- As VC deals shrink, convertible fundraisings are on the rise

- Alternatives to priced rounds: SAFEs and convertible notes

- The trend toward unpriced rounds

- Fundraising by Series A companies

- Deal terms demonstrate a market shift

- Cumulative dividends

- Liquidation preferences

- Participating preferred stock

- The new reality

- Learn more

- Get weekly insights in your inbox

Venture-backed valuations were down more than 15% at every stage of the startup lifecycle over the past year. At Series B and beyond, they’re down more than 40%. For many startups seeking new capital, this shift in the VC environment creates an unappealing possibility: having to raise a down round.

To avoid that outcome, startups and their investors are getting creative. Carta data shows that venture-backed companies have increasingly embraced different types of fundraising mechanisms and more investor-friendly deal terms over the past year-plus, demonstrating the lengths startups will go to avoid a downsized valuation—or at least mitigate the damage.

Alternatives to priced rounds: SAFEs and convertible notes

Not every venture-backed investment results in a new valuation. SAFEs and convertible notes are two alternatives to priced rounds that allow companies to raise new capital without repricing their shares. SAFEs offer a right to equity through a later priced round, while convertible notes are debt instruments that can later convert to equity. Both are most common among very young startups, often those without an established business model that investors can confidently value.

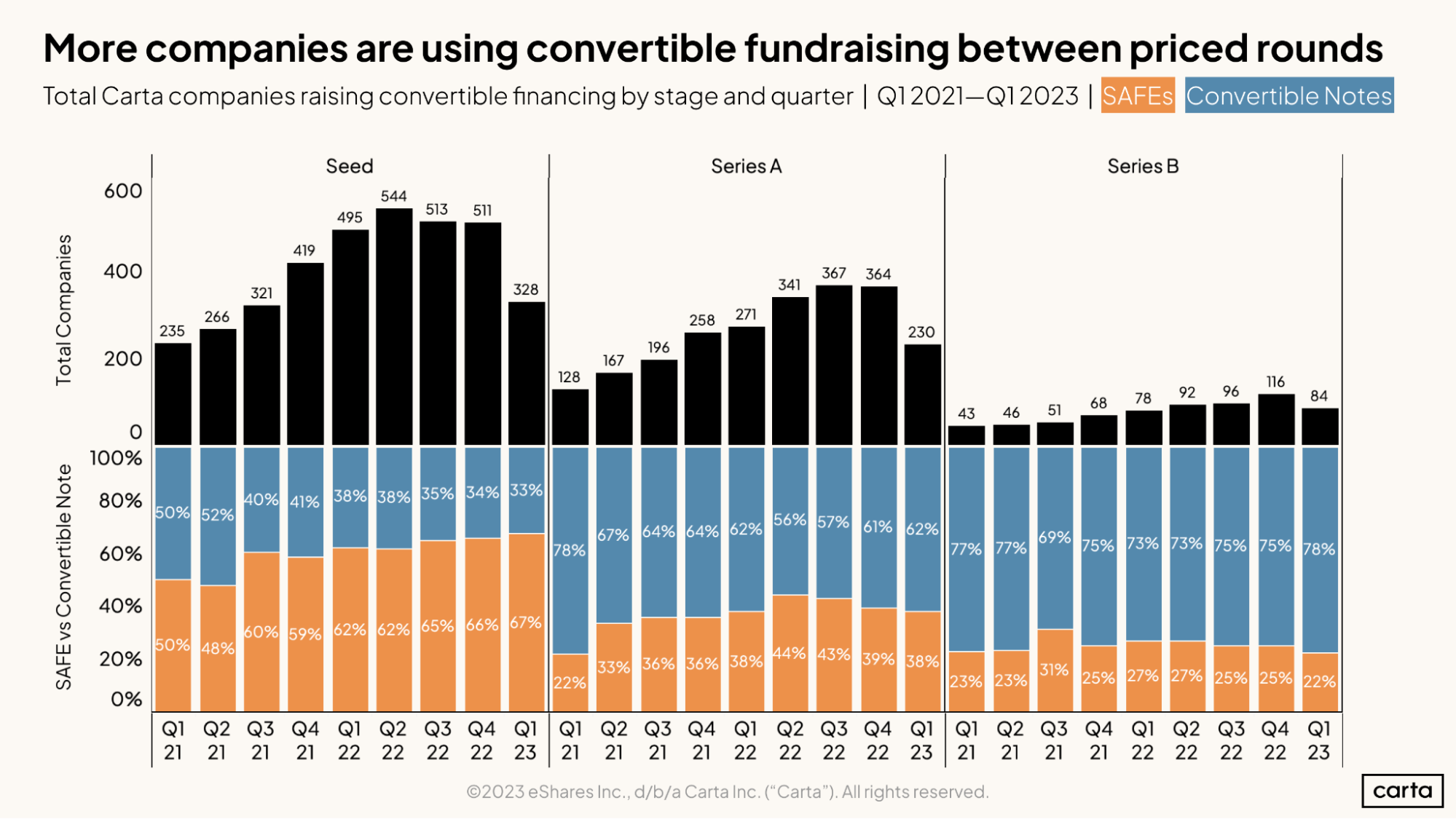

Last year, the number of more mature companies on Carta that raised SAFEs and convertible notes as an alternative to priced rounds climbed to recent highs at a few different stages. For instance, 367 companies that had most recently raised a Series A opted to raise a SAFE or convertible note during Q3 2022, an 87% increase over the number of companies at this stage raising alternatives to priced rounds in Q3 2021.

Convertible rounds typically raise less capital than priced rounds. But they offer companies a way to extend their financial runway without raising a down round.

