Venture capital closed out 2020 strong, despite a hard hit by COVID 19 at the beginning of the year. Q3 2020 saw the seeds of recovery, with median valuations and involuntary terminations returning to pre-COVID levels. In Q4, recovery became growth in many areas except headcount, which remains low.

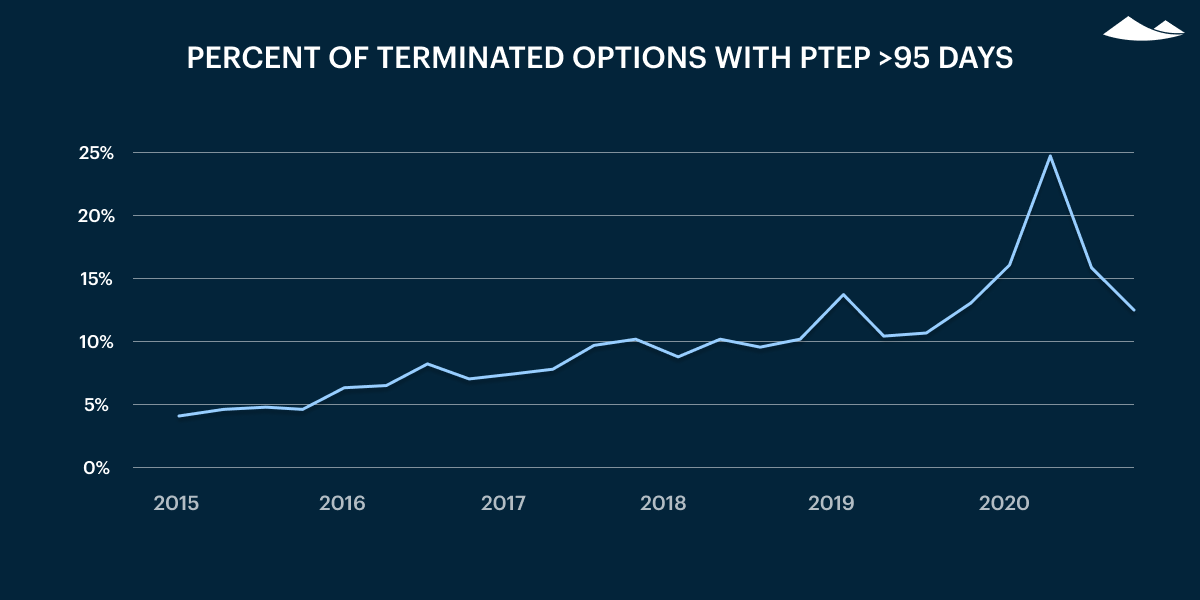

Companies are returning their post-termination exercise periods to their pre-COVID lengths. March of 2020 saw a lift in the percentage of post-termination exercise periods longer than 95 days. That percentage has once again dipped to 12.5%, implying that the extended PTEP periods were not a change in company policy but an exception made for those being laid off due to the effects of the pandemic.

