Some startups are the creation of a single visionary founder. Others are the result of several co-founders coming together to combine their complementary skills.

Over the past decade, however, one type of founding team has been more popular than the rest. Since 2016, two-founder teams have consistently been the most common construction among new companies formed on Carta.

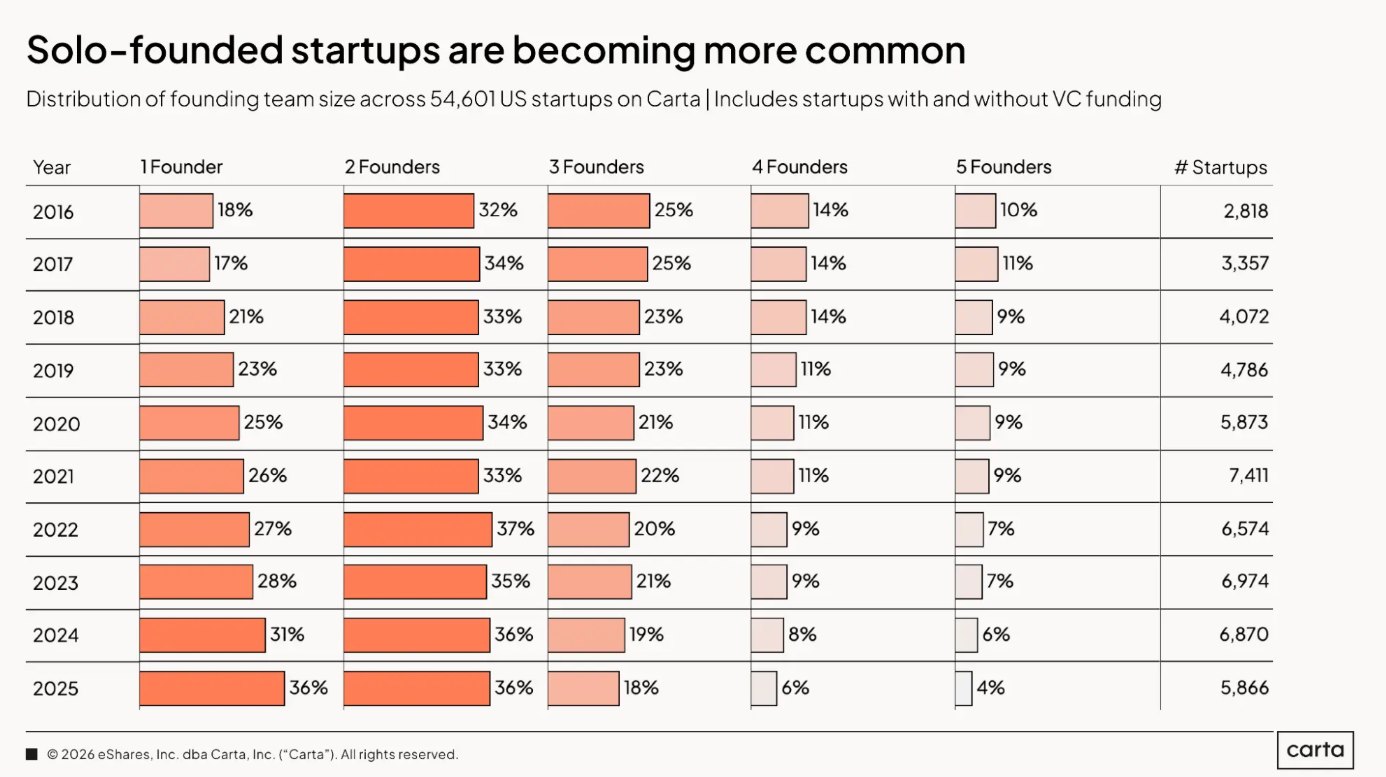

In 2025, about 36% of all new startups were founded by two-person teams, according to Carta’s latest Founder Ownership Report, in line with the historical norm. This was tied for the most common size of founding teams from last year, with another 36% of startups led by solo founders, who are becoming increasingly common in the age of AI.

