- A guide to private credit financing for private companies

- What is private credit financing?

- Private credit vs. other types of financing

- Types of private credit

- Senior debt

- Mezzanine debt

- Distressed debt

- Venture debt

- Special situations lending

- Asset-based lending

- Secured loans and unsecured loans

- Why private credit financing appeals to companies

- Flexible terms

- Easier access to capital

- Higher leverage

- Disclosures and oversight

- What are the risks of private credit for founders?

- Conclusion: Private credit is on the rise

- Frequently asked questions about private credit financing

- Can an early-stage startup get private credit?

- What is the difference between private credit and venture debt?

- How does private credit affect future fundraising?

Private credit is a rapidly growing segment of the private markets that functions as an alternative to traditional bank loans or public debt markets for private companies. Compared to these other debt financing options, private credit financing can provide borrowers a higher degree of financial flexibility, including more customizable loan terms and repayment schedules.

In the 2010s and early 2020s, privately held companies have increasingly turned to private credit as a way to fuel their growth. Today, experts place the size of the global private credit market at more than $1 trillion, with plenty of room for expansion on the horizon.

What is private credit financing?

Private credit financing is a type of corporate financing in which companies raise loans from non-bank lenders such as specialized private credit firms, asset managers, private equity (PE) firms, or hedge funds. While many types of companies can and do raise private credit, this type of lending is often associated with the private markets, particularly PE-backed companies. Private credit has become a common source of the loans that many PE firms use as a key component in leveraged buyouts.

Because a private credit loan does not typically involve broad syndication, the lender and borrower can negotiate terms directly to meet their specific needs, rather than structuring the loan so it will attract other investors. Some of the key points of negotiation can include interest rates, repayment schedules, covenants, and collateral requirements.

Private credit vs. other types of financing

To better understand how private credit financing works and its place within the economy, consider some of the other ways in which companies can raise new financing:

Public equity financing is when a publicly traded company issues and sells new shares for trading on a stock exchange, such as the NYSE or Nasdaq. Anyone with access to a brokerage account can invest in public equity.

Private equity financing is when a company issues and sells new stock through a privately arranged transaction, such as a venture capital (VC) round. The two main segments of PE are the VC market and the buyout market, which is also commonly referred to on its own as “private equity.” Most investments in this space come from funds that are raised specifically for the purpose of investing in private companies, such as VC funds and buyout funds.

Public debt financing is when a company issues bonds or other debt instruments that may or may not trade on a public exchange such as the NYSE Arca or via the over-the-counter market. Capital for public debt comes from public investors, and the trading price of public debt products varies to reflect investor confidence in the borrower’s future ability to maintain payment and market interest rate expectations, among other factors.

Bank lending is when a company raises debt through a bank. For borrowers, this has historically been the primary alternative to public debt. Most commonly, a bank first agrees to make a private term loan or revolver to a company, then, if the commitment requirement is substantial, raises the capital by syndicating the loan among other lenders. These loans are historically raised, negotiated, and syndicated on a deal-by-deal basis.

Private credit has gained significant traction relative to traditional bank debt since the 2008 financial crisis, driven largely by regulatory changes that constrained bank lending and made it more costly. This caused many banks to scale back their lending to middle-market companies, particularly those with higher leverage or unconventional financial profiles, and increased demand for the flexible financing offered by private lenders.

Private credit has fewer disclosure requirements than public credit, which can make private loans simpler for in-house finance teams to organize and execute. Private credit also tends to be a less liquid market than public credit, in the same way that PE is less liquid than public equity markets.

Types of private credit

Several different types of loans and debt instruments fall under the umbrella of private credit. These different loans typically serve different purposes, and from the perspective of an investor, they come with varying levels of risk and expected yield.

A company might raise multiple types of private credit at different points in time, and it might have multiple types of private loans on its books at the same time. For instance, a company might bring on venture debt funding when it’s a late-stage startup trying to fuel pre-exit growth, then raise senior debt and mezzanine debt as part of a leveraged buyout (LBO) that serves as an eventual exit.