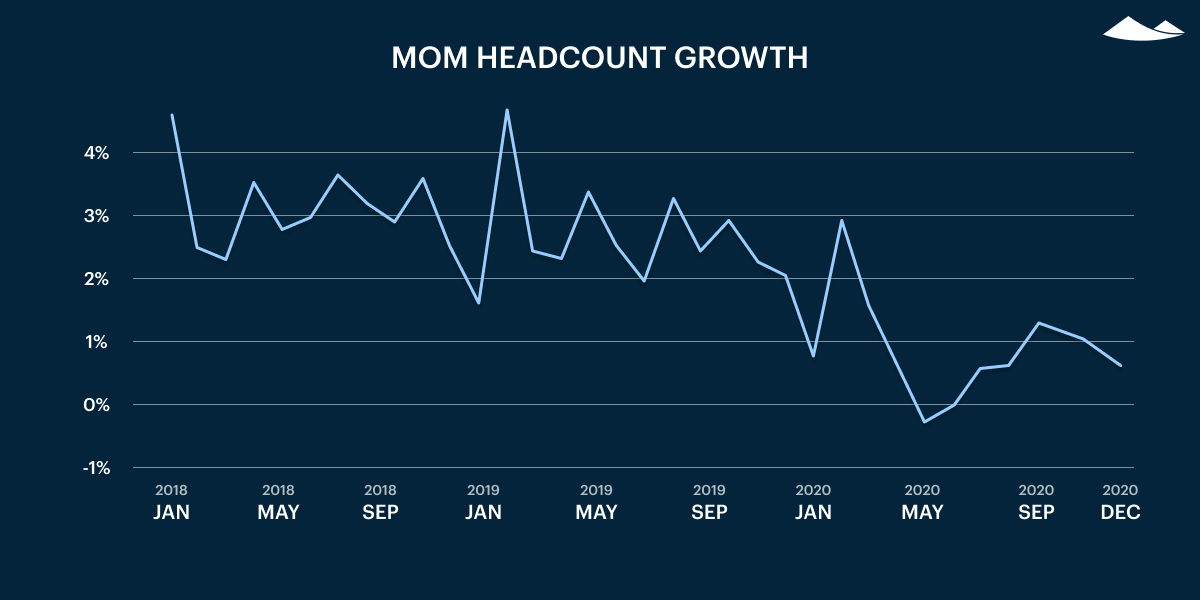

Headcount growth remained low, but began to see signs of growth in Q4 of 2020.

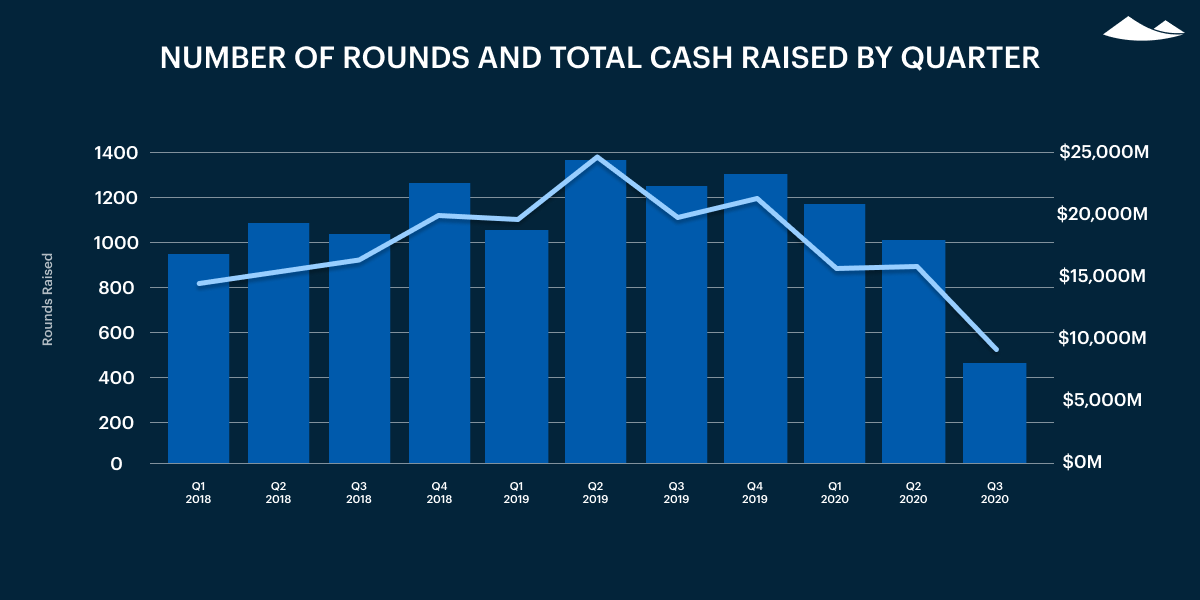

Startups raised a record dollar amount in Q4 of 2020 with the most growth on the rounds larger than $25M.

