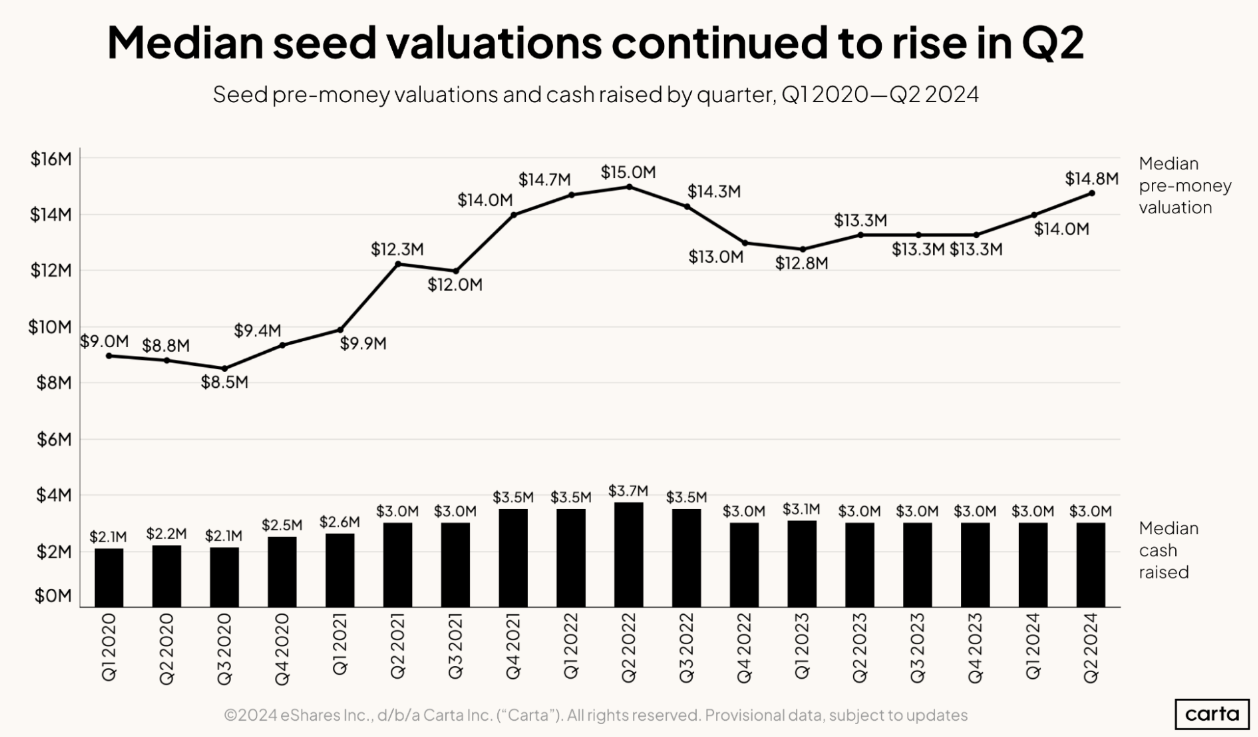

There was little variation in the median valuation for new seed investments during 2023. By and large, the market for companies at the earliest stages of startup life held steady.

During the first half of 2024, however, the price of doing business went up.

The median seed-stage valuation leaped from $13.3 million in Q4 2023 to $14 million in Q1 2024, then climbed again to $14.8 million in Q2, according to Carta's preliminary data from the quarter. That’s the second-highest median seed valuation in any quarter on record, trailing only Q2 2022, at the tail end of the venture industry’s high-flying pandemic bull market.

Over the past two quarters combined, the median seed valuation—encompassing both primary rounds and bridge rounds—has increased by 11.3%. But this uptick in valuations has not been accompanied by an increase in round sizes. The median seed-stage deal size remained at $3 million in Q2, the same as it’s been in six of the past seven quarters.

That’s different from the last time seed-stage valuations were on the rise, back in 2021 and early 2022. Then, round sizes were also growing: Between Q1 2021 and Q2 2022, the median seed deal size went from $2.6 million to $3.7 million.

