A casualty of the ongoing downturn in venture capital is the decline of the nine-figure megadeal, a category that gained prominence during the Covid-era venture bonanza.

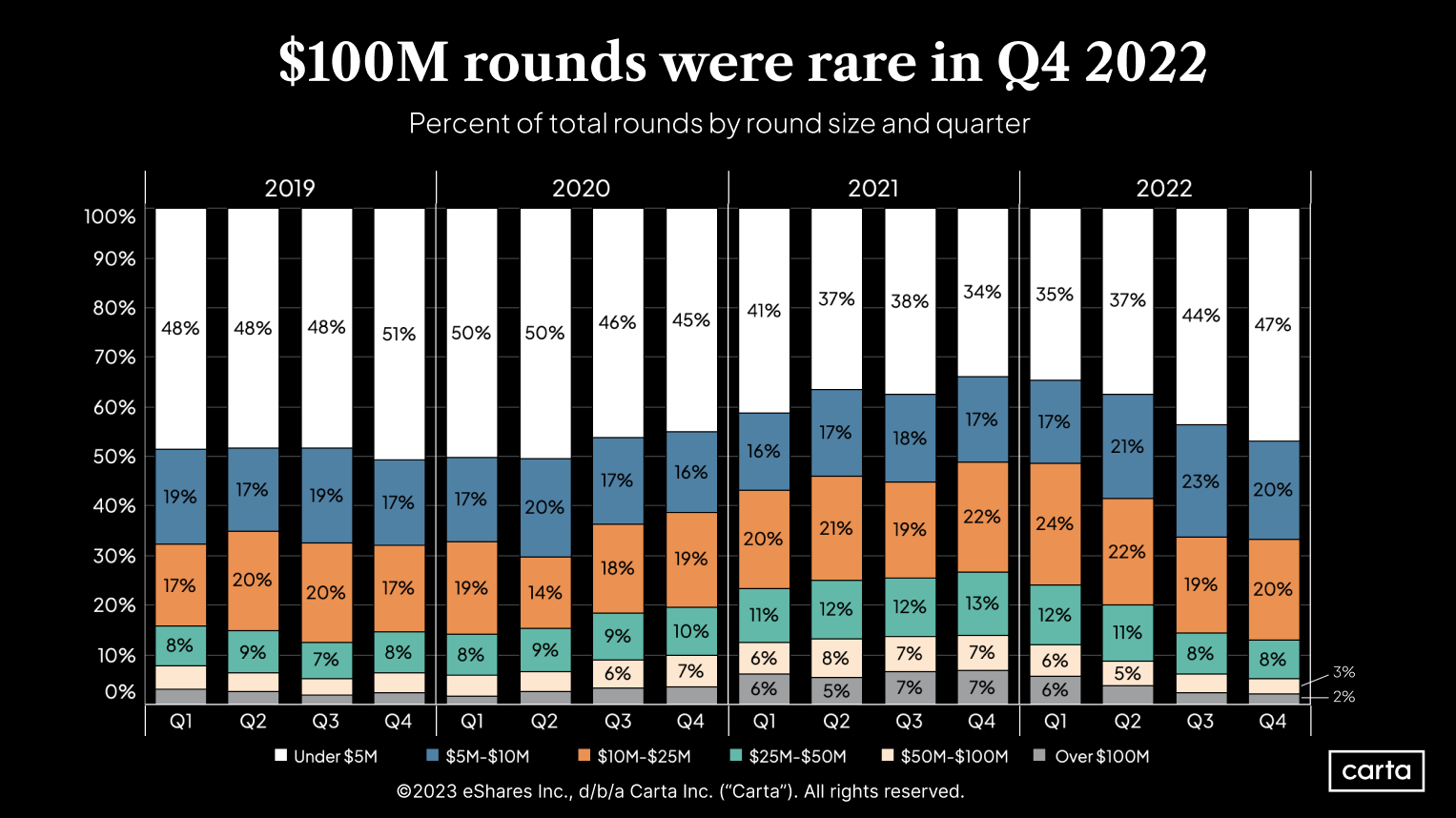

For five straight quarters beginning in Q1 2021, venture deals totaling $100 million or more accounted for at least 5% of all rounds recorded on Carta.

