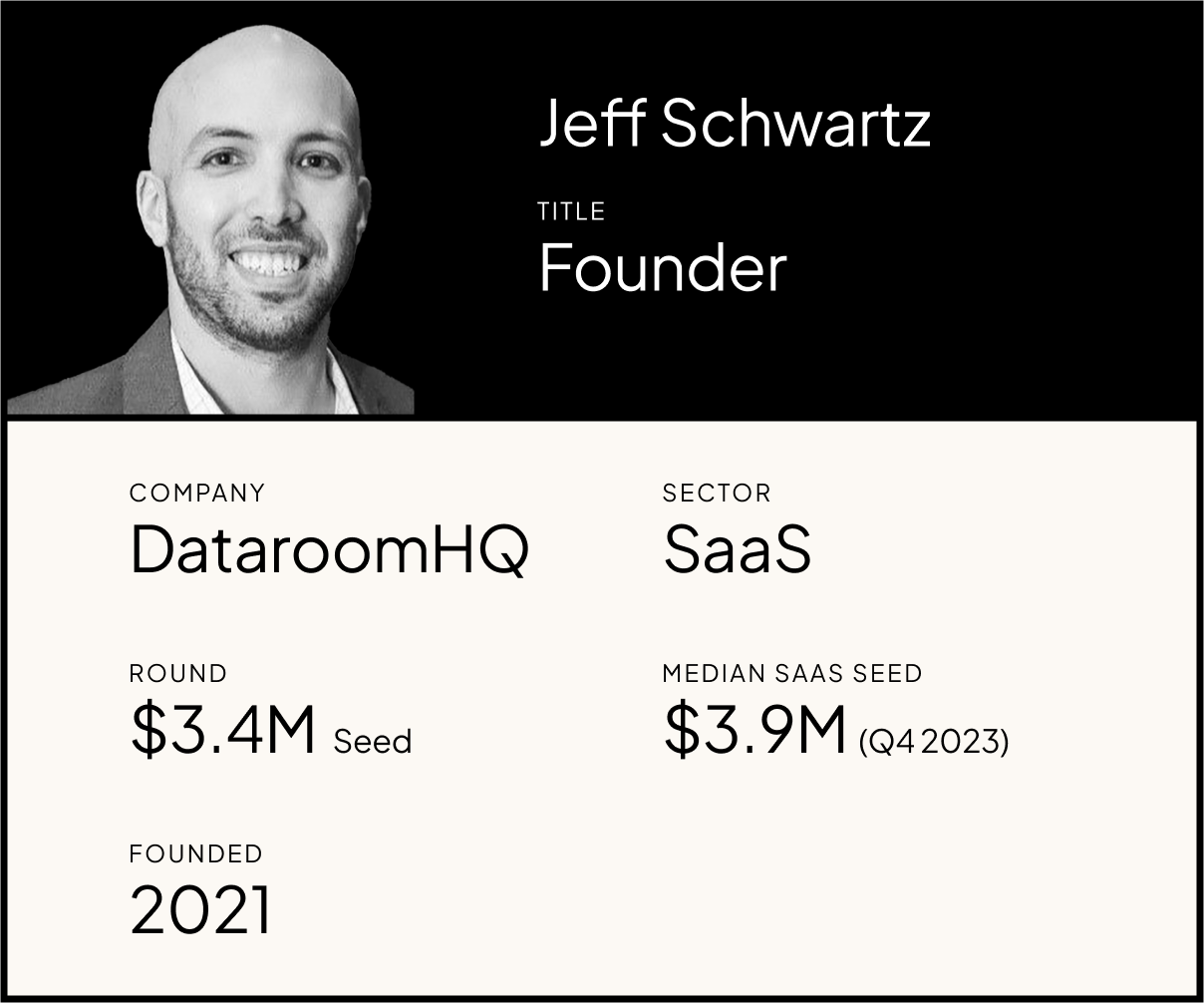

Jeff Schwartz is founder and CEO of dataroomHQ, a platform that enables investors to evaluate companies, and companies to report and analyze their metrics.