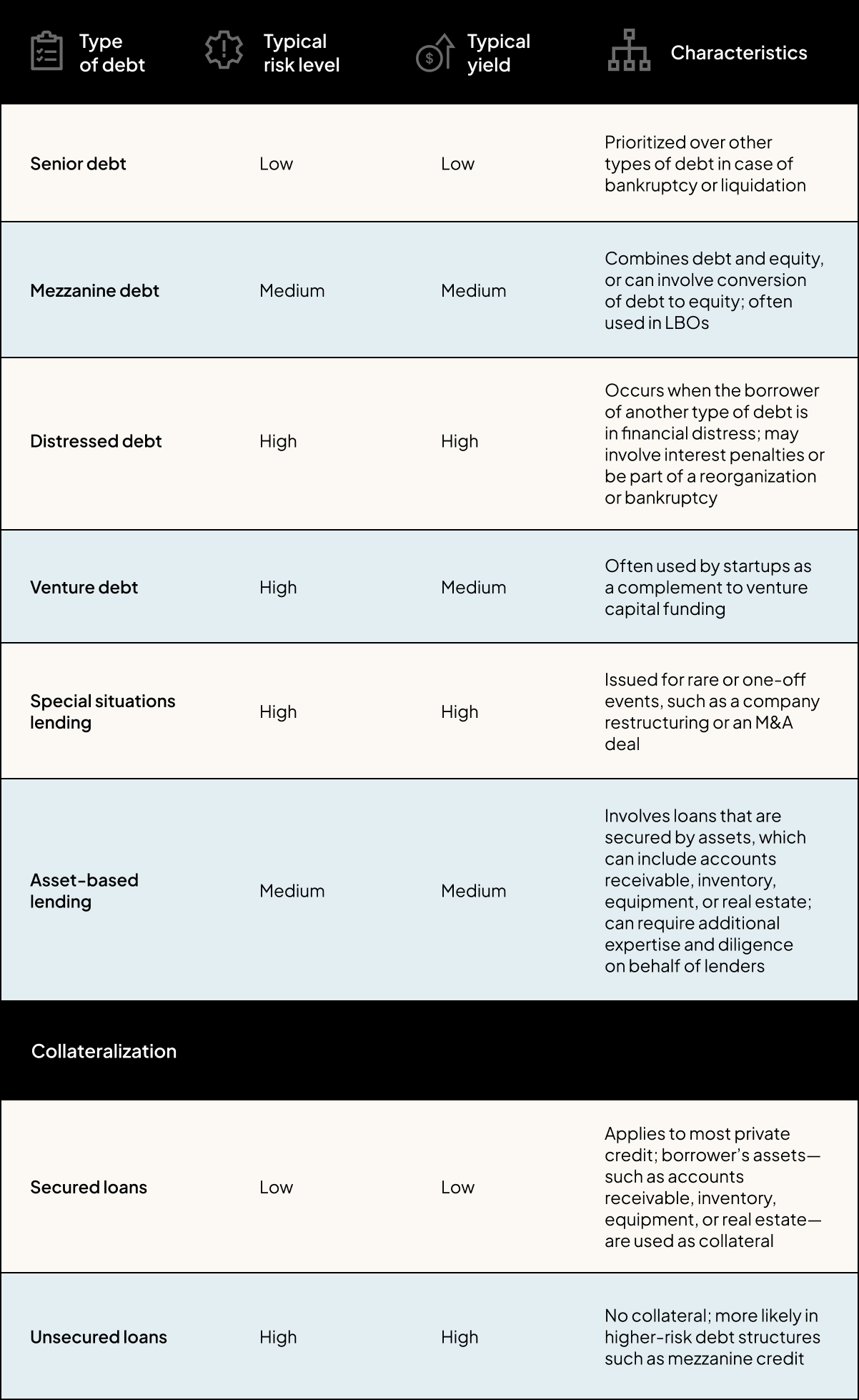

Senior debt

Senior debt is a loan that takes priority over other debt issued by a company in the event of a bankruptcy or liquidation. If a company goes out of business and has limited assets to pay back its lenders, any holders of senior debt will be made whole first, before holders of more junior debt receive any return. Because of this prioritization, senior debt is seen as the least risky place to invest in a company’s capital stack. Lenders may negotiate for senior debt status based on the amount of capital they’re providing, the quality of the collateral backing the loan, or their bargaining position in the transaction.

Mezzanine debt

Mezzanine debt is a type of issuance that combines debt but without the priority of senior debt. It is subordinate to senior debt in the capital stack, which means that if a company liquidates, senior debt holders are paid back before mezzanine debt holders. This often makes mezzanine debt riskier than senior debt. To compensate for this risk, mezzanine debt also frequently has higher yields than more senior debt products.

Mezzanine debt often includes some mechanism by which the loan might convert to equity or the lender might otherwise acquire equity in the company. PE investors frequently use mezzanine debt to help finance leveraged buyouts.

Distressed debt

Distressed debt refers to debt issued by a company that is either in default or experiencing some other form of financial difficulty. Distressed debt is typically rated below investment grade, and because of this, they often offer higher yields. Compared to other forms of debt, there’s a higher-than-normal chance that an investment in distressed debt will zero out, and because of this increased risk, distressed debt also typically brings the potential for higher-than-normal returns.

Unlike senior debt or mezzanine debt, distressed debt is not a particular type of debt that a company chooses to issue. Almost any type of debt product that’s issued might eventually become distressed debt if the issuer fails to live up to its financial expectations.

If a loan becomes distressed, the lender may begin to charge penalty interest, which typically increases the loan rate (and thus the yield). A lender might also increase the rate of a distressed loan through a restructuring. In some cases, a lender might choose to sell a distressed loan through the secondary debt markets. If a new investor buys a distressed loan at a discount, then by definition, the effective interest rate on the loan will also increase, again increasing the potential yield.

Venture debt

Venture debt refers to a loan that’s issued to a startup company that’s backed by VC. In most cases, companies that raise venture debt have already raised prior rounds of equity funding from VCs and are looking for additional capital to fuel medium- or late-stage growth without incurring further equity dilution. Venture debt is typically seen as a complement to traditional VC funding, rather than a replacement.

Special situations lending

Special situations lending involves issuing loans to companies in need of financing to support rare or one-off events, such as a company restructuring or an M&A deal. Some special situations loans might also qualify as distressed debt, and like distressed debt, special situations loans tend to be higher-yielding than some other types of private credit. The situations that prompt these types of loans are often complicated and unique, sometimes requiring significant expertise and oversight from lenders.

Asset-based lending

Asset-based lending involves loans that are secured by specific assets, rather than by the general credit of the borrower. These types of loans can be an attractive alternative to traditional term loans for borrowers with limited cash flows or with valuable portfolios of other assets, which can include accounts receivable, inventory, equipment, or real estate. Because the value of these sorts of assets can be difficult to assess when compared to cash, issuing asset-based loans can require additional expertise and diligence on behalf of lenders.

Secured loans and unsecured loans

Many loans in the private credit market are secured. In order to obtain a secured loan, a company puts up some assets as collateral. These assets might be hard assets, such as in asset-based loans, which are a type of secured loan. If a company fails to repay a secured loan as scheduled, it may enter default, and the lender could liquidate or seize some or all of the collateralized assets as compensation. These secured loans may be satisfied with the security assets before payments are made to general creditors, including senior debt holders.

Other private loans are unsecured, where the borrower does not put up collateral. Because unsecured loans present increased risk to the lender, they also typically feature higher interest rates, making them more expensive to the borrower. Other terms of unsecured loans can also be less friendly to borrowers. Unsecured loans are more likely to be found in higher risk areas of the market, such as mezzanine credit and distressed credit.

Why private credit financing appeals to companies

There are a number of potential scenarios when companies typically turn to private credit. Perhaps a growth-stage startup wants to raise capital to fuel its expansion without diluting its equity owners. Perhaps a small business is looking to use leverage to help finance a buyout or other type of M&A deal. Perhaps a major corporation is looking to raise a large loan on more flexible terms than it could find with traditional banks.

In these instances and many others, private credit may have some particular advantages over other traditional financing options:

Flexible terms

Private lenders are more likely to offer customizable loan structures that can meet a borrower’s specific needs, including flexible repayment timelines and covenants. Bank lenders are more likely to structure their loans on standard underwriting or banking models.

Easier access to capital

The process of raising private credit financing is typically faster and more streamlined than raising a bank loan, with fewer approvals required before closing a deal. This can be appealing to companies operating on a specific timeline. Private lenders may also be more willing than banks to issue private loans to companies with seasonal revenue swings or other non-standard financial models.

Higher leverage

Depending on the company and the situation, private lenders might also be more likely than banks to issue loans that will leave the borrower highly levered—that is, with a high level of debt relative to the company’s assets and income. This access to leverage can be particularly appealing for companies that are in distress or navigating other special situations.

Disclosures and oversight

Private loans typically require fewer regulatory disclosures and less regulatory oversight than publicly traded loans. This can allow companies to raise financing more discreetly and confidentially.

What are the risks of private credit for founders?

When a company raises capital through private credit, the terms of the loan (such as the repayment schedule and any financial covenants) are typically based on financial projections for the company’s future. If the company falls short of these projections—if it doesn’t grow as quickly as expected, for instance, or if it has a difficult quarter—then the company may struggle to satisfy the terms of the investment and may be at risk of default.

Practically, this might include strains on cash flow: If a larger percentage of revenue than expected must go to servicing debt, the business might have to cut spending elsewhere. If cash flow grows too strained, the company may be unable to repay the loan and be forced to default, which could result in lenders taking control of the company.

Financial difficulties might also cause a company that has raised private credit financing to fall out of alignment with financial covenants. These covenants might be related to metrics like cash flow, annual recurring revenue (ARR), or other growth metrics. The consequences for missing covenants are typically outlined in the terms of the loan, sometimes up to and including the seizure of assets or the forced liquidation of the company.

Raising private credit may also create strategic and operational challenges for some startups in the future. The presence of debt might complicate future equity funding rounds, or prevent some potential backers from investing altogether. The need to service debt and continue to meet covenants might also limit a company’s spending in other areas, such as hiring or new product development, which could have its own implications.

Conclusion: Private credit is on the rise

Over the past two decades, the general trend is clear: More and more corporate fundraising activity is moving to the private markets. Startups are staying private for longer periods of time before going public or pursuing another exit. And companies of all stripes are increasingly turning to private credit to meet their capital-raising needs.

The size of the private credit market grew from $2 trillion in 2020 to $3 trillion in 2025, and it’s expected to approach $5 trillion before the decade is out. For companies and founders, understanding the potential impacts of private credit is more important than ever.

Frequently asked questions about private credit financing

Can an early-stage startup get private credit?

Yes, an early-stage startup can raise private credit financing. In general, however, private credit is relatively rare among early-stage startups. One of the main reasons for this is that raising private credit funding locks a company into regular interest payments and financial covenants, which can limit flexibility as an early-stage startup grows. In most cases, private credit is more likely to be an option for later-stage startups with established product lines and revenue streams, while early-stage startups are more likely to rely on equity financing.

What is the difference between private credit and venture debt?

Venture debt is a type of private credit financing, in the same way that a square is a type of rectangle. Private credit refers to any type of loan from a non-bank lender. Venture debt refers to a loan from a non-bank lender that’s specifically raised by a company with VC backing.

How does private credit affect future fundraising?

For a startup, one of the main potential issues of raising private debt financing is that it increases the complexity of a company’s capital stack. Another issue is that debt holders typically hold a senior claim on a company’s assets and cash flows. For these reasons, some venture investors shy away from investing in companies that have previously raised debt funding, opting instead for targets with cleaner cap tables. Thus, raising private capital may limit a company’s pool of potential VC backers in the future.

Other VCs might see the presence of debt in a company’s capital stack as a risk factor, and thus ask for terms that are less favorable to the company. Some investors might also ask existing lenders to restructure their loan agreements, which can create challenging negotiations and lengthen fundraising timelines.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.