Most of the time, the two data points that get the most attention when a company raises new venture funding are round size and valuation. How much capital did you raise? And what did your investors decide your company is worth?

Just as important as these individual numbers, however, is the relationship between the two. Divide the valuation by the round size, and you get the round’s dilution. This metric answers two other key questions: How much of the company did you sell? And how much do you have left?

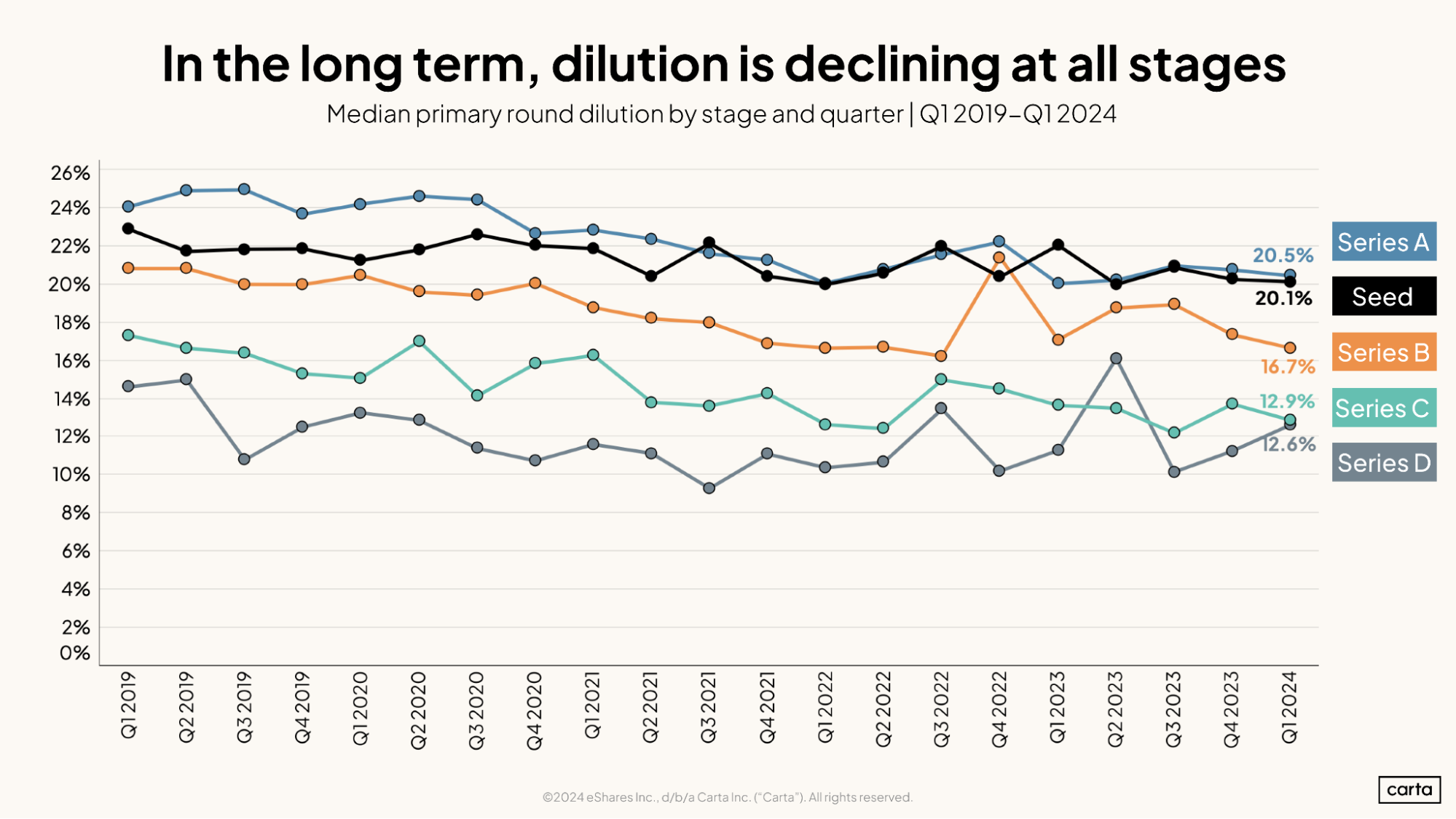

Dilution amounts can vary significantly across different companies, different industries, and different stages of the startup lifecycle. In the aggregate, however, a clear trend has emerged over the past several years: The typical startup is selling a smaller and smaller percentage of their shares when they raise new funding. Between Q1 2019 and Q1 2024, median dilution declined at every stage of the startup lifecycle.

