- How stock options are taxed: A complete guide

- How are stock options taxed?

- ISO vs. NSO

- Taxation at exercise

- Taxation at sale

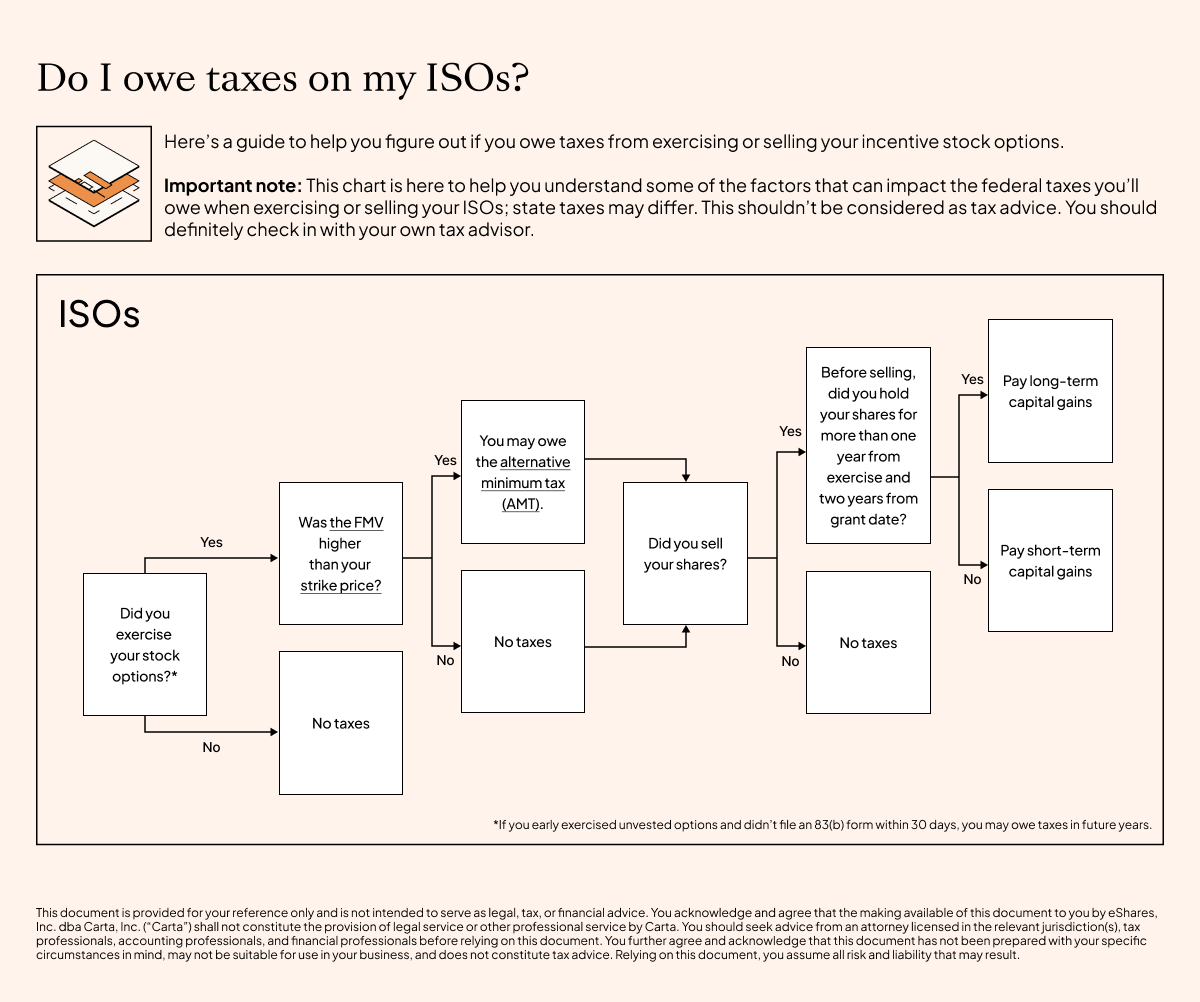

- How incentive stock options are taxed

- ISO taxation at exercise: Alternative minimum tax

- ISO taxation at sale: Qualifying and disqualifying dispositions

- How non-qualified stock options are taxed

- NSO taxation at exercise

- NSO taxation at sale

- Your company’s tax withholding obligation

- Capital gains tax vs. ordinary income tax for stock options

- Capital gains tax for stock options

- Ordinary income tax for stock options

- How to plan for stock option taxes

- Your company’s tax reporting responsibilities

- Form 3921 for ISO exercises

- W-2 reporting for NSO exercises

- Helping your team make smart equity decisions

- Frequently asked questions about stock option taxes

- What is the $100,000 rule for ISO?