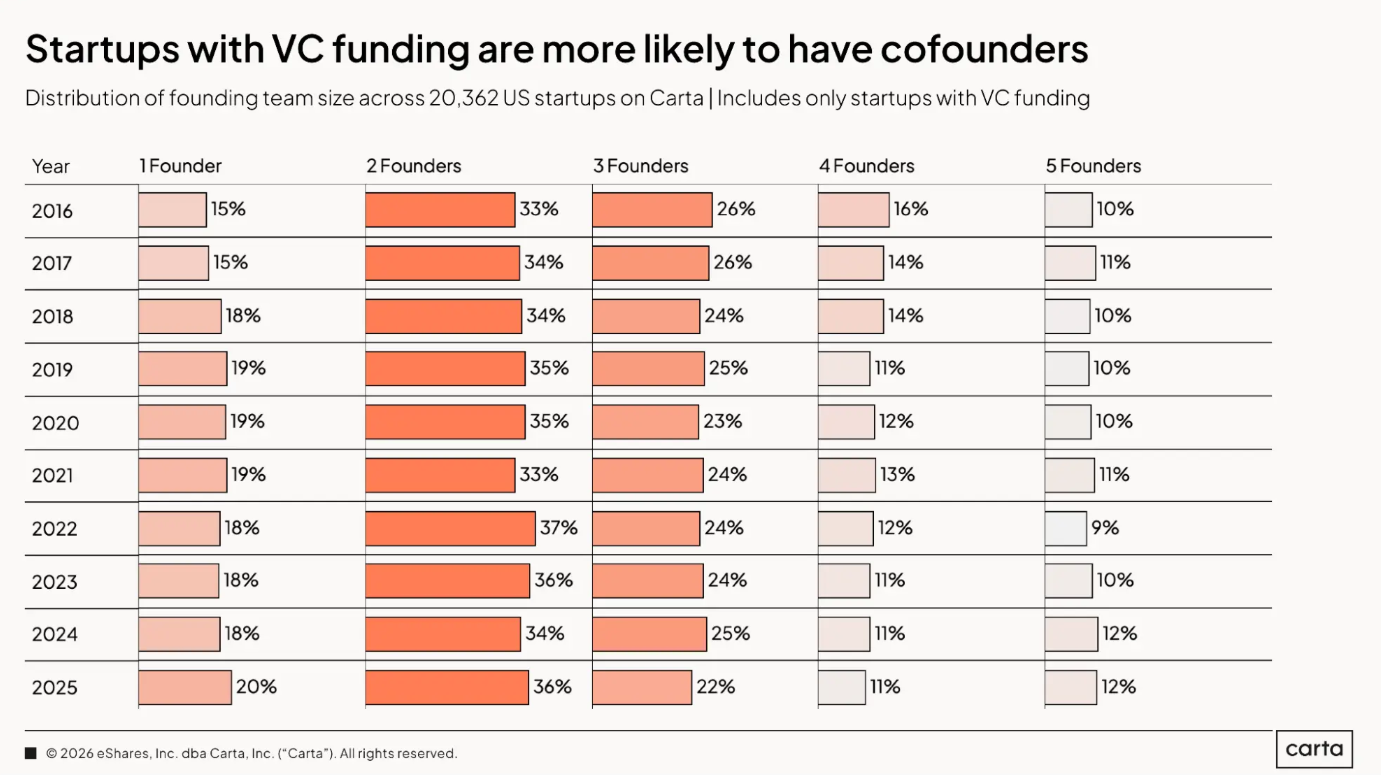

When it comes to fundraising, however, two-founder teams still dominate. Startups with two co-founders were responsible for 36% of all rounds closed on Carta during 2025, matching the percentage of newly formed companies that have two co-founders. Startups with solo founders, on the other hand, raised just 20% of rounds last year.

In terms of company formation, teams with one founder and two founders were equally common. But in terms of successfully raising VC funding, the two-founder teams were far more successful. Again, this aligns with typical industry norms: In each of the past 10 years, two-founder teams have been the dominant construction among startups that successfully raise VC funding.

The prevalence of two-founder teams hasn’t changed much over the past decade of VC fundraising. But one key variable among these teams of two co-founders has undergone a real shift. Today, the way two-founder teams choose to distribute their initial equity among themselves looks quite different than it used to.

