How public policy influences tech ecosystem development

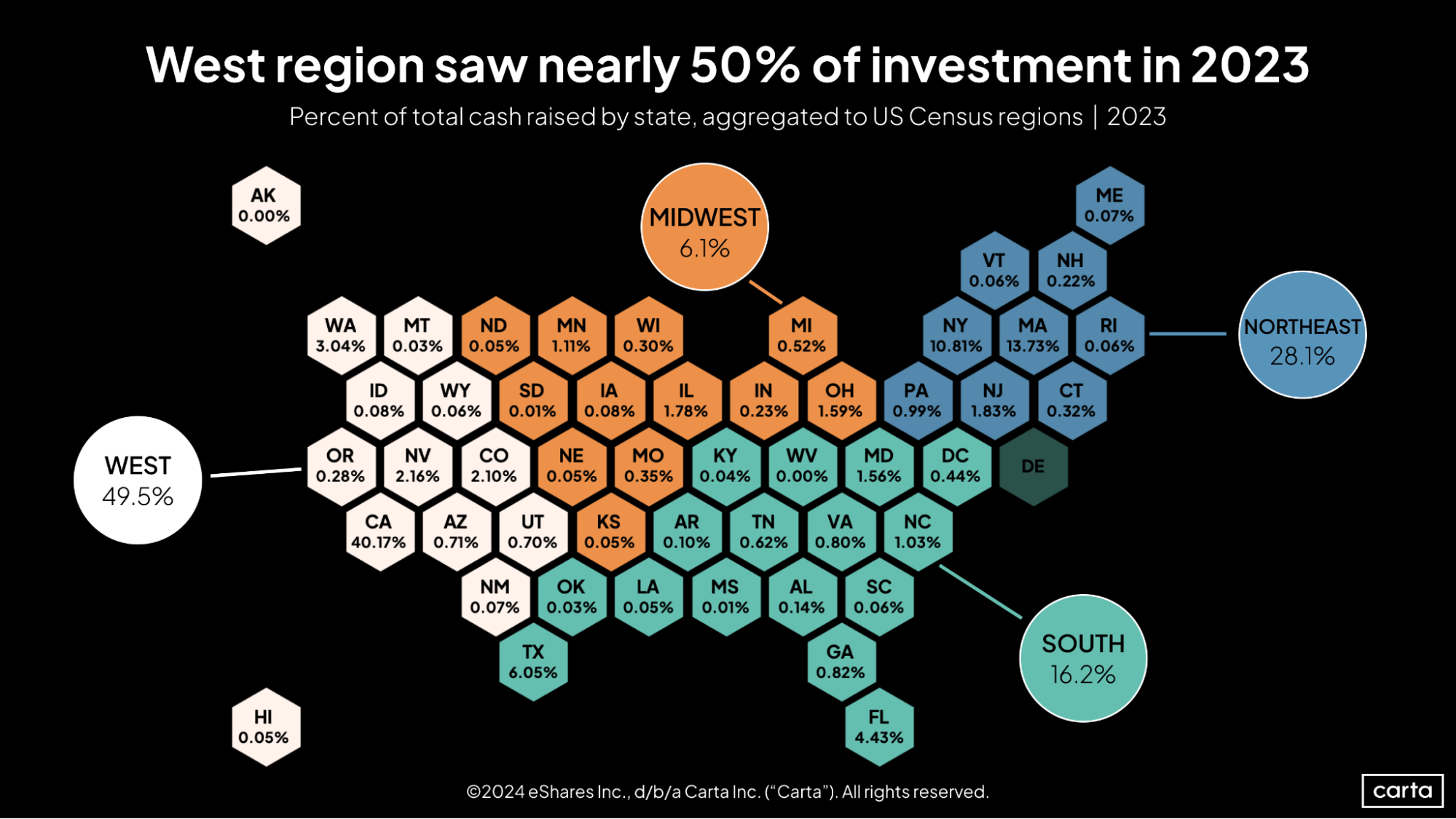

The venture economy is highly concentrated in three states: California dominates, and Massachusetts and New York each take significant shares of venture capital raised in each quarter. Together, these three states collect more than 60% of VC funding in a given quarter—well above their respective shares of the population.

