Venture capital firms invested heavily in SaaS over the past decade, with annual investment growing more than 6x from 2011 to 2021. But 2022 was a sobering about-face. Valuations plummeted in what Janelle Teng, vice president of Bessemer Venture Partners, described as a “SaaSacre.” The result? VC firms pulled back hard.

Initial data on Q1 2023 investment totals will be available soon. For now, here’s the state of play for SaaS investments:

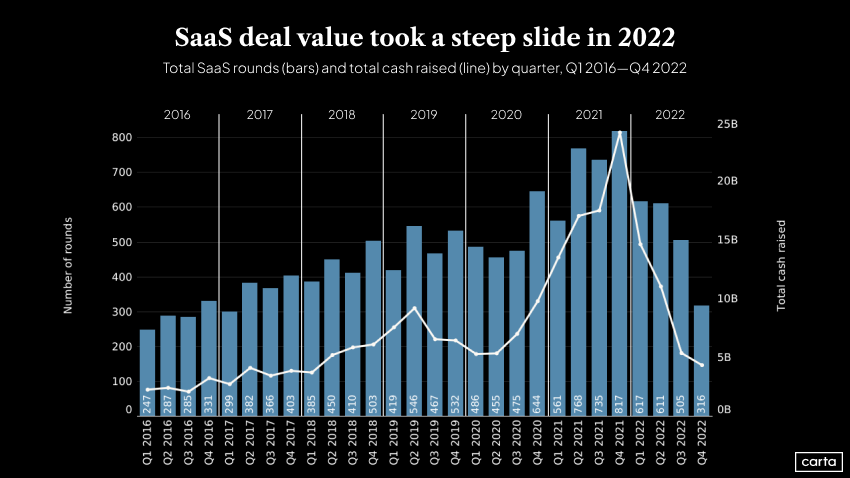

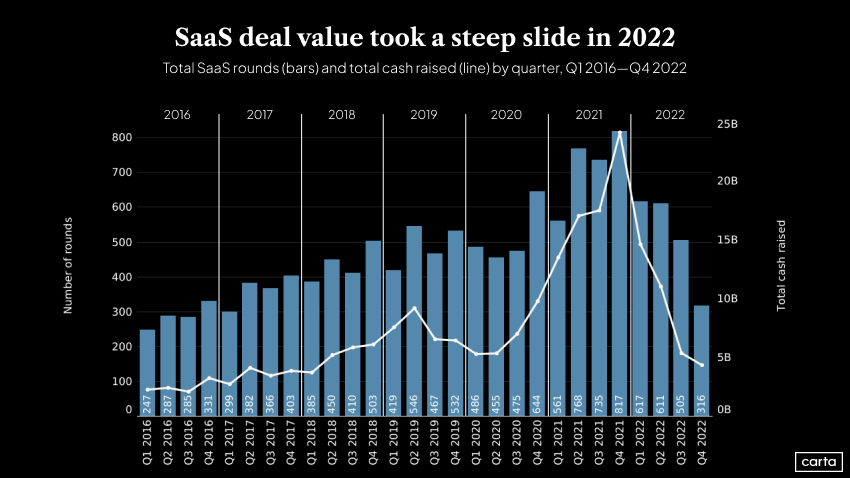

In Q4 2022, investors logged 316 deals and invested $4.3 billion in SaaS deals on the Carta platform—an 82% year-over-year drop in capital invested and a 61% YoY drop in deal count for the sector.

It was the fourth consecutive quarterly decline in total rounds and capital invested for SaaS companies on Carta.

For most of 2022, seed deals in SaaS companies remained relatively steady. But in Q4, investors logged just 130 rounds and invested some $381 million, compared to 230 rounds that totaled $771.5 million in the previous quarter—declines of 43% and 51%, respectively.

Some positive news: SaaS valuations have not shifted dramatically at the earliest stages of the VC investment cycle. The average pre-money valuation for a seed SaaS deal in Q4 2022 was $13 million, down just $1 million (-7.7%) YoY.