Equity is getting more equitable

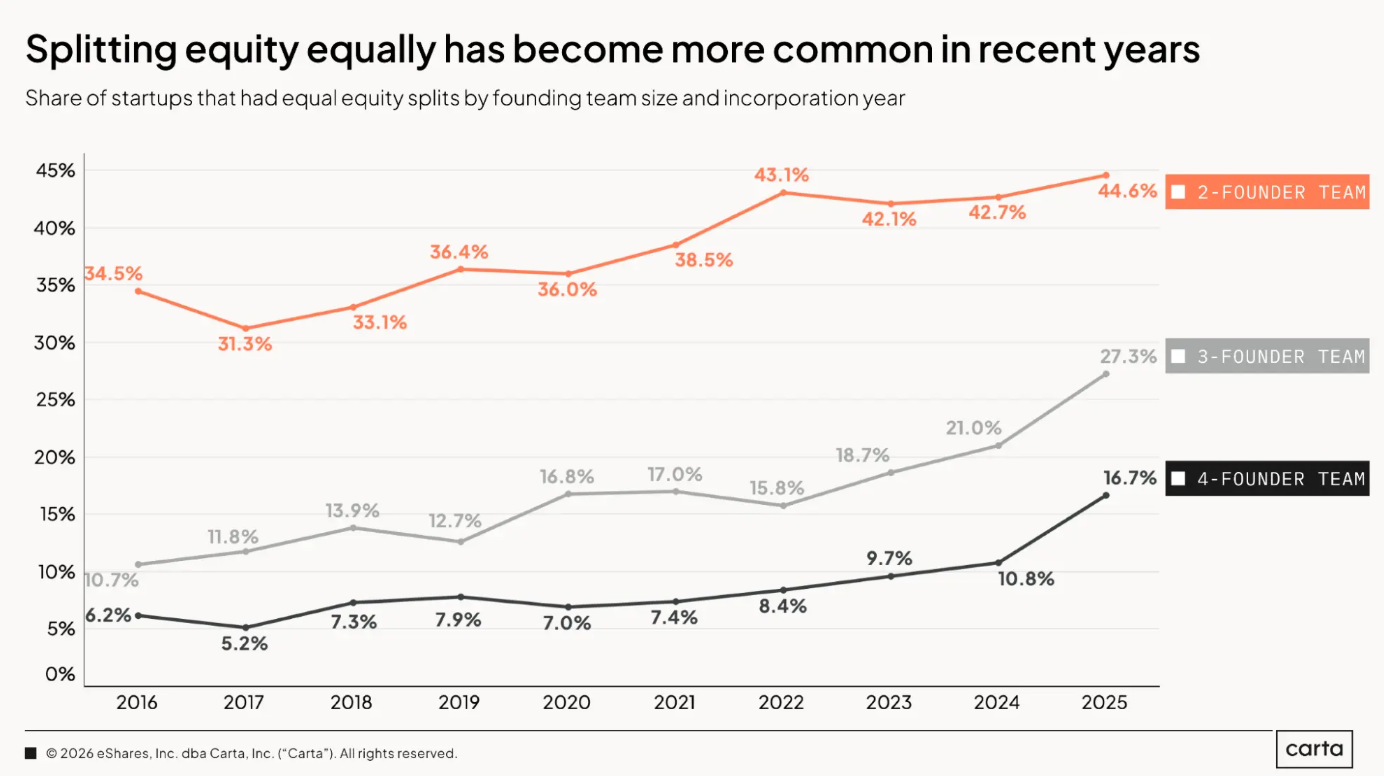

Among startups formed back in 2016, about 34.5% of two-founder teams chose to divide their initial equity equally among themselves. In the other 65.5% of cases, one of those two co-founders received more equity than the other.

By 2025, those figures had experienced a double-digit shift. Last year, the rate of two-founder teams that split their equity equally rose to 44.6%, reaching its highest point of the past decade.

This reflects a broader trend across founding teams of all sizes: An equal division of equity among all founders has also grown more common among startups with three and four co-founders. But equal equity allocations are still most common among two-founder teams.