- Can employees reduce taxes with qualified small business stock?

- Are stock options taxed twice?

- Download a free stock option taxes reporting guide

A stock option is a type of equity that allows employees and other service providers to buy a set number of shares in the company at a fixed price, called a strike price or exercise price. Your purchase price stays the same over time, so if the value of the stock goes up, you could make money on the difference, called the spread. You may also have to pay taxes on that spread.

The two main types of stock options are incentive stock options (ISO) and non-qualified stock options (NSO). The primary difference between them is how they are taxed, as ISOs could qualify for favorable tax treatment.

How are stock options taxed?

Stock options are typically taxed at two points in time: first when they are exercised and again when they’re sold. According to the IRS, you may receive income when you receive an option, when you exercise it, or when you sell the resulting shares of stock. The specific tax consequences of exercising stock options depend entirely on whether they are ISO or NSO. The tax implications at each stage differ significantly between the two.

ISO vs. NSO

Understanding the distinction between ISO and NSO is the first step in understanding their tax implications. Each type has different rules for who can receive them and how they are taxed.

Feature | Incentive stock options (ISO) | Non-qualified stock options (NSO) |

Who can receive them | Employees only | Employees, contractors, and advisors |

Tax at exercise | No regular income tax, but may trigger alternative minimum tax (AMT) | Ordinary income tax on the spread between exercise price and FMV |

Tax at sale | Gain is taxed as capital gain for qualifying dispositions | Gain is taxed as a capital gain |

Understanding when taxes on equity are due is a common point of confusion for employees. In fact, a survey from Carta found this confusion is so widespread that more than a quarter of employees received a higher-than-expected tax bill after exercising or selling shares.

Taxation at exercise

When you exercise your stock options, your potential tax liability is determined by the difference between your strike price (fixed purchase price) and the current fair market value (FMV) of those stock options.

