Two years ago, the entire market for investing in private startups was in a slump. Tender offers were no exception. Between the end of 2021 and the end of 2022, the quarterly count of new tenders administered by Carta fell by 74%.

In recent quarters, however, interest in these transactions has begun to rebound.

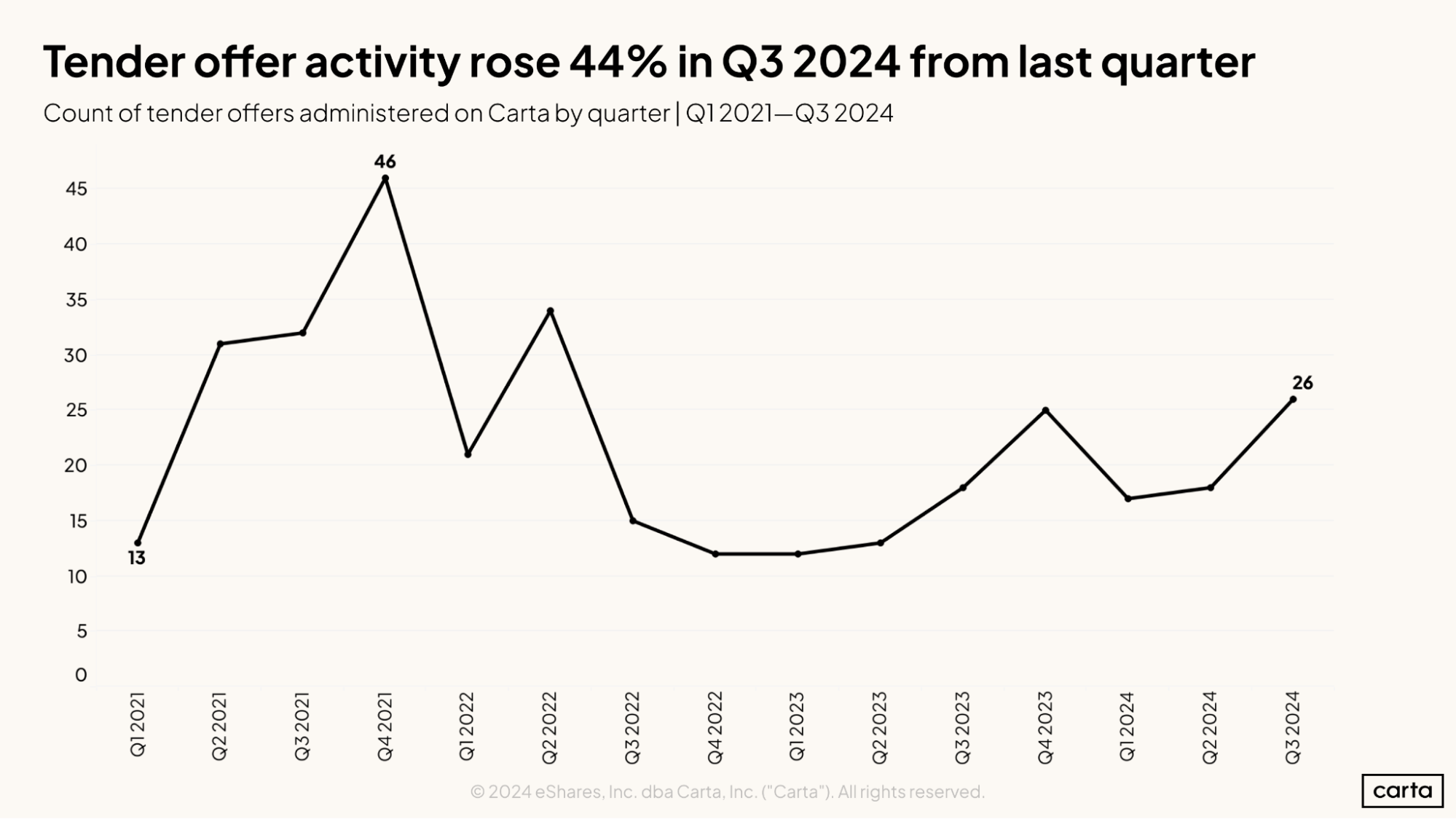

Dating back to Q2 2023, the number of new tender offers administered by Carta has now increased in five of the past six quarters. That includes Q3, which saw 26 new tender offers—the highest quarterly total since the middle of 2022, when the market was still feeling the heady effects of the recent venture boom.

