Halfway through 2026, the market for investing in AI is as frenzied as it’s ever been.

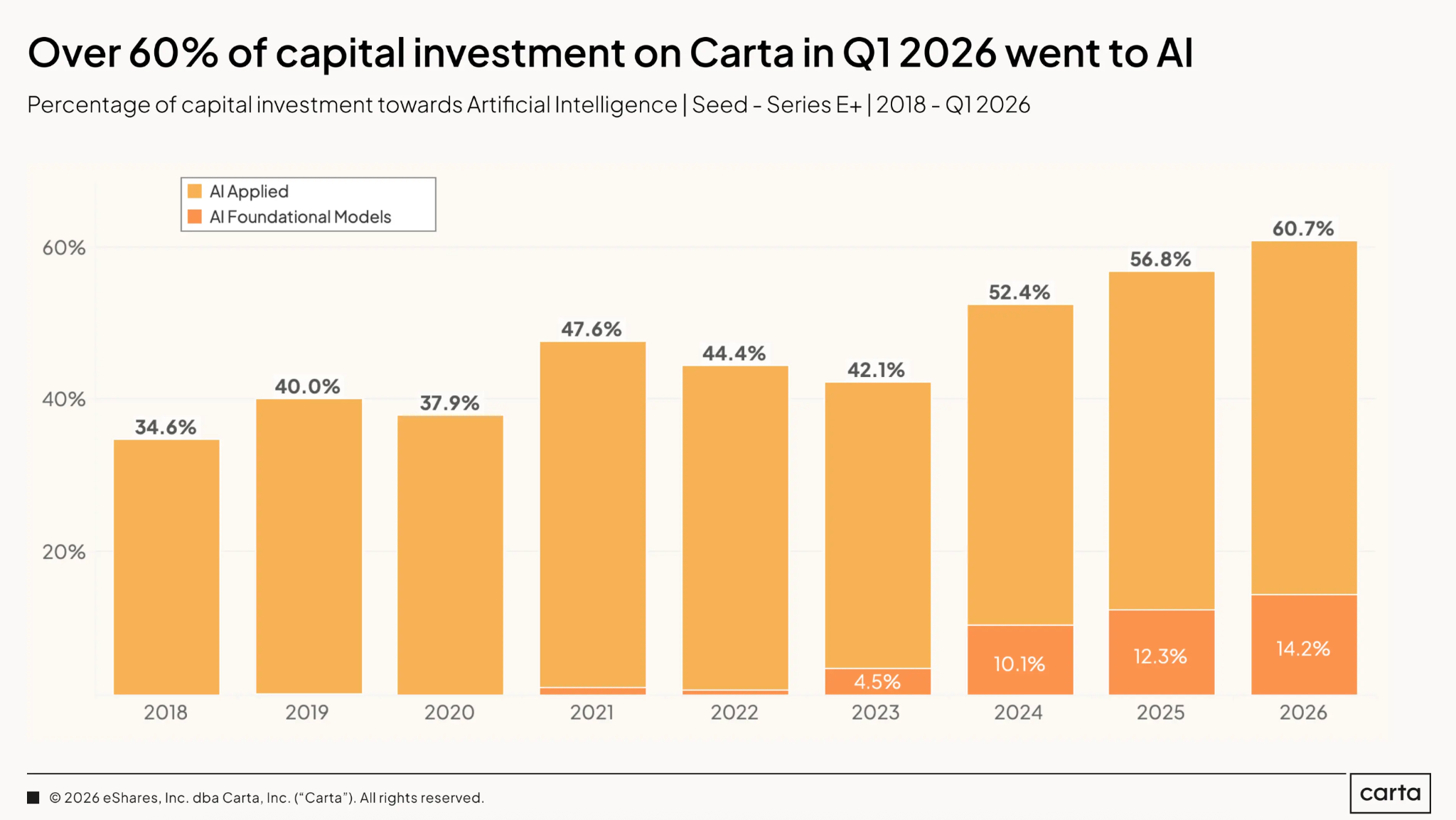

The world’s largest companies are spending hundreds of billions a year on building out AI infrastructure. Optimism around SpaceX’s AI capabilities helped drive the company to a $1.77 trillion IPO, and rivals OpenAI and Anthropic are planning mega-listings of their own. In June, AI coding startup Cursor lined up a $60 billion sale, one of the largest exits in venture capital history. So far this year, more than 60% of all VC funding raised on Carta went to AI startups, according to Carta’s latest State of Private Markets report.

“Public markets are rewarding AI-supported growth, and private markets are all about AI and AI-accelerated growth,” says Bobby Ocampo, co-founder and managing director at Blueprint Equity, a growth equity firm that invests in tech companies. “That seems to be what everyone is excited about.”