Here’s a glance at how each state performed across all of 2023:

The startup ecosystems in the Bay Area, Boston, and New York City are terrific engines of innovation and job creation. But for decades, policymakers have allowed these three ecosystems to become even wealthier and better resourced by allowing them to capture most of the benefits of the private markets.

Why? Because policies meant to protect investors have had the unintended consequence of concentrating the gains of private asset classes—including venture capital—in wealthy areas.

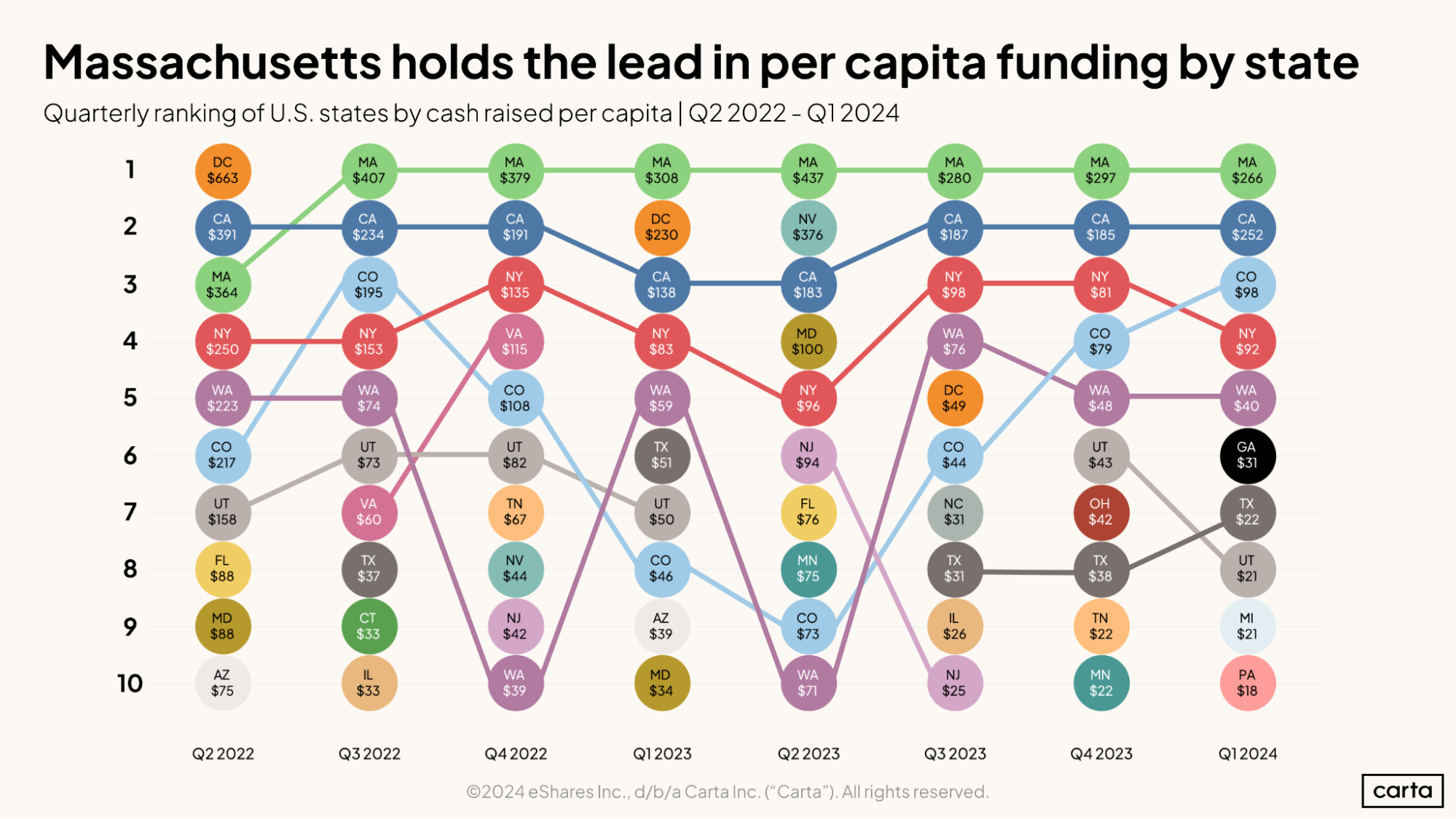

Considered on a per capita basis, Massachusetts actually dominates the venture capital sector. California consistently comes in second or third. Over the past eight quarters, CA and MA were never outside the top three, while New York almost always ranked in the top four.

Why is this? Many factors contribute to the predominance of the New York, San Francisco, and Boston tech ecosystems, including the population densities of these cities and anchor institutions of higher learning. But other cities, like Chicago, have similar profiles. Why hasn’t venture capital taken flight there?