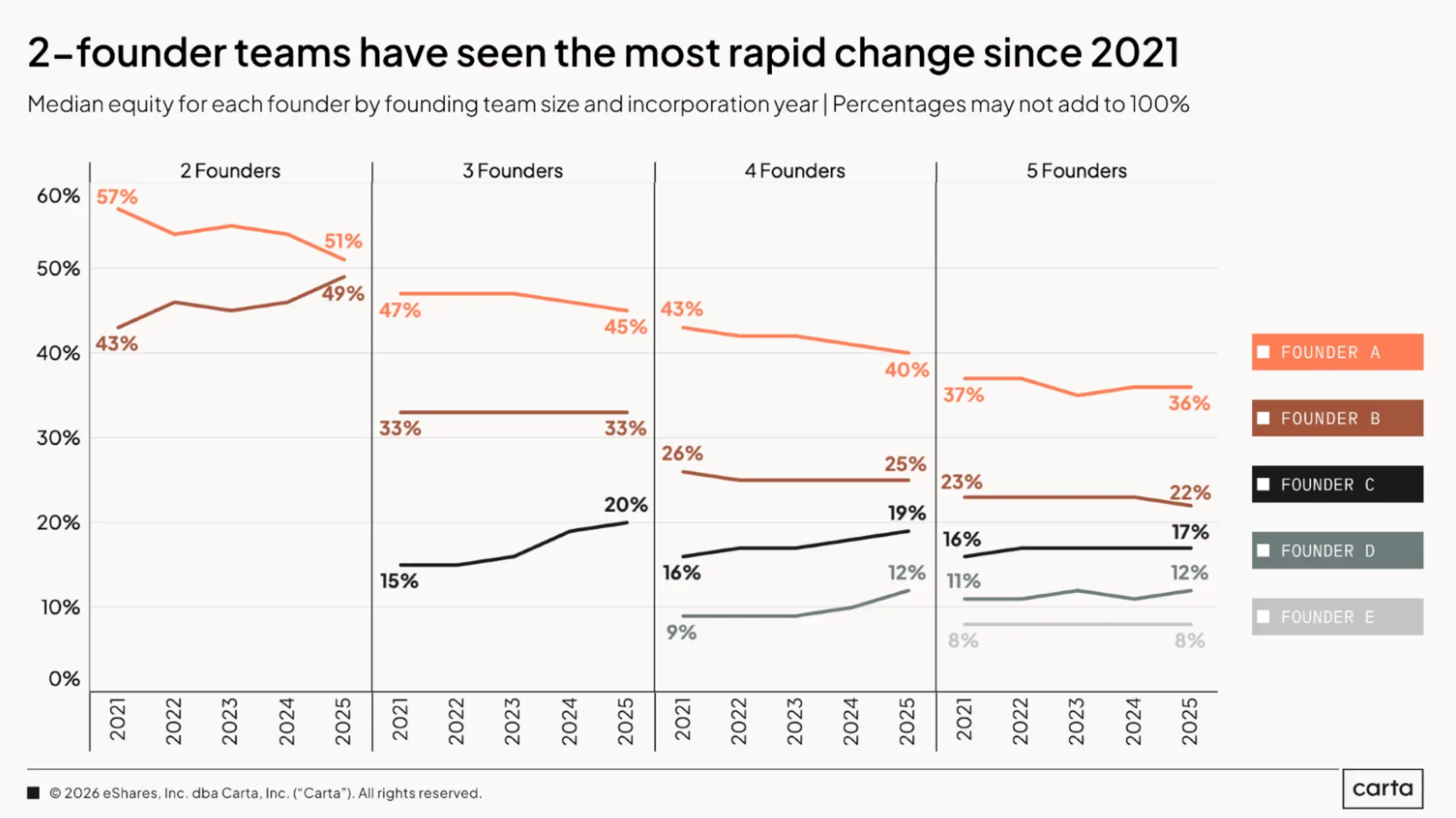

Even when two-founder teams don’t opt for a perfectly equal split of their company equity, the equity gap between the two co-founders tends to be negligible. Across all two-founder teams that formed new companies on Carta last year, the median divide of equity was 51–49. Those figures have grown substantially closer over just the past four years: In 2021, the median equity split among two-founder teams was 57–43.

