The typical venture capital fund raises investment from dozens of different limited partners (LPs). Not all of these LP investments are created equal.

Some LPs invest different amounts of capital than others. The LP that makes the biggest commitment to a VC fund—or, in some cases, multiple LPs—is referred to as the anchor investor, or anchor check.

For a VC fund manager, finding an anchor investor is often a critical early step in the fundraising process. This anchor check can provide a strong financial base for the rest of the fund, and a consequential investment from a key LP can send a strong signal to the rest of the market about a new fund’s viability.

The relationship between a fund and its anchor investor is often more than financial. As a fund matures and begins to make and manage investments, some anchor LPs take on an active strategic role, such as by serving on a fund’s Limited Partner Advisory Committee (LPAC).

“The anchor investors tend to be the largest, they tend to be first, they tend to be most involved, and they tend to be a thought partner,” says Sam Jones, partner at Torch Capital, a VC firm focused on consumer tech. “They’re more than just capital.”

>> Learn more: Read our 2024 VC Fund Performance report.

Anchor checks are getting bigger

Writing an anchor check in a new VC fund has always been a big commitment. In recent years, however, it’s getting even bigger.

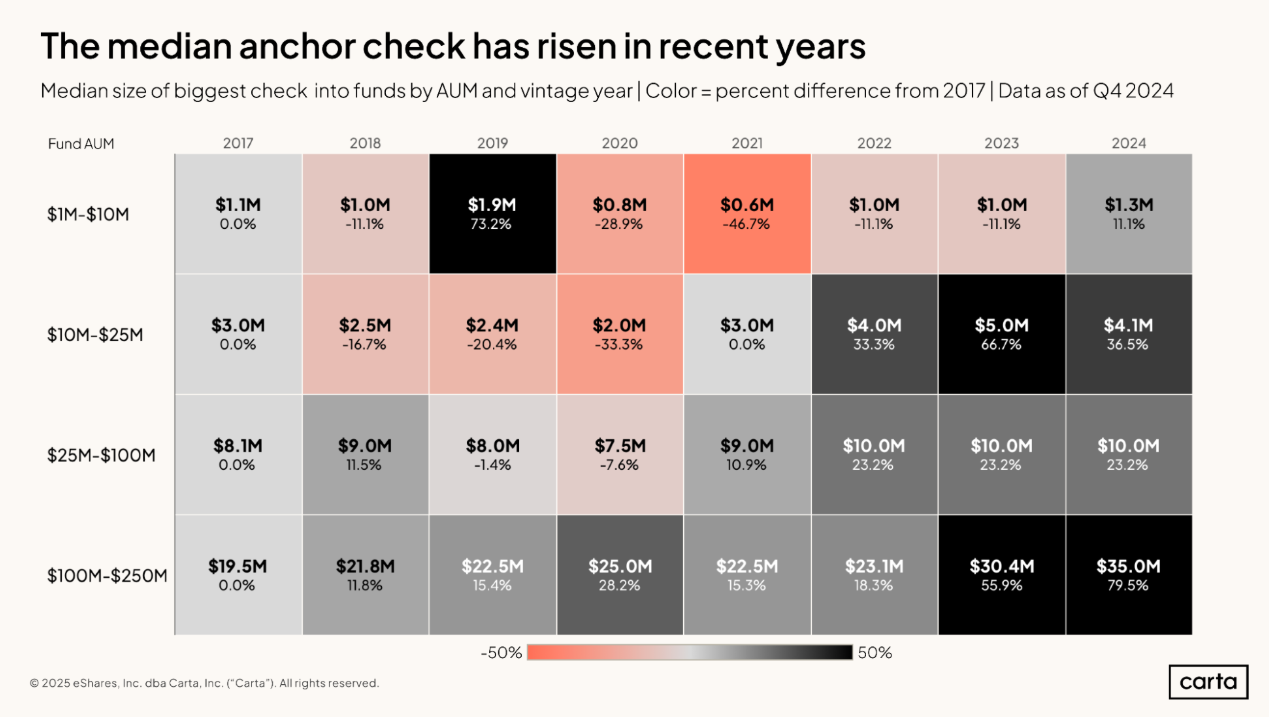

Compared to the late 2010s and early 2020s, the median anchor check among newly closed VC funds tracked on Carta was on the rise in 2023 and 2024 among funds of every size. In some cases, this growth is significant.

For funds with between $100 million and $250 million in assets under management, for instance, the median anchor check was $35 million in 2024. That’s 79.5% larger than it was in 2017. For funds with between $10 million and $25 million in AUM, the median anchor check has grown by 36.5% over the same span.

For smaller funds, this recent increase in size comes after anchor checks had been getting appreciably smaller in prior years. Among that same group of funds between $10 million and $25 million, the median anchor check had previously declined by 33% between 2017 and 2020.

This distinct growth in the size of anchor checks between the early 2020s and the past two years makes sense to Jones. Over that span, the venture market has undergone a transformation, one that was sparked by a broad-based decline in valuations that began in 2022. This made the VC asset class less attractive to some LPs, particularly those who had flooded into the space during the boom years of 2020 and 2021. After all, lower valuations tend to result in lower returns.

This meant fewer LPs were writing checks to VC funds—and those funds that did raise cash from LPs had to meet a higher bar. Different investors may take very different approaches to fund construction, but for various strategic reasons, fund managers tend to seek a diversified base of LPs, with no single LP playing too large a role. Faced with fewer fundraising options, however, managers might be inclined to lean more heavily on key investors.