In February, the company announced a $3.5 million round, led by Oceans and Bling Capital, with Garuda Ventures, Cortical Ventures, and others joining the round.

But 2023 was not an easy time to raise, with seed round deal count down 27% year-over-year, according to Carta data.

Despite a tough market, Jeff successfully closed his seed round, above what he was expecting to raise. And it all started with a cold LinkedIn DM.

Highlights

How a cold Linkedin message led to an unanticipated term sheet

Filling out a round when a fundraising opportunity surprises you

The decision to spend 1.5 years on R&D alone to build a “minimum remarkable product” and use that product to raise a round

Using a product demo as the ultimate pitch

CARTA: Tell me about your fundraising journey so far. What led you to where you are now?

JEFF SCHWARTZ: Our fundraising journey started at the end of 2021, when we were really pre-product. The former CEO and founder of DataRobot, Jeremy Achin, along with his and Igor Taber’s firm Cortical Ventures, wrote the first check into the company. I had known Jeremy since 2012, when we worked together at Travelers Insurance’s R&D department. We then spent five years at DataRobot together. He knew how passionate I was about using data to drive strategy and decision making, and understood my vision: allowing every company to have their own ‘operational command center’ to enable them to use real time data to make objective decisions.

So he wrote a SAFE for around $460,000. We secured that funding and it was pretty much like, “Okay, now go spend a year building a product that brings this vision to life.”

We didn't have the pressure of building a minimum viable product and pushing it to the market. Instead, we actually spent a year-and-a-half building what we call a “minimum remarkable product.” We built a really robust platform right from the get-go prior to bringing it to the market.

In this environment, where money is tighter, it helped having a fully baked product and not a MVP. Customers are no longer willing to purchase a shiny object or point solution anymore. Now they need to operate more efficiently and cut expenses—so they do look to consolidate across fewer platforms.

Once we had our minimum remarkable product we were open to doing our round. We raised $3.5 million. And ultimately, it was our product that helped us raise the round. Because we were able to dogfood it [use our own product], we showed investors our own metrics and operating plans within the platform—the exact way investors want to see metrics.

How did you know it was the right time to raise again?

We had intentionally kept our burn rate very low for the first 12 to 18 months since we knew we were not going to market right away. Every role on the team was focused on building the product. Once we built the product and we were ready to bring it to the world, we knew we needed to expand the team to do so. But interestingly enough, we weren't in active fundraising mode when our raise started.