Rising interest rates, expensive growth to blame for SaaS slowdown

When capital was cheap and abundant in 2020 and 2021 due to historically low interest rates, SaaS startups went on hiring sprees and raced to grow annual recurring revenue (ARR), a key metric used by investors to determine software company valuations. Achieving profitability and controlling cash burn were second-order concerns as long as valuations and round sizes marched steadily up and to the right. According to Bessemer’s Janelle Teng, only 22% of SaaS companies that went public during the peak of the SaaS investment frenzy in 2021 were already profitable.

Now the trends have reversed: The Federal Reserve raised interest rates repeatedly in 2022, prompting many SaaS companies to retrain their focus on reducing cash burn to stave off the need for another round of equity financing—at least until venture fundraising rebounds.

Teng specializes in growth-stage deals in the cloud software industry, concentrating on companies that are scaling past their Series B round. The less hospitable venture fundraising environment is particularly problematic for SaaS businesses, she explains, because they derive a greater portion of their valuations from future earnings. This has had a chilling effect on some private investors, who backed off the SaaS market in response to the rate hikes.

Others, including Teng, have remained steadfast in the belief that over the long term, SaaS companies will yield superior returns to competing industries. Teng is still bullish about cloud-based SaaS companies—particularly those with an AI component—and she sees a possible resurgence in SaaS IPOs in late 2023.

“Ultimately, I do believe that investors recognize that the cloud model, with its recurring revenue and strong net-dollar retention dynamics, is robust,” Teng says.

VCs emphasize efficiency for SaaS portcos

VCs are now urging founders to be more cautious about chasing ARR while ignoring burn rates regardless of the portfolio company’s stage.

“We’ve been encouraging our founders to be introspective around the concept of efficient growth, which is growth at optimal costs and contextualizing the trade-offs between growth and burn,” Teng says.

To account for the trade-offs between growth and profitability, Teng encourages startups to pay attention to a metric Bessemer refers to as “efficiency score.” The firm calculates this score in two different ways, based on the stage of the company:

For companies with over $30 million ARR, Bessemer determines this efficiency score by adding a company’s YoY ARR growth rate to the free-cash flow margin of the ARR. Their target benchmark for that efficiency score is 40% or above. This is commonly referred to as the “Rule of 40.”

For Bessemer, best-in-class portfolio companies with between $25 million and $50 million in ARR can attain a 70% efficiency score, while top-performing startups with $100 million or more in ARR achieve 50% efficiency.

For earlier-stage startups under $30 million ARR, Bessemer looks annually at net-new ARR, the annual change in recurring revenue, over net burn, or capital spent. The best-in-class benchmark is 1.5x.

Early-stage SaaS rediscovers efficiency

Even early-stage SaaS VCs, who are typically less impacted by profitability concerns than late-stage investors, are advising companies to adopt a new gameplan.

Euclid Ventures co-founder Omar El-Ayat launched a fund focused on seed-stage SaaS investments in 2022. Since entering the market, El-Ayat has noticed increased wariness from LPs. “It’s a risk-adverse environment,” he says. That hasn’t changed the number of investment opportunities in SaaS or valuations for Euclid’s portfolio companies. But on a broader scale, El-Ayat has noticed the slowdown is seeping into the seed stages.

Prior to the SaaS pullback, El-Ayat says, early-stage VCs didn’t put much emphasis on a startup attaining profitability until at least the Series A stage, or even much later. Today, things are different: Euclid is pushing portfolio companies to become profitable from the outset, in part because growing inefficiently becomes a “hard thing for a company to unlearn.” If a company can generate positive cash flow, it helps draw interest from late-stage investors who are now as concerned about profitability as they are about ARR.

“We care about it as early as we get to invest,” El-Ayat says of backing profitable companies. “We want businesses that can attract capital, but that aren’t relying on massive amounts of capital. We don’t want businesses that require hundreds of millions of dollars to get to scale.”

Learn more:

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.