At the seed stage, median dilution is down from 23% to 20.1% over that span. At Series A, it’s down from 24.1% to 20.5%. At Series B, median dilution fell from 20.8% to 16.7%. These are significant changes—and, taken together, they represent a significant shift in the fundraising scene.

A new perspective on dilution

One helpful way to understand the scale of this shift is to consider the compounding effects of dilution.

The degree of dilution in a company’s seed round can influence how its leaders will later think about their Series A, their Series B, and all future funding rounds. If a startup raises a seed round with sky-high dilution, its future fundraising options could be restricted. If a startup’s early rounds have low dilution, it will have more flexibility with its existing shares further down the road.

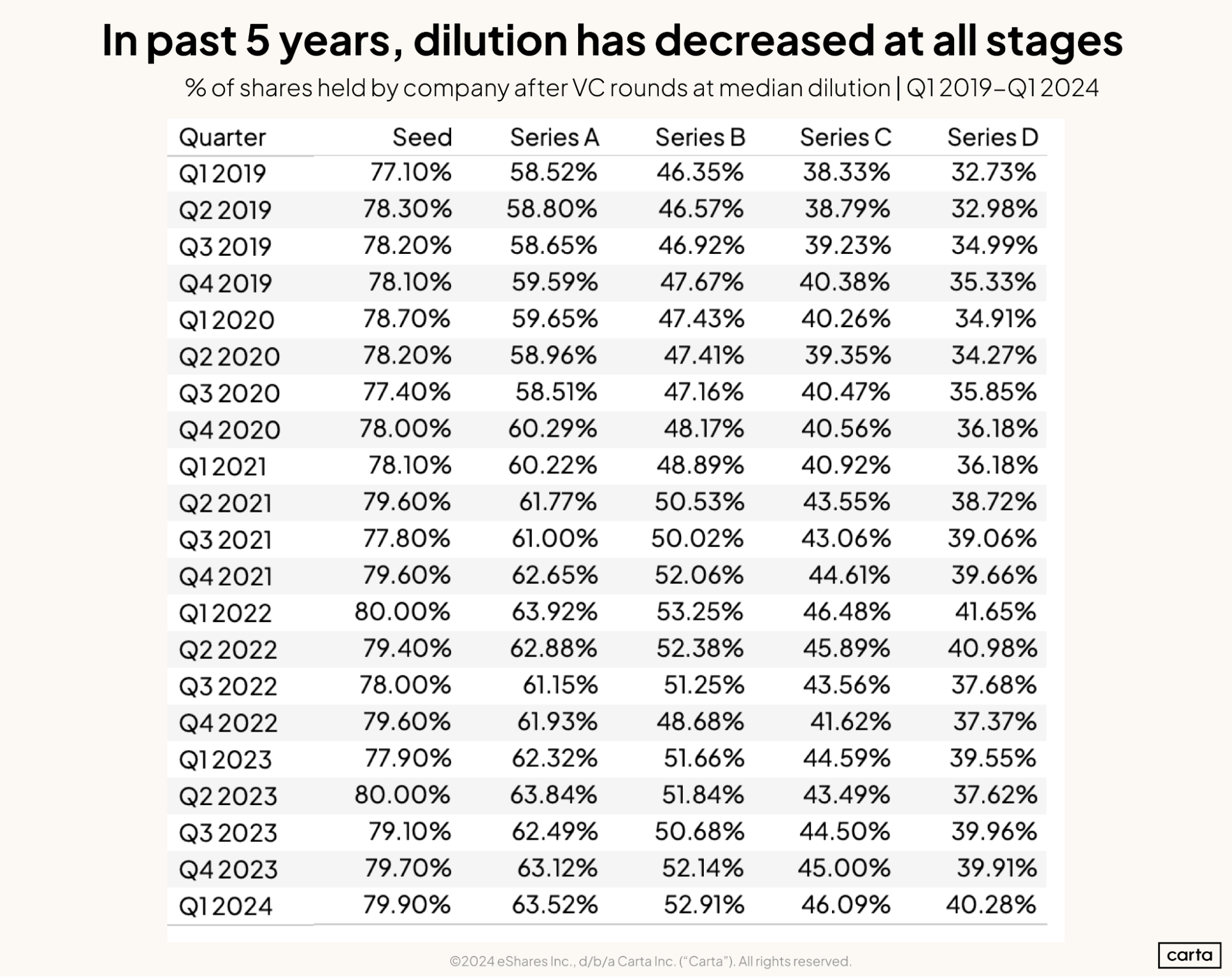

To conceptualize how different dilution environments can impact a company’s cap table—and to get a firmer grasp on how the environment has changed over time—we took the past several years of Carta data and applied it to a hypothetical (and highly simplified) fundraising journey.