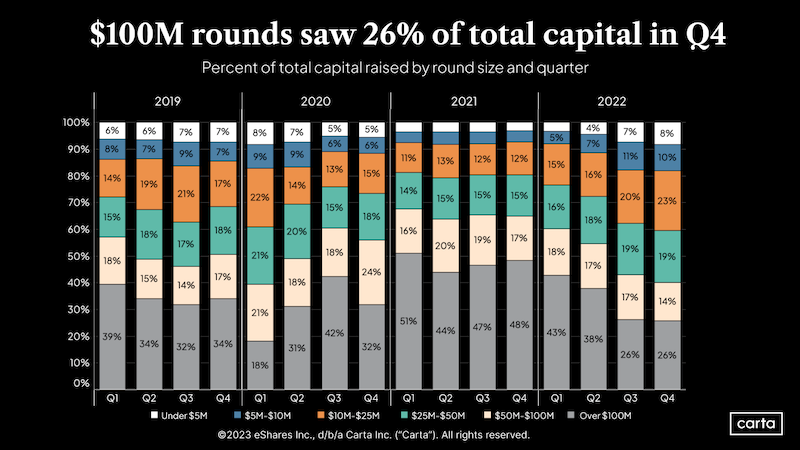

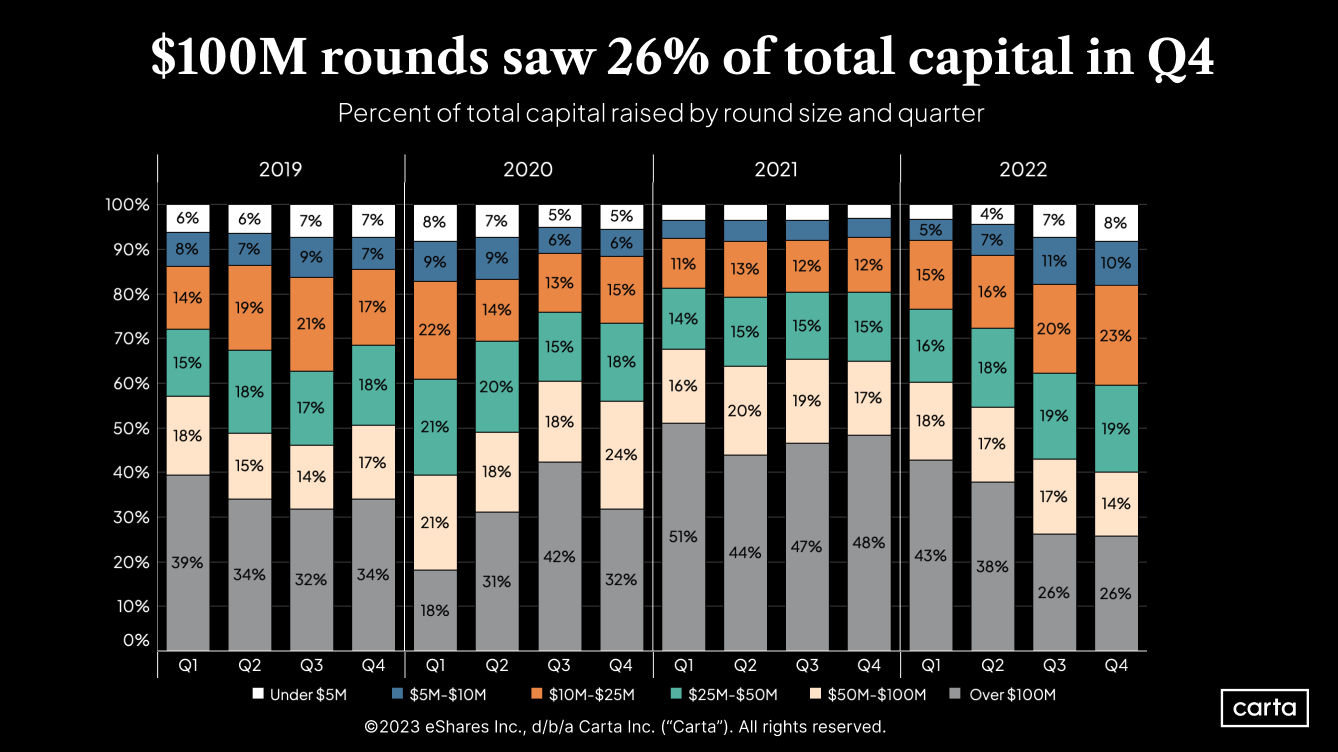

But throughout 2022, VCs investing in late-stage private companies dialed back the pace of megadeals. In Q4 of 2022, just 2% of deals reached the $100 million mark—a return to the lows logged in Q2 2020, when the global Covid-19 pandemic disrupted the financial markets.

Meanwhile, a corresponding trend occurred at the other end of the spectrum: Deals of $5 million or less jumped from 37% of deals in Q2 2022 to up 44% in Q3 and to 47% in Q4.

The percentage decline in megadeals might be small, but viewed as a percentage of total capital raised each quarter, the decline in megadeals is more dramatic: In the past four years, only Q1 2022—the quarter the World Health Organization declared Covid-19 a global pandemic—logged a lower percentage of capital raised from nine-figure deals.

Behind the slump in megadeals

Why are sub-$5 million deals back in the majority? Early-stage deal flow doesn’t correlate as closely to the public markets, which makes early-stage investing more resilient to macroeconomic downturns.

The later stages are another matter.

“Late-stage venture firms compete for deals with a variety of other financial investors,” says Shiloh Tillemann-Dick, research director at the National Venture Capital Association.

In 2021, some of these crossover investors—such as hedge funds, corporate venture capital units, and private equity firms—poured billions into late-stage tech companies, driving up valuations. But as private valuations declined in response to a slide in public tech stocks across 2022, crossover investors retreated from late-stage deals. Inflation and high interest rates took much of the blame for the slump in public tech stocks. But the private markets saw sharper declines for an additional reason: In times of economic upheaval, VC firms often focus first on stabilizing their own portfolios. That cuts down on the number of investors competing for deals and drives down prices.

Rather than risk a down-round, some late-stage private companies turned instead to unpriced bridge rounds rather than raise another priced round.

Dry powder to the rescue?

Some in the venture community have speculated that record levels of VC dry powder, estimated at around $290 billion, could help kickstart dealmaking again in 2023. But investors and industry analysts have raised doubts.

“We’re going to start to see that powder get deployed, but I’m not expecting an avalanche of dry powder to deluge the market,” Tillemann-Dick said. “We can expect to see investors be deliberate in their dealmaking.”

Tillemann-Dick thinks macroeconomic conditions must improve before megadeals return to previous levels.

“The mantra I’m hearing from industry participants is that lower inflation, lower interest rates, and higher market confidence are needed to lead to increased numbers of big, late-stage deals,” he said. “There are a lot of steps required to achieve a healthy version of those market conditions, but those are what people are looking for.”

Learn more:

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.