In Q2 2020, the U.S. went into an economic recession after the longest economic expansion in history. We saw record unemployment numbers and businesses—especially small businesses—struggle to keep their doors open.

To examine the impact on private markets, Carta examined its data1, including the cap tables of more than 16,000 companies.

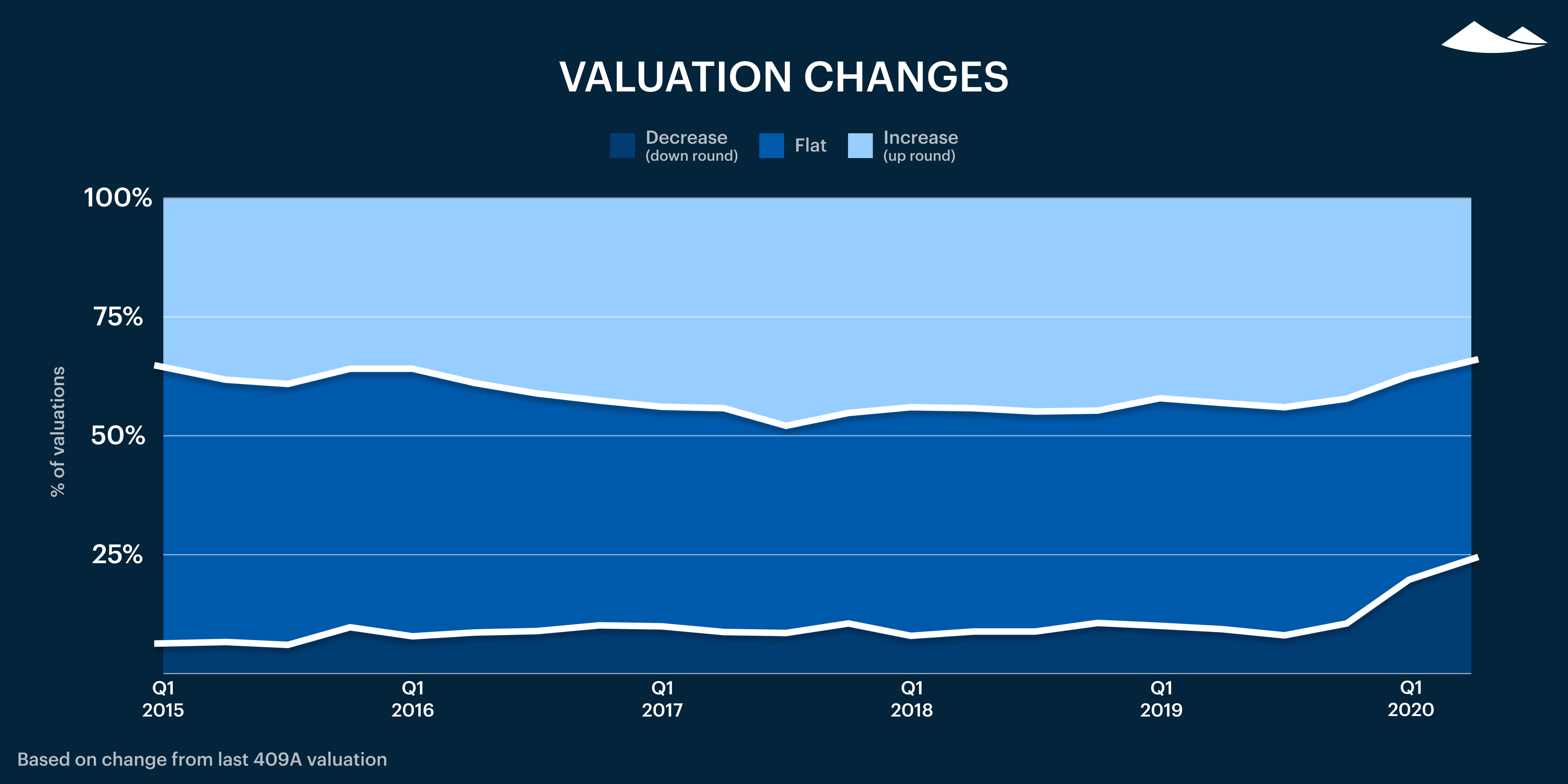

As others have reported, including Crunchbase and Pitchbook with the NVCA, the number of VC financings declined in Q2 while valuations stayed relatively flat across the board. In this report, we expand on the impact COVID-19 has had on employee shareholders as well as investors with data on employee terminations, equity left on the table, company valuations, and deal sizes.

More on methodology can be found at the end of the report.

