From the perspective of private equity firms and their limited partners (LP), an ideal PE investment is one that produces a substantial return in a short period of time. The larger the return, and the quicker that return comes, the better the outcome for investors.

In recent years, however, the trendlines for both of these figures have moved in the wrong direction. Compared to four years ago, PE investors today are waiting longer for exits. And when those exits arrive, the returns are less likely to be lucrative.

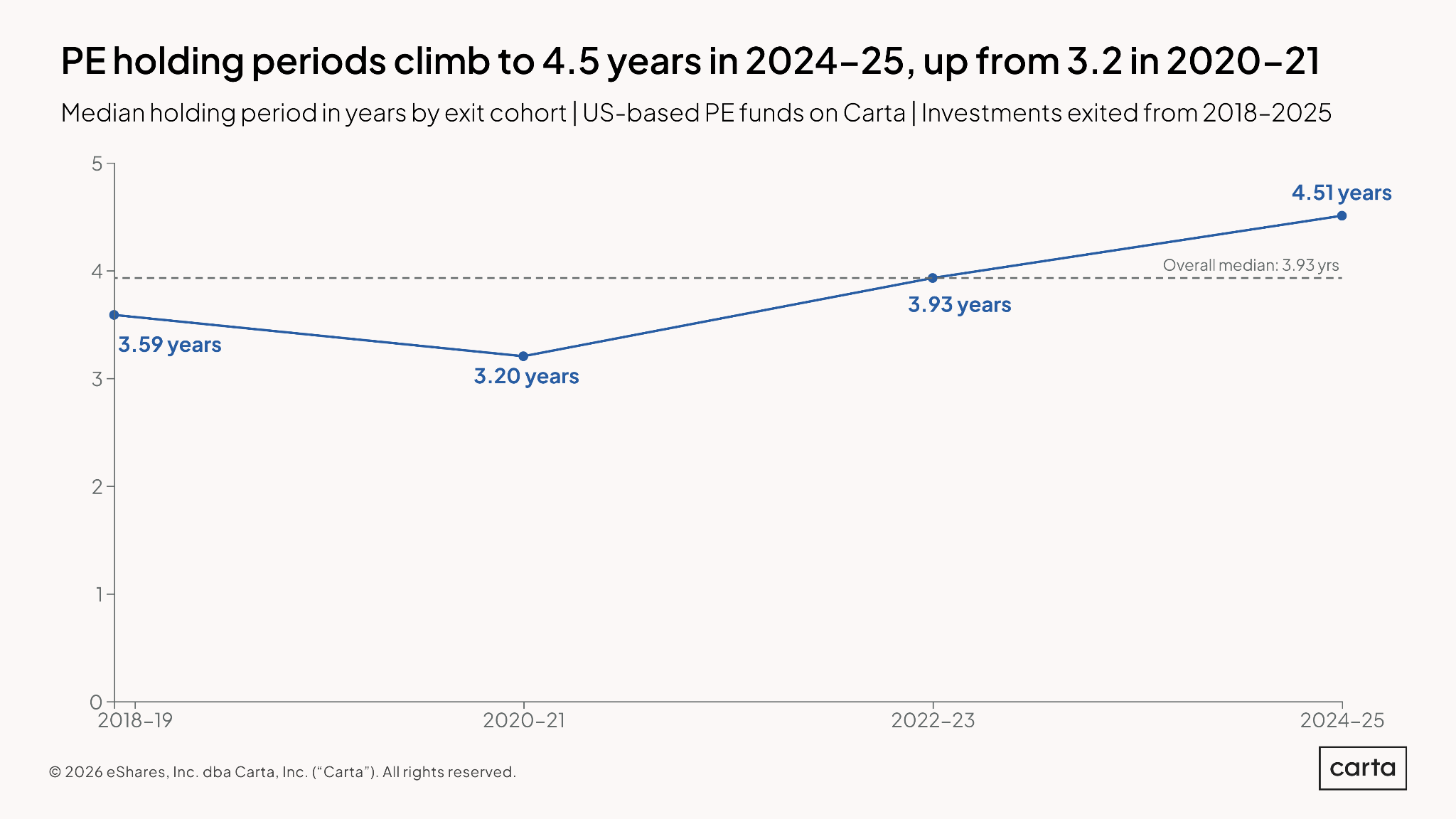

Among private equity funds on Carta, most of which are concentrated in the lower middle market, the typical holding period of portfolio companies at the time of exit rose by more than 40% during the first half of the 2020s. For exits that occurred in 2020 and 2021, median hold time was 3.2 years. For exits in 2024 and 2025, that period ballooned to 4.51 years.