Jamie Hutchinson, a partner in the private equity group at Goodwin, expects that momentum to continue, with plenty of other transactions in the pipeline.

“The market for tender offers is very busy,” says Hutchinson, who frequently works with clients on tenders and other secondary transactions. “Since January 1, it’s probably been busier than we’ve ever seen.”

This resurgence in activity isn’t the only way that the landscape for tender offers has shifted. Just as the wider venture market has undergone an evolution in the past few years, so has the role of tender offers, too.

Early stage vs. late stage

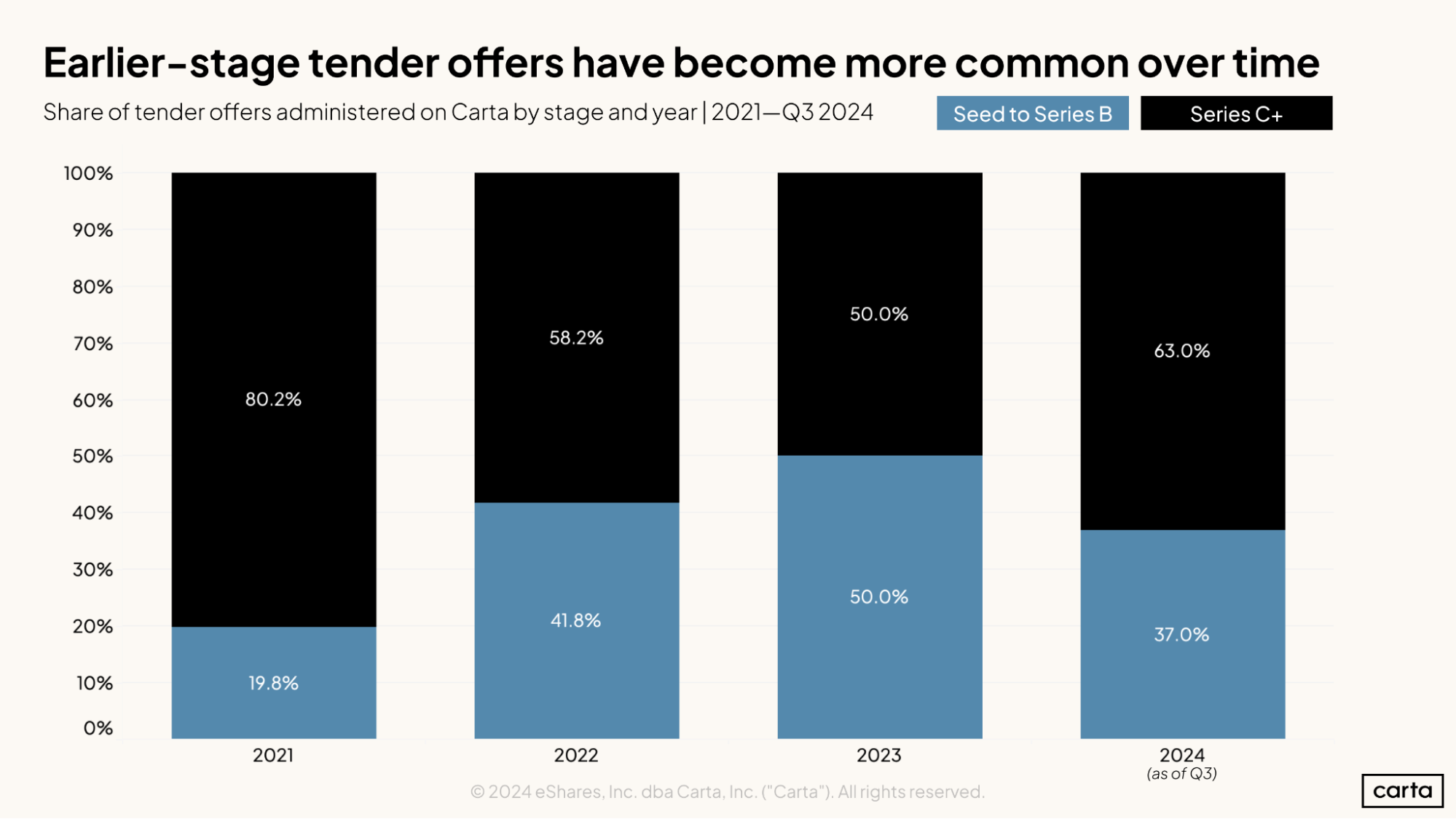

During the boom year of 2021, more than 80% of tender offers administered by Carta were conducted by companies at Series C or later, and less than 20% by companies at Series B or earlier. Over the next two years, this divide changed considerably. By 2023, tender activity was split evenly between early-stage and late-stage companies.

This shift in activity toward earlier stages mirrors what occurred in the market for new primary venture rounds, where activity fell off much more sharply at later stages during the recent venture slowdown. From 2021 to 2023, the total number of new primary rounds on Carta at the seed stage through Series B declined by 34%. The number of rounds at Series C and later, meanwhile, fell by 55%.

As the number of tender offers has ticked up in 2024, activity has again shifted back toward later-stage startups. Over the past few years, there’s been a clear correlation: When more tenders are taking place, a higher percentage of those tenders come from late-stage companies. When the market is cooler, the balance of tender activity shifts toward younger startups.

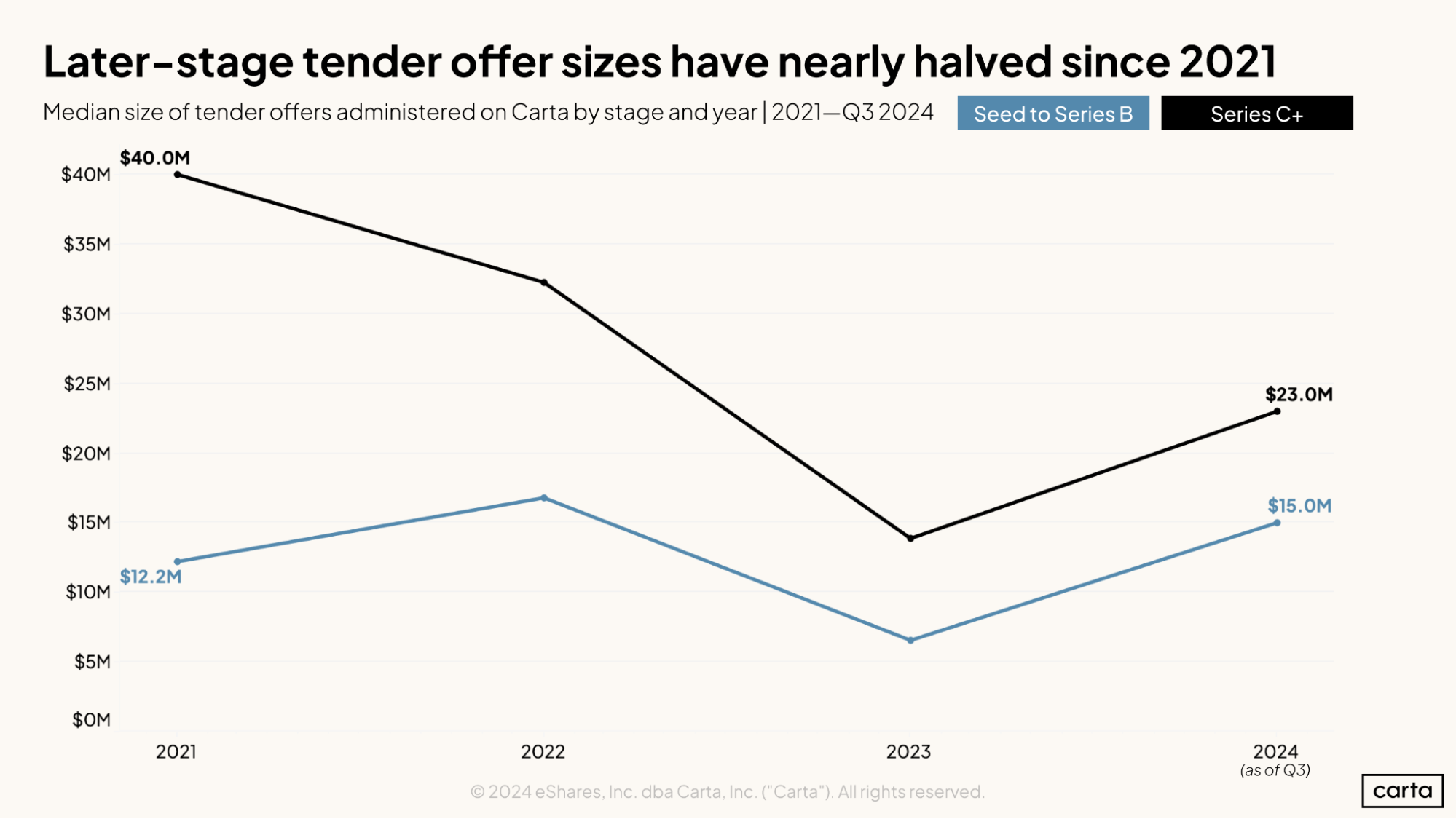

Offering sizes are increasing in 2024

While late-stage tenders grew less common, they also got smaller.

In 2021, the median tender offer among companies at Series C or later saw $40 million worth of shares change hands. By 2023, that number had dipped by some 65%, falling all the way to $14 million.

The same decline in tender size occurred among earlier-stage companies, but to a lesser extent. For companies at Series B or earlier, the median tender size fell 46%, from $12.2 million in 2021 to $6.6 million in 2023.

So far this year, median offering size has increased across tenders of all stages; for companies at Series B or earlier, the median is now higher than it was back in 2021. But there exists a wide range of transaction sizes across the spectrum of tender offers.

“We’re seeing some big tender offers in terms of dollar volume, but we’re seeing an equal number of smaller ones—say, $5 million to $10 million,” Hutchinson says. “A lot of those smaller offers have come from companies at Series B or Series C. But the big ones are usually the late-stage unicorn set.”

Ready buyers, willing sellers

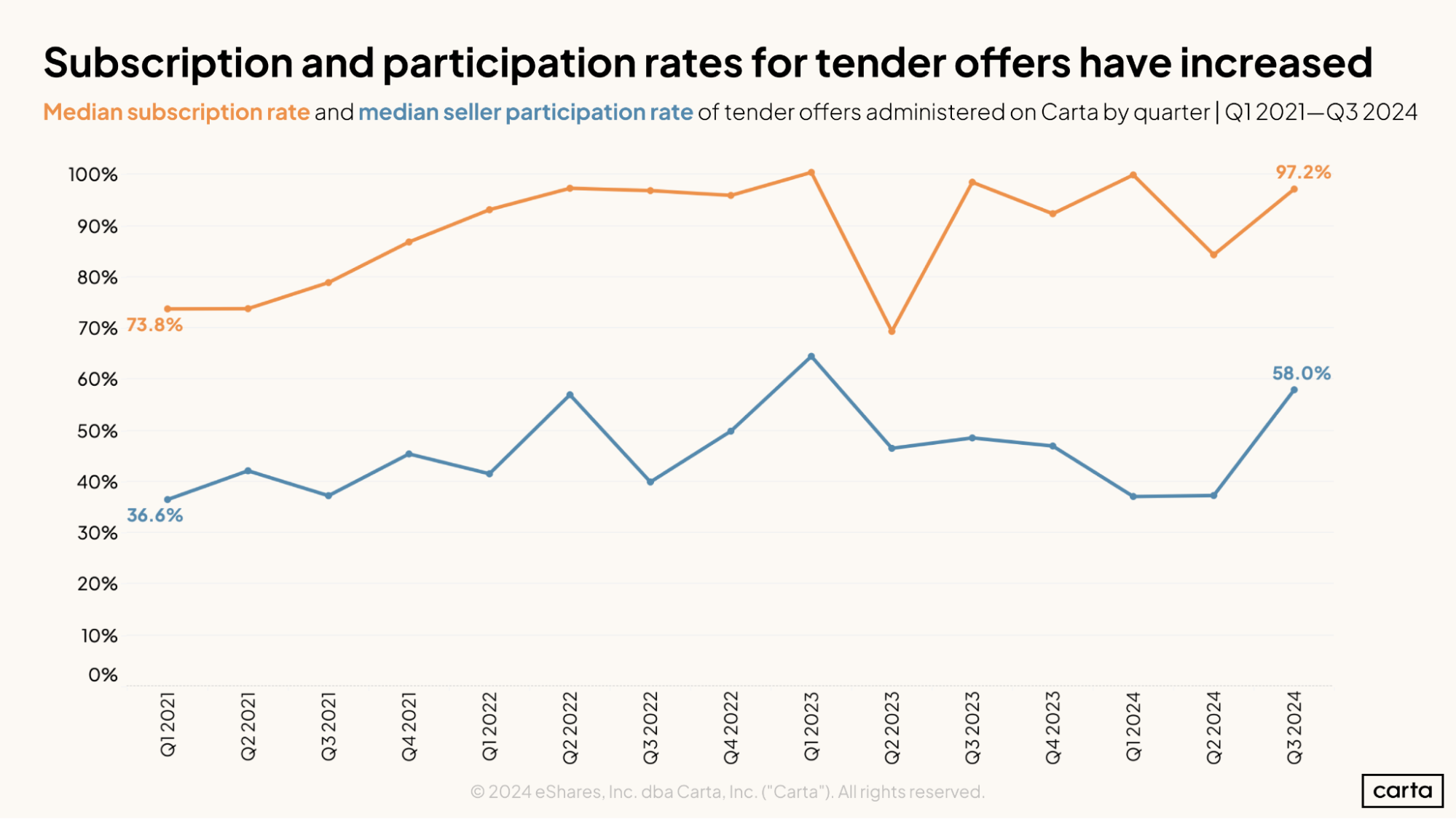

The uptick in volume and median size of tender offers this year suggests growing buyer interest. Other metrics indicate that overall seller interest is on the rise, too.

Subscription rate measures the amount of demand from potential buyers that was filled by eligible sellers. A 100% subscription rate means that sellers were willing to supply 100% of the shares that buyers wanted to purchase. Participation rate, meanwhile, tracks the percentage of eligible sellers who choose to sell shares in the listing. It’s calculated as the number of participating sellers divided by the number of stakeholders invited to sell.

These numbers soared in Q3 2024: Among tenders administered by Carta, the median subscription rate and median participation rate both climbed by more than 10 percentage points last quarter alone, and both are now up more than 20 percentage points compared to the start of 2021.

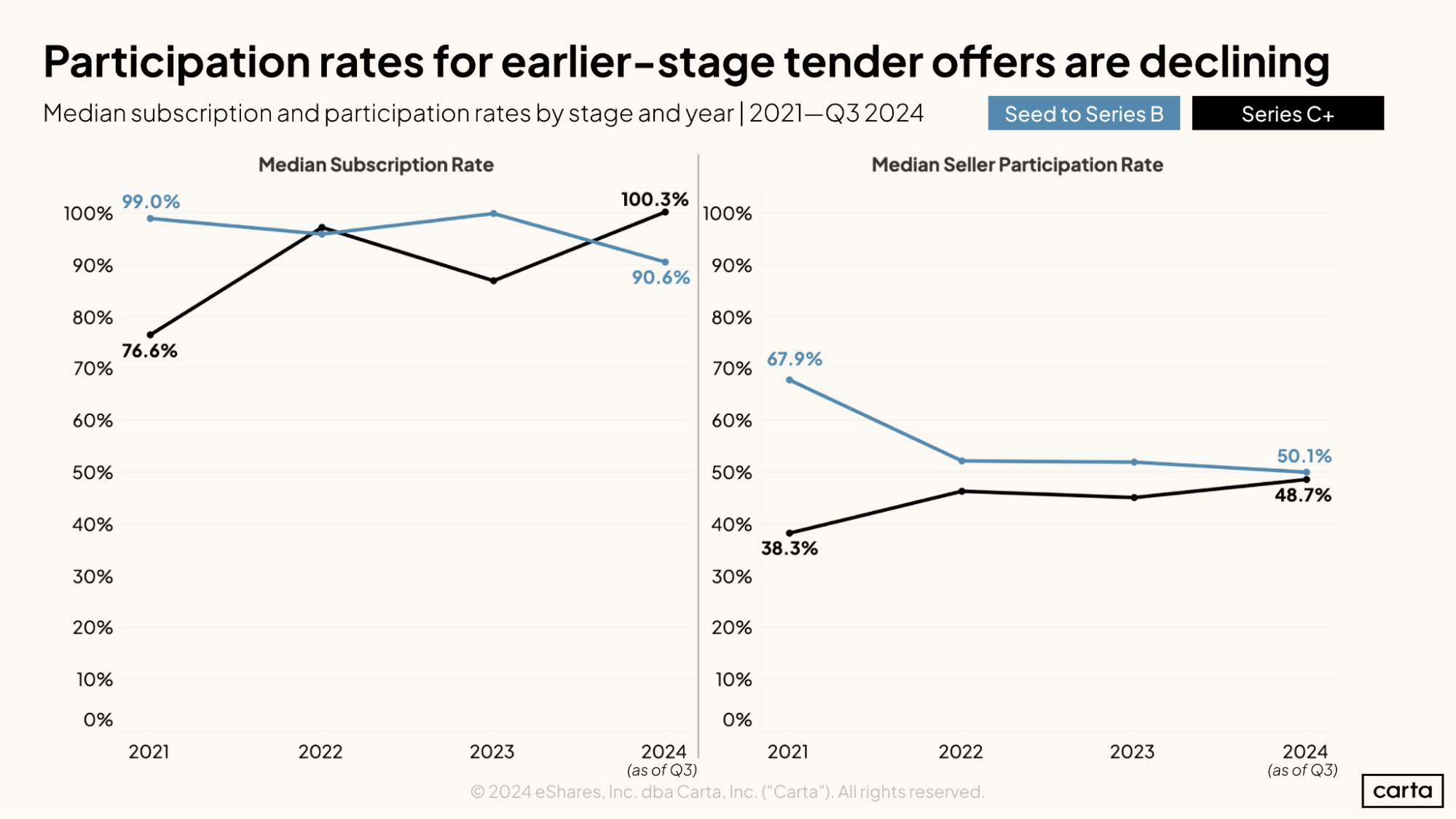

This is not, however, a secular trend across all stages. In fact, the median subscription rate and participation rate are both trending down on tenders involving startups at Series B or earlier and trending up on deals at Series C or later.

So far this year, later-stage companies have been more likely to achieve full subscription in their tender offers than earlier-stage startups, a reversal from 2023. In 2024, the median subscription rate on tender offers at Series C and later is 100.3%, which means that shareholders want to sell more shares than buyers are willing to acquire.

From 2022 on, participation rates among early-stage tender offers and late-stage tenders have been approaching parity. Shareholders at earlier-stage companies are less willing than they were in 2021 to sell off their shares, potentially indicating a greater appetite to wait for company growth before seeking liquidity. Shareholders at more mature startups, meanwhile, have grown more likely to sell at least some of their shares when they have the chance.

Part of this increase, surely, is due to a pent-up desire for liquidity among shareholders: With so few IPOs taking place, tender offers can be an attractive opportunity to take some money off the table.

More liquidity to come?

When Hutchinson looks back at some of the ways the private market has shifted in the past two years, he sees a familiar pattern.

First, there was an economic slowdown and a decline in venture and growth equity transactions as valuations reset. This led to a reduction in deal activity of all kinds—including M&A and IPOs—as both companies and investors adapted to a new normal. After the market began to settle, and with exit opportunities still scarce, the strongest companies began to conduct more tender offers to generate liquidity.

Hutchinson first saw this story play out in the aftermath of the 2008 global financial crisis. Back then, the increase in tender offers helped prime the market for an upswing in IPO activity. Heading into 2025, he expects the same thing will happen again.

“I think there’s a direct correlation between tenders and IPOs,” Hutchinson says. “If history repeats itself—which it tends to—this moment of time tells us that a year to a year and a half from now, we will be seeing an increase in IPOs.”

But that doesn’t mean tender offers are going anywhere. Recent rises in deal volume, offer size, participation rate, and subscription rate indicate that interest in tenders is high. With companies staying private for longer and liquidity needs continuing to increase, Hutchinson expects tender offers will continue to proliferate among private companies and the investors who specialize in these private liquidity transactions.

“It’s just become a normal part of the emerging company story,” Hutchinson says. “It used to be a little extraordinary—only certain companies could do tender offers resulting in liquidity for employees and early investors. Now, it’s just part of the plan.”

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.