- 2025 Policy Outlook: Implications for the private capital ecosystem

- I. Governing dynamics

- Congress

- Administration

- Judicial Branch

- II. Tax reform

- Process and dynamics

- Provisions to watch: Innovation economy

- Innovator Alliance

- III. Capital markets

- Congressional efforts

- SEC

- IV. Crypto, AI, and tech policy

- Crypto and digital assets

- Artificial intelligence

- Antitrust and competition

- China

- Engagement

- Sign up below to receive Carta’s Policy Weekly Brief:

Republicans have officially assumed unified control in Washington with an ambitious agenda and major policy shift from the previous administration, particularly as it pertains to private capital. Here’s what to expect from Congress and the new administration in 2025 and how the policy agenda will impact the innovation ecosystem—private equity, venture capital, and the startups and small businesses they support.

I. Governing dynamics

House dynamics

Senate dynamics

Congress

Republican control in the House and Senate will allow President Trump to more easily implement his agenda and advance his cabinet picks and other key hires. Regulators will also face less scrutiny from a sympathetic Congress.

Even with unified control, legislating will not be easy. Slim margins and intra-party dynamics will require bipartisan support to advance most policy initiatives. The exception: tax reform. Unified control unlocks the reconciliation process, which only requires a simple majority vote for tax and spending bills.

House dynamics: Republicans maintained control of the House with a slim majority of 220-215 (currently 218-215, with vacancies). Narrow margins mean every member is empowered and has negotiating power, making unifying a diverse conference challenging. These dynamics have caused Speaker Mike Johnson to partner with Democrats in the past to advance legislation, which has been a source of controversy from the conservative House Freedom Caucus. Trump in the White House may help this dynamic, but expect governing challenges to continue.

Senate dynamics: Republicans have a 53-47 majority in the Senate and new leadership as Majority Leader John Thune succeeds longtime leader Sen. Mitch McConnell. Republicans do not have a filibuster-proof majority, so bipartisan support is necessary for any legislation to clear the chamber’s 60-vote threshold. However, the Senate only needs a simple majority to advance tax and spending bills under the reconciliation process as well as approve nominations, including to the federal bench and to agency positions. Nominations will dominate much of the calendar over the first few months. With a three-seat margin, most of Trump’s personnel picks will likely be confirmed.

Administration

Much of the administration’s policy agenda will be driven through executive orders and rulemaking initiatives. On his first day in office, Trump set in motion efforts to reshape federal agencies by pausing implementation of all rules that have not taken effect and freezing federal hiring.