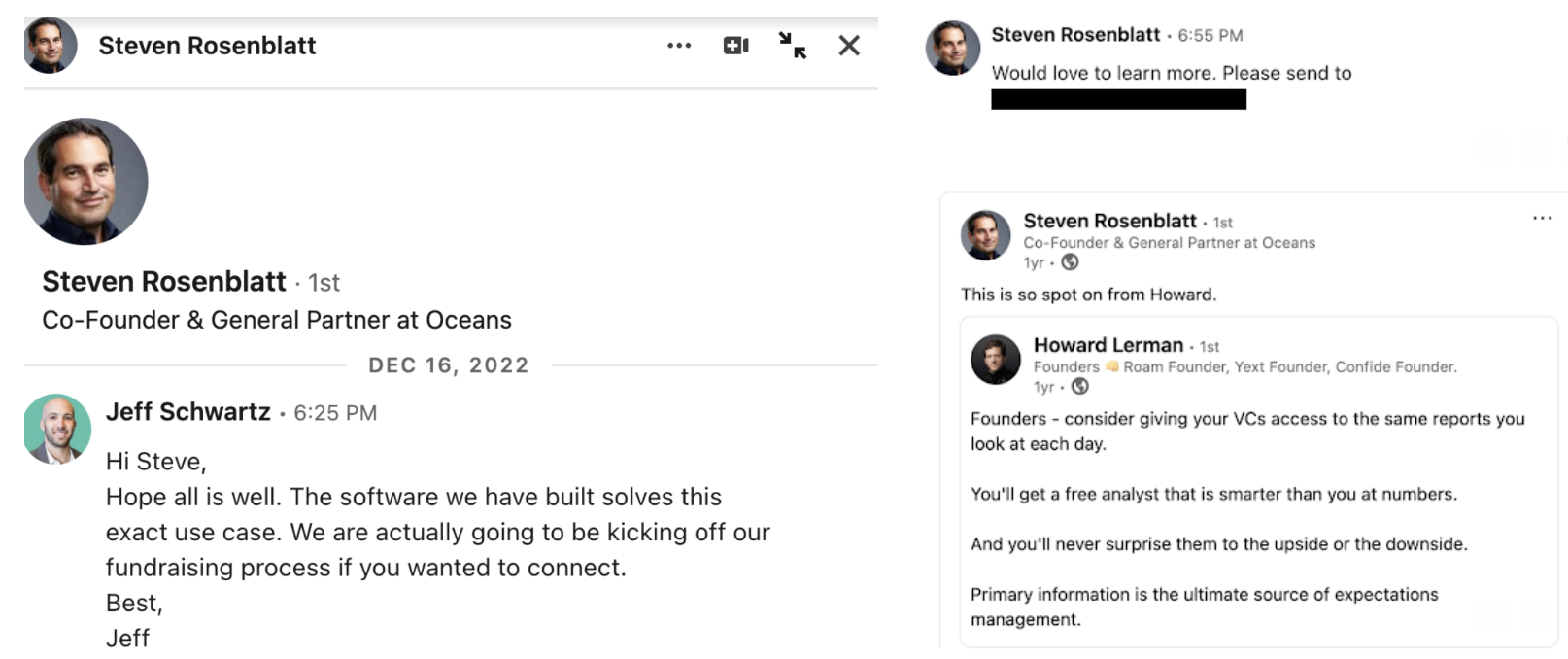

It's a pretty funny story. It all started with a LinkedIn post. One of the co-leads of our round, Steven Rosenblatt from Oceans, commented on Howard Lerman’s LinkedIn post essentially saying, "You should be using your board and your investors; you should be showing them the same information or dashboards that you're looking at on a day-to-day basis, because you'll get like a bunch of free, really smart FP&A [Financial Planning and Analysis] people in the room with you.”

And I saw it and immediately thought, “That’s what we’re building!”

So I sent him a cold message on LinkedIn that said something like “Hey, by the way, we're building software to solve this exact problem.” He responded right away and suggested we meet. It was December 2022 when I messaged him, and we weren’t actively raising yet. But we met, and soon after a term sheet came from that.

The LinkedIn exchange between Jeff Schwartz and investor Steven Rosenblatt.

The whole process was a little backwards. Most companies pitch a bunch of people, they get a term sheet, then go back to the others. But with our raise, we got a term sheet, but we hadn't talked to anyone else yet. Overall, we loved the conviction that Oceans had in what we were building and the velocity at which they moved. As a founder, that was exactly what I wanted from an investor.

We were looking to raise about $2.5 million at that point (it wasn’t until later we ended up deciding to raise $3.5 million) and needed to get other investors on board. So we're like, “Oh, crap, how do we fill the round?” [laughter] We had to hit the ground running from there.

That’s remarkable to get a term sheet from a cold LinkedIn message. It’s inspiring to know those sometimes work. Tell us about how you filled out the rest of the round.

Before the LinkedIn post, I didn't have a clear path or know what firms to go to for our next round. I knew I had to figure all that out.

Ultimately it was through introductions from firms like Oceans, and from our pre-seed investor, Cortical Ventures, that really helped fill out the round. That's how I met our co-lead, Bling Capital. Oceans introduced me to a venture partner at Bling Capital. The other big firm that was in the round, Garuda Ventures, we met through an introduction from our pre-seed investor, Cortical, Jeremy and Igor’s firm.