For larger founding teams, the math on divvying up equity has been more consistent over the past five years—and more unequal. Among startups with three, four, or five co-founders, the lead founder still typically receives at least 10 more percentage points of equity than the next best remunerated co-founder.

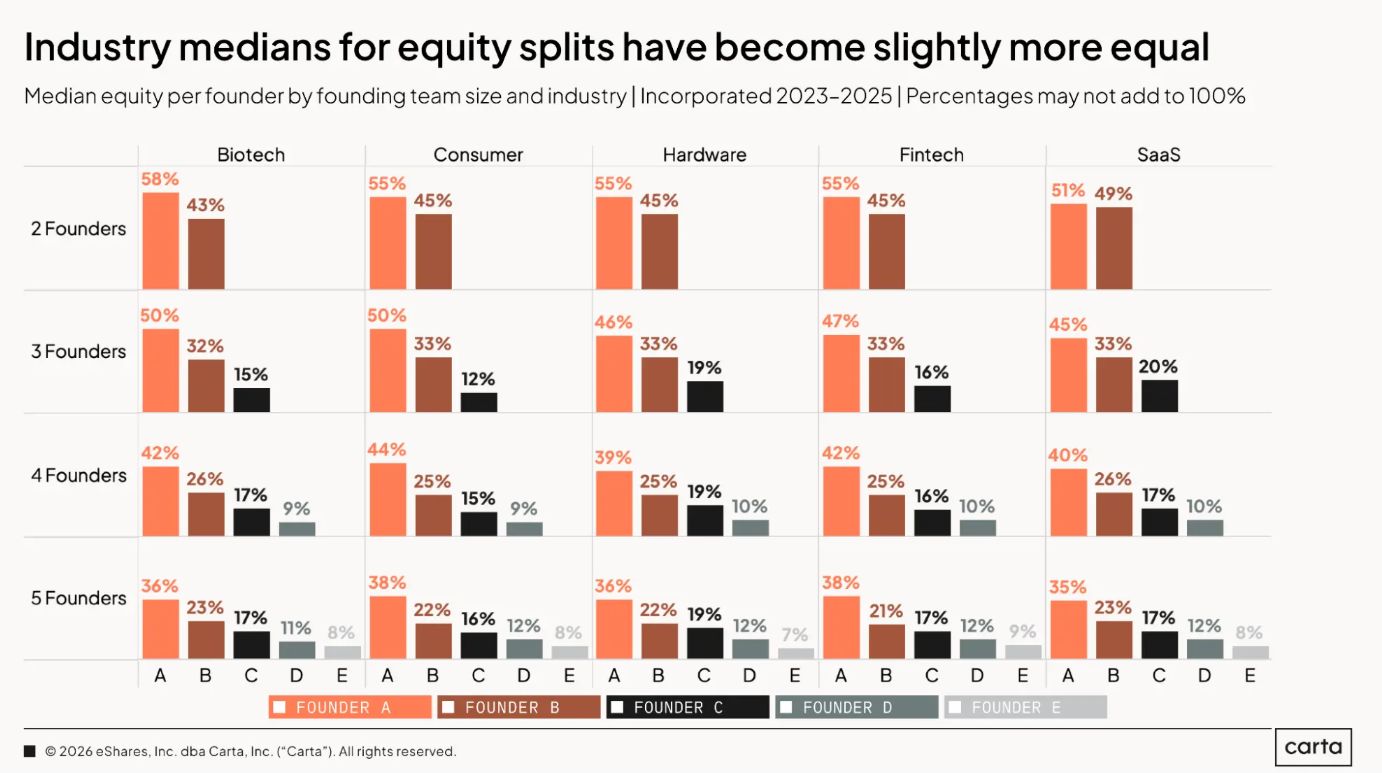

Approaches to dividing equity among founding teams differ by sector. In SaaS, the median two-founder team from the past three years has opted for a 51–49 split, the same ratio found across all two-founder teams regardless of sector. In other industries, uneven splits tend to be a little more common. This is most true in biotech, where the lead founder in a typical two-founder team receives 58% of company equity.