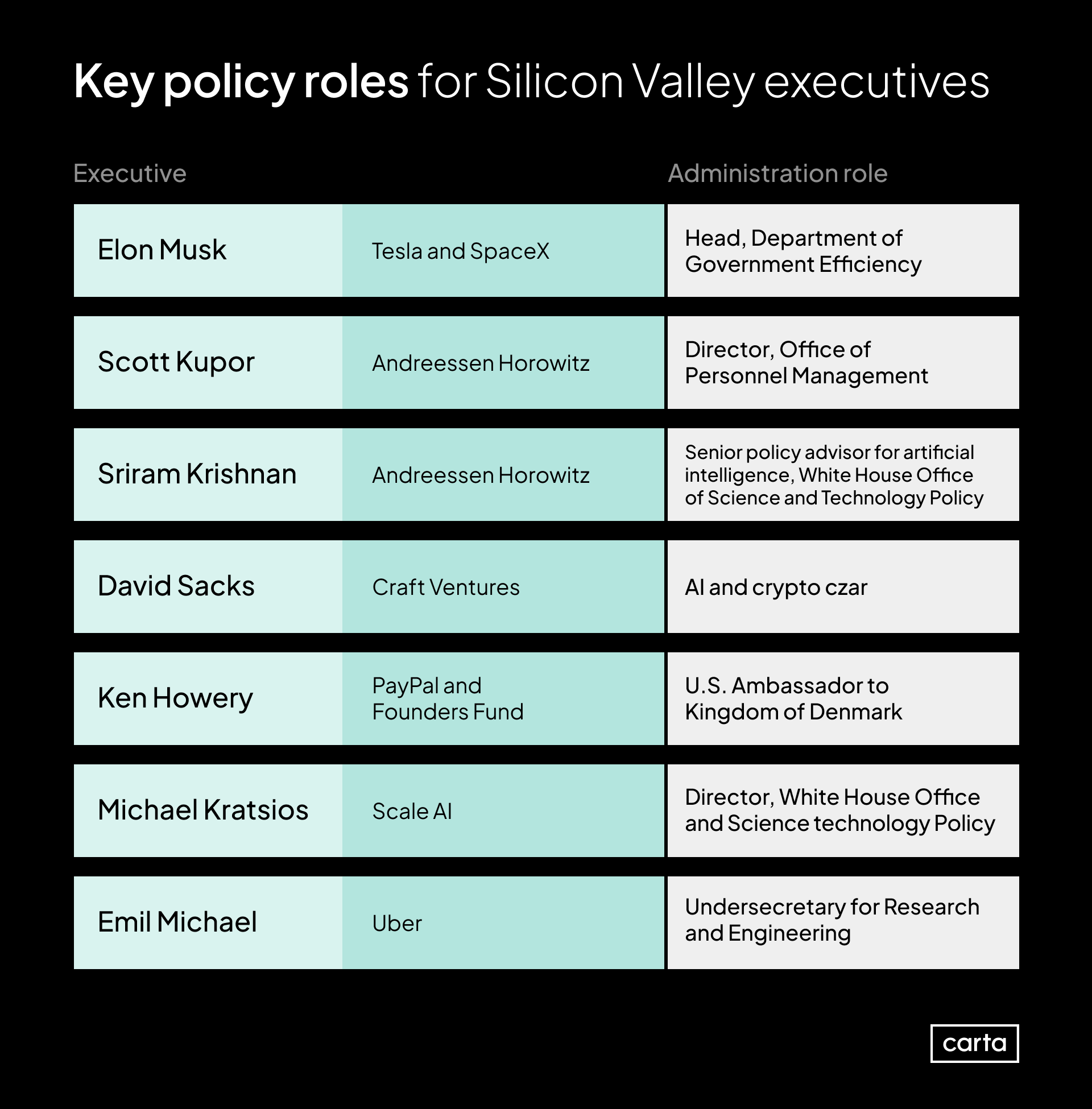

Silicon Valley will have an outsized role in shaping policy in the new administration. Tesla and SpaceX founder Elon Musk, a top donor and vocal Trump supporter, has become one of the president’s closest advisors. Musk will also head the Department of Government Efficiency (DOGE), which will be tasked with developing efficiencies, cutting costs, and reducing red tape across the federal bureaucracy. Trump also appointed David Sacks, founder of Craft Ventures, as the crypto and AI czar, in addition to a host of other VC executives in prominent roles that will influence policy development.

Judicial Branch

The Supreme Court has weakened agency authority, revoking the longstanding Chevron doctrine, which granted deference to agency interpretation of rules within their jurisdiction. Now questions of ambiguity will increasingly be resolved by courts. This will accelerate the recent trend where stakeholders challenge administrative rules. Under Biden, the business community successfully challenged a number of Biden administration rules in conservative-leaning jurisdictions, including the SEC’s private fund adviser rule. But now that litigation is the norm, Democrats could pursue a similar strategy—likely in more liberal jurisdictions. This could undermine or delay agency rulemakings and actions. And we’ve already seen legal challenges to DOGE and immigration-related actions.

Below is a deeper dive on policy initiatives that will impact the private capital ecosystem:

II. Tax reform

Reconciliation strategy

Price tag and pay-fors

Individual, corporate, and capital gains rates

Carried interest

QSBS

R&D expensing

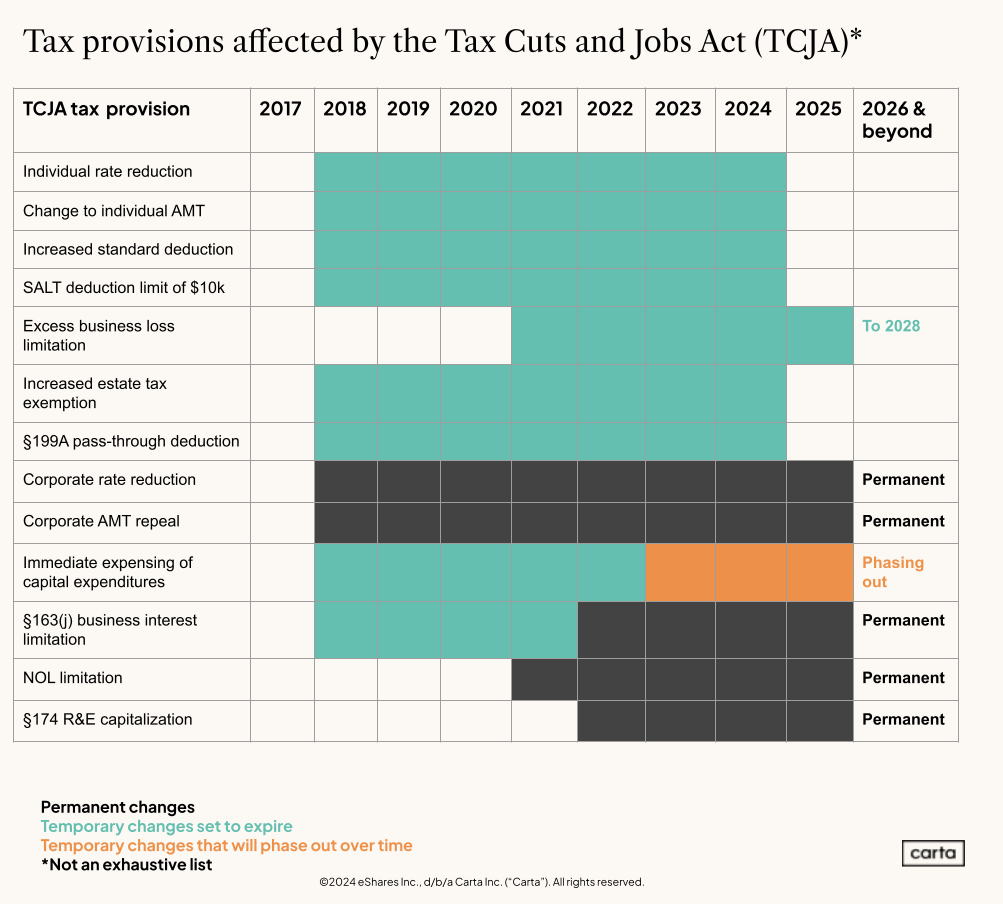

Tax policy will be a key focus in Congress in 2025 as key elements of the Tax Cuts and Jobs Act (TCJA) are set to expire. TCJA aimed to drive investment and economic growth by simplifying and lowering taxes for individuals while reducing the corporate rate and revamping how international corporations are taxed. However, only some of TCJA’s provisions were made permanent; the bulk of the changes will revert to pre-TCJA levels in 2026, and these changes will disproportionately impact individuals and small businesses. If Congress does not act, over $4.5 trillion in tax increases would take effect in 2026, impacting over 60% of U.S. households. Both parties have a vested interest in preventing this from happening.

Process and dynamics

Speaker Johnson has set a target date of April to pass tax reform as part of a more comprehensive bill that would also include energy and immigration priorities. This is an extremely ambitious timeline, and House and Senate leadership have yet to agree on strategy.

Reconciliation strategy: Republicans plan to use reconciliation to advance tax reform as well as other priorities like border security and energy. The debate is whether these provisions move as one comprehensive bill or in two vehicles. Either way, one complicating factor will be paying for tax reform.

Price tag and pay-fors: The Congressional Budget Office announced that extending the TCJA as-is would decrease revenue by more than $4 trillion. This does not even reflect adding other priorities such as raising SALT caps or the “no tax on tips” idea. Although it is unlikely tax reform will lower the deficit (or break even), policymakers will want to offset some of the lost revenue: A wide-ranging list of potential offsets have been floated, including repealing clean energy tax incentives under the Inflation Reduction Act, raising tariffs, and even raising the corporate rate. Given the price tag and governing challenges, the ultimate tax reform result is likely to be narrow.