In terms of key learnings, I'd say that finalizing the round did take longer than I expected. I was used to hearing stories about founders getting a term sheet and then everyone wants to join in. For me, it was like, we got a term sheet, but we hadn't talked to anyone else.

The formal raise took two to three months, from the first conversations to close. We had $5 million in commitments, and decided to narrow that down to $3.5 million. And that’s where we settled. Having a firm like Oceans on-board really helped catalyze the round. They’ve spent 25 years building a deep network in NYC, and it’s clear they have so much respect from the tech community.

How did you settle on that number?

Using our own platform’s forecasting and reporting, we identified we needed $2.5 million to hit our next milestones. And then, after the Oceans term sheet, we went out to the other investors simultaneously. And even though it felt long and stressful, numerous yeses all came in within the same week which got us to that $5 million number.

We decided to go above $2.5 million to allow ourselves to make some strategic bets, have a longer runway in this market, and get the people we wanted around the table with us on this journey.

But we didn't want to go all the way to $5 million, for many reasons. For me, it was important to control the valuation and not get too far ahead of ourselves. And then of course things like dilution come into play. So we wanted to make sure we ended up at the right number, not the highest number.

Once you had that goal number, how did you decide who to go with? I assume, once you’ve gotten to that point where you’re receiving term sheets, you’ve already vetted each other quite a bit. How did you separate good from great when it came to the right partnership?

It was a few different things.

I was really transparent when I started having conversations with investors about what I wanted from a founder-investor relationship. Going into it, you hear about the “dog-and-pony” shows founders often feel they have to put on for investors. A lot of founders feel like they need to go into the board meeting and say how great everything is. In my eyes that doesn’t accomplish anything.

This is quite literally why I built dataroomHQ: to create transparency around the business performance so that everyone is aligned, and able to make decisions based on the same set of information. I wanted to be able to come into the board room and say “These are the areas we suck. These are the things we're off on right now, let's talk about how we can make that better.” Our goal is to perpetuate that kind of open dialogue around performance. And our investors were very receptive to it.

In choosing our cap table, each person understood the problem, because they’re all equally data-driven. As a data-first company, that was a big piece for me.

Our entire ethos is getting comfortable with sharing less about successes, and more about areas of struggle. It turns out, we share that sentiment with a lot of former operators who became VCs.

Like Ben and Kyle from Bling. Ben was at Google early on and Kyle founded ChoicePass (which was later acquired by SalesForce). Arpan and Rishi from Garuda were early at Okta and Poynt, respectively. The Oceans team were early at Facebook, Google, Apple, and Foursquare. And then of course Cortical, where Jeremy previously founded and served as CEO at DataRobot.

Each of the investors at our cap table could empathize with me as they were on my side of the table in their prior lives. Maybe this will change as we raise future rounds but for now, I wanted to surround myself with people who had been through it before and can empathize.

So there was a parallel between the product you’re building and what you personally wanted from your investors.

Yes, I even worded it that way to investors. My whole thesis is around transparency, and building an open relationship between companies and their boards, especially since we all are on the same mission…to create an iconic company.

I want to be able to be very open. If I come into the meeting and just start touting all our successes, that's really not doing anything for the company. Maybe we will all high five and smile for a bit, but it isn’t going to help build a durable business. It is way more productive to talk about what we suck at—to get better at those things. I do think a lot more companies should operate this way.

The beauty of our situation is that I was able to collaborate with these former operators turned VC to build new functionality into the product. Automating the tools they were manually using to evaluate investment decisions.

For instance, we worked with the Bling team to bring the cohort analysis framework they use in making investment decisions into the product. Now in a few clicks, they can determine if a business is durable. Similarly, we partnered with the Cortical team to build what they call “the company building formula” into the product. This now allows them to have a leading indicator framework to give their portfolio companies the best chance at becoming durable, instantly.