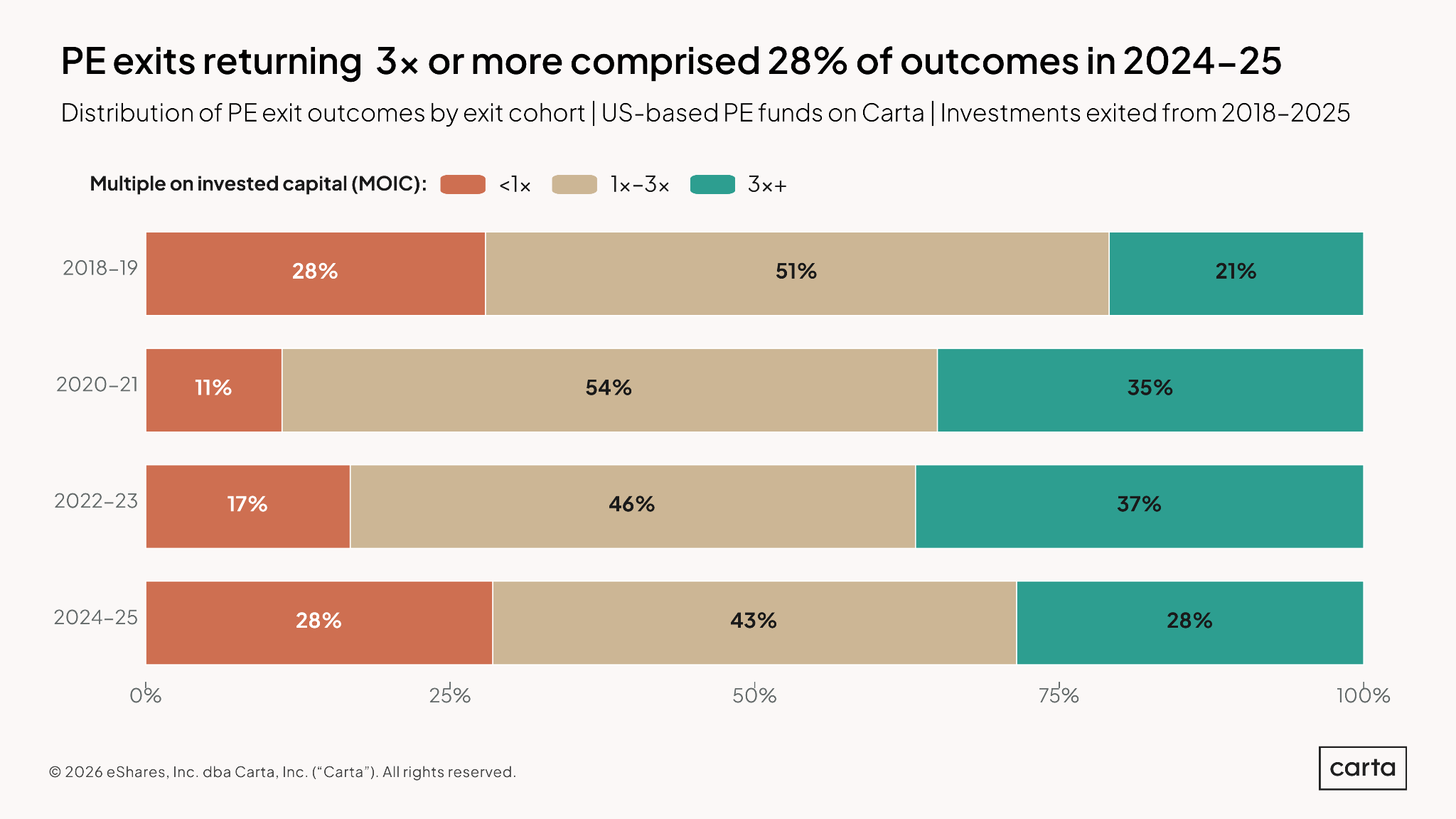

At the same time, the likelihood of achieving a standout return on a portfolio company exit declined, and exits that resulted in an underwater return grew more common. About 35% of exits across 2020 and 2021 resulted in a return greater than 3x, while 11% had a return below 1x. For PE-backed exits in 2024 and 2025, these two figures were equal: 28% of exits led to a 3x return, and another 28% resulted in a return below 1x.

In terms of return multiples, the PE exit environment of the past two years looked quite similar to that of 2018 and 2019, the final years before the onset of COVID began to transform the economy.

Why PE’s exit math is changing

If you’re familiar with the story of the private markets during the 2020s, the causes for these shifts in the PE exit environment likely won’t come as a shock. During 2020 and 2021, financial markets of all kinds were in a rare state of froth, with more deals occurring than ever before and valuations soaring to record-breaking heights. In this era, it was perhaps easier than ever for PE firms to find attractive exits.