Provisions to watch: Innovation economy

The looming tax debate will center on the TCJA, but negotiations will put the entire tax code on the table—including issues affecting startups, growth-stage companies, and investors in the innovation ecosystem.

Individual, corporate, and capital gains rates: The TCJA made substantial changes to how individuals are taxed—it lowered the top tax rates, capped popular itemized deductions (SALT and mortgage interest) in exchange for an increased standard deduction, and increased the estate and gift-tax exemptions. Unless Congress acts, these changes will revert to pre-TCJA levels. TCJA also permanently lowered the corporate tax rate from 35% to 21%, and while it is not set to expire, there is ongoing debate as to whether to lower it further or increase it to pay for other priorities.

Prediction |

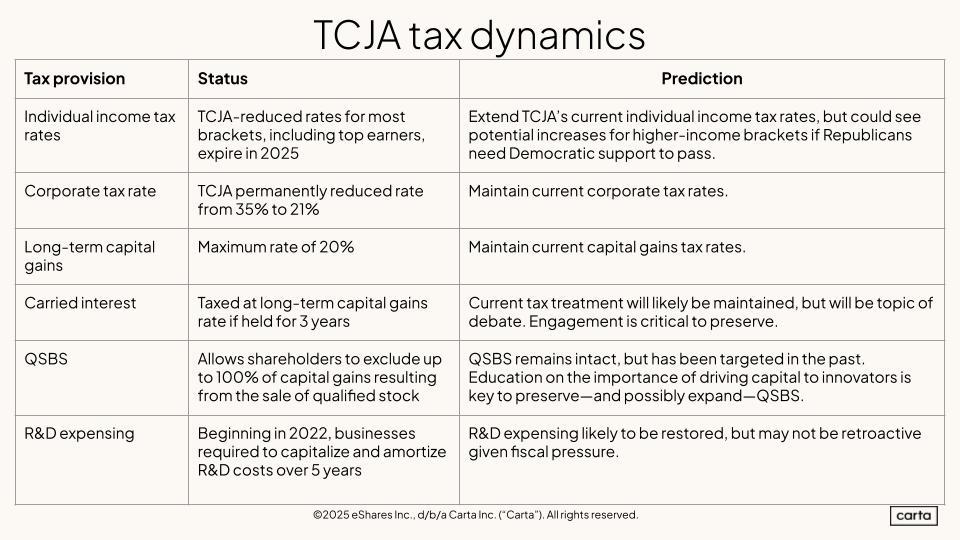

We expect Congress will extend the TCJA’s current individual income tax rates; however, if Republicans have to rely on Democrats to pass a tax bill (this is not the plan, but may happen given the slim majority), there is a chance higher-income brackets ($1M+) could see a slight increase on income and/or capital gains tax rates. The corporate rate will likely remain at its current level. |

Carried interest: Carried interest is the share of a private fund’s investment profits that a fund manager receives as compensation. Because carry is derived from investment returns, it is currently taxed at the long-term capital gains rate rather than as ordinary income. This encourages investment in private markets by supporting the fund economics—particularly for smaller and emerging fund managers.

The dynamic: Carried interest tax treatment is in a decent position. But fund managers need to stay engaged: Even though cutting carried interest only raises $6.5B, expect critics to target the treatment as an unfair break for wealthy fund managers and seek to drive a wedge between the populist factions of the Republican party and the elites who benefit from such treatment.

Prediction |

Despite the pressure, carried interest likely remains intact. |

Qualified small business stock (QSBS): Section 1202 of the tax code exempts shareholders—investors, founders, and employee-owners—from capital gains tax on proceeds from qualified small business stock (QSBS) if they have held the eligible stock for at least five years. This incentive helps drive capital and talent to startups and growth-stage companies.

The dynamic: Democrats sought to curtail the benefit in 2021 to pay for other spending priorities, as they viewed the provision as an unnecessary benefit for wealthy investors. We are playing offense—pushing to expand QSBS—even if only to secure the current treatment, but QSBS could be another issue targeted by progressives and populists.