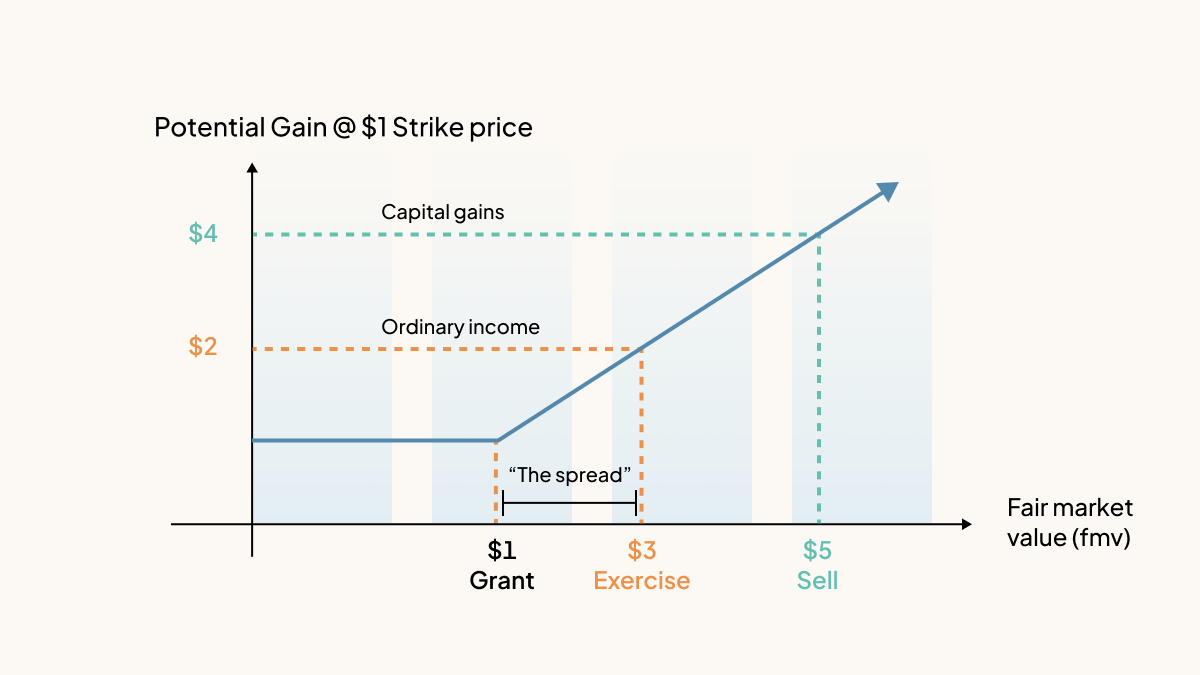

For NSOs, the moment of exercise creates a clear taxable event. The spread is taxable as ordinary income and your company will usually withhold taxes (including federal, payroll, and any applicable state taxes) on the spread when you exercise. For example, if you exercise 100 vested NSOs at a grant price of $1 and the current value is $3, you’ll pay ordinary income tax on the $200 gain at exercise.

For ISOs, there is no regular income tax due at exercise. Instead of the spread being includable in ordinary income tax, it is included as income in something called the alternative minimum tax (AMT) calculation, which could trigger additional taxes owed when you file your tax return.

This financial uncertainty is a major hurdle. A Carta survey found that 23% of employees didn't exercise past employee stock options because they couldn't afford the associated taxes. The employee must pay federal, state, and payroll taxes on that amount, though some may use a cashless exercise to cover these costs.

Taxation at sale

When you sell your company stock, you are taxed on any increase in value you realized on your investment. This gain can be taxed as either ordinary income or capital gains depending on the type of option and your holding period, which is how long the employee owns the shares after exercising them. If you hold the shares for a year or less, the profit is typically taxed at higher short-term capital gains rates. If you hold them for more than a year, the profit may be taxed at lower long-term capital gains rates.

How incentive stock options are taxed

ISOs are a type of stock option that can qualify for special tax treatment. Unlike with NSOs, you only sometimes have to pay taxes when you exercise ISOs. While ISOs offer the potential for a more favorable tax outcome, they come with specific rules that both the company and the employee must follow. Adhering to these rules is what allows employees to receive the special ISO tax treatment. This favorable tax treatment of stock options can make ISO a powerful tool for retaining key employees over the long term.

ISO taxation at exercise: Alternative minimum tax

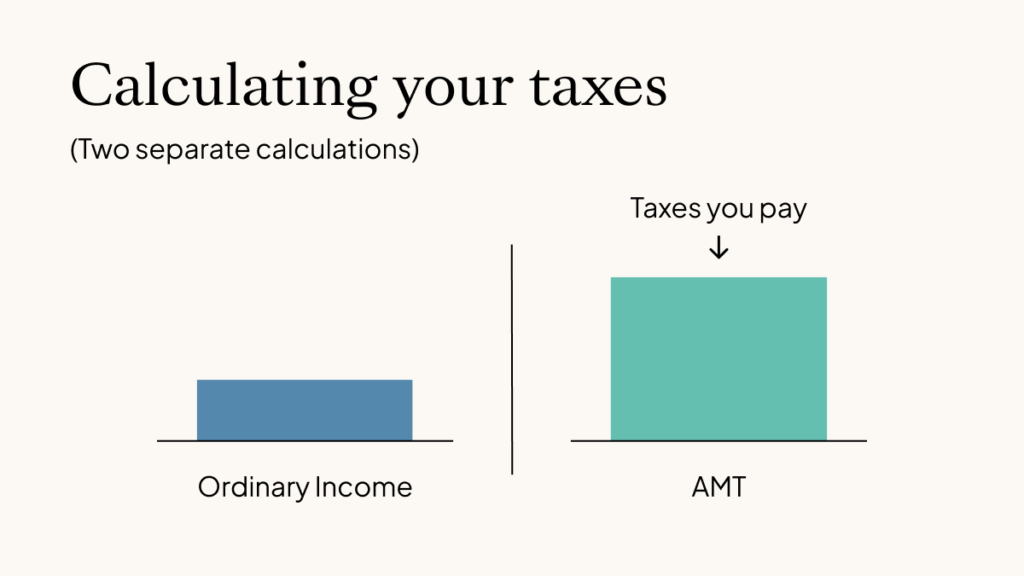

Depending on when you exercise your options and the spread at exercise (the difference between the FMV and your purchase price), the AMT may impact your taxes owed.