“The most notable trend that I am seeing is the prevalence of fundraising through bridge financings—usually with convertible debt, sometimes with SAFEs—where the round itself isn’t priced and companies are essentially postponing the priced round until the market gets better,” says Josh Fox, a startup lawyer and member at Mintz who’s spent more than 20 years working with tech and biotech companies.

The trend toward unpriced rounds

Unpriced fundraisings were already growing more frequent as early as 2021, but that growth accelerated in 2022. This shift to unpriced rounds is more stark when we compare the ratio of unpriced rounds to priced rounds at each stage over time.

In Q3 2022, there were 367 unpriced rounds among Series A companies on Carta, compared with 159 Series B rounds. A year earlier, in Q3 2021, the relationship was the inverse:

Fundraising by Series A companies

Priced Series B rounds | Unpriced rounds | Total rounds | Rate of priced rounds | |

Q3 2021 | 354 | 196 | 550 | 64% |

Q3 2022 | 159 | 367 | 526 | 30% |

Some companies didn’t have enough investor interest to raise a new priced round. Others did, but only at a greatly reduced valuation. For startups in both camps, an unpriced round began to look more attractive.

“A company that’s running out of cash, they don’t like the price they can get out in the market or with their own investors—they can raise some much lower dollar amount on a SAFE and sort of kick the can down the road,” says Eric Hanson, a partner at WilmerHale. “And they say, ‘OK, we’ll go out and fundraise in six months when valuations are stable, or back where we think they should be.”

Deal terms demonstrate a market shift

Other startups have tried to counter the recent valuation reset in different ways. Among companies that are still raising priced rounds, there’s been an increase in structured deal terms—such as cumulative dividends, multiple liquidation preferences, and participating preferred stock—that allow investors to protect against downside risk.

When negotiating a VC deal, giving ground on some of the structured terms below can allow companies to hold firmer on valuation:

Cumulative dividends

Cumulative dividends are guaranteed returns owed to a shareholder regardless of the company’s financial performance. They were a feature of 10.4% of venture deals on Carta in Q4 2022 and 9.2% in Q1, up from 4.7% in Q4 2021.