Employee shareholders in Q2 2020

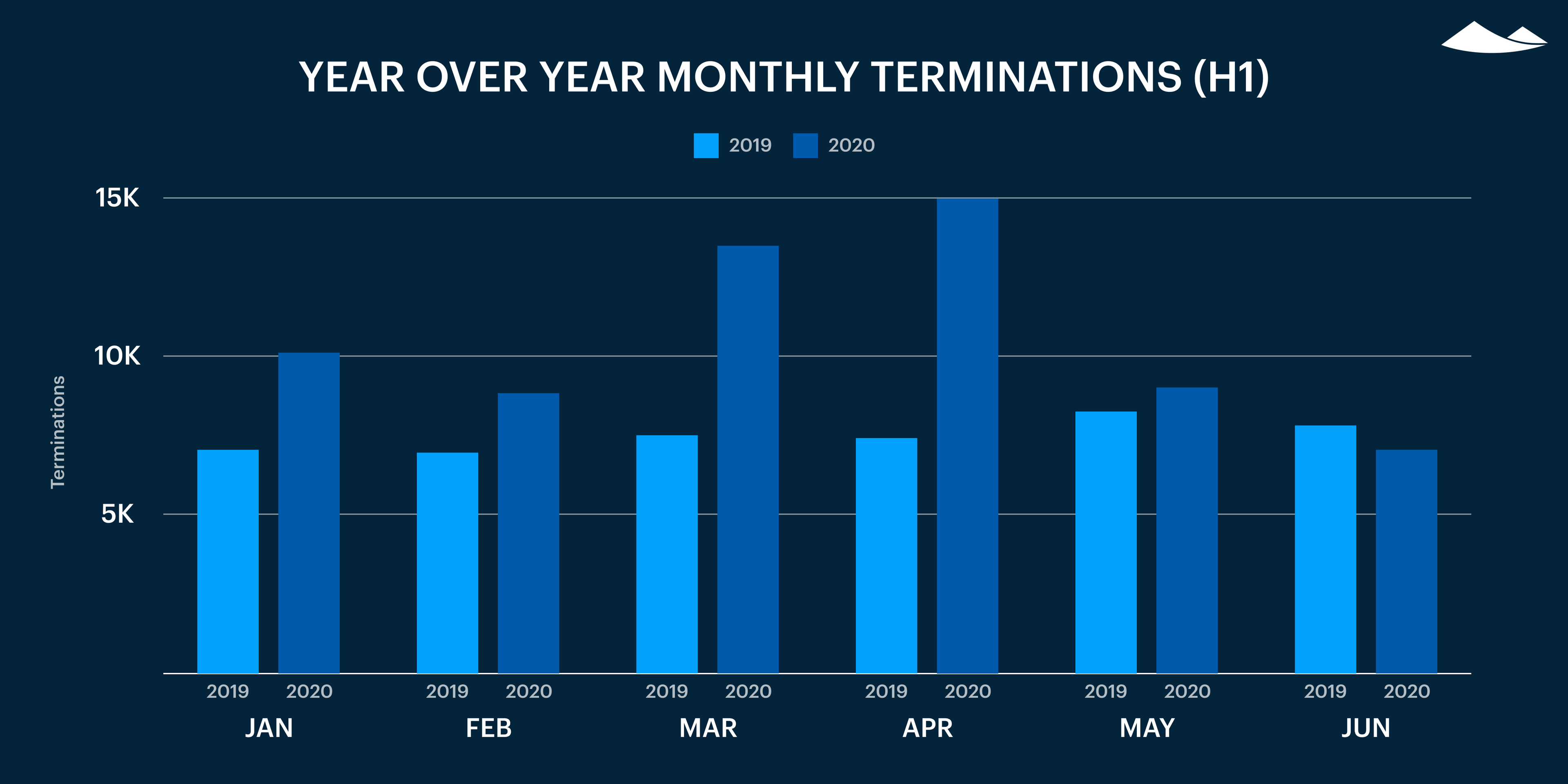

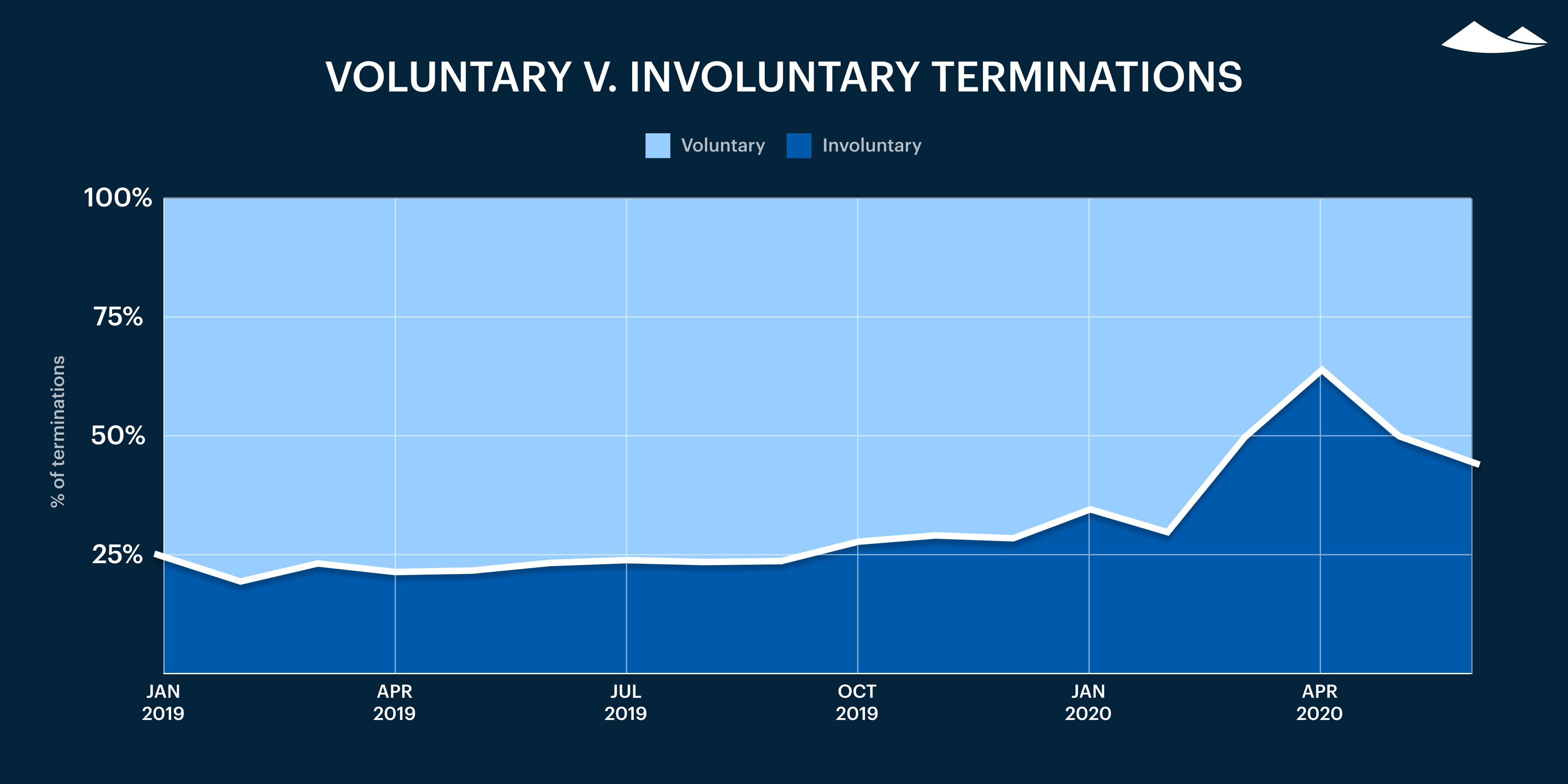

In Q2 2020, involuntary terminations exceeded voluntary terminations for the first time in the history of our data, which dates back to 2015.