This more recent combination of deal data—rising valuations and steady deal sizes—means that dilution on seed investments has been decreasing in 2024. If founders are able to raise the same amount of capital as before while attaining higher valuations, that means they’re selling a smaller percentage of company shares to VCs and retaining a larger percentage for themselves.

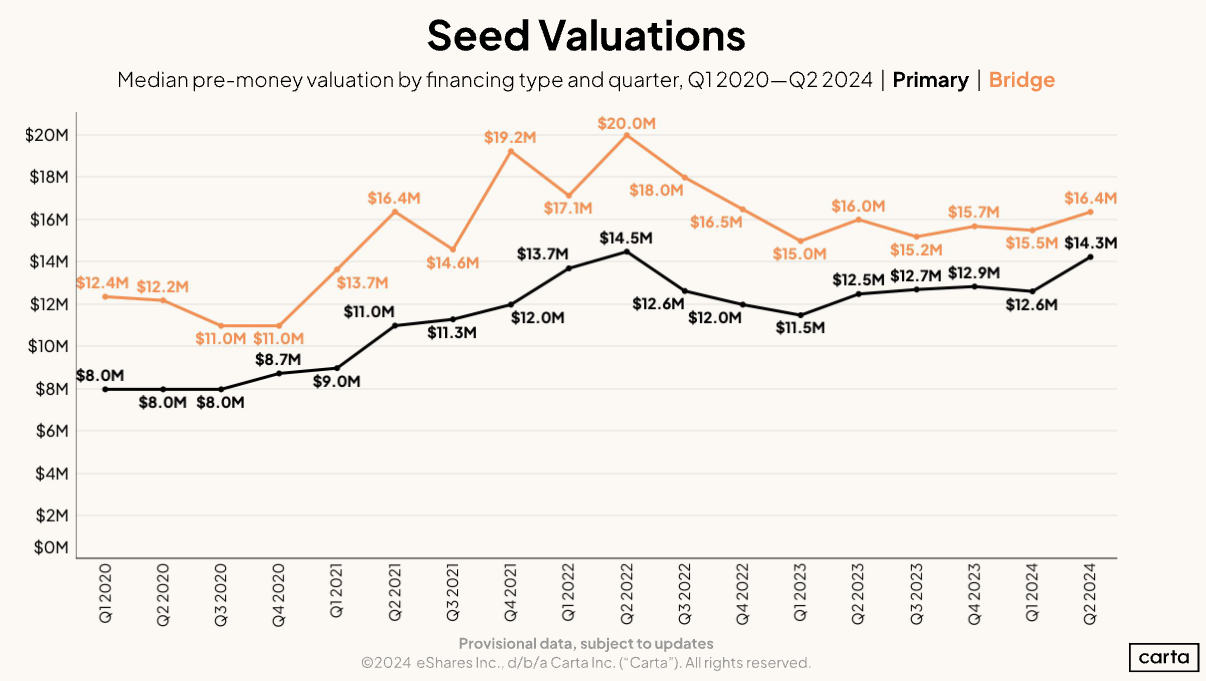

Primary seed valuations jump 13%

This overall increase in median valuations was aided by increases both on primary seed deals and on bridge rounds raised by seed-stage companies. But primary deals experienced a larger leap, rising from $12.6 million to $14.3 million—up 13% quarter over quarter.

For primary rounds, this was the second-highest quarterly median valuation on record, just $0.2 million off the record set in Q2 2022. Among bridge rounds, however, seed valuations remain low relative to recent years. At $16.4 million, Q2 2024 was tied for the sixth-highest quarterly median since the start of 2020, well behind the high of $20 million, again from Q2 2022.

At the seed stage, median bridge valuations have historically always been higher than median primary valuations. But in Q2, the difference between the two was just $2.1 million—the smallest the gap has been so far this decade.

Get the latest data

Sign up for the Carta Data Minute newsletter to receive the latest data on VC financings, valuations, compensation, and more:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2024 eShares, Inc. dba Carta, Inc. ("Carta"). All rights reserved. Reproduction prohibited.