The AMT is a parallel tax system, which the IRS defines as a separate tax imposed in addition to your regular tax. Whichever yields a bigger tax obligation—your ordinary tax or the AMT—is the amount you’ll pay. It is meant to help prevent creative tax deductions and write-offs that historically allowed people to avoid or significantly lower their taxes. For AMT purposes, the spread from an ISO exercise is considered income on Form 6251, even if no shares are sold and no cash is received.

This can create a significant risk for employees at high-growth companies. For example, an employee might exercise their ISO when the company’s valuation has grown substantially. The large difference between their low strike price and the current high FMV creates a paper gain that could lead to a large, unexpected tax bill from the AMT.

When you exercise an ISO, the spread is included in your AMT tax calculation. Your company does not withhold AMT on your behalf, so you’re solely responsible. For example, if you exercise 1,000 shares at $1 each when they’re worth $5 each, you need to add $4,000 to your income when calculating AMT. Your regular tax calculation would not change.

AMT applies only if you bought ISOs and did not sell them in the same tax year. We recommend setting aside money any year when you’ve exercised ISOs to pay any year-end AMT obligations if this applies to you.

ISO taxation at sale: Qualifying and disqualifying dispositions

When an employee sells shares they acquired from an ISO exercise, the sale is classified as either a qualifying or disqualifying disposition. This classification determines how the profit is taxed.

Qualifying disposition: This occurs when an employee sells their shares at least two years after the grant date and at least one year after the exercise date. Meeting both of these holding period requirements allows the entire profit from the sale of stock to be taxed at the more favorable long-term capital gains rates.

Disqualifying disposition: This happens if an employee sells their shares before meeting both holding period requirements.

Qualifying dispositions for ISOs

You can take advantage of tax savings for ISOs by meeting certain holding requirements and having a qualified disposition. This will entitle you to the lower long-term capital gains rate on your full taxable gain. To qualify, you must hold the shares for both:

Two years from the date your ISOs were granted, and

One year after exercising your ISOs

If both conditions are met, the difference between your sale price and the price you paid for the ISOs will be subject to preferential long-term capital gains tax.

Disqualifying dispositions for ISOs

If you do not meet the qualifications listed above for a qualifying disposition, the sale of your ISOs may be subject to less favorable tax treatment.

How non-qualified stock options are taxed

Understanding how stock options are taxed at exercise is an important consideration for NSO holders. However, they often result in immediate tax consequences for the employee upon exercise.

The taxation of stock option exercise is the most important event for NSO holders. This action creates a clear taxable event for the employee, and the company has a role to play in managing the resulting tax obligations.

Action | Tax implication |

You exercise your NSOs | You’ll likely pay ordinary income tax on the difference between your strike price and the current market price of the stock |

You exercise and sell your NSOs in one transaction | You’ll likely pay ordinary income tax on the difference between your strike price and the current market price of the stock |

You sell your NSOs within a year of exercising | You’ll likely pay short-term capital gains taxes on the profit you made selling your options |

You sell your NSOs after holding them for at least a year | You’ll likely pay long-term capital gains taxes on the profit you made selling your options |