Prediction |

QSBS remains intact. |

R&D expensing: Section 174 incentivizes innovation by allowing businesses to recoup some of the costs of developing new products and services. This provision previously allowed companies to immediately expense research and development (R&D) costs in the year they were incurred. In 2022, that changed: Now companies are required to capitalize those costs and amortize them over five years for domestic research and 15 years for international.

The dynamic: Both parties support restoring R&D expensing, and it will likely be restored as part of the tax package.

Prediction |

Gets fixed, but given the spending pressure it is unlikely to apply on a retroactive basis. |

Innovator Alliance

None of these predictions—which are largely positive—come true without engagement. Carta wants to advance tax policy that bolsters private capital and incentivizes investment in startups, small business, and growth-stage businesses. Carta and our coalition partners have launched the Innovator Alliance to help shape tax policy that drives more capital, talent, and investment to the innovation ecosystem. We have already been engaging with Congress and the new administration on our priorities, but the work is just beginning. Contact us to get involved.

Innovator Alliance: Learn moreIII. Capital markets

Key policy initiatives

Access to capital, access to investment and ownership opportunities

Agenda:

Access to private markets, private fund initiatives, path to IPO

The new government is likely to increase its focus on capital formation initiatives and expanding investment opportunities. Much of the work can be accomplished at the SEC, where we expect the agency to devote more attention to bolstering capital formation under new leadership. But there are also opportunities for policymakers to enact bipartisan solutions to drive more capital to the innovation ecosystem and make private markets more accessible.

Congressional efforts

In Congress, capital markets policy is primarily driven by the House Financial Services Committee (HFSC) and Senate Banking Committee (SBC). In the House, Chairman French Hill, a former community banker and Treasury official, will serve alongside Ranking Member Maxine Waters. In the Senate, Sen. Tim Scott will have the SBC gavel, while Sen. Elizabeth Warren has been elevated to serve as the lead Democrat following former Sen. Sherrod Brown’s defeat in the last election.

Chairmen Hill and Scott have designated capital formation as a key focus of their agendas, and have called for a regulatory framework that fosters innovation. Both committees will likely pick up capital formation efforts from the last Congress, including Scott’s Empowering Main Street in America Act, designed to expand access to capital for small businesses and funds, increase investment opportunities, and ease the transition for companies to go public if it fits their business model.

Key private market policy initiatives

Expanding access to capital. Policymakers will focus on making it easier for companies and funds to raise capital outside of traditional funding networks. This includes:

Increasing size and investor limitations for qualifying venture capital funds to help emerging fund managers reach more investors with smaller check sizes.

Expanding the scope of VC qualifying investments to include secondaries and fund-of-fund investments to help drive capital to emerging ecosystems and increase liquidity.

Expanding the ability for companies and funds to use crowdfunding to reach more investors.

Promoting access to investment and ownership opportunities. Today, most individuals are generally prohibited from participating in private markets because of the wealth-based accreditation standard. Expanding private market investment opportunities while preserving important investor protections will not only drive innovation, but will also help broaden economic opportunity. Efforts include:

Modernizing the accredited investor standard to reflect financial sophistication, including through testing.

Permitting structured access to private fund investments through professionally managed fund vehicles and investment professionals.

Expanding access to private market investments through retirement vehicles.

Industry will need to engage to ensure capital formation remains a top priority rather than getting crowded out by competing priorities, such as developing a framework for digital assets, easing burdens on community banks, and housing finance reform.

Prospects |

A comprehensive capital formation package is more likely with Republican control in both the House and Senate, but any ultimate legislation will need bipartisan support to advance with the 60-vote threshold in the Senate. Both parties support entrepreneurship and capital formation, but diverge on the means to that end and the policy trade-offs to accomplish it. Reforms are likely to be more narrowly crafted rather than comprehensive, but that still provides an opportunity to expand investor access to private markets and bolster fund managers. |

SEC

The SEC will drive many of the private market reforms, and under the second Trump administration, we will see a sharp policy pivot both on rulemaking and enforcement. President Trump has nominated former SEC Commissioner Paul Atkins to replace former Chair Gary Gensler and lead the agency. Atkins is expected to be confirmed before Easter recess, but efforts to implement a new agenda are already underway. Acting Chair Mark Uyeda has already launched a new crypto task force headed by Commissioner Hester Peirce.