Liquidation preferences

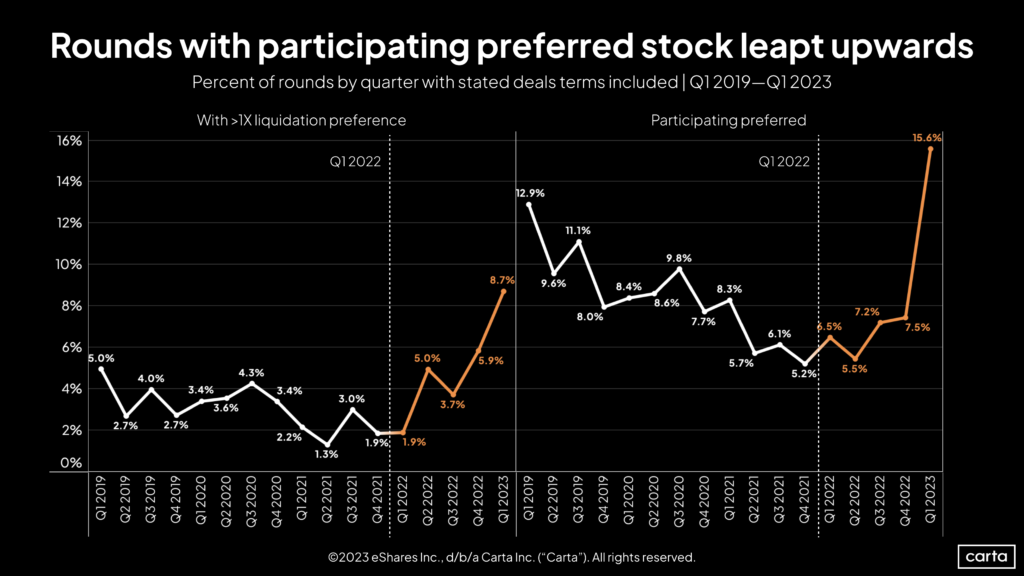

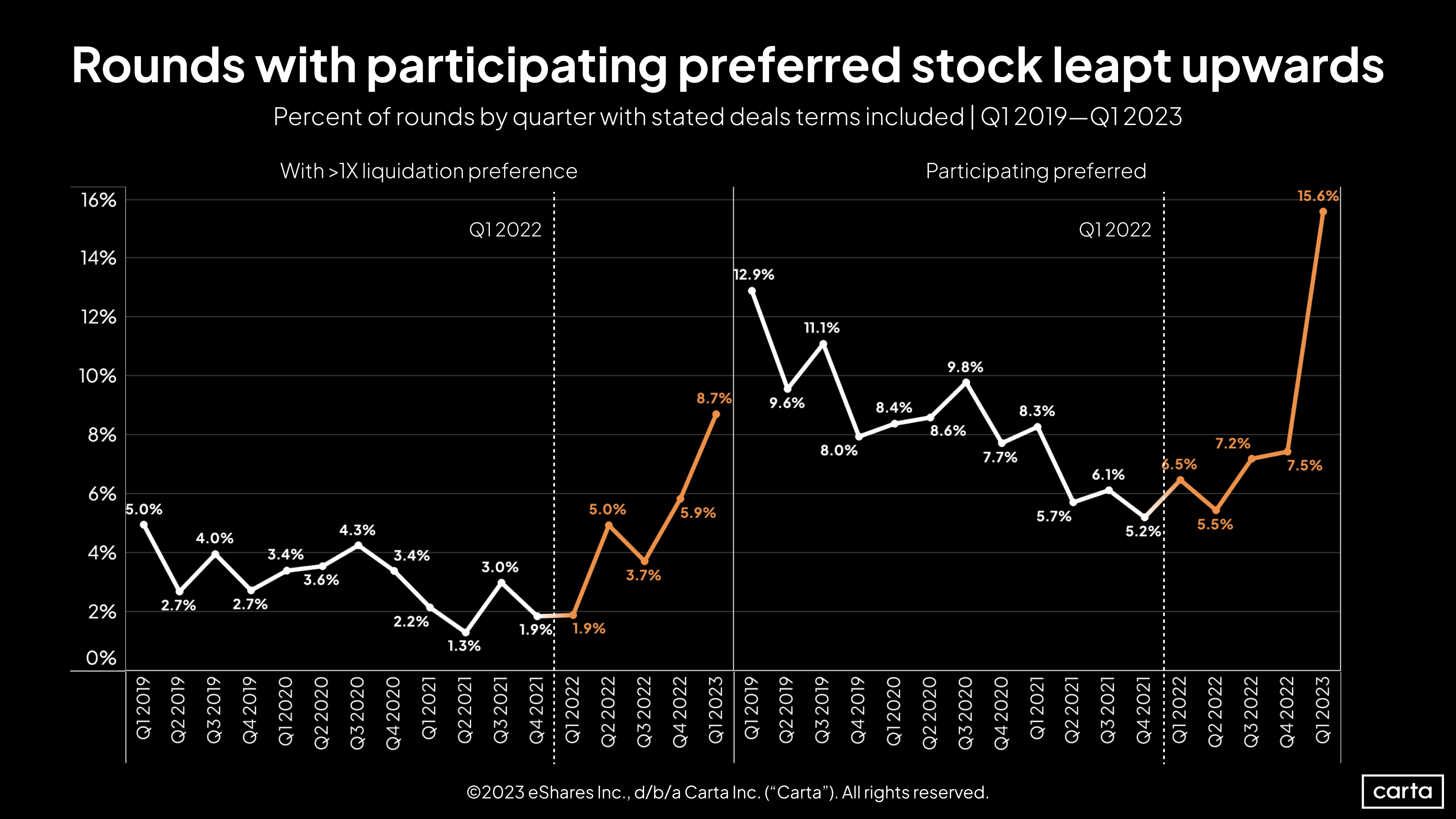

Liquidation preferences give a shareholder the right to be paid out first if the company liquidates or is sold, often at a specific multiple of their original investment. Between Q1 2022 and Q1 2023, the rate of venture deals on Carta with liquidation preferences greater than 1x climbed from 1.9% to 8.7%.

Participating preferred stock

The rate of deals featuring participating preferred stock, meanwhile, shot from 7.5% in Q4 to 15.6% in Q1, easily a new high point in the past four years. Holders of participating preferred shares are first in line to be paid out if a liquidity event occurs.

All three types of deal terms are still relatively rare among companies on Carta. But in recent months, they were less rare than they used to be.

“I’m seeing a little bit more of the accruing or cumulative dividend concept. I have seen multiple liquidation preferences being proposed a little more than before,” Fox says. “It’s still not typical to see multiple liquidation preferences. But once in a while now, there’s an investor looking for that.”

Not everyone, though, is seeing the same shift. In his work at WilmerHale, Hanson helps compile and write the law firm’s annual report on venture capital activity. Hanson says WilmerHale’s internal database does not reflect a significant increase in these sorts of structured deal terms—even if he expected it would.

“We actually haven’t seen folks tweaking the knobs to account for valuation gaps,” Hanson says. “There is definitely a disconnect in terms of what venture investors think and what founders think about what their companies are worth. So you would have thought they might try to bridge the gap in some way different than just valuation. But we haven’t seen that in our data.”

The new reality

There’s something else Hanson hasn’t seen lately: Any slowdown in business. Investors have grown more discerning, he says, but they’re still writing checks. And there’s no shortage of companies seeking capital. From a lawyer’s perspective, the market is still plenty busy.

But there are also plenty of challenges. Hanson says raising capital in this environment is particularly tough for early-stage companies, who have limited track records to prove their concept to investors. Later-stage companies, meanwhile, are trying to tighten their belts and lengthen their cash runways.

Fox and Hanson agree on the bigger picture: The changing market for venture fundraising is forcing companies to adapt.

“You may not get the valuation that you’d like. You may not raise as much as you’d like,” Hanson says. “The most important thing for a lot of these companies is to raise capital and survive through to the next stage. They may have to make some compromises.”

Learn more

The 2023 Enterprise Tech 30 list: How does the ET30 universe compare?

In late-stage VC valuations, what went up has come down—and then some

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. This post contains links to articles or other information that may be contained on third-party websites. The inclusion of any hyperlink is not and does not imply any endorsement, approval, investigation, or verification by Carta, and Carta does not endorse or accept responsibility for the content, or the use, of such third-party websites. Carta assumes no liability for any inaccuracies, errors or omissions in or from any data or other information provided on such third-party websites.©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.