For biotech in particular, this may be a function of some real structural differences between sectors. Compared to SaaS, startups in biotech and other research-intensive fields are more likely to be built around intellectual property that sprouts from a single founder. When that’s the case, the founder whose research has made the startup possible is more likely to receive a larger equity stake.

When co-founders lose control—and when they break up

No matter how the members of a founding team decide to initially divide their equity, they usually don’t keep majority control of the company for long. As startups begin to raise funding rounds from VCs and issue equity to their employees, the math of ownership rapidly changes.

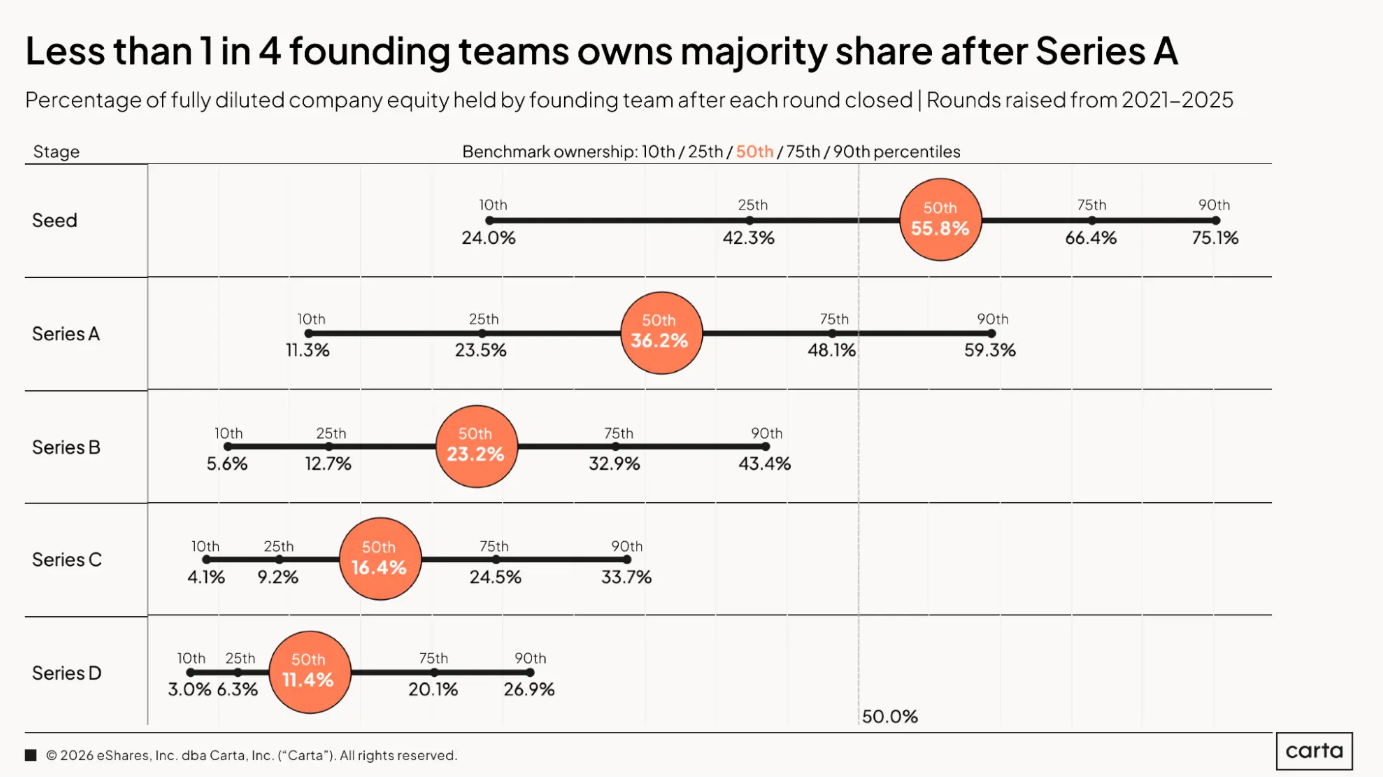

By the time a startup raises its seed round, the median founding team combines to own just 55.8% of the company’s fully diluted equity. By the time of raising a Series A, that median figure drops all the way to 36.2%.