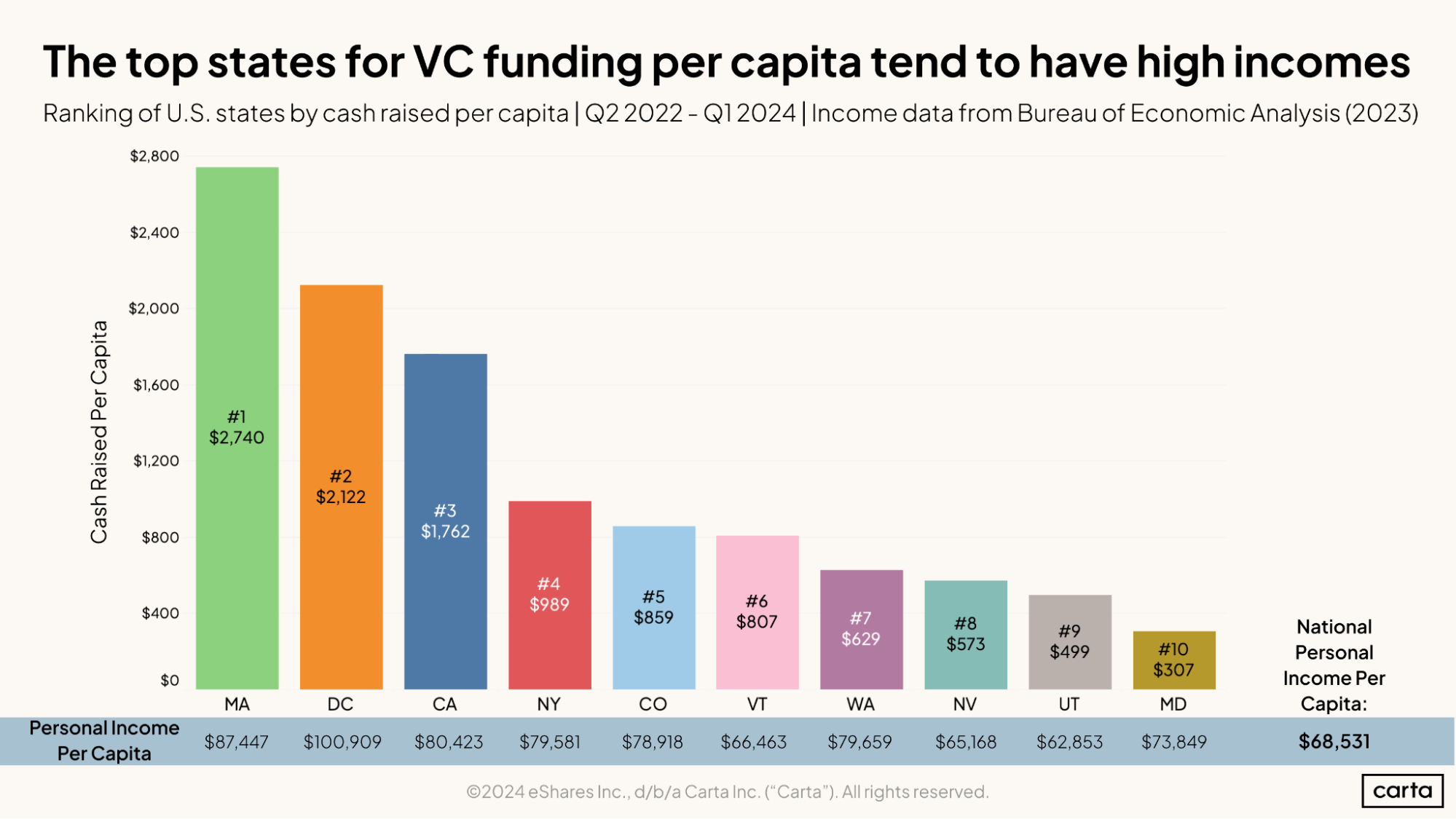

The answer brings us back to public policy. The states that dominate venture capital are among the wealthiest in the country—and therefore have a high number or high density of accredited investors. Massachusetts, California, and New York rank first, fourth, and sixth in terms of per capita personal income. Illinois, meanwhile, ranks 15th.

Sign up for the Carta Policy Team's weekly newsletterIf we aggregate the last eight quarters together, Massachusetts ranks first in terms of per capita VC dollars raised. Washington, D.C., actually edges out California for the No. 2 spot, and New York and Colorado round out the top five:

What do the top five states have in common? They all have a per capita personal income well above the national figure of $68,531—anywhere from 17% (NY) to 47% higher (DC).

It’s time for policymakers to consider ways to diversify the flow of venture capital to new geographies and to nascent startup ecosystems. One of the simplest solutions—increasing pathways to becoming an accredited investor—has bipartisan support.

