Over the past decade, new venture capital investments into U.S. startups have been about 10 times more common than VC-backed exits.

To Kamran Ansari, a longtime VC and current venture partner at Headline Ventures, the data sends a clear message about where the true challenge lies for investors.

“Getting into deals can be relatively straightforward if there is allocation and interest,” Ansari says. “Getting out is hard.”

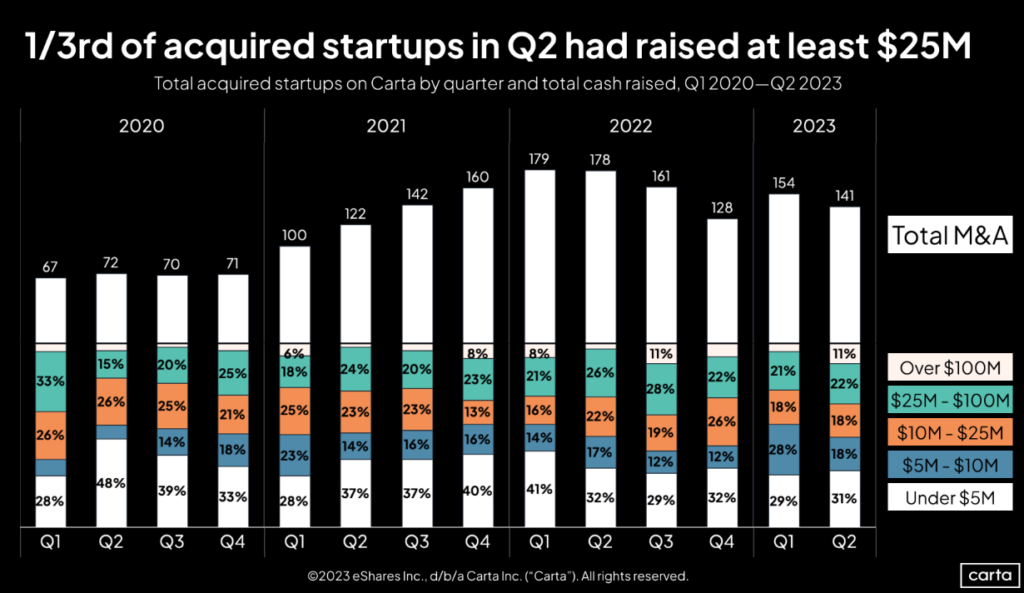

So far this year, plenty of investors and startups have been up to the task of finding an exit. Venture-backed startups completed 295 M&A deals on Carta during the first half of 2023, including 141 in Q2. It was the third-busiest half-year for M&A activity on Carta since the start of 2020.

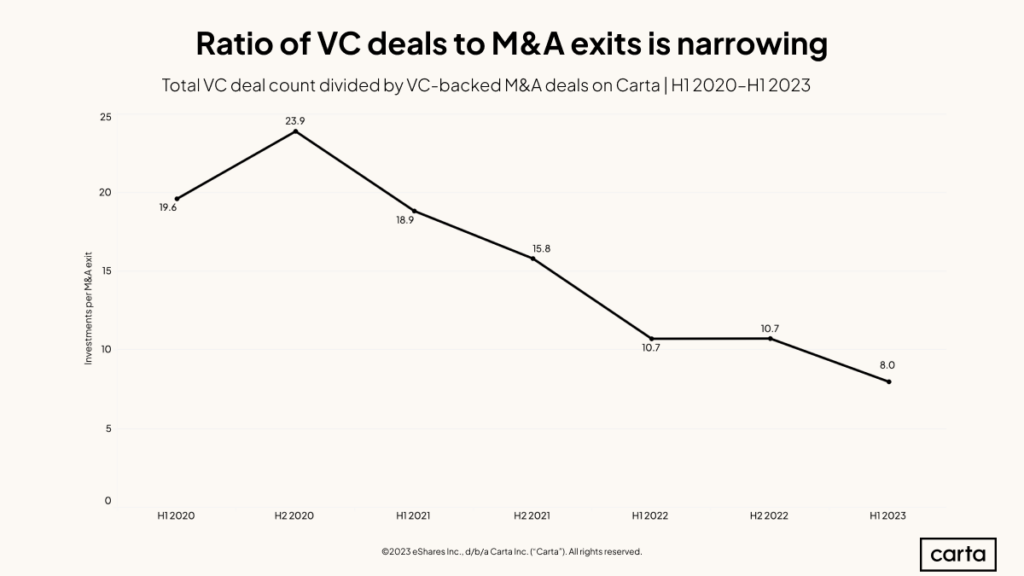

In addition to these 295 VC-backed M&A deals, there were 2,359 VC investments on Carta in H1. That works out to a rate of eight investments for each exit via M&A—the fewest investments per M&A exit of any half year so far this decade.