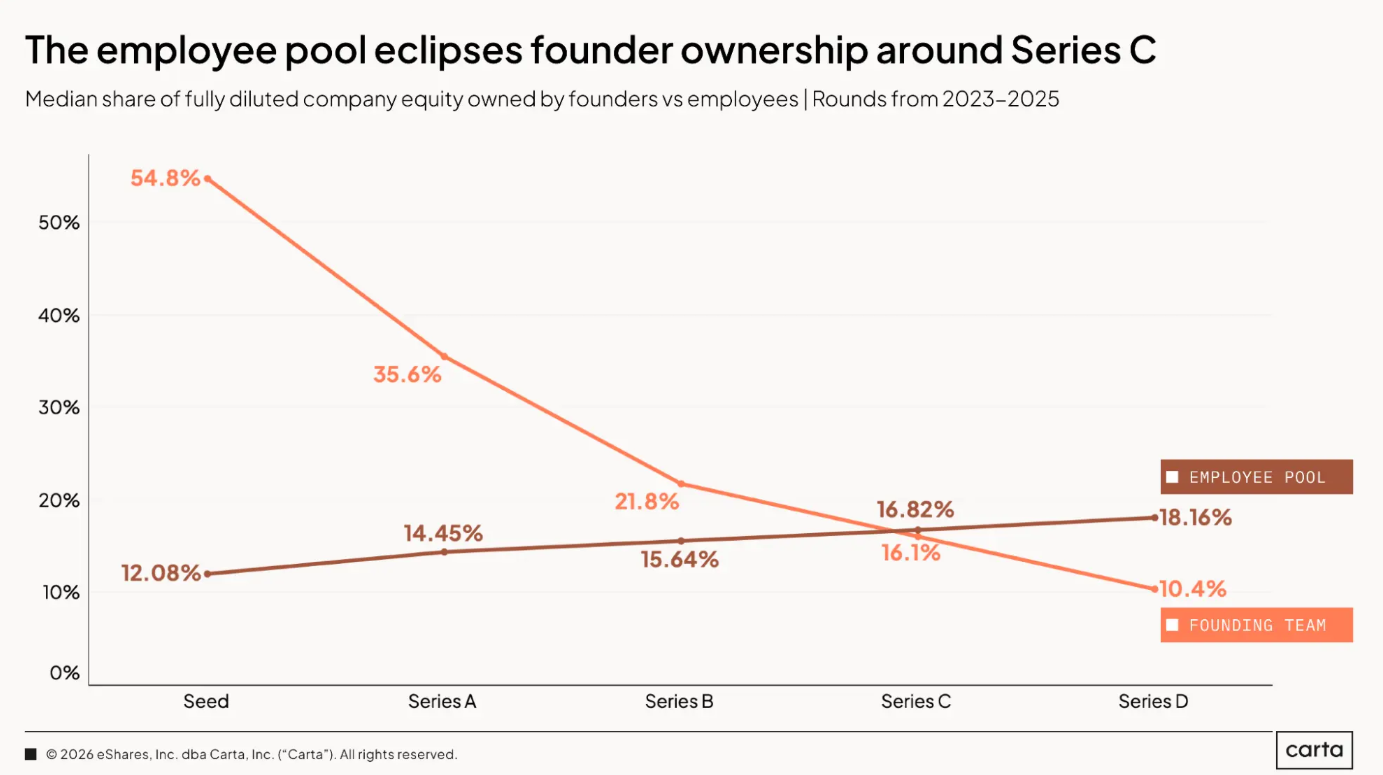

And by the time a startup hits Series C, the typical founders aren’t even the largest shareholder base within their own company. For rounds raised between 2023 and 2025 (see below), the median founding team retains just 16.1% of fully diluted equity after raising a Series C, while the median employee ownership pool rises to 16.8% at the same stage.