Atkins supports efforts to reduce regulatory burdens and foster capital markets innovation. Much of the focus will be on rolling back enforcement and other initiatives put in place under Gensler. Under Atkins, the SEC will likely prioritize combatting retail investor harm over large-scale compliance sweeps and impose sanctions based on individual accountability rather than hefty corporate penalties.

On the policy front, a major focus of the Commission will be developing a regulatory framework for digital assets alongside Congress and other regulators (more below), but we also expect more emphasis on capital formation. Much of the work will be focused on making it more attractive for companies to go public. There will be opportunities to drive private market policy, but it will be incumbent on the ecosystem to engage and help drive these efforts to make private capital a priority.

Investor access to private markets. Atkins will likely work to permit retail investors to participate in private markets through appropriately structured fund vehicles, including retirement vehicles. This includes removing the staff-imposed 15% cap on closed-end fund investments in private funds and working with the Department of Labor (DOL) to clarify the ability for 401(k) funds to offer exposure to private equity and other alternative assets. Given the bipartisan support in Congress, the agency is also expected to look at expanding accredited investor accreditation through tests to demonstrate financial sophistication or the use of investment professionals to access private market opportunities.

Private fund initiatives. The private fund adviser rules were rolled back by the court and proposals from the Gensler era are not likely to move forward. But given the growth of private capital, do not expect scrutiny to completely go away. New anti-money-laundering requirements for venture capital and private equity fund advisers will be coming online, which the SEC will be responsible for enforcing, in addition to existing obligations like the Marketing Rule. We are not expecting these rules to be rescinded or reversed, but there will be more opportunity to work with the agency to shape problematic aspects or streamline compliance.

Path to IPO. Atkins is expected to streamline the IPO process and examine some of the regulatory costs and other factors (short-termism, activist shareholders) that make public markets less attractive for companies. Atkins is also a proponent of a materiality-based disclosure framework, so ESG and other disclosure regimes put in place under Gensler will likely be reevaluated or rolled back.

Like Congress, engagement will be key to ensure capital formation remains top of mind at the SEC. The agency will also have to grapple with the Supreme Court’s rollback of the Chevron doctrine, which will limit the SEC’s ability to fill in regulatory gaps and address novel challenges without explicit congressional authority. This means the rulemaking process may take longer to examine and justify authority and will require greater coordination with Congress if additional authorities are needed.

IV. Crypto, AI, and tech policy

Congress, the administration, the SEC

Congress, state efforts

Federal Trade Commission, Department of Justice, M&A activity

A major focus of the new administration and the Republican Congress will be the development of a regulatory framework for digital assets as well as artificial intelligence. The Trump administration will likely take a more permissive posture, allowing the technology to drive the regulatory framework instead of imposing a regulatory framework to drive the development of technology.

Crypto and digital assets

Crypto played a major role in the 2024 election, and pro-crypto initiatives will be a key part of the financial services policy agenda in 2025.

Congress: Developing a regulatory framework for digital assets and stablecoins is a key priority as multi-committee, bicameral workstreams are already taking shape. The House’s FIT21 framework, which passed the House with the support of over 70 Democrats (including party leaders), will likely be the starting point. Congress will engage closely with the SEC, the Commodity Futures Trading Commission (CFTC), and the White House.

Administration: President Trump signed an executive order on digital assets that establishes a Presidential Working Group to identify all regulations and guidance that should be rescinded or modified; propose a federal regulatory framework for digital assets, including stablecoins; and evaluate the creation of a national digital asset stockpile. Crypto czar David Sacks will lead this effort alongside Treasury, the SEC, and other relevant agencies.

The SEC, which was viewed as hostile to the industry under former Chair Gensler, is expected to take a more collaborative posture toward working with the crypto industry, Congress, and agencies like the CFTC to provide clarity and develop a comprehensive framework to regulate digital assets. New SEC leadership has already rescinded controversial accounting guidance that prevented banks from custodying crypto assets. The agency is also expected to reverse course on the aggressive enforcement posture taken by Gensler, and ongoing litigation for non-fraud claims may be dismissed.