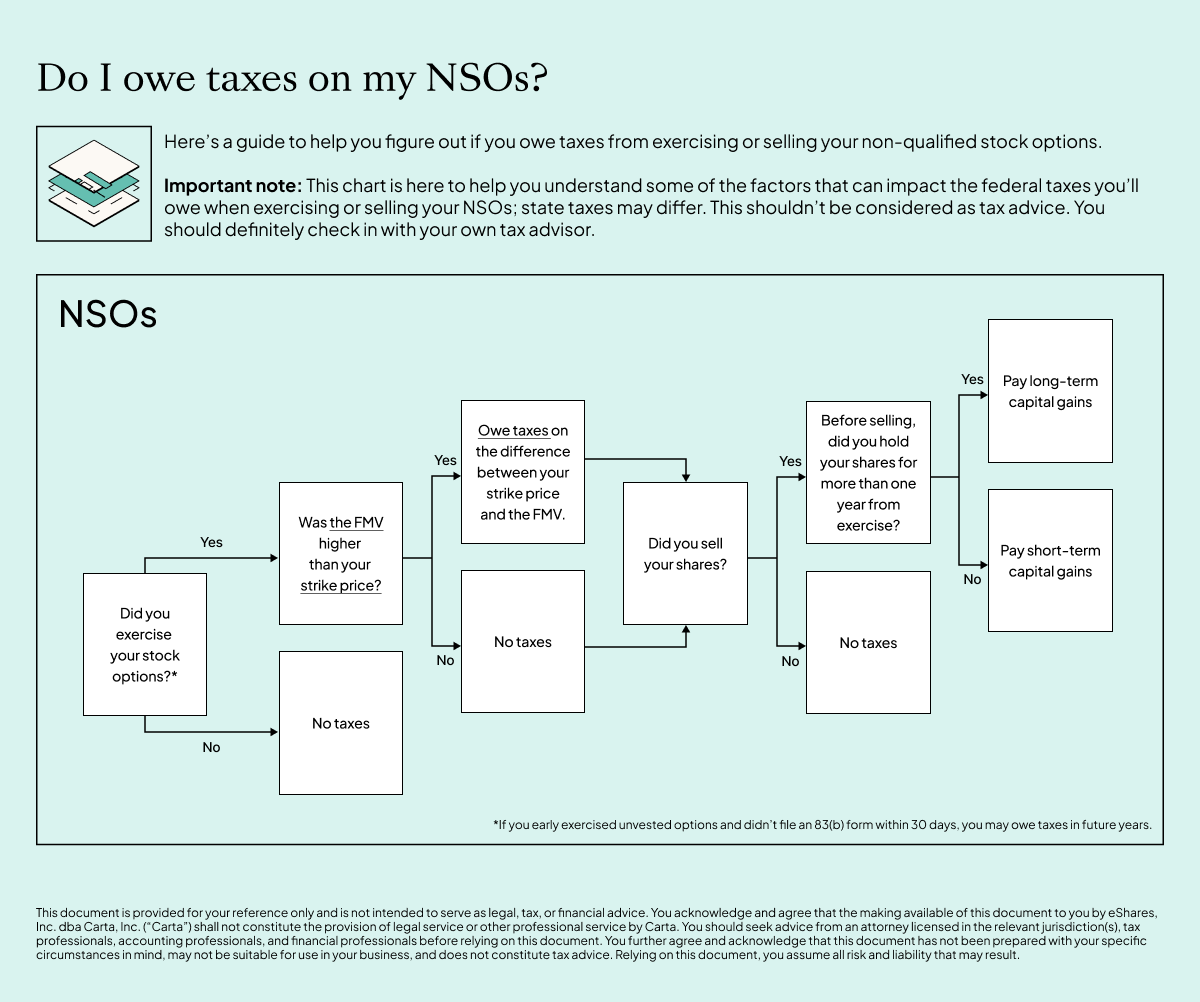

NSO taxation at exercise

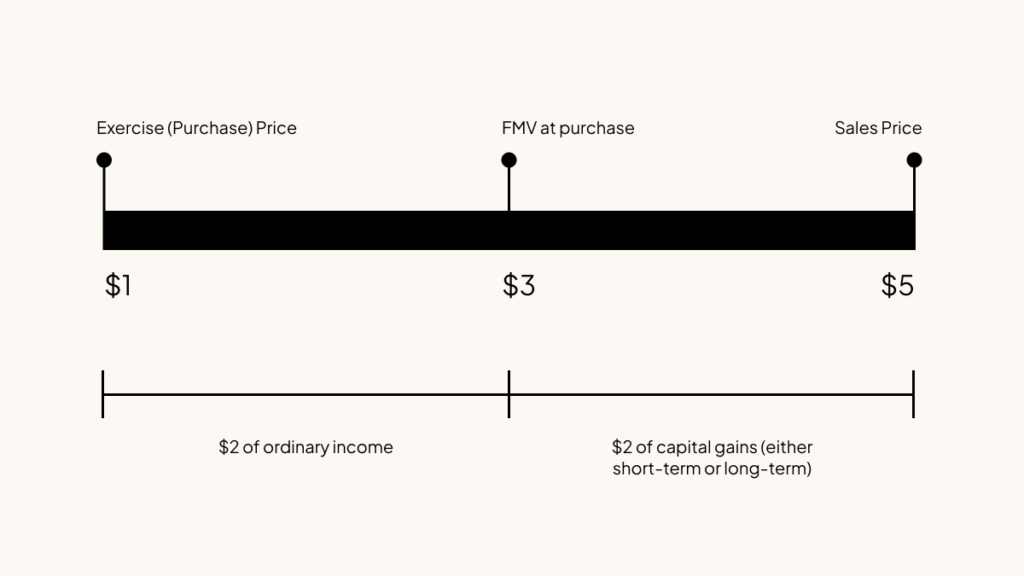

With NSOs, you could trigger taxes both when you exercise and when you sell your options. This usually means you pay more taxes with NSOs than with ISOs.

When you exercise an NSO, any spread between the FMV on the date you exercise and the price you are paying for the stock is considered ordinary income to you. Your company will usually withhold ordinary income tax (including federal, payroll, and any applicable state taxes). Typically, because there is no cash involved in the transaction, you will need to pay your employer to cover the cost of the withholdings at purchase.

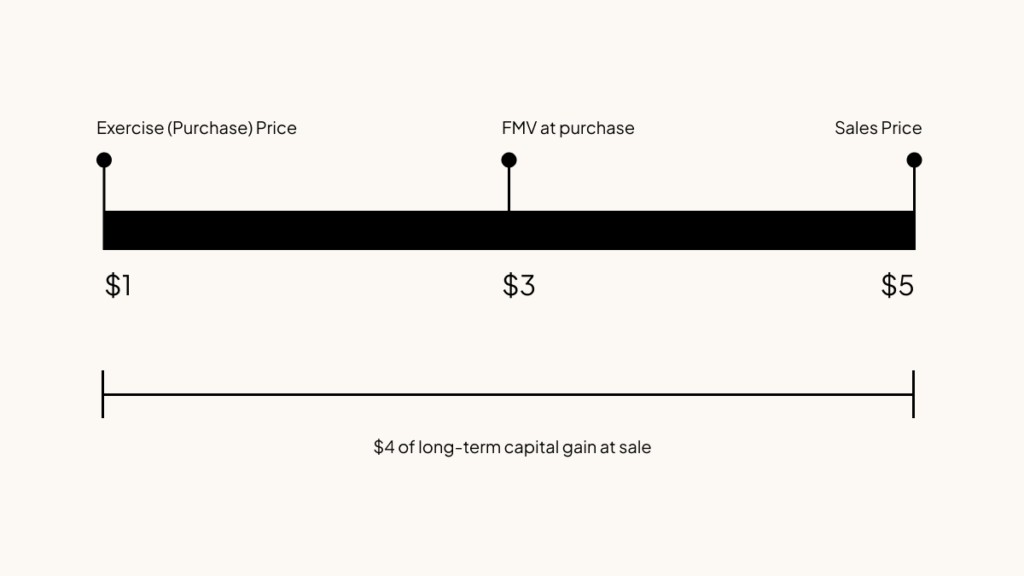

NSO taxation at sale

When you sell NSOs, any appreciation on the stock will be taxed as capital gains. The taxable capital gain for NSOs is calculated by subtracting the FMV of the stock on the day you purchased your shares from the sale price.

Your company’s tax withholding obligation

When an employee exercises NSO, your company is legally required to withhold ordinary income and payroll taxes, such as Social Security and Medicare, on the spread. This is because the spread is considered supplemental wages, and these types of share-based payments have specific tax and accounting rules.

This creates an administrative responsibility that requires accurate, real-time data on your company’s valuation and your employees’ grants. Managing this process manually with spreadsheets is prone to costly errors and can become a significant compliance risk. A platform like Carta automates these calculations directly from your cap table, helping you stay compliant and saving your team valuable time.

Capital gains tax vs. ordinary income tax for stock options

There are two types of taxes you need to keep in mind when dealing with your options: ordinary income tax and capital gains tax.