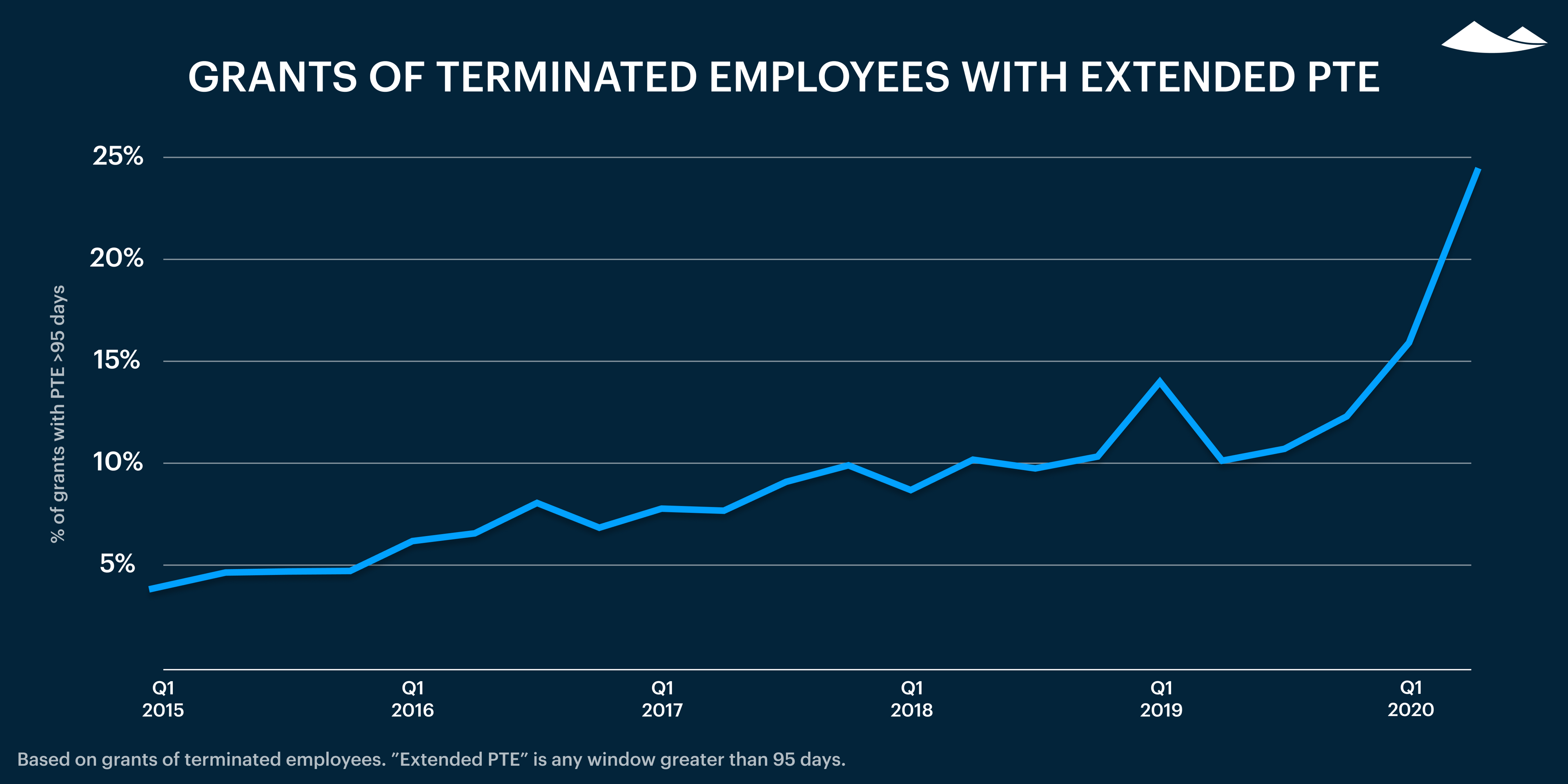

Many companies extended their post-termination exercise period beyond the standard 90 day window in light of this crisis. Some, including Carta, even eliminated the one year vesting cliff for employees affected by layoffs related to COVID-19. Our data show a 48% increase in the percentage of terminated grants with a PTE period longer than 90 days between Q1 and Q2 of 2020.