Artificial intelligence

The Trump administration will likely take on a more pro-business approach to AI, prioritizing innovation, economic dominance, and competition with global adversaries like China. In one of his first official actions, President Trump revoked President Biden’s wide-ranging executive order on AI, immediately halting the implementation of safety and transparency requirements for AI developers. Trump has tasked Sacks and others to develop an AI Action Plan over the next six months geared toward sustaining and enhancing U.S. dominance. Republicans have favored a light-touch regulatory approach to emerging technologies, encouraging the private sector to develop AI technologies with minimal regulatory constraints. Regulators are likely to look at the use of AI technologies rather than attempting to regulate the development of the technology itself.

Congress: AI policy remains a relatively bipartisan pocket on Capitol Hill. A host of bipartisan AI task forces and working groups emerged last session, with many expected to reemerge this year. While discussions of AI-related issues in national security and disinformation have proven contentious, measures that support AI research and workforce training programs should advance. A web of committees share jurisdiction over AI policy, however, which can further complicate legislating.

State efforts: In the absence of broad federal action, states will continue to step in and fill the void. To date, at least 45 states have introduced AI legislation and continue to push forward to fill the gaps at the federal level. Colorado led the way, enacting legislation that regulates the private sector’s use of AI in decision-making processes and implements discrimination protections for consumers when AI is used for “consequential” decisions by requiring companies deploying these types of high-risk AI systems to create a notification and risk-management regime. A growing patchwork of state AI laws could prompt action at the federal level to preempt state policies that could disadvantage U.S. AI competitiveness.

Antitrust and competition

Federal antitrust agencies—the Federal Trade Commission (FTC) and the Department of Justice (DOJ) —will likely scale back the aggressive merger enforcement and novel theories of harm that the Biden administration pursued. Much of the scrutiny directed toward the private equity industry is likely to go away, and agencies are expected to constructively engage with merging parties to remedy potentially anticompetitive mergers, rather than blocking transactions. A more accommodative antitrust posture and less scrutiny around horizontal and vertical reviews that have started to impact private equity roll-ups and acquisitions could support M&A activity, which could help on company exits.

But do not assume competition policy reverts back to the hands-off approach that existed in pre-Biden days. Both parties have embraced a more expansive antitrust enforcement framework (including Vice President J.D. Vance), particularly as it pertains to Big Tech, and those efforts are likely to continue. Big Tech has worked hard to ingratiate itself to President Trump, but many policymakers may still be skeptical of these companies and see antitrust as a lever to hold them accountable. Regardless of federal action, states—particularly states with Democratic leadership—will likely step in to fill gaps in a more accommodative federal antitrust posture. We are seeing this already with respect to private equity involvement in healthcare, where Massachusetts recently enacted legislation granting the state greater authority to scrutinize and review PE investments in healthcare providers.

China

Policymakers will remain focused on bolstering U.S. competition and protecting against national security, economic, and technological threats posed by China. Beyond the Tik-Tok ban, Congress and the administration will grapple with a number of China-related issues that will impact the innovation economy, including implementing an outbound investment screening regime for investments in Chinese companies in technology sectors that may impact national security. These new rules will introduce compliance obligations and potential divestment risk for venture capital and private equity funds. While China competition is a rare area of bipartisan agreement, policymakers diverge on approach and emphasis. President Trump has maintained the outbound investment rules, but directed the Treasury Department to ensure they sufficiently address national security threats, opening the door that they could be strengthened.

Engagement

There is an opportunity to shape and drive policy that incentivizes investment in startups and growth-stage businesses through the tax code, expands access to capital for these companies and their investors, and creates more opportunities for everyday investors to participate in and benefit from the private markets. Engagement will be key to ensure that private capital remains a priority for Congress and the new administration, and that regulatory frameworks are appropriately tailored to foster the development of new technologies and maintain America’s competitive edge.

Carta has been and will continue to work with policymakers on a bipartisan basis to advance these initiatives to bolster the private capital ecosystem.

Sign up below to receive Carta’s Policy Weekly Brief:

For timely updates on how public policy is shaping the private markets, sign up for the Carta Policy Team's weekly newsletter.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.