“People were spending in a way they’ve never spent before,” says Melonie Boone, CEO at Boone Management Group, a strategic consulting firm that provides various services and solutions to help PE-backed companies prepare for exit. “Companies were making money in a way they’ve never made money before. You could sell a company that was nowhere near worth what you sold it for, but people were clamoring for it.”

Then, the market experienced a clear transition. Interest rates began to rise. Investors began to reconsider the math behind all those lofty valuations. Suddenly, deal activity of all kinds started to slacken. IPOs, one of the primary exit pathways for PE portfolio companies, became a relative rarity. In many ways, PE investors have spent the past four years trying to recalibrate their plans for this new environment.

For some firms, this return back to earth after the heady days of the COVID-era boom has been a difficult transition.

“You built the playbook off those times, but those times were superficial,” Boone says. “That wasn’t the real state. And now we’re coming back to the real state.”

This new reality has had a direct impact on hold times, according to Matthew Bennett, a partner at Invidia Capital Management, a middle-market PE firm that pursues buyouts in the healthcare sector. The sorts of exits that firms may have been counting on when they invested in many of their current portfolio companies simply aren’t possible anymore. As previous assumptions have been upended and portfolio plans have been disrupted, investors are looking for new ways to drive growth and increase value at their portfolio companies. Many are now holding onto assets for longer than they once anticipated.

“If you were in a space impacted by the COVID disruption, you might have had a couple sideways years, so you’ve got to get on a growth path to exit,” Bennett says. “As a result, you just have to hold that asset longer to work out of that.”

And the stakes are high. If PE funds don’t find a way to achieve results that please their LPs, they could find themselves facing an existential threat.

“Those funds that don’t have a lot of assets that have been returned, they’re under a lot of pressure to return,” Bennett says. “If I’m a limited partner, why should I give you more money if you haven’t returned my old money at a multiple?”

How PE firms and portfolio companies are responding

Of course, PE firms aren’t simply sitting around and waiting for another bull market to arrive. Investors are pursuing a number of strategies to drive growth, improve efficiency, and help spur their portfolio companies toward the exits they ultimately desire.

According to Bennett, many of these strategies originate with the operating partners within a PE firm, who are tasked with finding and implementing operational improvements across the portfolio. These are typically experienced executives with firsthand experience in helping companies achieve the sorts of outcomes their sponsors are seeking.

“The operating partner or the operating executive that lives within a private equity firm and goes and helps companies perform has really been a growth area,” Bennett says. “You see those groups working across financial issues, building the commercial success of companies, making companies better from a cybersecurity perspective.”

At some PE firms—particularly larger firms—operating partners might implement a long list of changes, targeting anything and everything that could be streamlined or improved. At Invidia, Bennett says his team usually focuses on a shorter list of targets—perhaps three specific things that, if successfully implemented, could drive a substantial financial response. These might include shifts in areas like pricing, growth, procurement, or human resources.

“We’re trying to be very intentional about picking what really matters,” Bennett says. “We think that has the benefit of really driving performance, driving focus, and it frankly lowers the anxiety [for company leaders].”

The human element of PE’s hunt for exits

In Boone’s consulting work, this anxiety that missed timelines and operational changes can create at portfolio companies is a primary point of focus. When a company fails to meet the expectations of its sponsors, it can be a highly stressful, pressure-packed time. In her view, it’s critical for PE firms to keep this human element in mind.

“All this external stuff is creating pressure that executives have not dealt with before,” Boone says. “Private equity professionals, the sponsors, they’re great people. But they haven’t been in that pressure cooker for a very long time, or they haven’t experienced it the way it is today. They have these expectations, but it’s very hard right now to carry those expectations through.”

In her experience, achieving significant financial improvements at a portfolio company isn’t just about abandoning a wrongheaded strategy or implementing new software. Sometimes, the best way to drive performance is to focus on factors like interpersonal dynamics, internal systems and processes, and behavioral psychology—less quantifiable variables that, in a financially driven industry like PE, can easily be overlooked.

This can include examining the strengths and weaknesses of certain individuals and how those personal traits align with their responsibilities. It can include reassessing workflows for points of systemic friction. It can include taking steps to ensure employees feel empowered to speak up to managers when they disagree with a decision or when they see a problem that high-level executives might miss.

Boone believes it’s a mistake to view portfolio companies as simply numbers on a spreadsheet. In seeking to drive toward the exit outcomes they desire, she thinks it’s critical for PE firms to remember the people behind those numbers, and how those people will be the ultimate drivers of the exits that sponsors and their LPs crave.

“What they need to look at is: What is additive to our playbook that we don’t have today? What is going to move the needle in the direction that we want?” Boone says. “And I see that behavioral element as the [place where] you’re going to see private equity and portcos really excel and move past some of the others who are going to do the same old thing.”

Subscribe to the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.