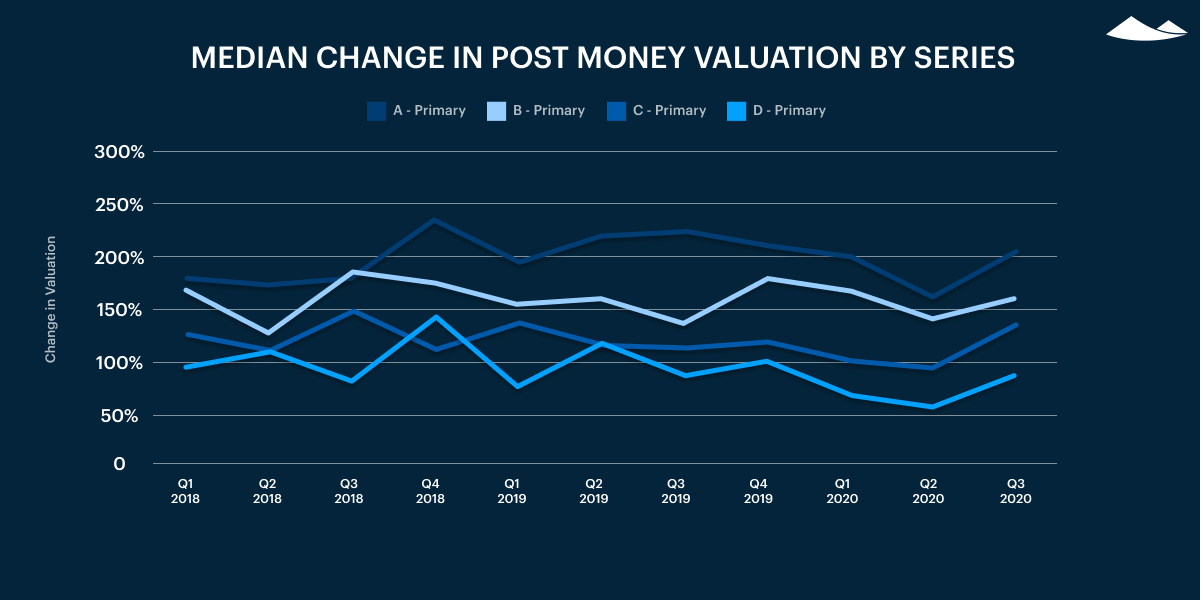

Change in post money valuations nearly reached record levels in nearly all stages. The median change in valuation is the highest Carta has seen in 5 years.

Carta’s Private Markets Quarterly Report examines trends across venture-backed companies and security holders in private companies to promote transparency between employers and employees, prompting fair equity management across private markets. Carta uses its quarterly data, including the aggregated and anonymized data of more than 18,000 companies, representative of over a trillion dollars in post-money valuation and reflecting more than 220,000 investors in the startup ecosystem. More on methodology can be found at the end of the report.

Employee Shareholders in Q4 2020

Headcount growth is still well below pre-COVID levels ending the year at 0.5%. Recovery slowed down in Q4. With fundraising levels at an all time high, we will be watching this number closely in Q1 for signs of recovery.