In the world of private equity, however, the response to the rise of AI has looked a little different. Major buyout shops are not pouring billions into AI acquisitions. They’re not chasing down deals with developers of bleeding-edge models. In most cases, PE investors are taking a more cautious, patient, and specialized approach to investing in the world’s latest wave of technological upheaval.

“In VC, the industries they’re investing in are slightly different,” says Raymond Gong, a former PE investor who’s now a senior partner at Profitability Partners, which provides various financial services to PE-backed companies in the home services space. “The VC guys, the growth guys, they’re looking at the technology itself and how they can invest in the technology. Whereas the PE guys are looking at how they can apply this technology to a certain industry to make things more efficient, or to grow, or to become more profitable.”

This contrasting approach to investing in AI highlights some of the most significant differences between the VC and PE models. For the most part, VC is about speculative upside. Investors acquire minority stakes in a wide range of relatively young companies, hoping that a small handful of those startups will eventually become industry leaders and produce outsized returns. The goal is to get in early and swing for the fences. It’s an ideal strategy for investing in assets that still have a huge range of potential outcomes.

The PE model, meanwhile, is about steadiness and certainty. PE investors typically acquire majority stakes in companies with stable, predictable finances, using operational improvements and financial leverage to spur growth and drive value. Instead of the big swings seen in VC, the goal is to produce a steady stream of singles and doubles.

Startups are not the typical PE target. And just about every pure-play AI company currently in existence is still, at least on some level, a startup.

“An AI company doesn’t make a great PE buyout target, because you’re usually financing the acquisition with debt,” Gong says. “You’re looking for stable, old-world business, cash-flow generative. A lot of the AI companies, they’re not profitable, right? So they don’t make good acquisition targets for PE.”

How AI is reshaping PE-backed businesses

To be sure, PE investors aren’t sitting on the sidelines and simply watching along as AI transforms the global economy. They’re trying to capitalize on the AI boom—just in a different way.

From Gong’s perspective, this comes down to finding real-world opportunities to deploy AI at legacy businesses to improve efficiency and drive value while minimizing the risk of company-wide upheaval. At least for now, in PE, he sees less of a revolution, and more of a reimagining.

“What’s a way you can implement AI into a company and do it reliably?” Gong says. “What are the opportunities that are actually practical, instead of using it like a buzzword? What are the things that are actually going to save us money and add value to the organization?”

As an example, consider the home services companies with which Gong and Profitability Partners typically work—think HVAC, plumbing, electrical, and roofing. These industries are traditionally in the PE sweet spot. They’re also well-protected from some types of AI disruption: ChatGPT isn’t going to fix the leak under your kitchen sink anytime soon. But these businesses are still finding ways to implement AI tools in incremental ways.

The customer-facing side of a business is one clear use case, Gong says, with companies using AI to aid with things like booking appointments, managing schedules, dispatching workers, and keeping records. A common mantra in the home-services space is “speed to lead”—how quickly can a company convert a prospect into a customer? In some cases, AI is already accelerating that timeline.

Many of the companies Gong works with are already PE-backed, and almost all of them hope to eventually sell to a PE buyer. The hope is that leaning into AI tooling will make them more appealing to potential acquirers and increase the eventual financial return.

For now, though, that’s still a hope. It remains to be seen exactly what sort of financial impact these sorts of AI upgrades will eventually have on a PE portfolio.

“We haven’t seen yet the ultimate true ROI across a portfolio,” Ocampo says. “I think the potential is incredible, but I would be lying if I told you that, you know, this piece of technology took this business from 1x to 5x in a year. It’s slower than the pace of adoption.”

PE ponders the price of AI

It also remains to be seen exactly what sort of price PE firms will pay for AI companies—either legacy businesses embracing AI, or AI-native companies with business models that may appeal to PE funds.