Here’s how the exercise works. For each quarter, we imagined a startup that owns 100% of its shares. We then took the median dilution from each stage in that quarter and performed a series of calculations to mimic the company moving from seed through Series D at those specific dilution levels. For each stage, we can see what percentage of its shares a hypothetical company would still own if it were raising rounds in that quarter’s dilution climate.

We can then use the compounding nature of dilution to compare overall dilution climates across time. Since companies generally prefer to retain as many shares as they can, quarters with less dilution can generally be considered a more company-friendly environment.

Here’s a look at the impact that median levels of dilution in primary rounds would have had on a company’s cap table across the past 21 quarters:

Before we get too far, some caveats:

This exercise is not meant to replicate an actual fundraising process. In reality, a startup’s seed round and its Series D would happen many years apart, not in the same quarter.

A new funding round almost always involves issuing new shares, which retroactively reduces the dilutive impact of prior rounds.

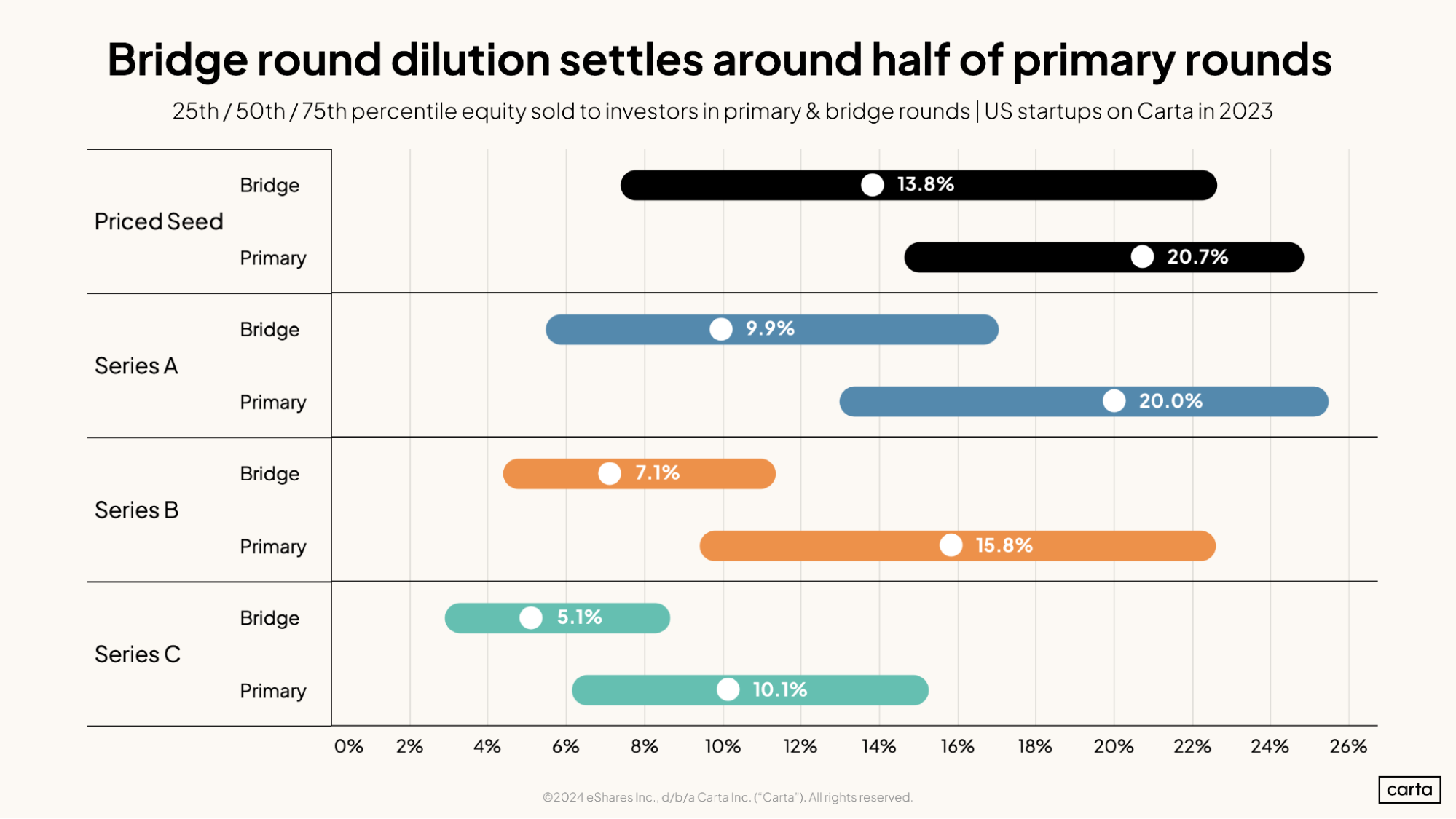

This exercise does not account for bridge rounds, which have grown more popular than ever in recent quarters and usually have additional dilutive impact on a company’s cap table. In 2023, there was typically about half as much dilution in priced bridge rounds on Carta as there was in primary rounds:

To sum it up, calculating dilution for a real startup is typically much more complicated than this exercise might suggest.

What the dilution data tells us

We already knew that dilution was declining in recent years. Now, we can look at that decline in a different context.

In Q1 2024, combined median dilution across stages leaves a hypothetical startup with 40.28% of its shares remaining after its Series D. Five years ago, in Q1 2019, median dilution levels would have left a startup with 32.73% of its shares remaining after a Series D. For the purposes of this exercise, we might say that the overall dilution climate was 7.6 percentage points friendlier to companies in Q1 2024 than it was five years ago.

In terms of company ownership, that’s a major difference. If a startup is valued at $10 million, 7.6% of company ownership is worth $760,000. If a startup is valued at $100 million, a 7.6% share is worth $7.6 million. And if a startup reaches that coveted $1 billion valuation, a 7.6% ownership stake is worth $76 million.

When founders retain a bigger piece of the pie, they have more shares at their disposal to own themselves, issue to employees, or sell to other investors in later fundraising events. And those shares have nearly unlimited upside.

That scenario is perhaps an imperfect comparison—again, these numbers don’t describe the experience of any single startup, because no company raises five rounds of funding in the same quarter. But it may be a useful way to visualize the compounding effects of declining dilution levels across multiple funding rounds.

A persistent downward trend

The venture capital market experienced a lot of ups and downs over the course of the past five years. But through all the tumult, the general trendline for dilution has remained the same.

Whether the venture world has been in the midst of a record-breaking bull market or an abrupt venture slowdown, dilution has been (for the most part) steadily declining across all fundraising stages.

This means the trend is perhaps more difficult than others to explain with a single unified theory. During 2020 and 2021, it would have made sense if dilution were declining because companies had more dealmaking leverage than investors and were able to attract more favorable terms. But that logic is less applicable in 2022 and 2023.

In those more recent years, it would make sense if dilution were declining because so few transactions have taken place, and only the most attractive startups were still able to raise funds—and these premium startups were still able to negotiate for lower levels of dilution. Other startups with fewer suitors and less leverage that would have shifted the data by raising rounds at a high level of dilution weren’t able to raise rounds at all, thus lowering the median of the remaining dataset. But this theory holds up less well in 2020 and 2021.

In all likelihood, the answer lies somewhere in the middle—a synthesis of these and other factors, rather than direct attribution to one cause or the other.

How dilution compares to other deal metrics

Dilution decreased steadily throughout 2019, 2020, and 2021. This aligns with some of the big-picture trends that defined venture activity during those years. As deal counts and valuations skyrocketed, the leverage of negotiations tilted in favor of companies, who were able to negotiate more favorable terms.

However, the downward trajectory in dilution was not as pronounced as it was in other key metrics related to startup fundraising. Venture deal counts and capital raised, for instance, experienced a much steeper rise in 2021.

In 2022, as the broader venture market entered a slowdown, dilution also suffered a dip. In our exercise, the median remaining dilution after a Series D was 37.4% in Q4 of that year, down from a recent high of 41.6% in Q1 2022. As the leverage of the venture market tilted in the direction of investors, some of them were able to start acquiring larger portions of companies.

Again, however, the investor-friendly tilt in terms of dilution was not nearly as pronounced as in other metrics of the venture market. Total cash raised, for instance, declined by 55% between Q1 and Q4 2022, compared to a 10% relative decline in combined dilution.

And since then, dilution is trending back up, even while many other areas of the venture landscape remain stuck in a slowdown.

The venture fundraising market of the past few years has been defined by multiple powerful shifts in momentum. These shifts have clearly affected how startups and VCs think about dilution. But compared to other areas of VC, the impacts on dilution have been less severe.

Get the latest data

For the latest data on venture capital fundraising, startup hiring, compensation benchmarks, and more, sign up the Carta Data Minute:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2024 eShares, Inc. dba Carta, Inc. ("Carta"). All rights reserved. Reproduction prohibited.