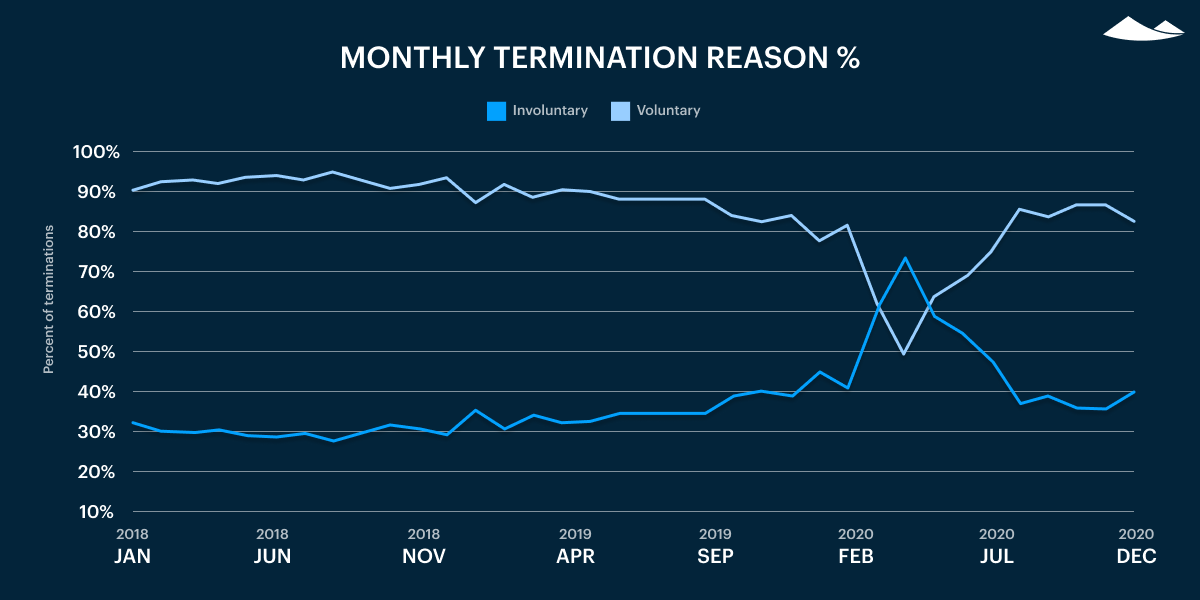

By the end of 2020 the mix of voluntary and involuntary terminations reverted back to what we saw at the end of 2019. In Q4 of 2020 79% of terminations were voluntary and 21% were involuntary.

The percent of post-termination exercise periods more than 95 days spiked in Q2, reaching 25%, then declined significantly through Q4 of 2020. The year ended with only 12.5% of post-termination exercise periods above 95 days, down from 15.8% in Q3. This trend suggests that companies haven’t offered extended PTEP beyond employees who were laid off during COVID.

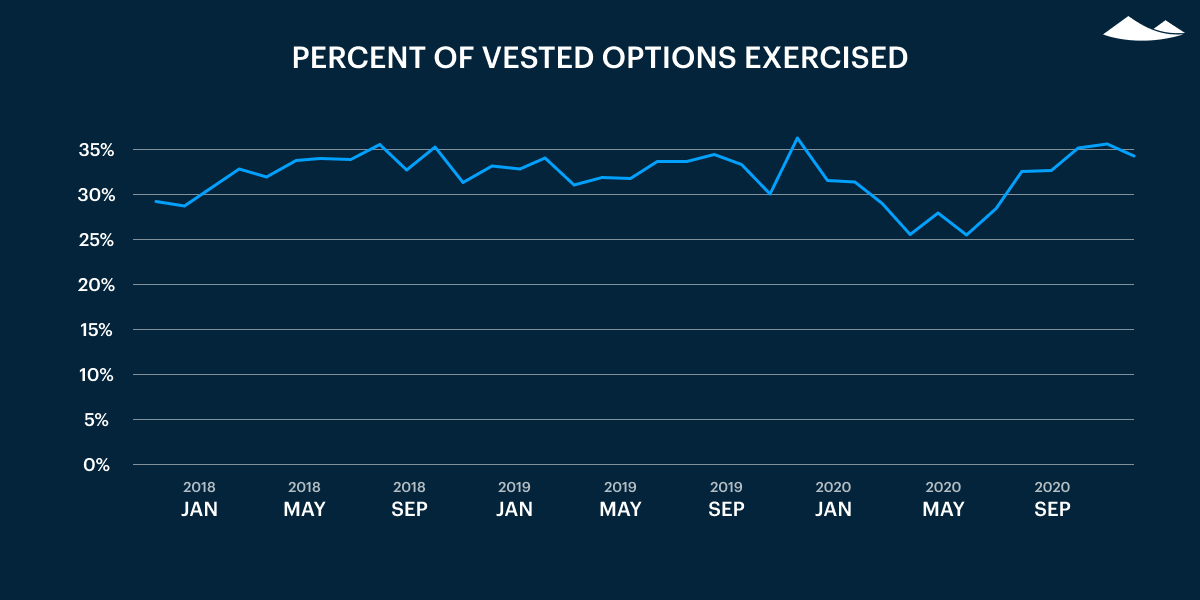

The percent of vested options exercised has completely recovered to pre-COVID levels.

Private Company Equity in Q4 2020

Q4 median cash raised | YoY change | |

Seed | $2.9M | 17% |

Series A | $11.8M | 17% |

Series B | $36.3M | 53% |

Series C | $54.5M | 1% |

In line with global venture capital funding as reported by Pitchbook, Carta saw a record dollar amount raised in Q4 2020.

In Q4 2020, Carta saw the largest growth on the rounds larger than $25M. In Q4 2020, there were X rounds larger than $25M, compared to Y in Q4 2019.

In Q4 2020, change in post money valuations nearly reached record levels in all stages except for Series A rounds.

Q4 Median Change in Post Money Valuation | QoQ change | |

Series A | 198% | -6% |

Series B | 204% | 35% |

Series C | 156% | 25% |

Series D | 138% | 63% |

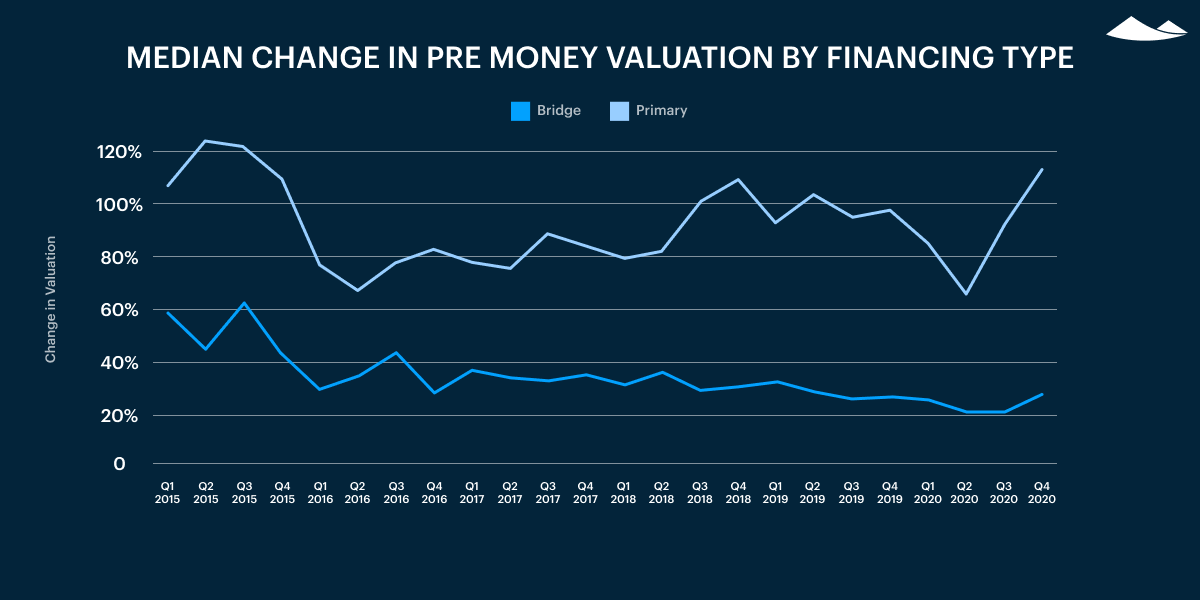

The median change in valuation is the highest Carta has seen in 5 years, with primary rounds seeing an 111% median change in pre money valuation.

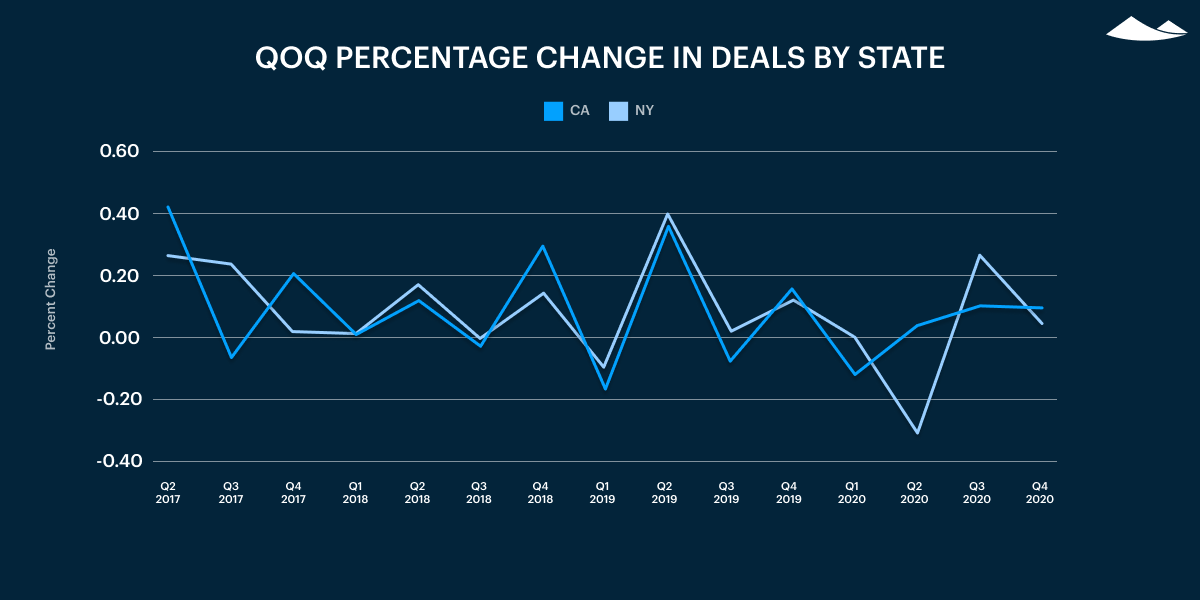

The number of deals in Q4 2020 were down 5% in California and 25% in NY when compared to Q4 2019, indicating startups in California seem to have been less impacted by COVID-19 than New York startups.

