At every stage of the startup lifecycle, median valuations in venture funding rounds trended down during the fourth quarter of 2022. Some drops were precipitous: At Series D, valuations were 58% lower than a year before.

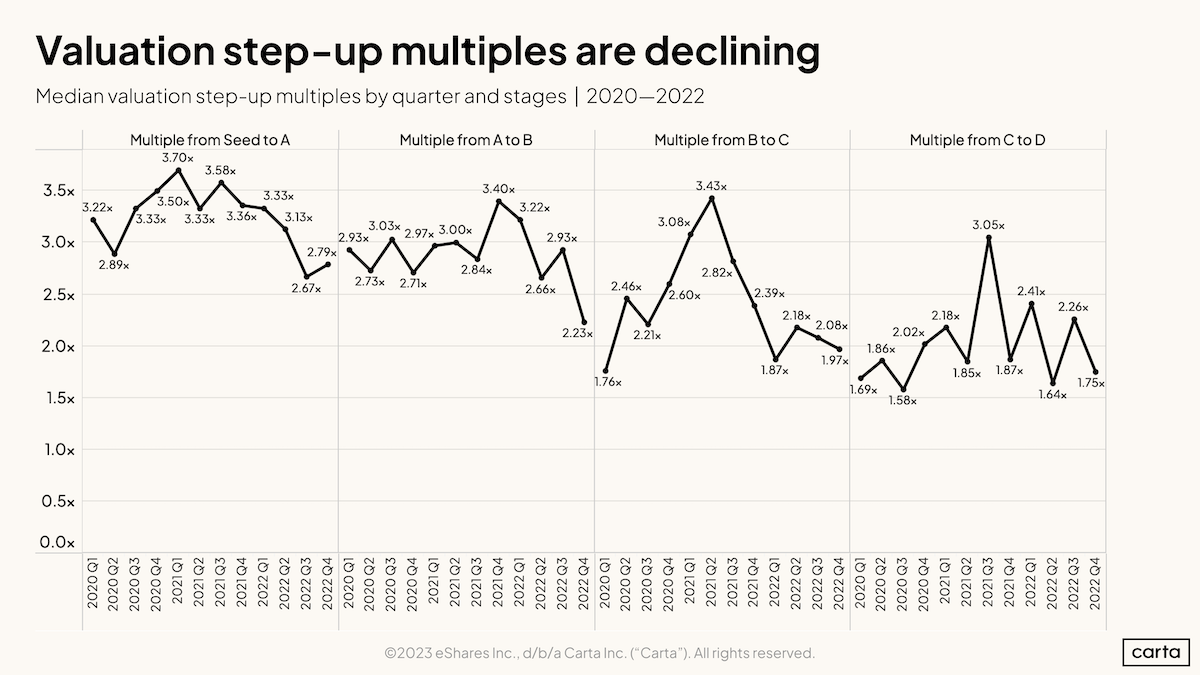

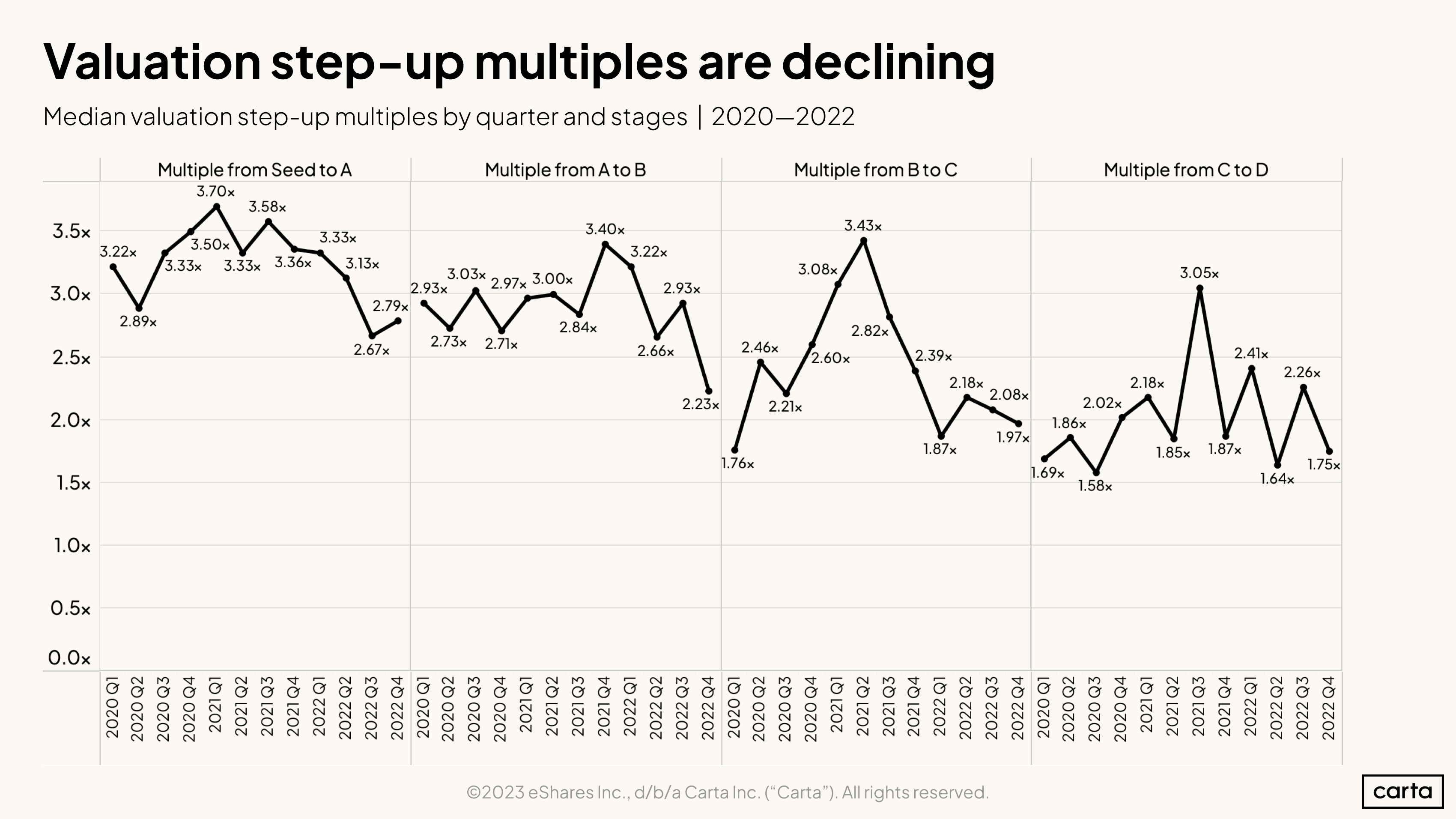

But valuations aren’t just shrinking within each stage. They’re also shrinking when compared against each other—in other words, the valuation gaps between distinct stages are getting smaller. This measure of stage-by-stage valuation growth, called a step-up multiple, can be a useful tool for founders to gauge what kind of valuation increase they might expect when raising their next funding round.

For instance: A year ago, in Q4 2021, the median Series C valuation was 2.39x the median Series B. By Q4 2022, that multiple had declined to 1.85x. The largest year-over-year decline occurred between Series A and Series B, where the median step-up multiple fell from 3.4x to 2.23x.

Valuation step-up multiples are down year over year at every stage

To put these figures into context, a thought exercise: Say Startup X raised its seed round at a $10 million valuation. Using the step-up multiples from Q4 2021, Startup X’s valuation would climb to $33.6 million at Series A, followed by $114.2 million at Series B. By Series D, Startup X would be valued at just over $510 million.

The math is very different if we use the step-up multiples from Q4 2022. In that scenario, Startup X would be valued at $27.9 million at Series A and $62.2 million at Series B—barely half of the Series B with more favorable multiples. Keep going, and Startup X would be worth just $214 million at Series D.

Of course, this is a completely hypothetical example; no company would ever raise five rounds within one quarter. These multiples are also based on medians, so they don’t capture the wide variation in valuations that exists across different sectors and companies. But the exercise helps demonstrate the potential compounding effects of compressed multiples over the course of a startup’s lifespan.

A few other takeaways from our valuations data:

In Q4, the median step-up multiple moving from Series A to Series B sunk to its lowest point in the past three years.

The step-up from seed to Series A is at its second-lowest point in the past three years, and the step-up from Series B to Series C hit its third-lowest point in that span.

SaaS startups are experiencing faster early valuation growth than other industries, with a median step-up multiple from seed to Series A of 3.54x in Q4, compared to 2.79x across all sectors.

On the other side of the coin, the median step-up from seed to Series A among healthtech startups in Q4 fell to just 1.06x.

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.