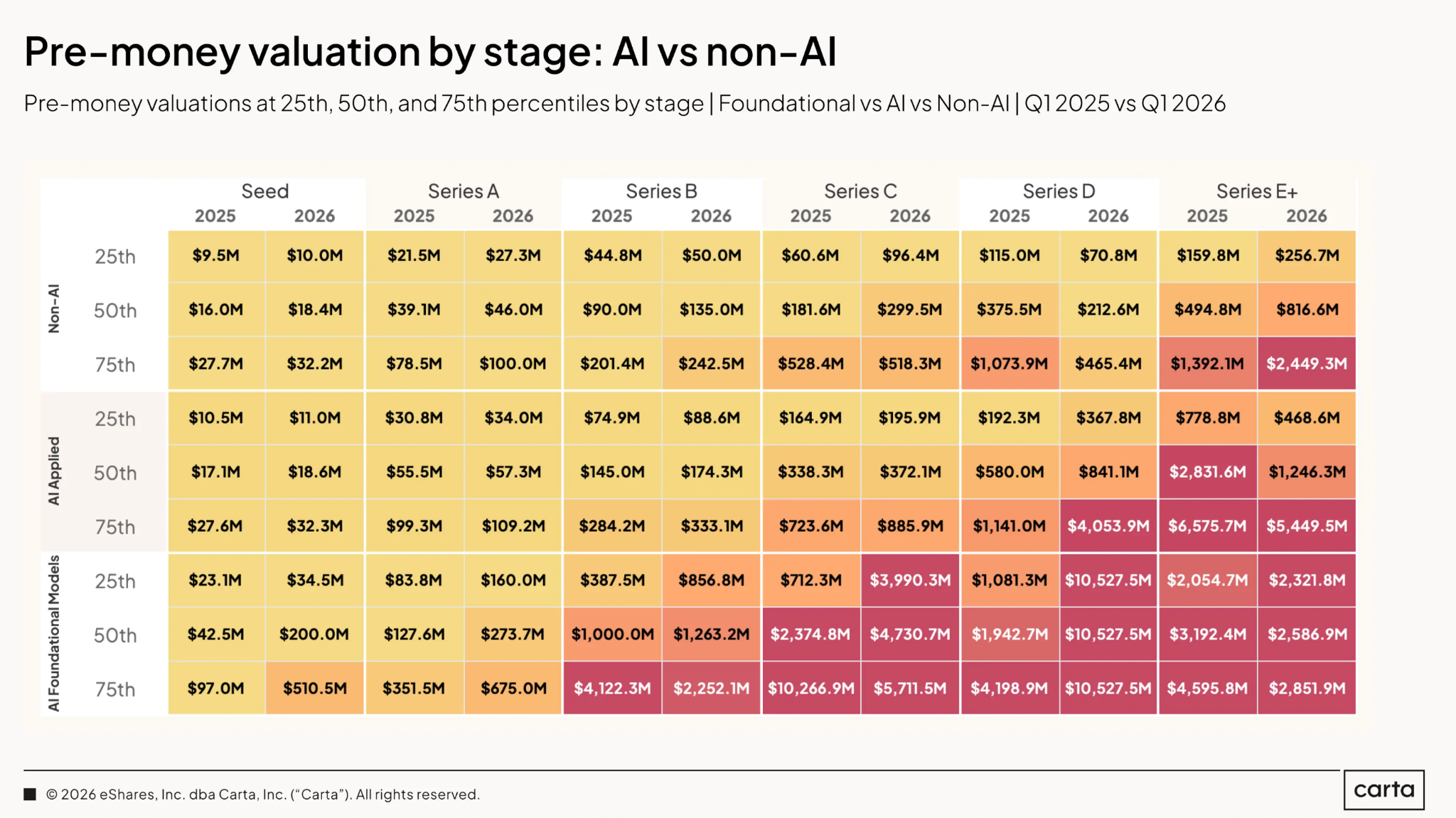

In VC, company valuations have soared in recent quarters. Investors have been grappling with how to value a new generation of companies with new kinds of economic profiles. For the most part, they’ve been willing to pay huge premiums for AI companies, spurred by the desire to ensure they don’t miss out on the next big thing.

For PE firms, the conundrum is slightly different. Instead of pricing a totally new crop of companies, they’re faced with figuring out how to price the same crop of companies in a different way.

“If you’re a middle-market buyout firm—or even us, as an early growth firm—you’re trying to figure out the bearings of how you should play it,” Ocampo says. “If you’re a mid-market buyout firm and you’re looking at an asset that has great AI-related growth, it’s being priced at a multiple that is well above and beyond what you’re used to. You’re used to paying x—are you going to pay 5x? You’re playing in a different pool now, a different game.”

So far, in Gong’s experience, PE investors have remained cautious. Prices haven’t skyrocketed, and companies implementing AI haven’t sparked all-out bidding wars. PE investors certainly acknowledge the potential benefits that AI might confer to portfolio companies. Compared to VC investors, however, they’re much less concerned about missing out on a once-in-a-generation opportunity.

“[AI is] a potential upside to the deal,” Gong says. “But I don’t think people are making decisions to invest purely on the capabilities of AI technology.”

Not yet, at least. Gong and Ocampo agree that PE firms are still extremely early in the process of determining the right way to approach investing in AI. The technology is changing rapidly; the degree of impact it has on companies in PE portfolios could change rapidly, too. As the years pass and the market evolves, some of the early-stage AI startups currently sparking VC bidding wars will eventually mature into the sort of stable, profitable businesses that PE firms tend to buy. For now, the consensus mood is one of cautious optimism. But who knows what the future will hold?

“I think I need another year to be able to feel like I really know where the puck is headed,” Ocampo says.

Subscribe to the Data Minute newsletter

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.