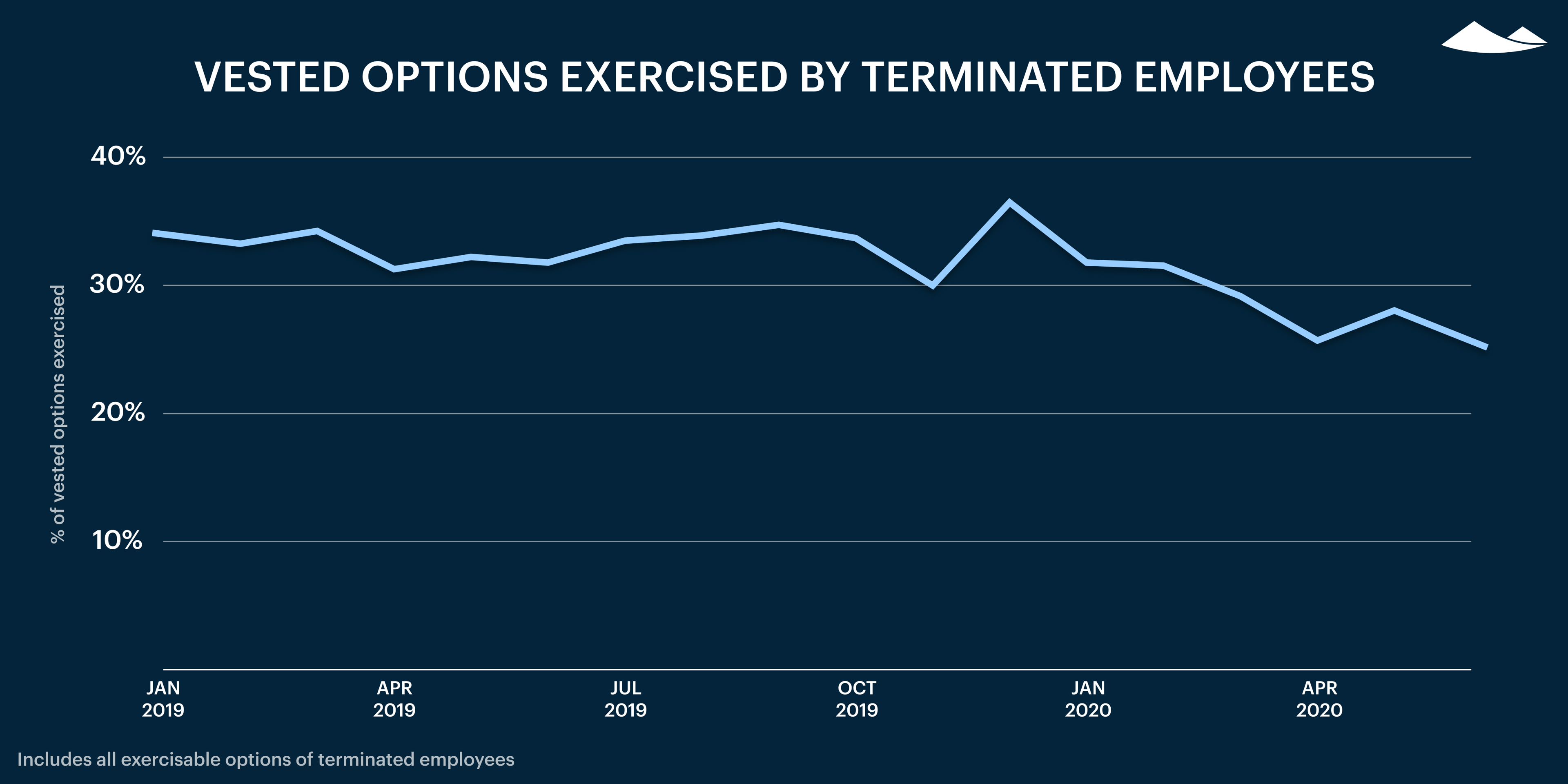

Despite positive trends in extended PTE windows, an unprecedented amount of vested equity was canceled in Q2 of 2020. After the spike in involuntary terminations in March and April, our data show that the percentage of vested options exercised dropped 20% compared to pre-COVID levels.

Private company equity in Q2 2020

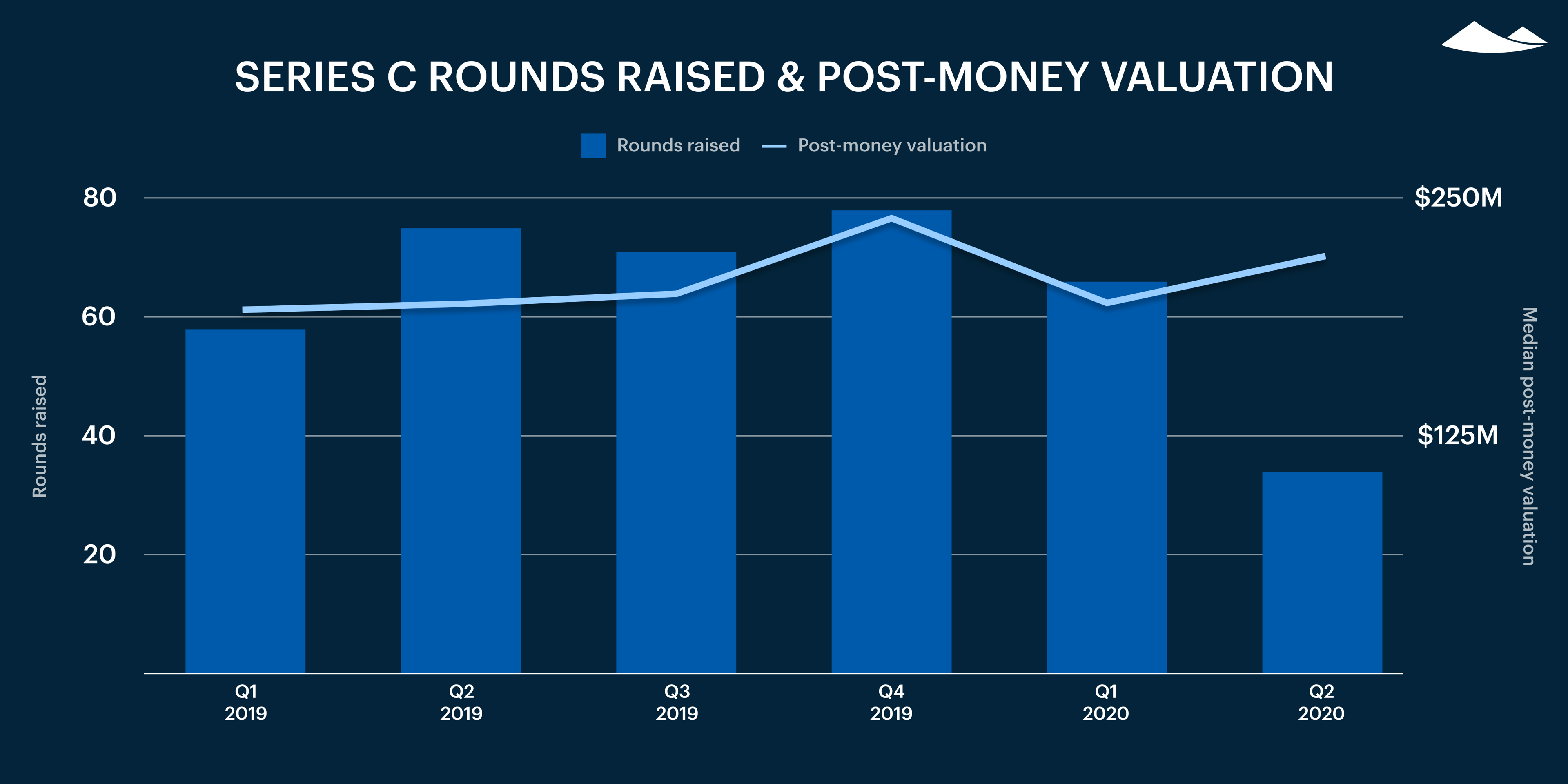

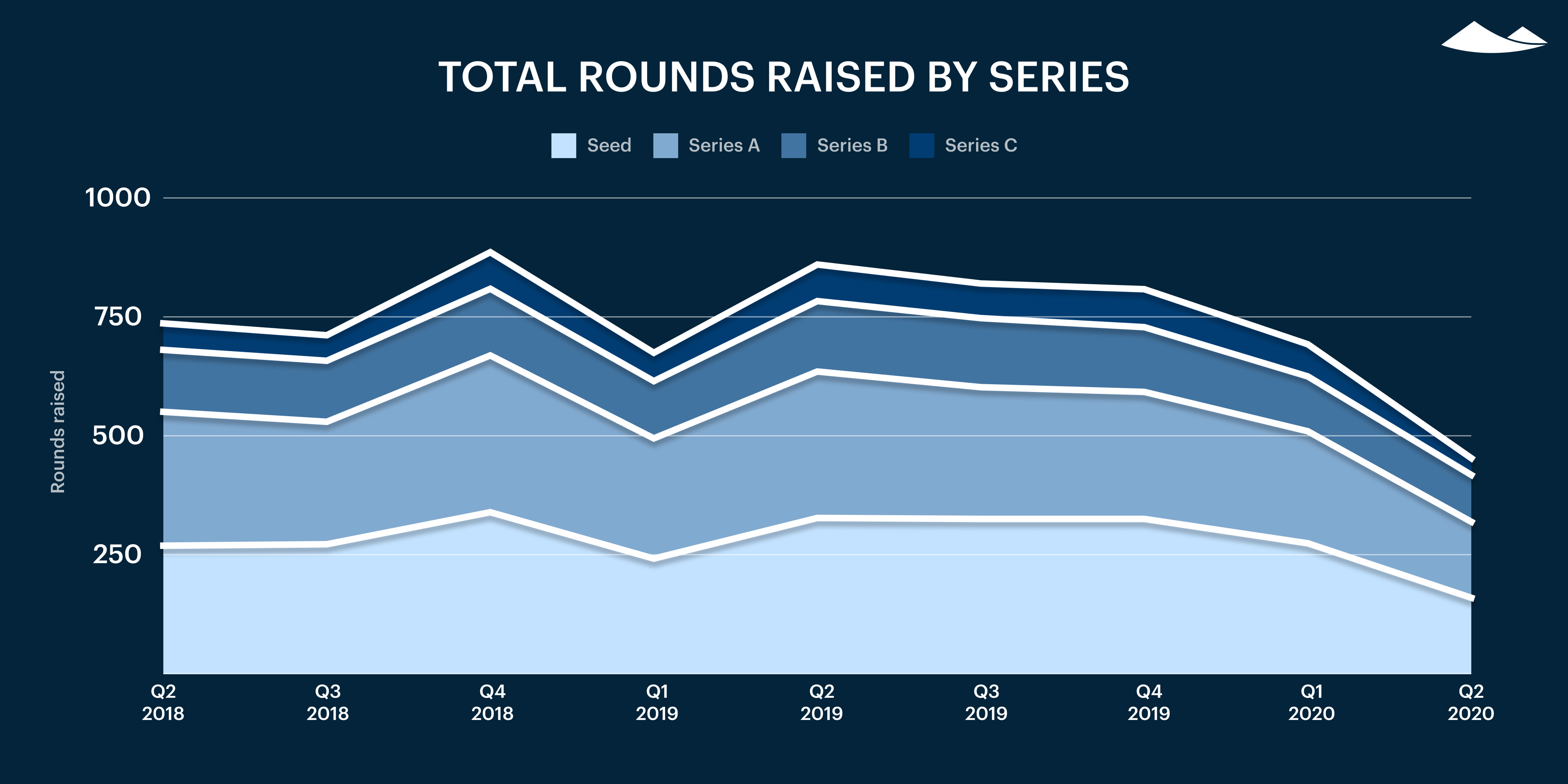

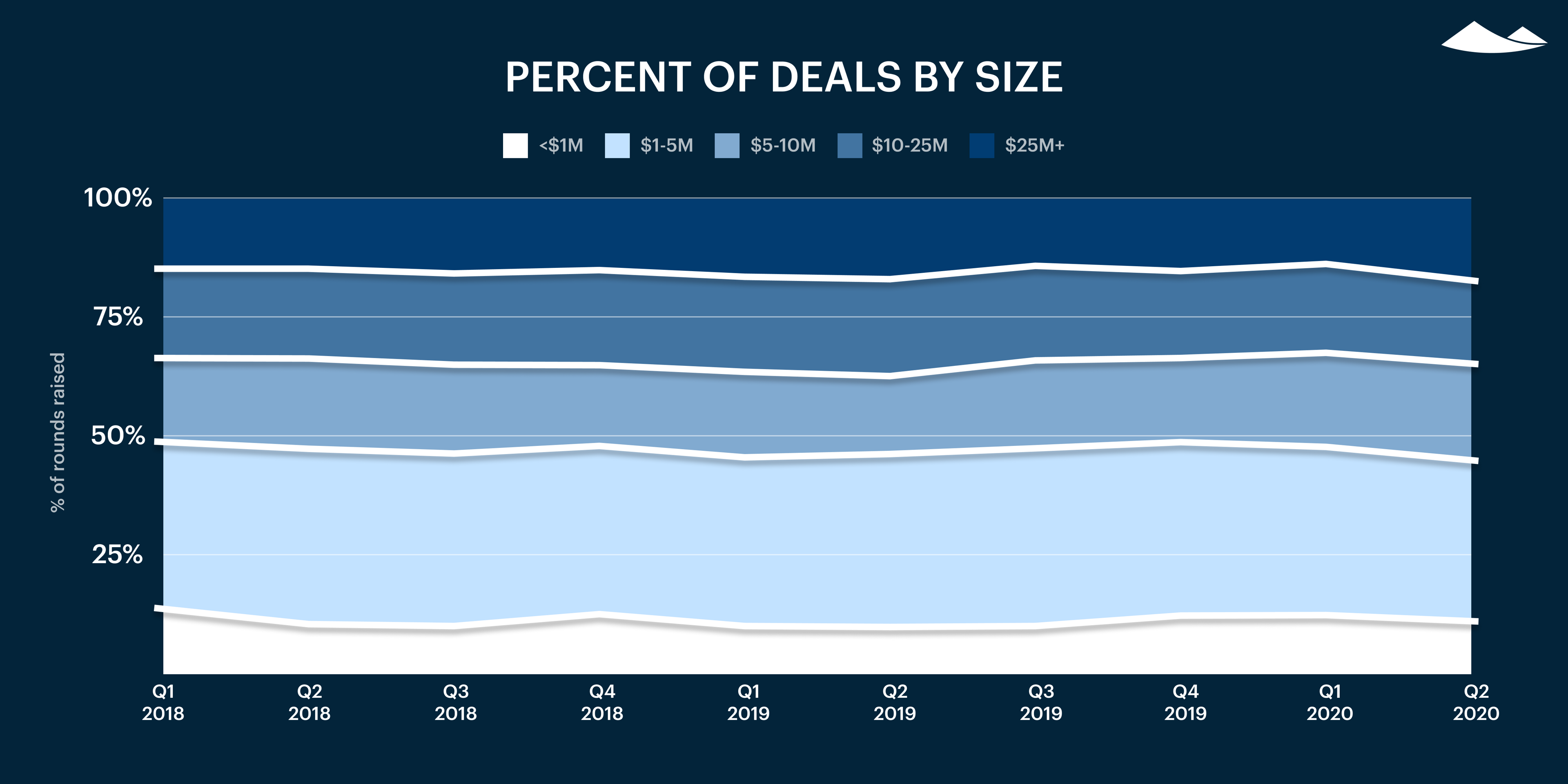

Q2 2020 saw 42% fewer rounds raised than Q2 2019. Median valuation across series remained flat YoY.

While our data show the number of deals decreasing across stage, both Seed and Series C financings enjoyed increases in median valuation (14% and 13% respectively).

Q2 2020 | YoY change | Q2 2020 | YoY change | |

Seed round | 160 | -51% | $11,999,977 | +14% |

Series A | 159 | -48% | $35,060,504 | — |

Series B | 98 | -34% | $88,991,769 | -10% |

Series C | 34 | -55% | $194,632,782 | +13% |

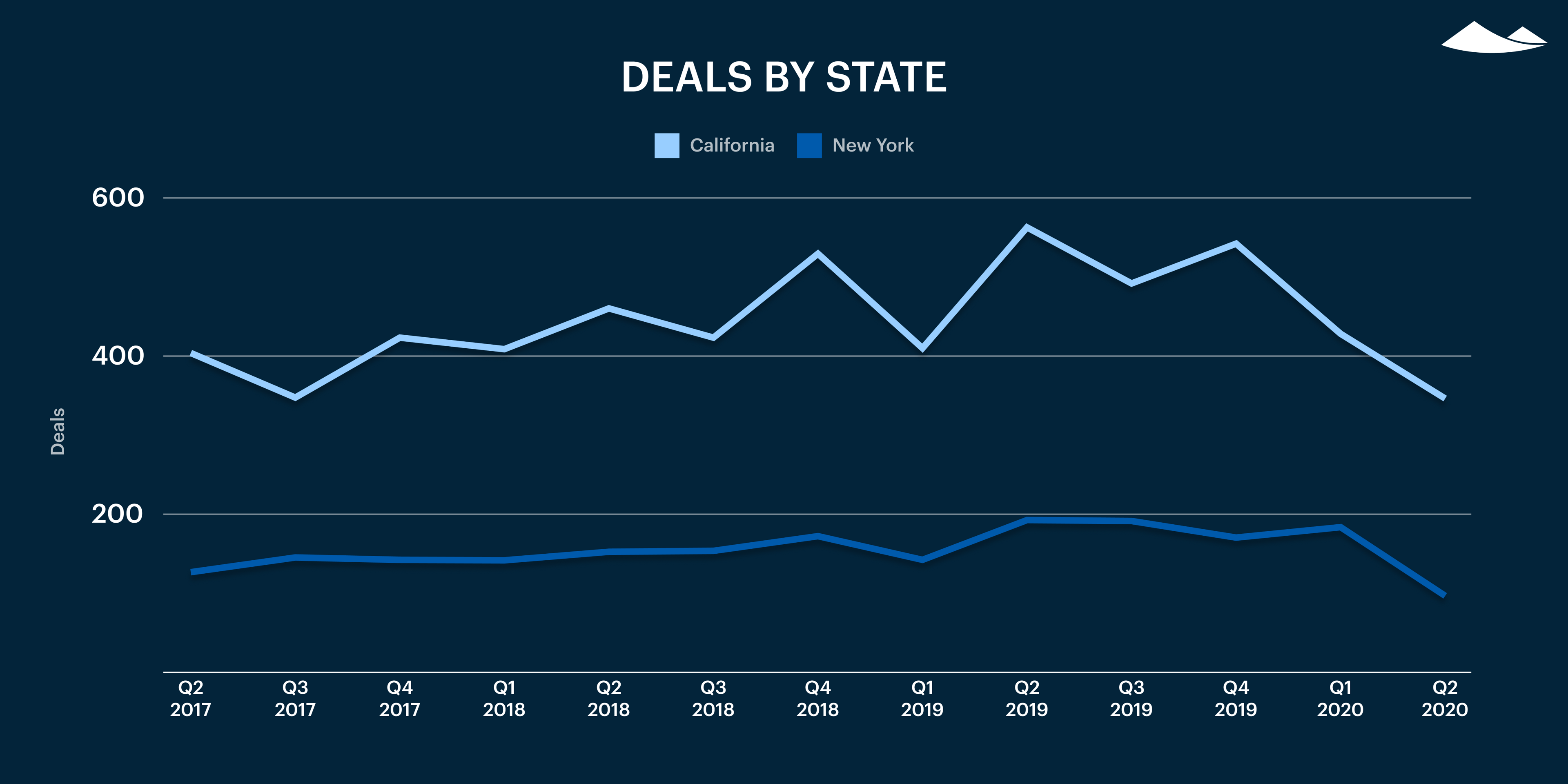

Regionally, California companies saw the biggest decline in dealmaking (-21% quarter over quarter from Q4 2019 to Q1 2020 and -19% from Q4 2019 to Q2 2020), whereas New York saw a more pronounced dip in dealmaking in Q2 (-47% quarter over quarter from Q1 2020 to Q2 2020). The H1 changes between CA and NY are similar—25% and 23% respectively.

When we examined the percentage of deals by state, we found that dealmaking in California dipped in Q1 and then remained flat in Q2.The decline in NY deals did not decline significantly until Q2. Massachusetts followed a similar trend as California despite the Gov. issuing a “recommendation” to SIP on March 24.

Venture Capital investors in Q2 2020

Overall, Venture Capital investors did fewer deals in Q2 (-43% YoY comparing Q2 2019 to Q2 2020).