Venture Capital Deal Terms in Q4 2020

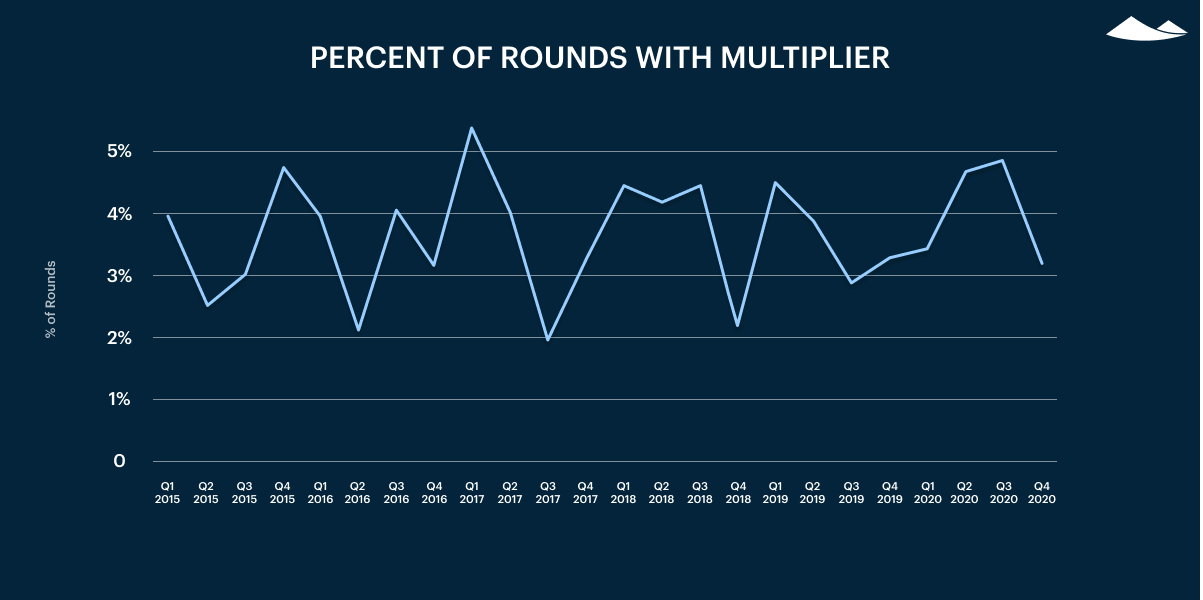

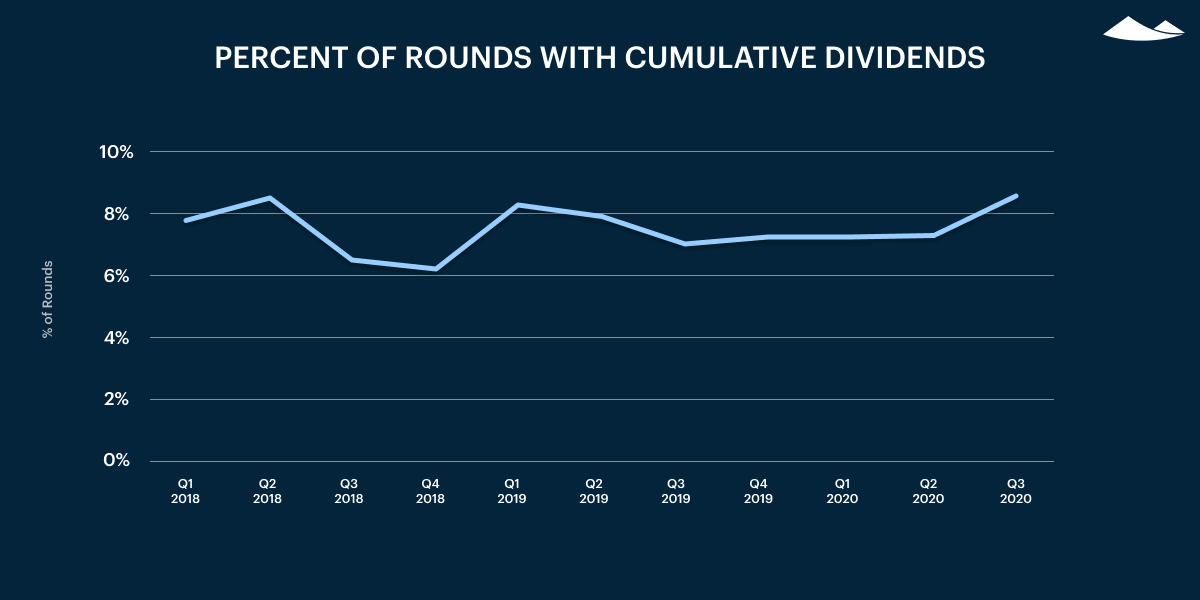

The percent of rounds with nonstandard terms, cumulative dividends or a multiplier, both dropped in Q42020.

Methodology

Overview

Carta helps over 18,000 primarily venture backed companies and 1,000,000 security holders manage equity. This study uses an aggregated and anonymized sample of Carta’s data. Companies who have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

The data presented in this private markets report represents a snapshot as of October 12, 2020. Historical data may change in future studies because there is typically an administrative lag between the time a transaction took place and when it is recorded in Carta. In addition, new companies signing up for Carta’s services will increase historical data available for the report.

Financings

Financings include equity deals raised in USD. The financing “Series” (e.g. Series A) is taken from the legal share class name. Financing rounds that don’t follow this standard are not included in any data shown by Series but are included in data not shown by Series.

Primary rounds are defined as the first equity round within a Series. Bridge rounds are defined as any round raised after the first round in a given Series. If there is no indication that a round is a Primary or Bridge round, both are included.

In some cases, convertible notes are raised and converted into multiple share classes within a Series at various discounted prices (e.g. Series A-1, Series A-2, Series A-3). In these cases, converted securities are not included in Cashed Raised and only the Post Money Valuation of the new money is included.

Terminations

Terminations entered into Carta must include a reason. Involuntary terminations include both terminations for performance and company layoffs. Voluntary terminations are employees that decided to leave of their own accord. Other termination reasons, including For Cause, Death, Disability, and Retirement were not included in the data and make up less than 1% of all terminations combined.

1 This study uses an aggregated and anonymized sample of Carta’s cap table data. Companies who have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta, Inc. (“Carta”). This communication is not to be construed as legal, financial, accounting or tax advice and is for informational purposes only. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein.