1000x startups

The best startups are worth 1000x the median startup. Most employees forget that startups follow a power law. This is why when Sheryl Sandberg was considering joining Google, Eric Schmidt told her: “If you are offered a seat on a rocket ship, get on—don’t ask what seat.” Picking the right company is far more important than picking the right role.

The hard part is figuring out which startup is the rocket ship. If an employee can get that right, they might win the Silicon Valley lottery. If they don’t, they won’t.

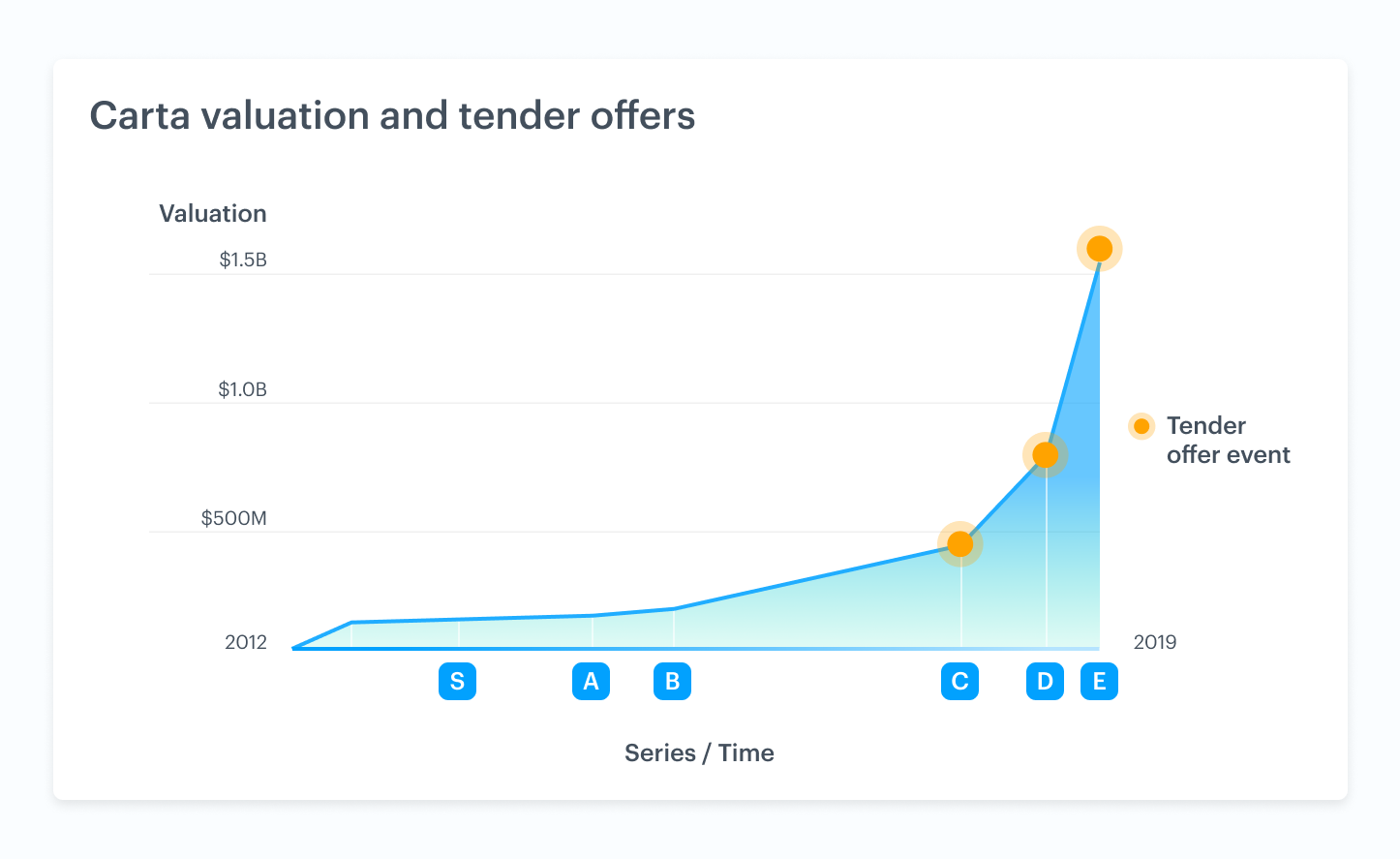

Venture capitalists do this for a living. For our Series E, investors wrote over 500 pages of investment memos to decide whether to invest. It took them weeks of diligence going through our financials and forecasts, interviewing customers and employees, and doing reference checks on our executives and me.

Employees joining a startup don’t get anywhere close to that level of information. Most employees are limited to a handful of interviews and Glassdoor.

Some employees look at investors as a signal for the company’s trajectory. But even with all that time, information, and experience, the best VCs still get it wrong 9 times out of 10. Investors can afford those odds because they have diverse portfolios. Employees, on the other hand, can only pick one company to work for.

Demand for stock

A hot stock has lots of demand. Investors try to pile on and invest more money into the company. Certainly, investors can be wrong. But demand is often a good predictor of value.

Private markets are different than public markets. In public stock markets, the stock price is set by the last buyer. So when more buyers enter the market, the price goes up until there are no more buyers left at that price. In private markets, the price is set by the first buyer (known as the lead investor). Once the price is set, the following investors buy additional stock at the same price.

Since the price doesn’t change, there isn’t a demand curve for the price to climb up until supply matches demand.