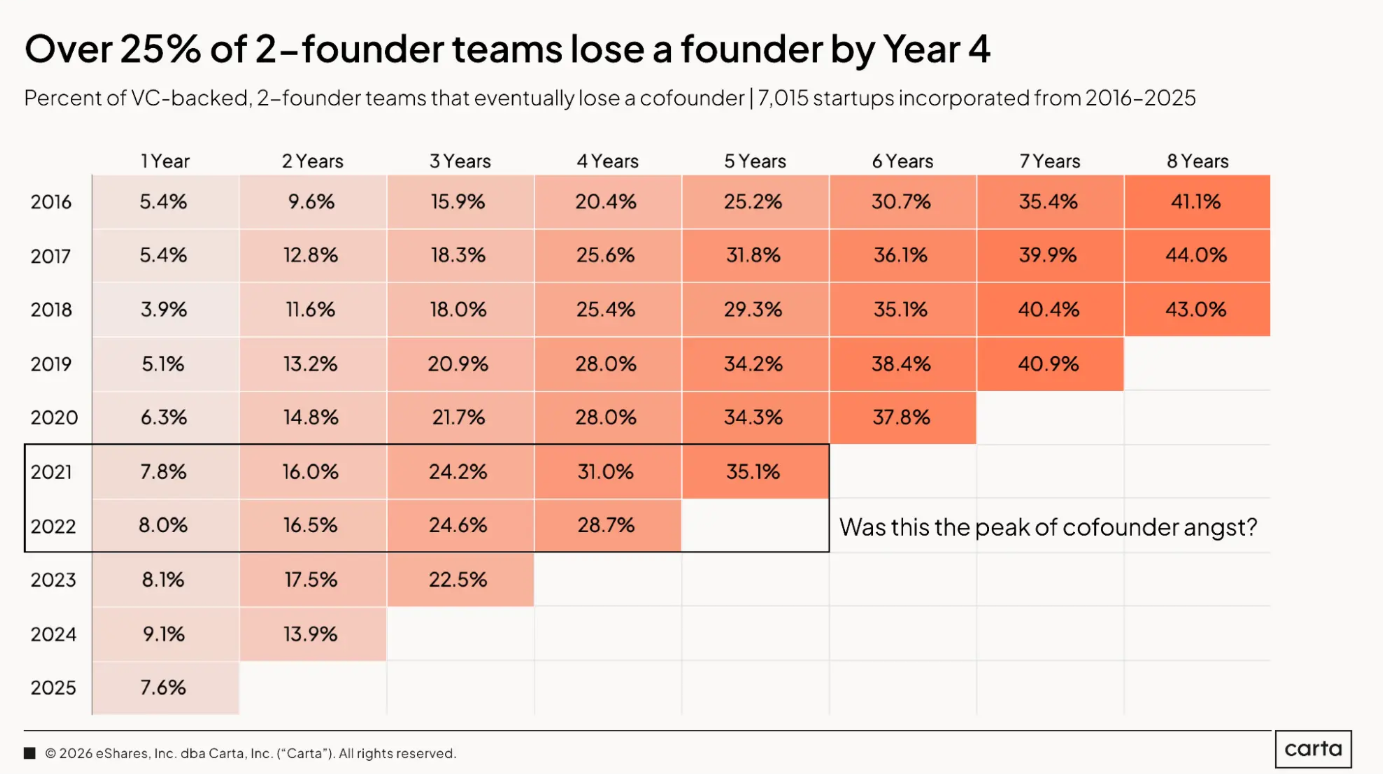

Most two-founder teams stick together for many years—long enough to proceed through multiple stages of venture fundraising, if all goes well. But a significant portion do not.

Among startups founded from 2016 to 2021, somewhere between 25% and 35% of two-founder teams had parted ways after five years, depending on the exact year of founding. Among startups founded from 2016 to 2018, more than 40% of two-founder teams experienced a breakup within eight years of forming their company.

By definition, this statistic is a lagging indicator: As we’ve seen, those companies formed in the mid-2010s were created in a different environment than the new crop of startups being launched in 2026. Will the more equitable approach to distributing equity that has emerged in recent years encourage two-founder teams to stick together for longer than they used to? To find out, we’ll have to be patient. Check back in the 2030s.

Subscribe to the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.