However, this elevated rate of VC-backed exits on Carta runs counter to some other key deal trends. A startup’s two most likely exit paths are a sale through M&A or going public through an IPO. And the broader market for both these deal types has been depressed in H1. The overall value of M&A deals in the U.S. declined by 30% compared to H1 2022. And there were just 52 IPOs in the U.S. between January and June, putting 2023 on pace to be the second-slowest year for public debuts in the past decade (2022 was the slowest).

VC-backed companies are still finding exits. But to do so, they must navigate a challenging macro environment.

Fewer deals, limited price discovery

Some of the headwinds in the exit market have also contributed to the recent downturn in venture activity: In the face of inflation, rising interest rates, and geopolitical unrest, investors are uncertain about where the global economy will go next. When investors are uncertain, they’re less likely to do deals.

This can create a spiral. More uncertainty leads to fewer deals, which in turn causes more uncertainty, and so on. In the context of M&A, the recent reduction in venture capital deal counts means acquirers have less context for how to properly price their potential targets.

“There’s very little price discovery that’s happened,” says Ansari, who formerly spent three years as head of business development at Pinterest. “Seed and Series A, those markets are pretty active. But once you’re past Series B, and you’re trying to look at the market for these companies right now, it’s really hard to handicap.”

Across seed and Series A, there were 1,622 transactions on Carta in H1. At every stage from Series B and beyond, there was a combined total of just 570 transactions. Fewer deals means fewer data points for investors trying to determine a company’s market value.

Profits take precedence

Over the past several quarters, the desires of venture capital investors—and thus the aims of startups—have shifted. After years of prioritizing rapid growth at all costs, VCs and founders are now focusing more on managing cash, extending their runways, and establishing a path to profitability.

The same shift toward thrift has occurred in the market for startup M&A. When looking at late-stage assets, corporate acquirers have grown more leery about losses.

“I do think that all strategic buyers right now are hyper cash-conscious,” Ansari says. “If someone is looking at a company that I’m involved with for M&A, they’re much more focused on, how much is it burning? And how much will it take to get to profitability?”

In other words, buyers have grown more conservative. In general, they’re less intent on finding companies with the highest ceilings, and more concerned with high floors.

Faced with these new priorities, Ansari says many firms that invest across a range of asset classes—such as hedge funds and private equity firms—have shifted some of their focus away from the private markets and toward the public markets. For instance, several of the year’s biggest acquisitions have been buyouts of public companies led by tech-focused private equity firms that also have significant holdings in private companies, such as Silver Lake’s $12.5 billion purchase of Qualtrics and Thoma Bravo’s $8 billion takeover of Coupa Software.

Particularly after revenue multiples for public tech companies declined significantly in 2022, investors see the potential for bargains in the public market.

“They could own this cash-burning Series D or Series E company and spend a bunch of effort to retool the management team, to cut costs … it’s just a lot more work,” Ansari says. “Or, they could buy what’s already a public company that’s generating cash and trading at a deep discount to 2021 levels. They can take it private for a few years, and then bring it back onto the public market in a better environment and probably get a nice 2x or 3x return.”

All eyes on Wall Street

There are signs that the public market is on an upswing. The S&P 500 was up more than 16% during the first half of the year, although it cooled off some in July and August. And while IPO activity remains slow, it has begun to perk back up after a torpid 2022. Ansari pointed particularly to the public debut of Cava as a promising sign: The Mediterranean restaurant chain’s stock price is up more than 90% since its IPO in June.

More big names might be on the way: Food delivery startup Instacart and chip design giant Arm are reportedly both planning IPOs for this fall.

“The window was kind of shut for the past 18 months. But it’s reopening again a little bit coming on the heels of Cava, which I think really enlivened the IPO market again,” Ansari says. “It took pita and hummus to get us back.”

If Wall Street’s IPO machine revs back up and public stocks continue to perform well, the market may come to a tipping point. When public stock prices keep going up, at some point, they stop looking like such a bargain. If and when that happens, Ansari expects the attention of many corporate acquirers, PE firms, and other buyers to return to the private markets.

”Since the beginning of the year, everything on the public side is up,” Ansari says. ”There’s going to be a tipping point here. And it may not be very far off.”

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.