The way private markets match supply and demand is to constrain buyers by limiting the round size. When companies have to limit the number of investors in a round, that signals they have a high demand curve.

It’s not the round size that’s important; it’s the amount a company can raise compared to how much it needs. When a company can raise more than it needs, it has excess buy-side demand. When a company has excess buy-side demand, it has the opportunity to offer liquidity.

Liquidity as a demand signal

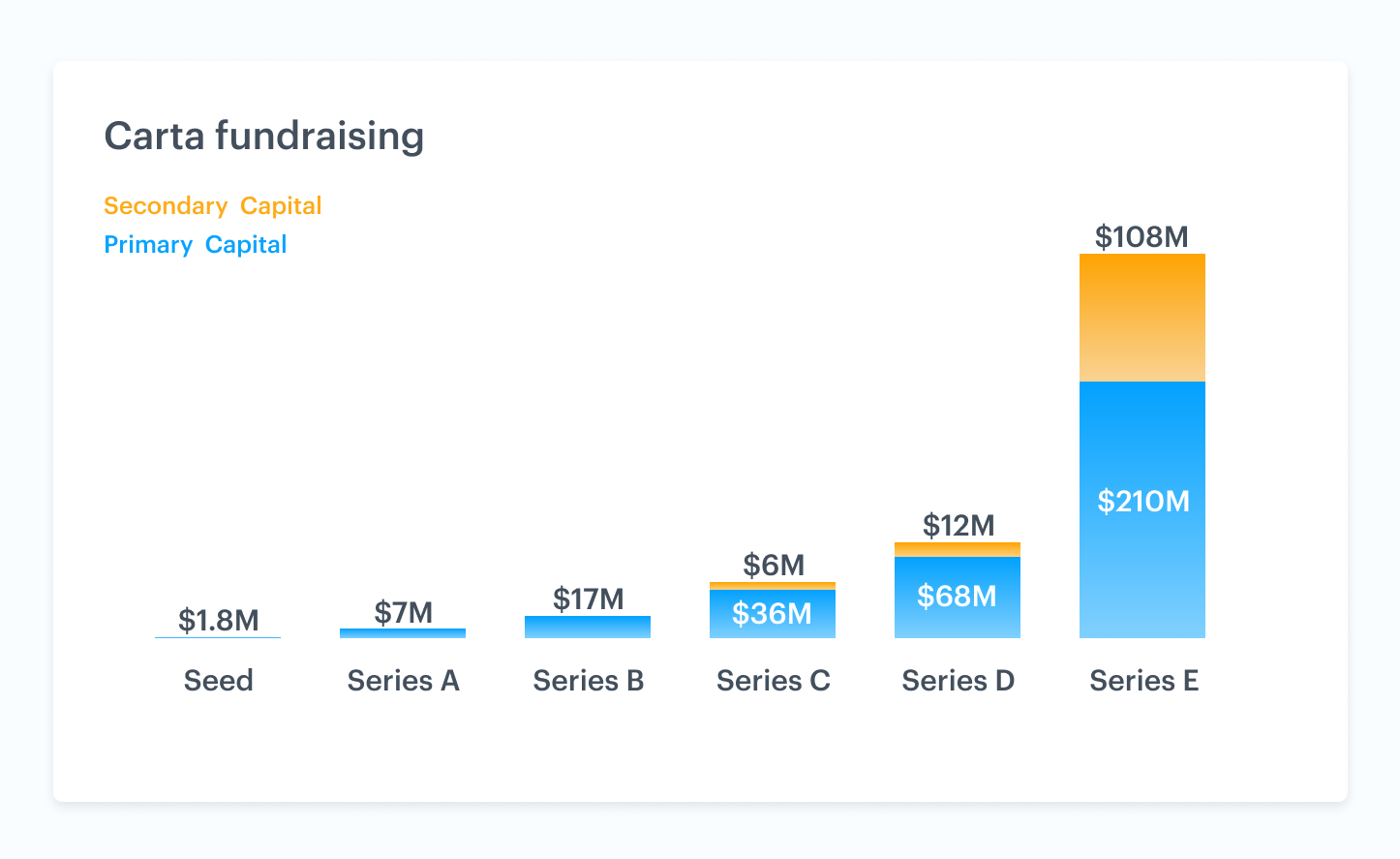

Today, startup employee liquidity programs are often structured as a tender offer. They are frequently run in conjunction with a financing event where there is excess buy-side demand—an oversubscribed round. For example, in our most recent $318M Series E,1 we only took $210M onto our balance sheet. We used the additional $108M to buy shares from early employees and investors and give them liquidity. We’ve run tender offers in the past and hope to run them every 12 to 18 months going forward.

Employees don’t get many signals of a private company’s trajectory. Without all the information that investors get, one clear way for employees to tell if a company has excess buy-side demand is whether that company offers liquidity.

1 The Series E total ($318M) is slightly bigger than previously announced ($300M). This is because of additional funding that took place after the initial close.

DISCLOSURE: This communication is being sent on behalf of eShares, Inc. dba Carta, Inc. (“Carta”). This communication is not to be construed as legal, financial or tax advice and is for informational purposes only. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein.

This post contains links to articles or other information that may be contained on third-party websites. The inclusion of any hyperlink is not and does not imply any endorsement, approval, investigation, or verification by Carta, and Carta does not endorse or accept responsibility for the content, or the use, of such third-party websites. Carta assumes no liability for any inaccuracies, errors or omissions in or from any data or other information provided on such third-party websites.