By some measures, the venture capital market is heating back up. Valuations are trending in the right direction: In Q2, the median pre-money valuation on Carta increased at every stage from seed to Series C.

For the right startups, investors are still willing to pay pre-downturn prices.

“High-quality founders and teams can still drive a premium,” says Marcos Fernandez, managing partner at Fiat Ventures, an early-stage fintech firm. “There are still people with dry powder, and there are still great teams.”

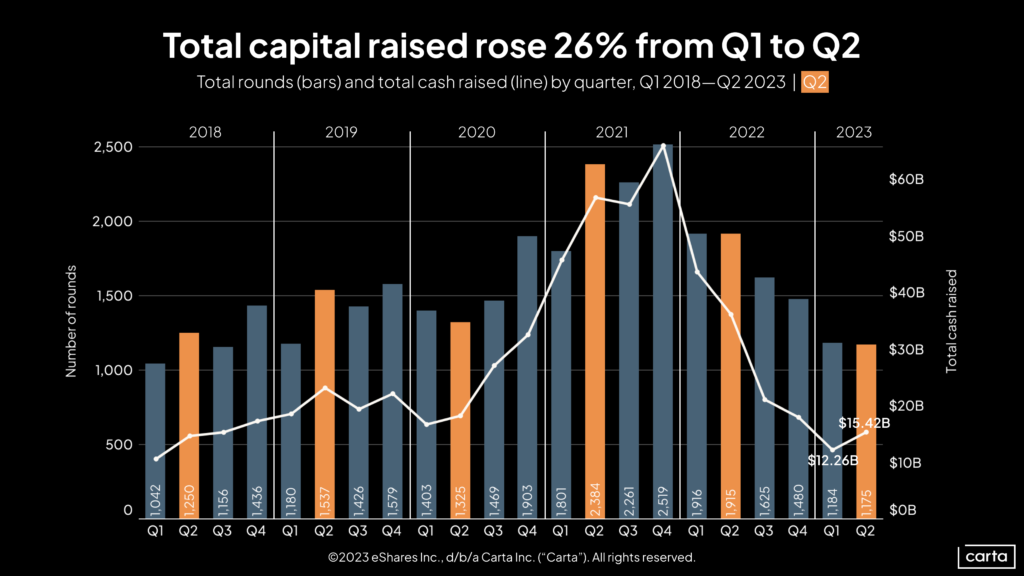

By other measures, the market looks chillier. There were 2,359 venture investments on Carta in the first half of 2023, the slowest half-year for deal activity since early 2018. That’s down 44% from two years ago, in the first half of 2021.

In the context of deal count, looking back two years is a particularly meaningful comparison. Among startups, that time frame—equivalent to 730 days—is a rough estimate for the typical interval between priced rounds. In Q2, the median company raising a Series B round on Carta did so 720 days after its Series A, and the median Series C came 740 days after a Series B.

Thus, we can expect that many of the companies that raised capital in H1 2021 will be returning to market in 2023. The steep reduction in deal count suggests some will be facing an uphill climb.

The limits of bridge rounds

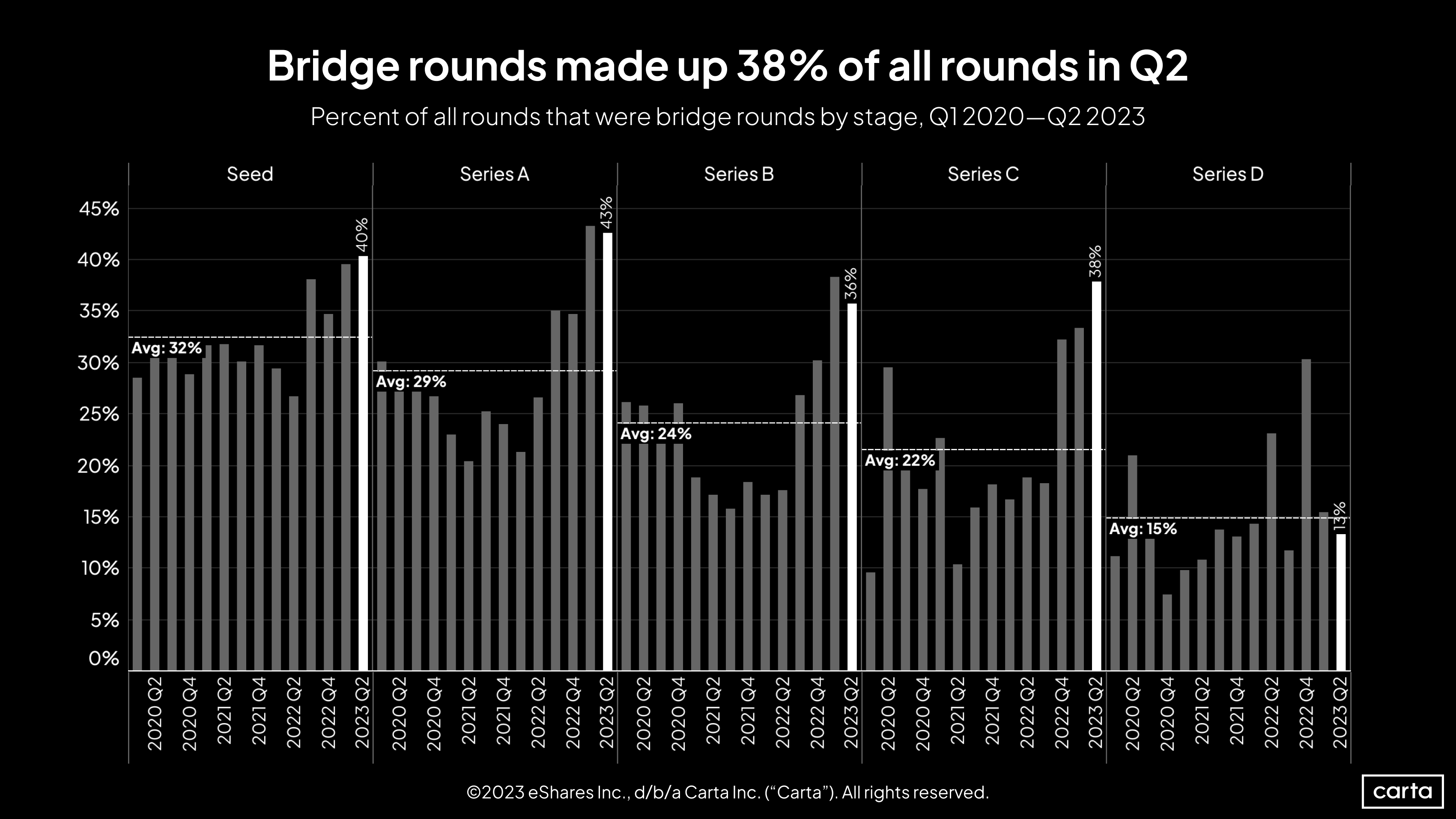

Instead of raising a new primary round, some startups are opting for bridge funding (which Carta defines as any new capital raised after the first round in a given series). This often takes the form of follow-on funding from existing investors who want to tide over their portfolio companies until a more favorable fundraising environment arises. In recent quarters, the rate of bridge rounds on Carta has increased at every stage from seed to Series C.

But bridge rounds are not a long-term solution to the gap in deal count from two years ago compared to today, Fernandez says. If deal counts remain low, the math will no longer add up. A reckoning may come.

“The bridge rounds are still sustaining sideways growth for the time being. But at some point, companies are forced to make really tough decisions,” Fernandez says. “They can’t raise capital in the open market. They’ve already tapped their existing investors. They’ve tapped into other alternative instruments, like debt financing. They either need to find an acquirer for this business, or they can shut down.”

Some investors see this potential contraction as a healthy correction to an overstuffed startup landscape—the culling of a herd that had grown too fat on the bounty of the 2010s bull market. But for startups, that doesn’t make the prospect any less unpleasant.

“I have a ton of sympathy for founders. It’s a really difficult and painful position,” Fernandez says. “You dedicate your whole life to this, and things were going well. But some things are out of your control.”

Buyers, VCs are circling

M&A activity on Carta has remained elevated so far this year, a sign that some startups might already be opting for acquisitions instead of trying to raise new venture funding. If a company does decide to pursue a sale, Fernandez says there should be plenty of potential buyers—although those buyers might have leverage on their side when it comes to price.

“I’ve heard from people from private equity firms to even corporate VCs who are waiting on the sidelines right now, because they know there’s going to be an incredible opportunity for consolidation,” he says.

The leverage equation is similar in the VC market. With so many startups seeking new rounds of primary capital, investors are able to pick and choose from a long list of targets.

And some of those targets look more attractive than ever. The venture downturn has caused founders to reassess their priorities, putting fundamentals like unit economics and profitability ahead of breakneck growth. This early financial discipline can set a strong foundation for growth.

Not every startup has been able to adjust its approach. And not every startup will succeed in raising new funding. But for those that do, Fernandez maintains that the sky’s the limit.

“We’re not slowing down,” Fernandez says. “We think the investments we’ll make over the next 24 months will be some of the best investments we ever make.”

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.