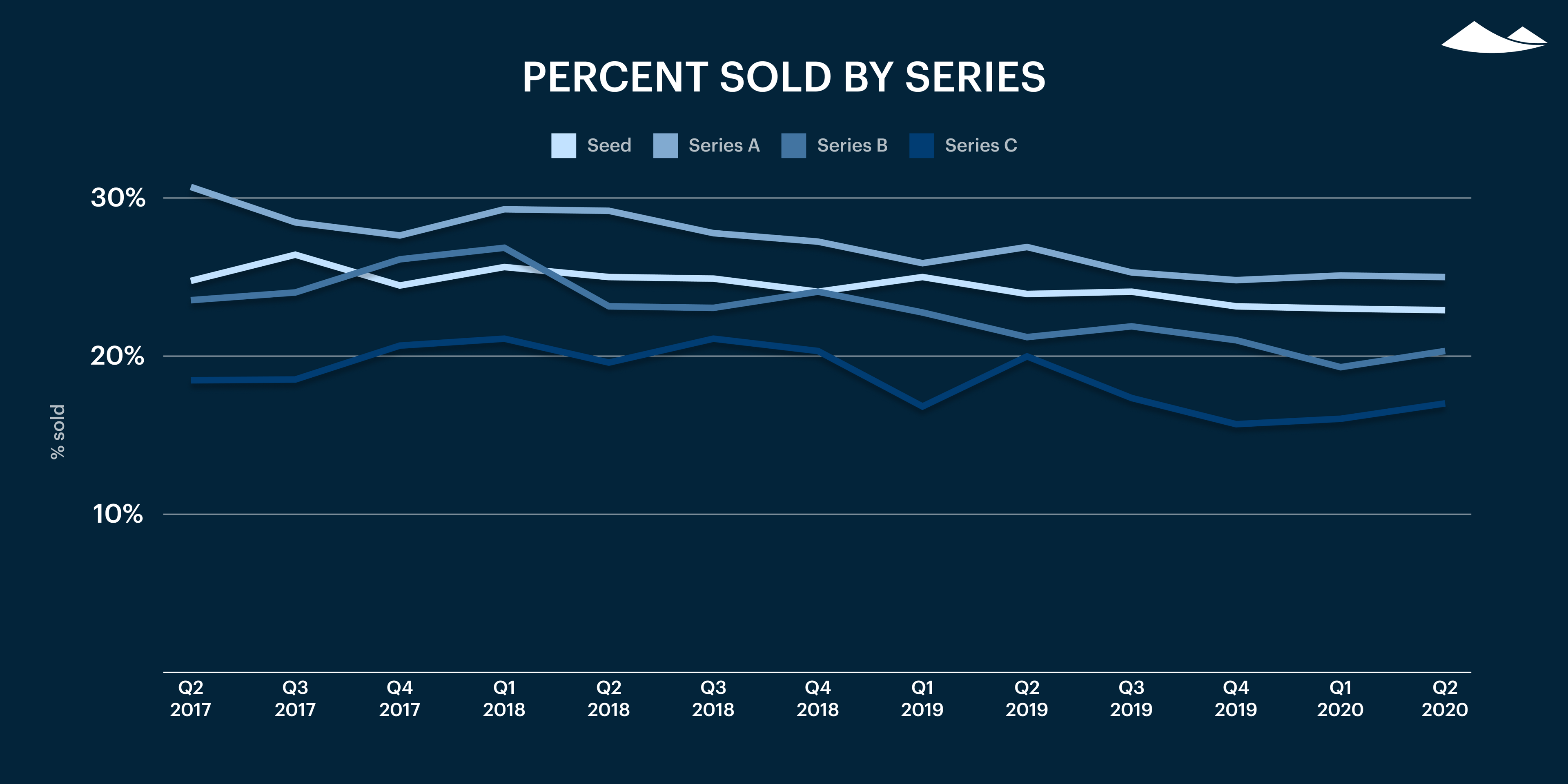

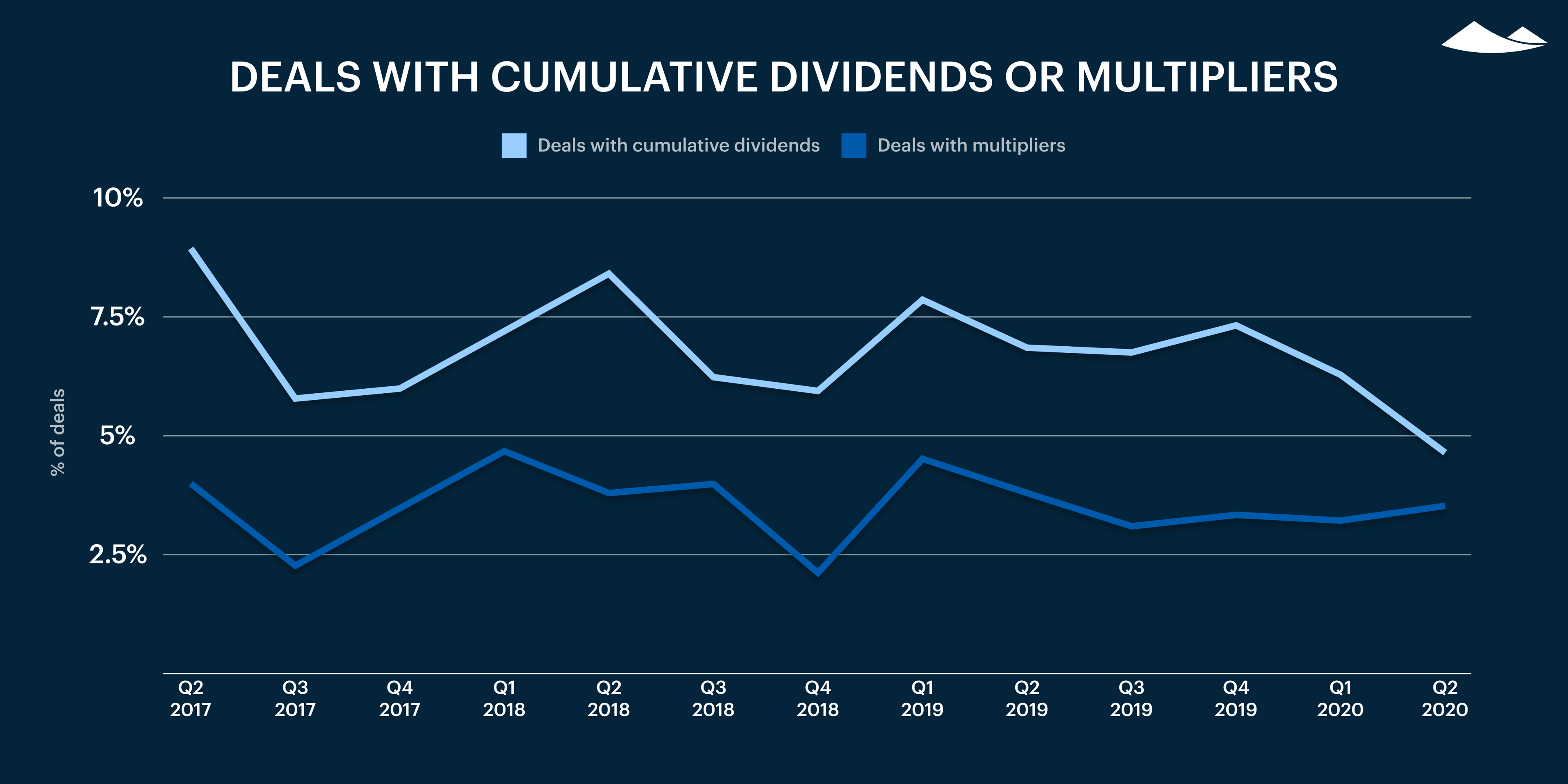

The percent of the company sold during a round was unaffected by the COVID crisis and continues to trend downward. Additionally, the percentage of deals with cumulative dividends continues to decline slightly and multipliers continue to be rare—included in less than 5% of deals—despite the economic downturn.

Conclusion

Carta’s data provides insight into private equity and venture capital. We will continue to report on the state of private markets in an ongoing series.

Methodology

Overview

Carta helps over 16,000 primarily venture backed companies and 1,000,000 security holders manage equity. This study uses an aggregated and anonymized sample of Carta’s cap table data. Companies who have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

The data presented in this private markets report was taken as of July 22, 2020. Historical data may change in future studies because there is typically an administrative lag between the time a transaction took place and when it is recorded in Carta. In addition, new companies signing up for Carta’s services will increase historical data available for the report.

Financings

Financings include equity deals raised in USD. The financing “Series” (e.g. Series A) is taken from the legal share class name. Financing rounds that don’t follow this standard are not included in any data shown by Series but are included in data not shown by Series.

Primary rounds are defined as the first equity round within a Series. Bridge rounds are defined as any round raised after the first round in a given Series. If there is no indication that a round is a Primary or Bridge round, both are included.

In some cases, convertible notes are raised and converted into multiple share classes within a Series at various discounted prices (e.g. Series A-1, Series A-2, Series A-3). In these cases, converted securities are not included in Cashed Raised and only the Post Money Valuation of the new money is included.

Terminations

Terminations entered into Carta must include a reason. Involuntary terminations include both terminations for performance and company layoffs. Voluntary terminations are employees that decided to leave of their own accord. Other termination reasons, including For Cause, Death, Disability, and Retirement were not included in the data and make up less than 1% of all terminations combined.

Many companies have variable Post Termination Exercise Periods (“PTEPs”) based on the employment length of the terminated employee. The PTEP for an option is only known once an employee has been terminated.

1 This study uses an aggregated and anonymized sample of Carta’s cap table data. Companies who have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta, Inc. (“Carta”). This communication is not to be construed as legal, financial, accounting or tax advice and is for informational purposes only. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein.