- Carta's 409A valuation practice

- How does Carta prepare 409A reports?

- Why should customers have confidence in the valuation reports prepared by Carta and trust that they are valid in the eyes of auditors and/or the IRS?

- What is the guideline transaction method for valuations?

- Why does Carta use the guideline transaction method in its 409A valuation analysis for early-stage companies?

- What types of companies qualify to obtain their 409A valuation based on the guideline transaction method at Carta?

- How does Carta source data used for 409A valuations conducted using the guideline transaction methodology?

- Why does Carta use its own private-company database over traditional data sets when adopting the guideline transaction method?

- How are SAFEs and/or convertible notes treated for pre-seed companies under the guideline transaction methodology?

- Are there any discussions between Carta and company management teams about valuation results? If so, how frequently do these discussions take place?

- How does Carta support customers during an audit of its valuation reports?

How does Carta prepare 409A reports?

Carta’s 409A valuation reports are prepared when we receive a customer’s request for a new 409A valuation report through our platform.

The customer must go through a verification exercise upfront during the request process before Carta delivers a 409A valuation report. During this verification process, the customer makes several representations to Carta, including:

Cap table is accurate and up-to-date;

Financial data (cash runway, financial performance) is correct;

No pivot in business model; and

No current or pending Letter of Intent (LOI) exists for a corporate transaction (M&A or financing);

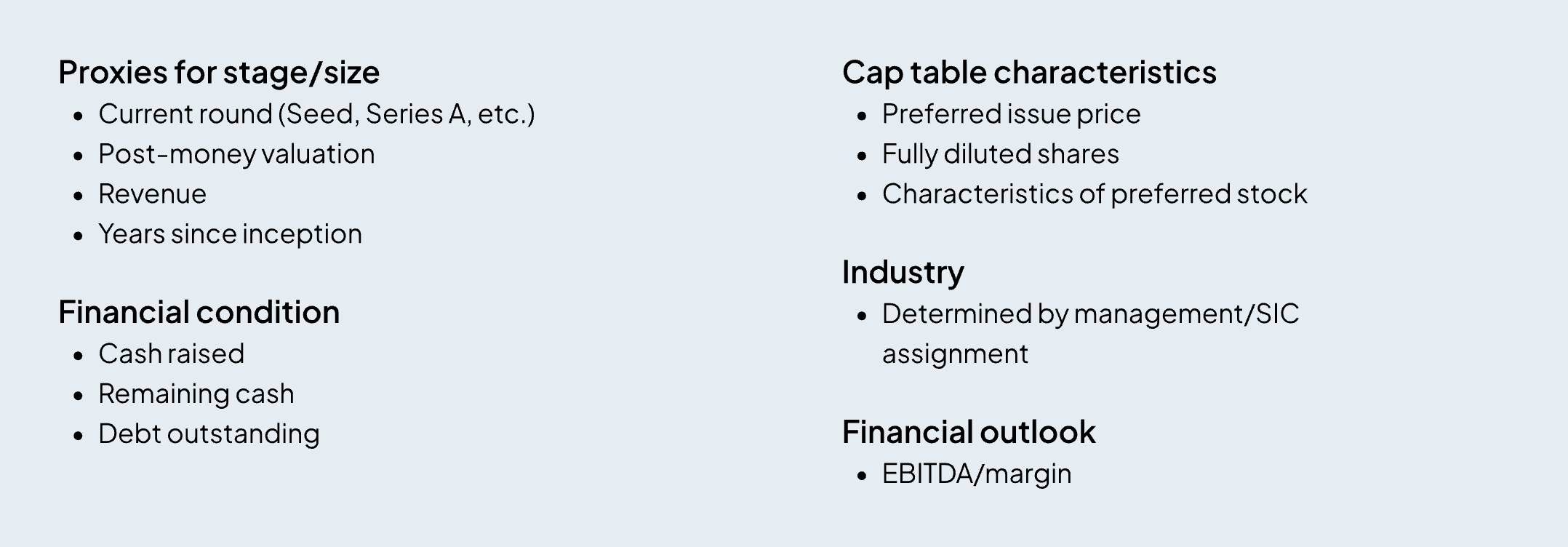

Our valuation specialists analyze each company to determine the most appropriate valuation methodology. For those valuations prepared using the guideline transaction method, our valuation specialists consider the following factors in a subject company to identify comparable companies within our private company data set:

Our valuation analysts review all materials thoroughly to ensure compliance with our internal policies (as detailed below) before the customer receives their draft 409A valuation report. After receiving the report, all customers have access to our team of valuation specialists for any follow-up questions and audit support if necessary.

Why should customers have confidence in the valuation reports prepared by Carta and trust that they are valid in the eyes of auditors and/or the IRS?

Carta regularly has its valuations reviewed by financial auditors, including the Big Four accounting firms, and has successfully concluded many audits for valuation reports.

Carta’s 409A valuations use standard valuation methodologies in accordance with IRS guidance. A valuation that is prepared by an independent appraiser is considered to qualify for safe harbor under Section 409A. This shifts the burden of proof from the company to the IRS, which must demonstrate that the valuation is grossly unreasonable if it challenges the valuation. The results of Carta’s valuations are consistent with results obtained using other methodologies as well as results from valuations performed by other third-party valuation providers.

Valuations that are prepared for tax compliance related to 409A are also used for financial reporting under ASC 718 (stock-based compensation expense accounting). This means the value determined for a company’s common stock in the 409A valuation report is used in a calculation that results in an expense on a company’s income statement.

Financial auditors review the valuations as an input into this expense calculation. As such, the auditors will review (1) whether the valuation methodology used is appropriate; (2) whether the inputs to that methodology are supportable, and (3) whether the overall conclusion of common stock value falls within a reasonable range.

What is the guideline transaction method for valuations?

The guideline transaction method is one of several industry standard methodologies used when valuing small businesses.

The method is one of two commonly used valuation methods within the “market approach,” which is a valuation technique that evaluates prices and other relevant information gathered from market transactions involving similar or identical assets. Under the market approach, valuation practitioners value assets by comparing them to identical or similar assets. The other method within the market approach is the guideline public company method.

Why does Carta use the guideline transaction method in its 409A valuation analysis for early-stage companies?

The guideline transaction method benchmarks the subject company against other companies that exhibit similar attributes (e.g., stage, size, financial condition, etc.). In line with market practice, Carta adopts this method when performing valuations for early-stage, venture-backed private companies.

Carta leverages its private company database on an aggregated and anonymized basis to deploy the guideline transaction method in our 409A valuations based on actual venture capital financings across various industries and company stages.

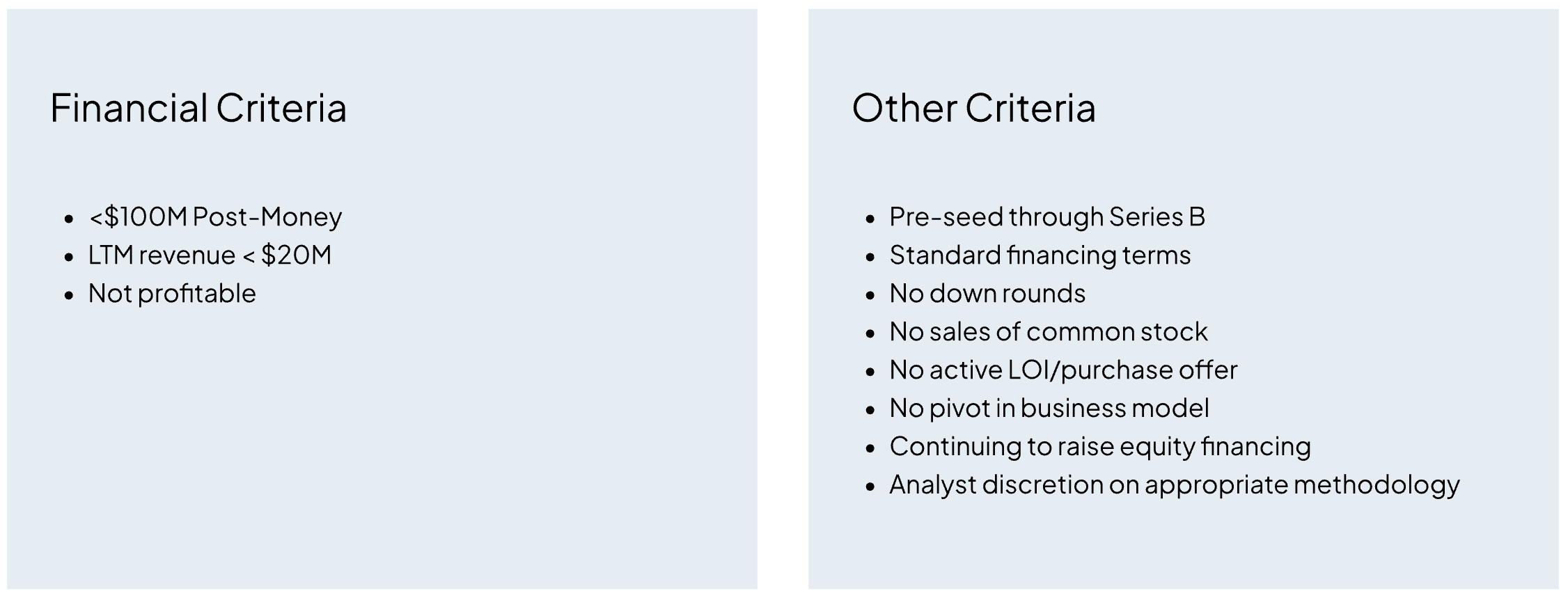

What types of companies qualify to obtain their 409A valuation based on the guideline transaction method at Carta?