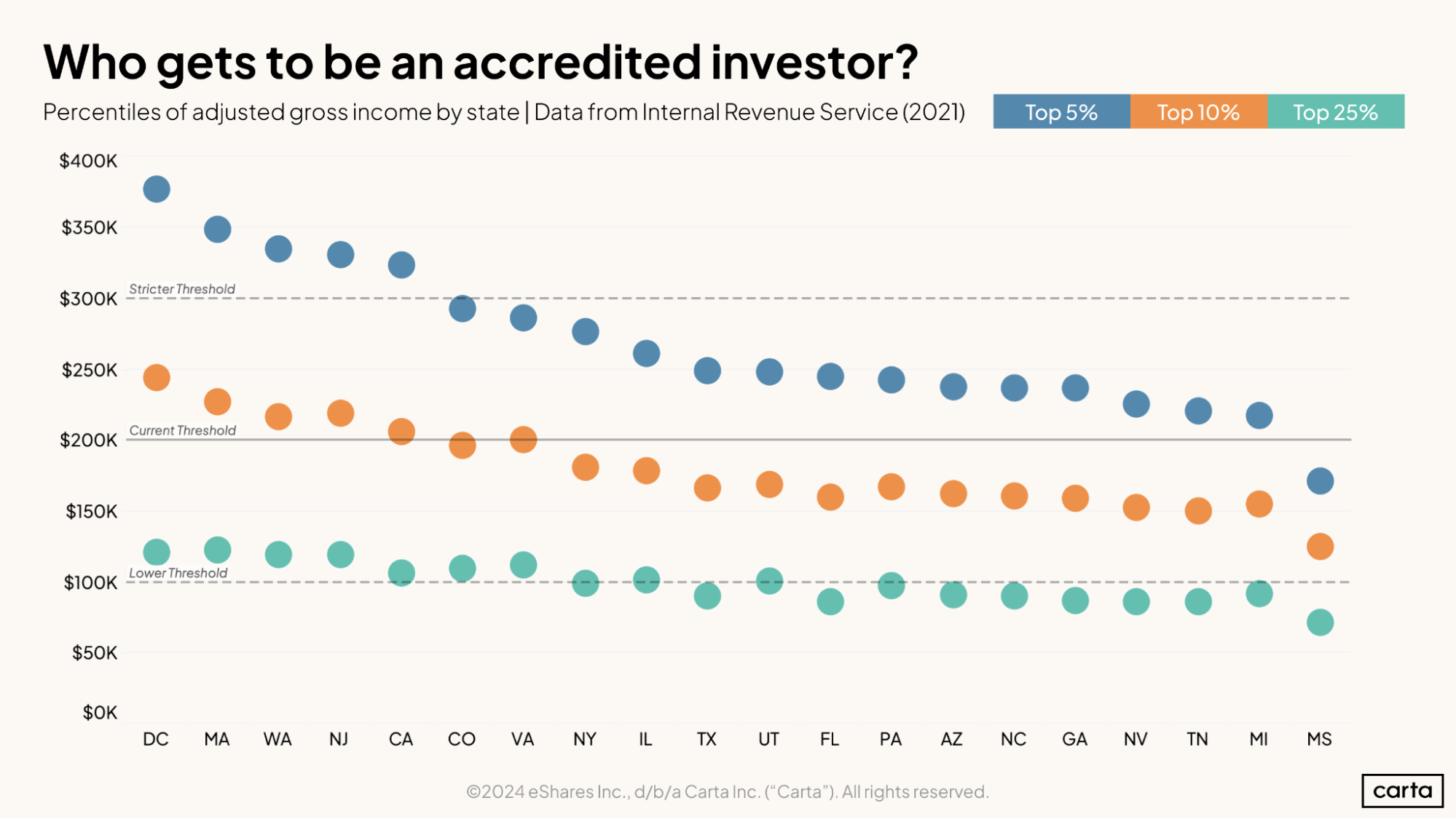

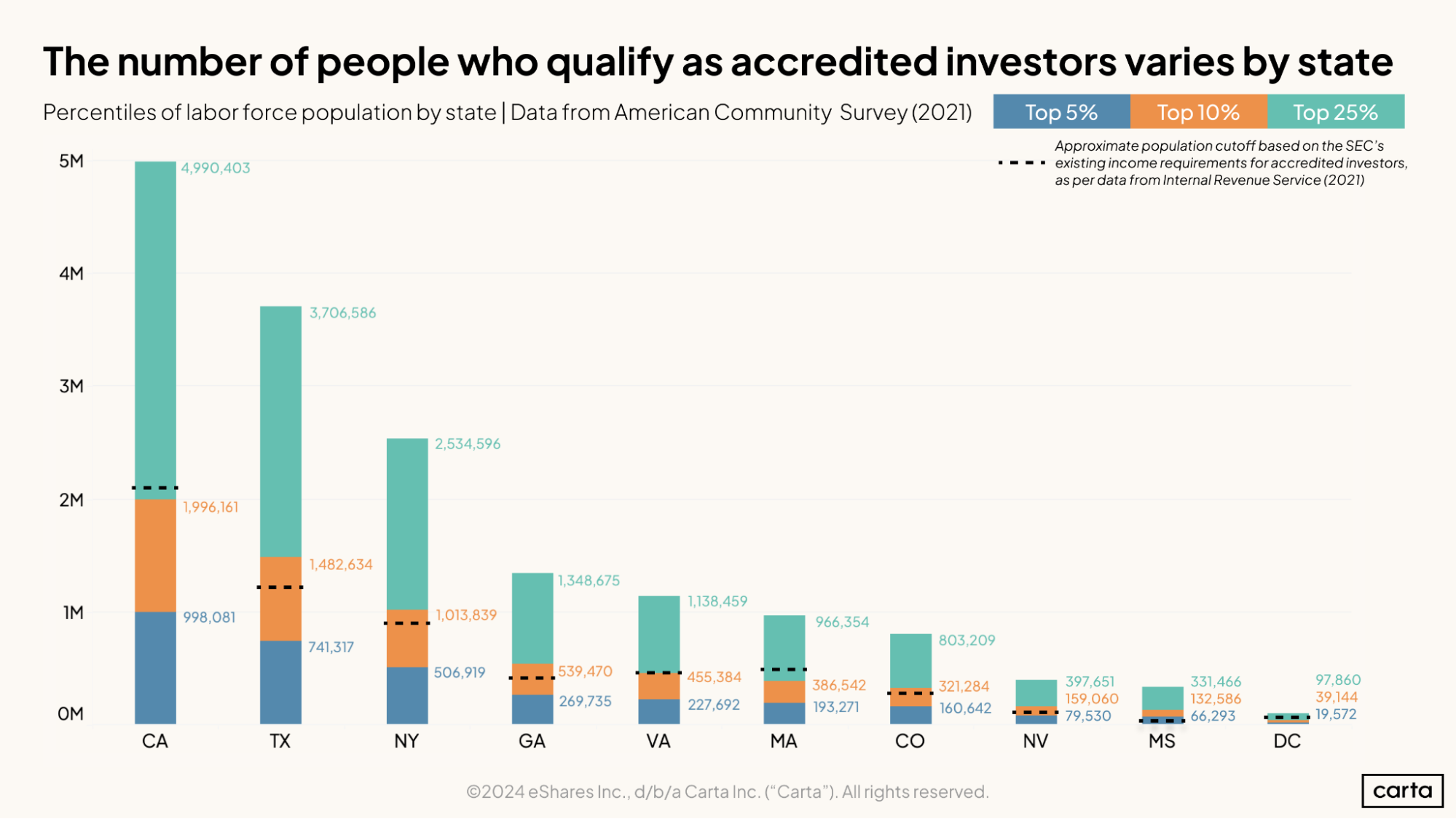

Typically, most of the investors in emerging venture funds and pre-seed startups are accredited investors—people who meet criteria set by the SEC that allows them to invest in private assets.

The vast majority of accredited investors become accredited by meeting a wealth or income threshold. For individuals, these thresholds are an annual income of $200,000 ($300,000 for married couples) or a net worth of $1 million, excluding the value of their primary residence.

States with large populations tend to have larger numbers of accredited investors. But the proportion of people who meet these thresholds varies greatly by state. In states like New Mexico and Mississippi, fewer than 5% of individuals qualify, while in Massachusetts more than 10% do.

The unitary, national standard for accredited status is blocking the growth of venture ecosystems in lower-income states and has concentrated the gains of the innovation economy in wealthy enclaves with higher costs of living.

If the SEC lowered the income threshold to $100,000, around 25% of individuals around the country would qualify for private-market investment, allowing millions more Americans who live in lower-income states with lower costs of living to participate in private market prosperity.

Congress is actively considering amending the accredited investor criteria. But the SEC is also considering raising the income and wealth thresholds—which would compound the problem.

Carta is engaging policymakers to ensure we reach an outcome that stimulates the innovation economy and allows more people to benefit from the prosperity it generates.

To get involved, write policy@carta.com.

Updates in your inbox

Sign up below to receive the Carta Policy Team's weekly roundup of public policy developments impacting the private market ecosystem:

DISCLOSURE: This publication contains general information only and eShares, Inc. dba Carta, Inc. (“Carta”) is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein.

All product names, logos, and brands are property of their respective owners in the U.S. and other countries, and are used for identification purposes only. Use of these names, logos, and brands does not imply affiliation or endorsement. ©2024 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.