For a company’s employees, being acquired by a private equity firm or PE-backed portfolio company can spark a period of transition. New ownership might have new strategic plans. Those plans may lead to significant operational shifts. Some executives might move on, and new managers might be brought in.

When a PE buyer institutes these sorts of changes at a newly acquired portfolio company, it wants to make sure that the company’s employees are properly motivated to achieve the financial outcome that ownership is seeking. In many cases, PE firms issue equity compensation to portfolio company executives and other employees as a way to align incentives among key stakeholders across the breadth of an organization.

>> Read the 2025 PE Executive Equity report

In her career as a PE investor and operator in the energy sector, including stops at Blackstone and Morgan Stanley, Andrejka Bernatova has seen the impact that equity can have. Now the CEO and chairman of Dynamix, a SPAC pursuing deals in the energy, power, and infrastructure sectors, as well as the founder and managing partner at private equity firm Regen Capital, Bernatova believes it’s a critical piece of the puzzle for PE firms.

“As an investor, you need to issue equity,” Bernatova says. “You need to be aligned with the management team, and it needs to be very thoughtful in the way it’s distributed.”

Rowing in the same direction

There are different types of equity grants that PE firms and their portfolio companies issue to employees. At corporations, it’s typical to receive stock options, in the form of ISOs or NSOs. At LLCs, grants are most likely to take the form of profit interest units.

In both cases, the idea is similar. If an employee owns part of the company’s stock or a right to some of its future profits, then the employee will be more motivated to help the company succeed.

But success can come in many different forms. To make sure that incentives are aligned as closely as possible, some equity grants come with performance conditions—clearly defined terms that must be met before those shares are eligible to vest.

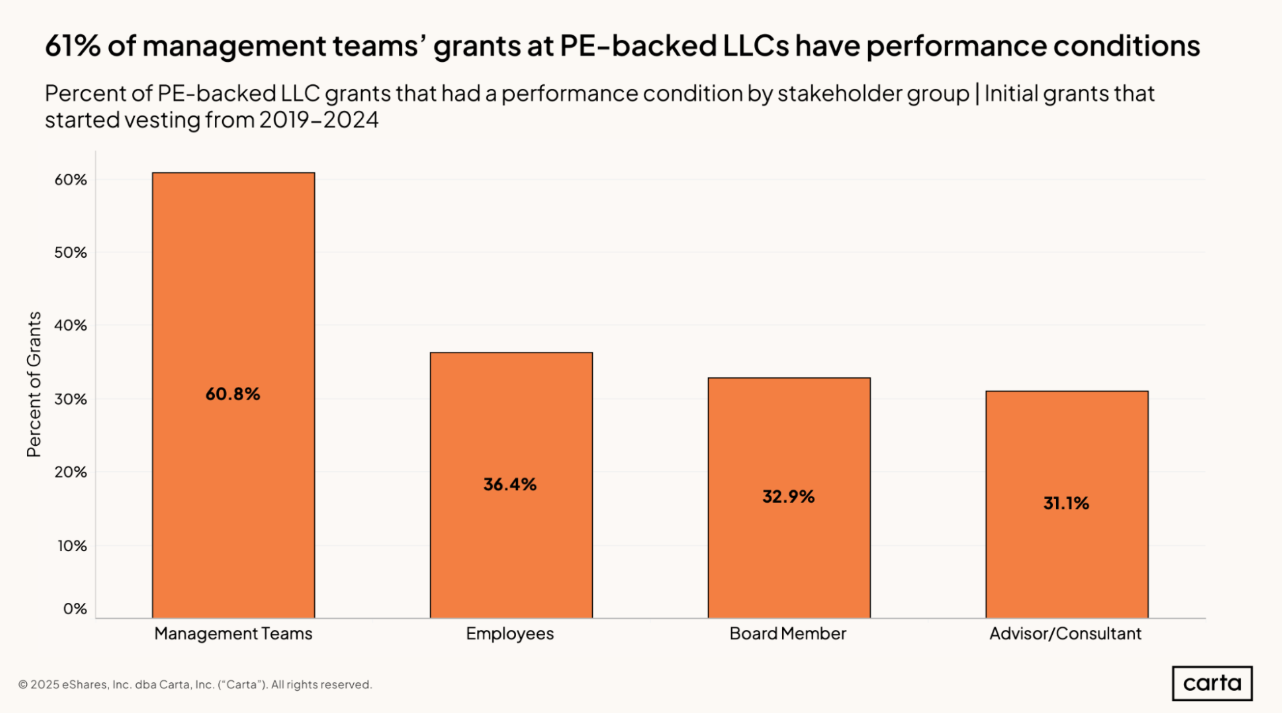

At PE-backed LLCs, performance conditions were present in nearly 61% of initial equity grants issued to management teams tracked on Carta from 2019 through 2024. About 36% of grants issued to all employees at PE-backed LLCs came with performance conditions. This gap makes intuitive sense: Executives are in a position to have a greater impact on a company’s future, so their compensation is more likely to be linked to a desired outcome.

This importance of management teams can also play a role in whether employees receive any equity at all as part of their compensation. While some companies issue stock options or PIUs to all employees, others reserve it for key executives or some other defined segment of the workforce. Bernatova says that either option can be appropriate, depending on a company’s specific circumstances.

“How deep do you go in terms of equity? I don’t think there’s any silver bullet,” Bernatova says. “You may want to give the majority of your equity to the CEO, who is truly a rainmaker. Or you can distribute it more widely. It’s very dependent.”

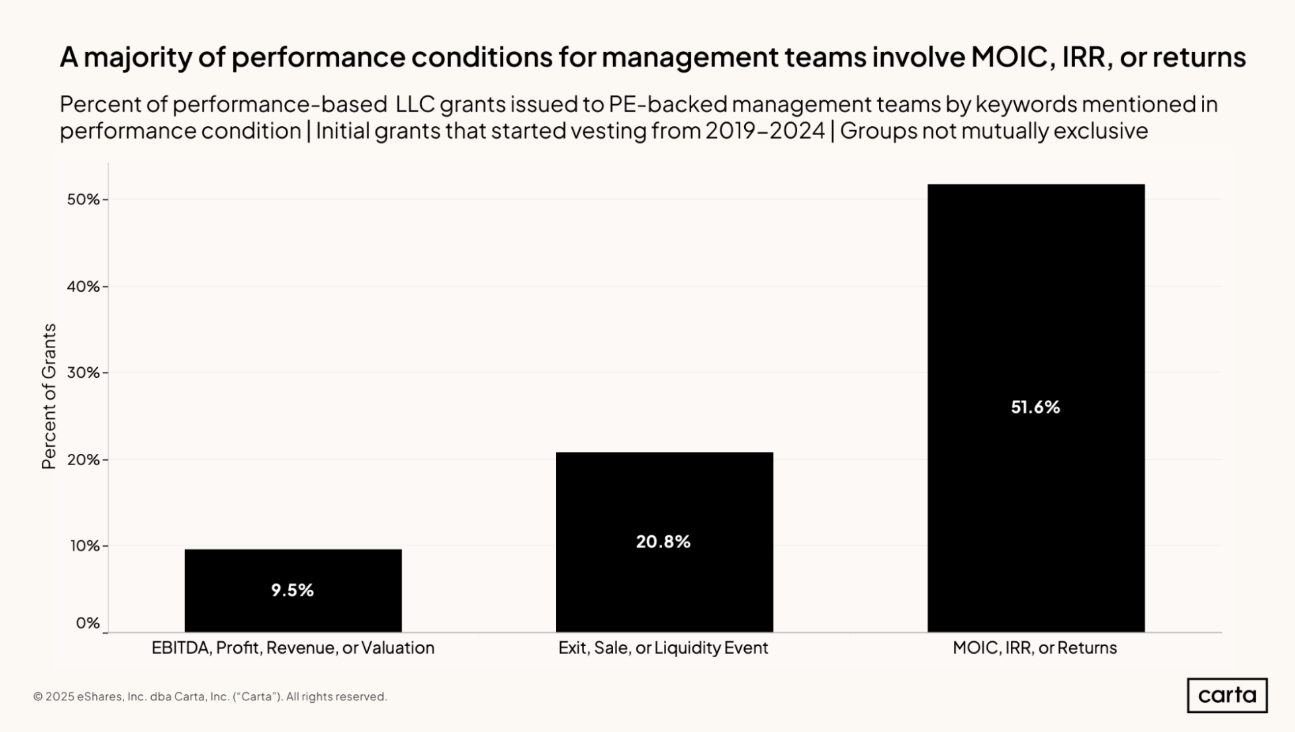

Among this same population of PE-backed LLCs, nearly 52% of performance conditions on initial grants issued from 2019 through 2024 were tied to a metric that measures the investor’s financial return, such as MOIC or IRR. This was the most common type of condition. About 21% of performance-based grants were conditional on achieving an exit or some other liquidity event, and just shy of 10% were based on other financial metrics, such as EBITDA or revenue.

If a PE-backed owner is targeting a certain return on their investment or a certain revenue figure, they can link these specific metrics to performance conditions. The details of these conditions can vary widely. In general, though, they should be set at thresholds that the owners might reasonably expect to meet.

“If you want to be aligned, you need to be realistic with the expectations you’re setting with management as it relates to equity,” Bernatova says. “It needs to be something that’s achievable.”

PE buyers are staying busy

For employees throughout the private markets, these sorts of questions around how PE-backed buyers approach their equity are growing increasingly common.

PE firms and their portfolio companies accounted for 36% of all M&A activity in 2024, up from 28% in 2023, according to a recent study of the M&A market by SRS Acquiom. And these PE-backed transactions are often some of the largest deals in the market. The share of all M&A transactions larger than $750 million rose from 3% in 2023 to 10% in 2024, which SRS Acquiom senior director of thought leadership Kip Wallen attributed to the growing presence of PE.

“I think we can thank private equity buyers for that,” Wallen says.

Aziz Gilani, general partner at Mercury Fund, an early-stage software investor, has noticed something similar.

“We have record amounts of PE-backed companies trying to do acquisitions,” Gilani says. “You’re seeing them do a ton of activity.”

As these PE firms and PE-backed portfolio companies continue to pursue and complete new deals, the decisions they make about equity could have implications for years to come—both for employees, and for the ultimate outcome of an investment.

“You have to think about, how do I want the management team to be aligned with me as an investor over the period of time that I’m going to be invested in this company?” Bernatova says.

Read the full PE Executive Equity report