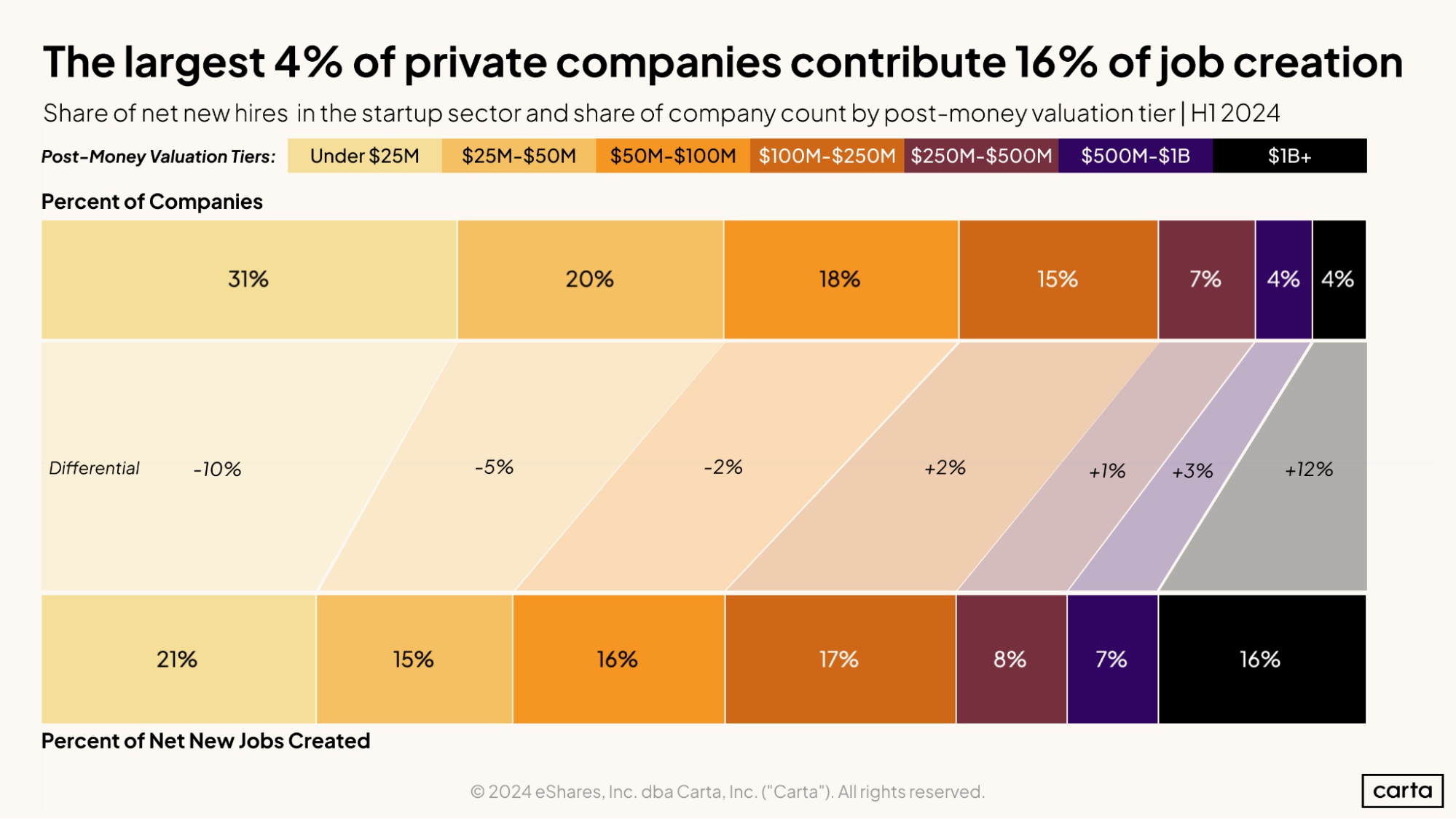

Unicorns are few in number but important job creators

This chart compares the distribution of the different valuation tiers by percent of companies vs. percent of jobs created, looking at data from H1 2024.

Share of companies across tiers: While smaller companies create more jobs in aggregate, it is important to note that there are more of them. 31% of companies fall into the under $25M valuation tier, while only 4% fall into the $1B+ tier.

Late-stage contribution to job creation: The 4% of companies in the unicorn category as of H1 2024 were responsible for 16% of net new hires. This shows that larger companies create more jobs per company.

Policy as infrastructure

The data shows that startups drive job growth. The Carta Policy team pushes for policies that will continue this trend—and expand it further outside the traditional startup hubs of California and New York.

Policy recommendations:

Adopt tax policies that incentivize investment in the startup ecosystem. Carta supports policies to bolster and expand tax incentives that drive investment to the startup and growth-stage business ecosystem, such as the QSBS exclusion and R&D credit. These policies incentivize investment in startups, encourage long-term investment in early-stage growth companies, and help small businesses attract and retain talented employees.

Expand access to capital. Carta supports reducing friction in the capital-raising process and making it easier for emerging fund managers to raise and deploy capital to more entrepreneurs across the country. This can be achieved by increasing onramps to become an accredited investor and expanding what is considered a qualifying investment for venture capital. Doing so will help improve capital formation opportunities, particularly for diverse and traditionally underrepresented entrepreneurs and investors outside of traditional capital-raising hubs.