“In many ways, it hasn’t been the most venture-friendly market over the last couple of years,” Jones says. “I think from a GP perspective, being able to accelerate your fundraise with a larger initial check is a very helpful way to move through the fundraising process at a more accelerated speed.”

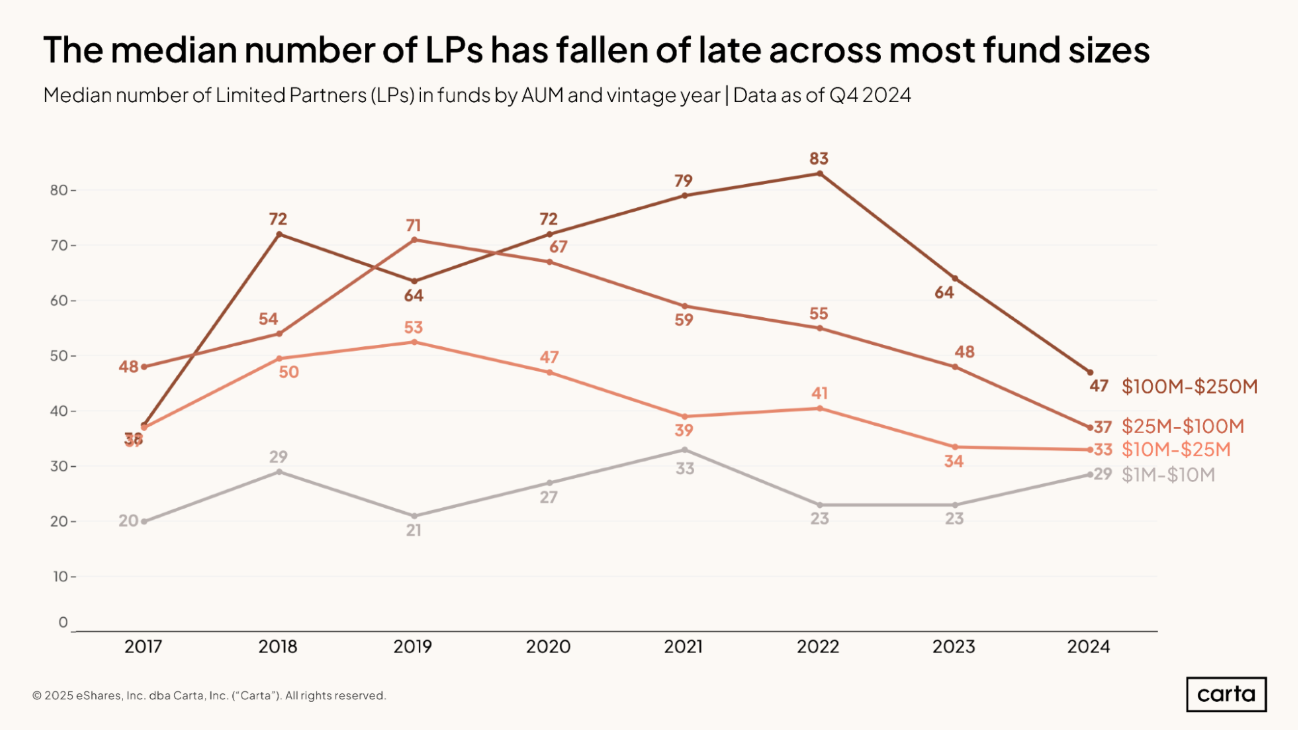

Recent funds have fewer LPs

This contraction of the active LP universe is apparent in other ways, too. For funds of most sizes, the median number of LPs investing in new vehicles has been declining since 2022.

The biggest dropoff is among the biggest funds. In 2022, the median fund with between $100 million and $250 million in AUM had 83 LPs. In 2024, the median fund in the same size interval had just 47 LPs, a decline of 43%.

The LPs who invest in VC funds come in many shapes and sizes. Some are large institutional investors, such as state pension plans or university endowments. Some are family offices. Some are high-net-worth individuals investing their own capital.

In the past two years, Jones says, those in the latter group have been more likely to pull back from investing in new VC funds. Compared to a truly long-term investor such as a pension plan, these individual investors might be more inclined to maintain financial flexibility when the market starts to ebb.

Individuals are also less likely than other LP types to be anchor investors. Rather than one or two high-net-worth individuals writing very large checks, it’s more common for VC funds to include several smaller checks from their high-net-worth LPs.

“For a VC fund, high-net-worth individuals tend to be smaller tickets and higher volume,” Jones says. “In this environment, they’re just being more conservative. They’re less willing to tie up long-term capital.”

Signing up for the long haul

There are many LPs, however, with long-term commitments to the VC asset class. When an LP writes an anchor check for a new fund, they often do so with the hope that it will be a fruitful relationship for many years to come.

If a new VC fund is successful, the fund manager may very well raise a second fund a few years in the future, and perhaps more funds after that. If an anchor LP is happy with one fund’s performance, they often sign on to write anchor checks for future funds in the series, too.

“Most people are coming into the fund with the idea of supporting the next two, three, four funds,” Jones says.

At the most basic level, finding an anchor investor is beneficial for a fund manager because it results in a big check. But a strong relationship between a GP and an anchor LP can produce much more. And it has the potential to persist for many years to come.

“There’s no doubt that having an anchor investor is a critical piece of a fundraise,” Jones says.

Sign up for the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.