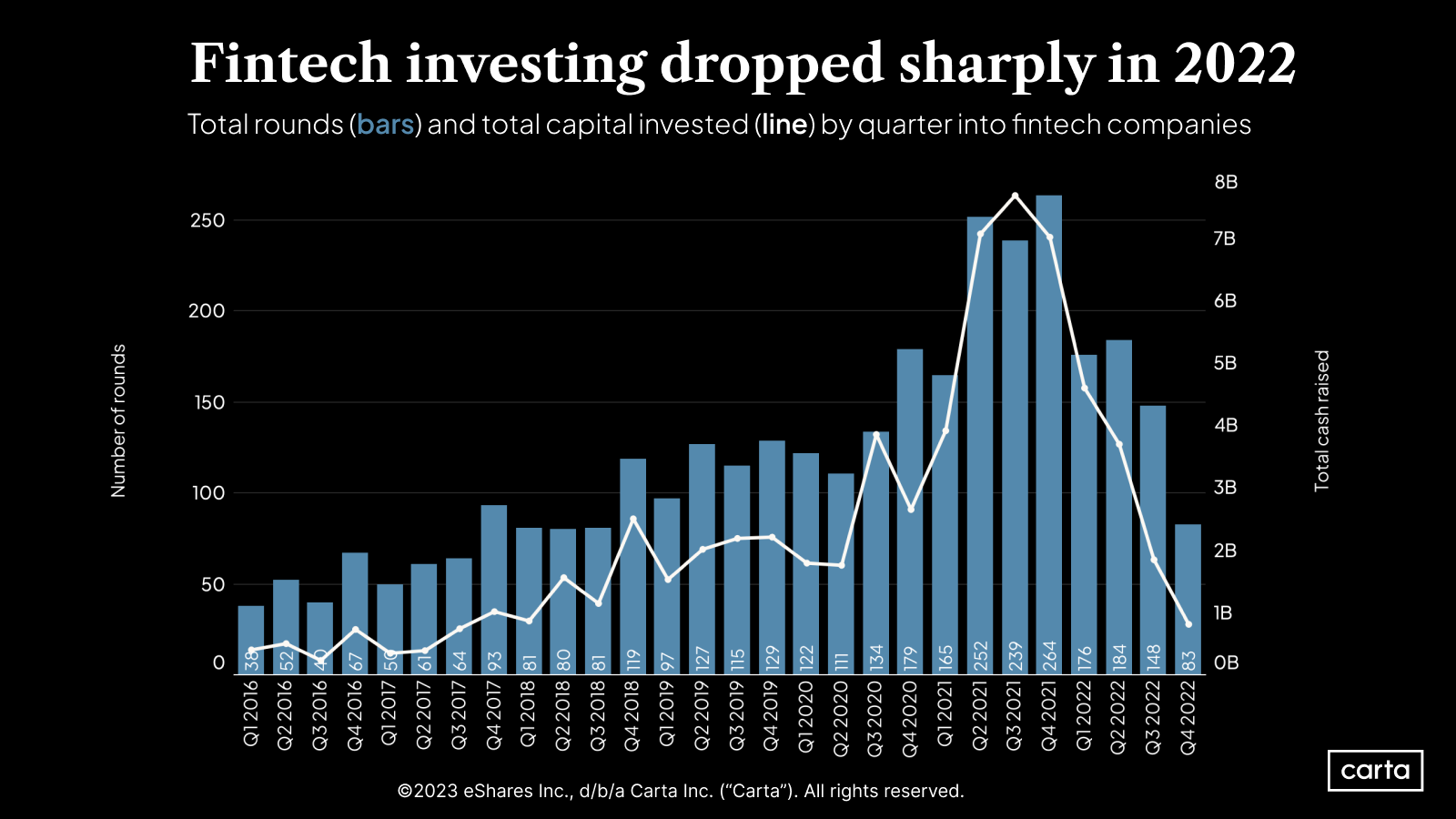

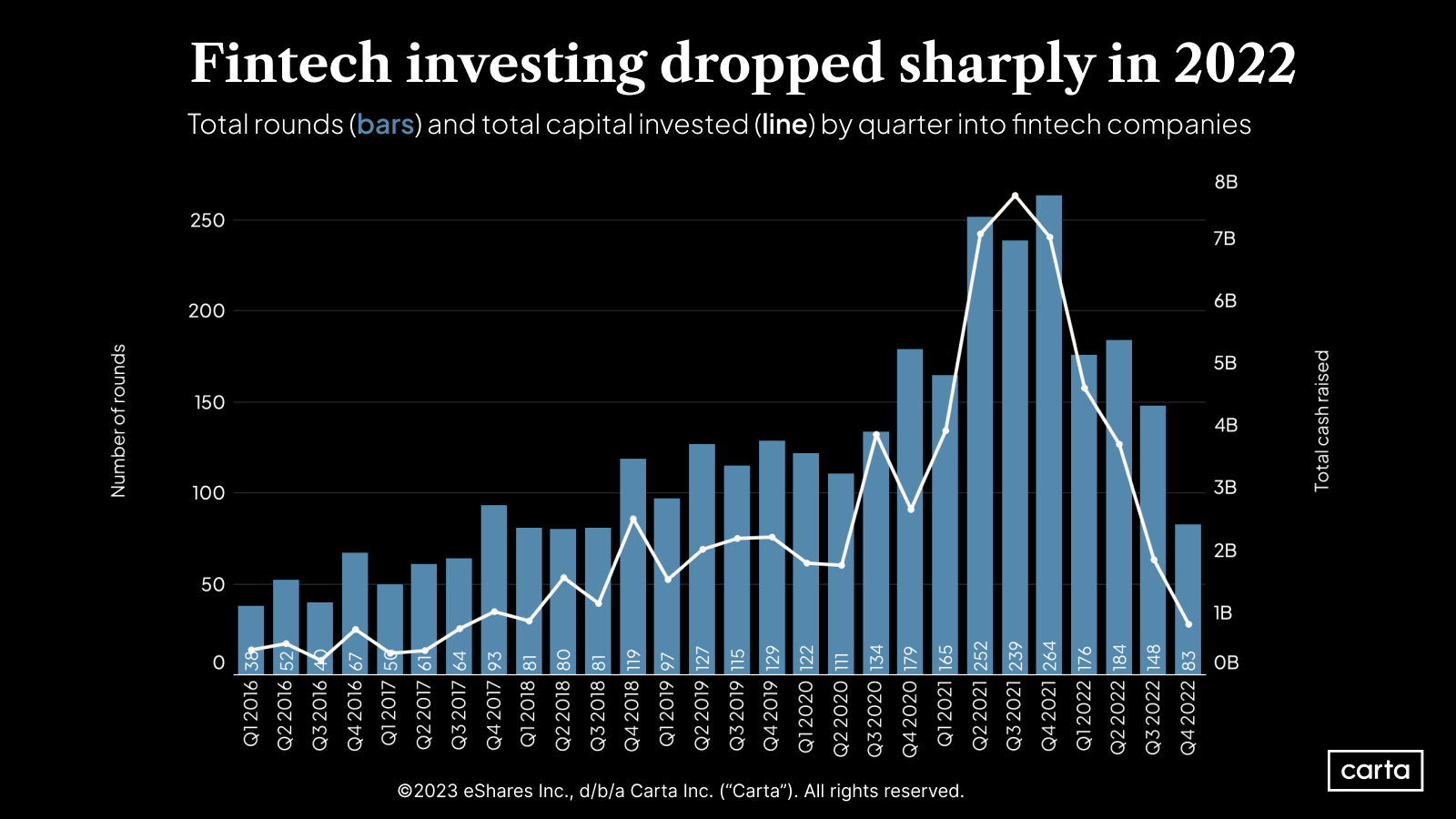

Venture capital activity declined in nearly every corner of the tech industry during the fourth quarter of 2022. But the dropoff was particularly abrupt in fintech.

The value of fintech fundings on Carta fell 63% from Q3 2022 to Q4, with quarterly funding plunging below $1 billion for the first time since Q1 2018. Across all sectors, venture deal value fell a more modest 31%. The number of fintech deals, meanwhile, dipped 52% from Q3 to Q4, outpacing a 27% decline in the broader venture market.

Fintech deal value has fallen in five straight quarters

A few other takeaways from fintech’s recent falloff:

Deal value was 90% lower in Q4 2022 than in Q4 2021, compared to an 80% year-over-year decline across all sectors.

Deal count dropped 72% in that same year-over-year stretch, compared to 56% for VC at large.

In 2021, fintech investments made up 11.3% of all venture deals tracked on Carta. In 2022, that figure fell to 10%.

At every stage of the startup lifecycle, median fintech valuations are down at least 30% from a year ago. At Series B and beyond, valuations are down more than 60% at each stage.

It’s been a swift rise and fall. But Morgan Flager is taking the long view. Flager is managing partner at Silverton Partners, an early-stage firm based in Austin, Texas, with several fintech startups in its portfolio. He’s seen plenty of twists and turns during a 25-year career in venture capital. In that context, the current downturn isn’t so daunting.

“If you look at it from the perspective of where things were in 2021, it certainly was a big decline,” Flager says. “If you look at things over a longer period of time, the multiples that we’re seeing now are actually not that far off historical averages.”