Your round before this was a SAFE. I’m curious when it came to this seed round, how you thought about that decision of priced round vs. convertible note. What kinds of conversations were you having with investors about this? How did you decide on a priced round?

The first round, I definitely wanted it to be a SAFE. You know, we only raised $460,000. So at that point, it would’ve been way too expensive for us to do a priced round, because a SAFE is pretty much free from an execution perspective. It is very low cost.

But for a priced round, the legal fees are significant. And in most situations the company is taking on a lot of the bill from the investors, right? Because they usually write in the term sheet, like, “you'll cover up to X dollars of legal fees.” So you are not only paying your fees but theirs as well.

Therefore, it gets expensive to do a priced round. And at early, pre-seed stages, the amount of money you are raising compared to the legal costs, makes it hard to justify. So this time, why did we do a priced round? At some point, depending on the size of the round, there's a threshold at which investors feel much more comfortable with a priced round and a more formal agreement. If they are making a big enough investment a priced round does help formalize all the legal language and investor rights – versus a SAFE round, where it’ll usually just convert according to the legal terms of the next round.

So in my case the priced round was more investor-led. But from a founder’s perspective there are also advantages to it.

Let’s talk about the pitch deck. What went into that? What was your strategy?

Looking back on it, my pitch deck was probably awful [laughter]. But if I'm being honest, the biggest part of our pitch for the round was demoing the product.

We went into it believing we built an amazing product. And to investors, positioned it by asking if they’re willing to bet that the world needs a product like ours. The best part was proving to them that we used our own product to show them our metrics.

We also did have a deck. We did talk about the problem, the opportunity, the TAM. And we talked about what we thought our go-to-market strategy was going to look like, and the flywheel effect we wanted to build.

And of course, they wanted to know a bit about me as a founder and my background to determine if I’m the right person to solve the problem. I think that there were a lot of questions like, "Why you?" and "Why now?" That type of stuff.

But it all came down to showing the product and showing what we built.

By the way, I don't know if it's the right or wrong strategy. Readers, take that with a grain of salt. It’s just what worked for us.

However, what my investors relayed to me after the fact was my passion for the problem. Too many companies are flying blind and wait until it's too late to focus on their key business drivers. That needs to change. I always found it fascinating that investors look at a business a certain way to decide whether or not they should make an investment. But the ah-ha moment was realizing companies themselves don’t have a live view of that. So we built it with dataroomHQ.

If most companies are relying on investors to survive, why shouldn’t they view their business through the lens of an investor? This is not to say they can’t look at their business in other ways. But front and center should be a centralized view from the eyes of the people who determine your survival and how valuable you are.

That’s interesting, especially since back in 2021, you’d hear about a lot of money raised pre-product and pre-anything really, that proverbial “sketch on a napkin.” What did you notice was different raising in this environment?

The main difference from my perspective between amazing times to raise, and the times that we raised this round in, was that thing I mentioned before—as soon as someone got a term sheet, it felt like other investors had this FOMO and jumped into the round.

More recently, every single check-in there’s been a deep level of diligence. It’s not just “the lead must have done all the analysis and diligence”. And it's super healthy for the market that you actually have to win each of your investors, not just the lead.

Which seems like it would be more exhausting to experience, but in the end you know your idea is stress-tested.

Exactly. These companies should be well-vetted because of what they had to go through to get these yeses. I will be very interested to see Peter’s (Carta’s Peter Walker) future analysis on the 2022-2023 cohort of companies that were able to secure a seed round. Given the stricter scrutiny placed on them, it will be interesting to see if they have higher success rates.

I will say, for anyone going through it, there are definitely ups and downs. It’s an emotional rollercoaster. Every” yes” is so meaningful, but every no hits hard. And I know people have talked about it before, but it’s really crazy to know how much, at this stage, just one yes can change things. You only need a few yeses to have a chance to build a company, to build something that could be iconic for years to come. If you get 50 no's, but you get a few yeses, you can still do what you set out to.