Capital gains tax for stock options

You’ll likely pay capital gains tax on a portion of the profit when you sell stock you have previously exercised. For tax purposes, there are two types of capital gains:

Short-term capital gains: If you have held the stock for one year or less from the date of exercise

Long-term capital gains: If you have held the stock more than one year from the date of exercise

Short-term capital gains are not tax preferential and are taxed at ordinary income rates. However, long-term capital gains are taxed at lower rates. The tax rate for long-term capital gains is between zero and 20%. Therefore, holding your shares long enough to qualify for long-term rates is favorable for tax purposes if you are selling at a gain.

Ordinary income tax for stock options

If a portion of your taxable gain is subject to ordinary income tax (as described above), you will be taxed at the same rate as the rest of your ordinary income based on your taxable income, filing status, and tax bracket.

The ordinary income tax rate is currently almost double the long-term capital gains tax rate, so optimizing your exercise strategy to maximize the benefits of long-term capital gains tax treatment will most likely result in lower tax liabilities.

How to plan for stock option taxes

When you exercise your stock options, gains are not guaranteed. All investment decisions, including whether or not to exercise, carry risk. Reach out to a CPA, professional tax advisor, or legal advisor to understand your options.

If your company uses Carta's equity management software, you may have access to Carta Equity Advisory for free.

Your company’s tax reporting responsibilities

Issuing equity is a sign of a growing company, but it also comes with specific IRS reporting requirements. As a founder, running a professional and compliant company builds trust with investors, auditors, and employees.

Failing to meet reporting obligations can result in penalties and create significant confusion for your team. This internal communication gap is widespread: According to a survey of employees on the Carta platform, 41% don’t know who to talk to at their company about how their equity is taxed.

Form 3921 for ISO exercises

Your company must file this form with the IRS for each transfer of stock to an employee who exercised an ISO during the tax year. You must also provide a copy of this form to each of those employees.

This form provides the information an employee needs to accurately calculate their potential AMT liability on their personal tax return. It includes details like the grant date, exercise date, strike price, and the FMV of the stock on the date of exercise. Carta’s tax and compliance tools can automatically generate and distribute these forms, simplifying a complex annual process.

W-2 reporting for NSO exercises

The ordinary income an employee recognizes from an NSO exercise must be included as wages on their Form W-2 for that year. This amount is added to their regular salary and other compensation, similar to how income from a restricted stock unit (RSU) is reported.

This requirement reinforces the value of having a clean, accurate cap table as the single source of truth for all equity data. It prevents reporting mistakes that could lead to compliance problems with the IRS and payroll tax authorities, which is why following guidelines like ASC 718 is important.

Helping your team make smart equity decisions

Helping employees understand their ownership is a common challenge for leaders at growing companies. A 2022 survey found that while 69% of employees think it’s important for their company to help them understand how their equity works, only 37% believe their companies provide adequate equity education.

As a founder, you want to empower your team with knowledge about their equity. However, you cannot provide personalized tax or legal advice, which can put you in a difficult position when you receive employee questions.

This is where a dedicated service can bridge the gap. Speak to an expert to learn how Carta Equity Advisory can help your team make informed decisions.

Frequently asked questions about stock option taxes

What is the $100,000 rule for ISO?

For any employee, only the first one hundred thousand dollars worth of ISO that become exercisable in a single calendar year can receive the special ISO tax treatment, a rule known as the ISO $100,000 limit. Any amount above this limit is automatically treated and taxed as an NSO.

Can employees reduce taxes with qualified small business stock?

Qualified small business stock (QSBS) is a U.S. tax incentive that may allow shareholders to exclude some or all of their capital gains from federal tax when they sell their shares, effectively making the gain tax-free. To qualify, both the company and the shareholder must meet a number of specific requirements, including a five-year holding period for the stock, which requires the holder to exercise their options to begin the holding period.

Are stock options taxed twice?

NSOs are taxed at two different times on two different types of gains. You first pay ordinary income tax on the spread at the time of exercise, and then pay a second time as a capital gain on any additional profit when the shares are eventually sold, which could happen after an employee exercises during their post-termination exercise period.

Download a free stock option taxes reporting guide

Find out when and how to report taxes on your stakeholders' ISOs or NSOs. Download our step-by-step guide to company tax reporting requirements.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.