Why fintech funding thrived in 2021

For fintech startups—as for startups in many other industries—the past three years have been a roller coaster.

The onset of the pandemic in 2020 sent a serious scare through world financial markets. But the fear didn’t last for long. The fiscal response of governments and central banks led to a swift macro recovery. By the second half of 2020, deal activity and company valuations were again on the rise, as they were throughout most of the 2010s.

That pandemic response created friendly conditions for consumer fintech startups. Stimulus checks meant that many people had plenty of cash on hand to spend or invest. That was great news for personal investing specialists such as Robinood, whose annual revenue climbed 89% in 2021. Near-zero interest rates meant that the cost of borrowing was low, making it less expensive to issue loans for online-only banks such as Chime, also known as neobanks. And the combination of increased consumer spending and low rates helped drive new business and reduce costs for buy now, pay later companies like Affirm and Klarna, which issue short-term installment loans for online purchases.

But the climate shifted in 2022, with rising interest rates and declining personal savings rates. In a downturn, things look different.

“Those tailwinds are gone,” Flager says, pointing in particular to the recent decline in savings rates and the end of the pandemic surge in consumer investing. “They’ve turned into headwinds. And at the same time, capital markets have tightened. Growth is at a premium. You’re no longer able to just spend into (growth) like you were, which breaks down most people’s forecasts, which then further affects valuations.”

Take Affirm, which has seen its public stock price fall more than 65% over the past year. Or Klarna, whose valuation fell 85% in its latest funding round. When Affirm laid off 19% of its workers in early February, CEO Max Levchin cited rising interest rates as the biggest factor. “This has already dampened consumer spending and increased Affirm’s cost of borrowing dramatically,” Levchin wrote in a statement.

How fintech business models are changing

Fintech founders and investors are responding to the shifting winds, according to Drew Glover, general partner at early-stage fintech firm Fiat Ventures. One change he cites: Attention is moving away from the once-buzzy consumer space and toward startups that provide fintech tools for other companies.

“We’re starting to see a big B2B trend popping up right now,” Glover says. “It’s the less-sexy business models and the less-sexy brands that are rising to the top.”

Glover says there can be several benefits to the B2B model in this sort of market, with venture investors renewing their emphasis on profitability and shying away from supersized investments. One perk is that B2B revenue is more likely to be subscription-based, making it easier to retain year over year. Another: While B2B accounts require much more work to win, they also come with much higher revenue potential.

“The B2B model is just a much quicker path to profitability,” Glover says. “You could close three really strategic clients, and that could turn into $20 million, $30 million, $40 million in revenue overnight.”

Some startups, of course, will continue to focus on the consumer market. Glover expects many of these B2C business models will change, too. The free or freemium model that prioritizes winning as many customers as possible is falling out of favor, he says. Instead, Glover sees companies turning to paywalls, subscriptions, and other ways to generate immediate revenue.

What’s next for fintech?

The past year’s dropoff in deal activity and valuations has been particularly steep at later stages of the startup lifecycle, where companies are more closely compared to their publicly traded peers. That means some late-stage startups would likely face significant down rounds if they raised new capital. Instead, many are trying to make do with the capital they raised during the looser funding environment of 2021.

Patience and prudence led to a quiet market. But the clock is ticking. At every stage, the average time startups are waiting between funding rounds is at its highest point in the past five years, topping 900 days at Series D. Companies are running out of runway.

“There weren’t a lot of quality [companies] in the market [last year] because they raised in 2021, they have a balance sheet, and they know the market sucks right now. So they’re going to try to last as long as they can before they go back to market,” Flager says. “I think that will change in the second half of this year. A lot of those companies tightened up and tried to get longer runways. But longer isn’t forever.”

Flager doesn’t expect the multiples that existed in 2021 to return anytime soon. But both he and Glover made it clear that they are still busy writing checks—and that they think the sky is the limit for startups that are managing to raise funds and generate revenue during the downturn.

A whole generation of well-known unicorn startups was born out of the turmoil of the Great Recession, including names like Uber, Airbnb, and Stripe. Glover believes that, in the future, we might look back at the current environment as a similar catalyst for growth in fintech.

“We’re seeing a different type of entrepreneur in the space right now,” he says. “If you want to start a business in this market, you’ve got to be a real serious player. It’s been really exciting to see this invigorated type of entrepreneur.”

The fintech market is down. But that doesn’t mean it’s out.

“This whole idea that fintech is dead—what we believe is really the opposite,” Glover says.

Learn more:

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. All product names, logos, and brands are property of their respective owners in the U.S. and other countries, and are used for identification purposes only. Use of these names, logos, and brands does not imply affiliation or endorsement. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.