At Carta, companies that meet the criteria set out below qualify for 409A valuations conducted using the guideline transaction methodology:

While the guideline transaction method could potentially be considered for companies of any stage, Carta currently adopts this valuation methodology for early-stage companies only (e.g., pre-seed, Series Seed, or Series A). This is in part due to the large volume of comparable transactions among companies at these stages that Carta can leverage from its database, as discussed below.

How does Carta source data used for 409A valuations conducted using the guideline transaction methodology?

Carta is the largest cap table management software provider in the market. As of the date of this FAQ, more than 40,000 companies use Carta to track and reflect financing transactions relating to their company’s securities.

When anonymizing and aggregating all financing transactions as reflected by companies on Carta, we can identify key characteristics underlying these transactions, including the date of financing, cash raised, post-money valuation, company stage, industry, and financial conditions of the company, among others.

With this, Carta is well-positioned to build a rich database of actual venture-capital financing attributes among companies across industries and stages, which we can benchmark against when conducting valuations using the guideline transaction method. This allows Carta to perform the most robust analysis of financing transactions that occurred among early-stage companies that have standard financing terms.

Carta’s private-company data set is not based on valuations previously performed by Carta—it is based on third-party financing transactions.

Why does Carta use its own private-company database over traditional data sets when adopting the guideline transaction method?

Valuation practitioners typically work with a few types of data sets when deploying the market approach. They include (1) public company data and (2) public or private company M&A transaction data.

Carta’s private-company data set is the most appropriate data source to use for early-stage and venture-backed companies, given that public company data and public or private company M&A transaction data both have significant limitations for these types of companies.

Limitations of public company data

Public companies are typically much larger in terms of capitalization, exhibit more diverse and complex business structures, have better access to capital, and are of a lower risk of failure compared to private companies (especially those that are early-stage and venture-backed).

Even though there is a significant lack of comparability of public-company data for private-company valuations, many valuation professionals nonetheless still use public-company data to run valuation reports given the lack of or limited accessibility to private-company data sets. This approach produces valuation results that are less accurate for startups given the vastly different nature between public and private companies.

Limitations of M&A transaction data

Alternatively, valuation professionals often use M&A transaction data sourced from various paid databases (e.g., Capital IQ and DealStats) to perform valuations using the guideline transaction methodology.

Relying on M&A transaction data to perform valuations for private companies presents several significant limitations. First, since M&A transactions (especially those relating to private-company transactions) are not often reported, the data sets that valuation professionals end up using are often stale (e.g., more than two or three years prior to the valuation date). Second, the price that buyers pay for a company may include premiums for expected synergies from a merger or for the ability to gain control over the business. These premiums are difficult to quantify and result in less comparable data. Third, like the limitations presented in public-company data sets, M&A transaction data is not necessarily comparable to private companies given company size or transaction value.

Applicability of Carta’s private-company database

Given these limitations in traditional data sets, Carta performed an extensive analysis of our own private-company database to explore its usability in our valuation practice. Our analysis led us to conclude that the attributes of our underlying private-company data, when deployed in an aggregated and anonymized fashion, represent the most appropriate data source to adopt for valuations conducted in accordance with the guideline transaction methodology. This practice enables Carta to deliver our customers 409A valuation reports that qualify for safe harbor under IRC Section 409A.

How are SAFEs and/or convertible notes treated for pre-seed companies under the guideline transaction methodology?

The investment amount as set out in a company’s SAFE or convertible note is a key characteristic that we consider when we benchmark the subject company against similar transactions. Other characteristics considered include industry, total capital raised, and number of years since inception. These factors are considered to be the most relevant in determining the valuation of a pre-seed company that plans to seek venture financing.

Convertible notes and SAFEs are generally treated as debt for valuation purposes, as the conversion of these instruments to equity is based on a future round of financing whose structure is highly speculative. As such, the conversion terms (discounts and val caps) do not impact the valuation.

Are there any discussions between Carta and company management teams about valuation results? If so, how frequently do these discussions take place?

Carta is committed to transparent communications with its customers about their valuations.

As of the date of this FAQ, a team of over 80 valuation professionals make up Carta’s valuation practice. Our valuation professionals regularly engage with customers on their valuation reports.

Approximately 40% of our early-stage company customers discuss results from their valuation reports with our valuation team. Customers typically contact our valuation professionals through email, chat, phone, or Zoom via their Carta valuation ledger tab. These customer discussions typically include a range of topics, including walkthroughs of the valuation report, customer inquiries about the valuation results, or the underlying assumptions made in our reports, to name a few examples.

How does Carta support customers during an audit of its valuation reports?

Carta supports more than 1,000 customers each year during financial audits of their valuation reports, working with auditors to respond to questions on the valuation and providing supporting calculations as needed.

If needed, customers and their audit firms may also request a copy of Carta’s System and Organization Controls (SOC) 1 Type 2 Report, which provides information on controls Carta maintains over its data. This report notes that these controls provide reasonable assurance that transaction information is complete and accurate. Further details and reports can be found here.

DISCLOSURE: This publication contains general information only and eShares, Inc. dba Carta, Inc. (“Carta”) is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein.