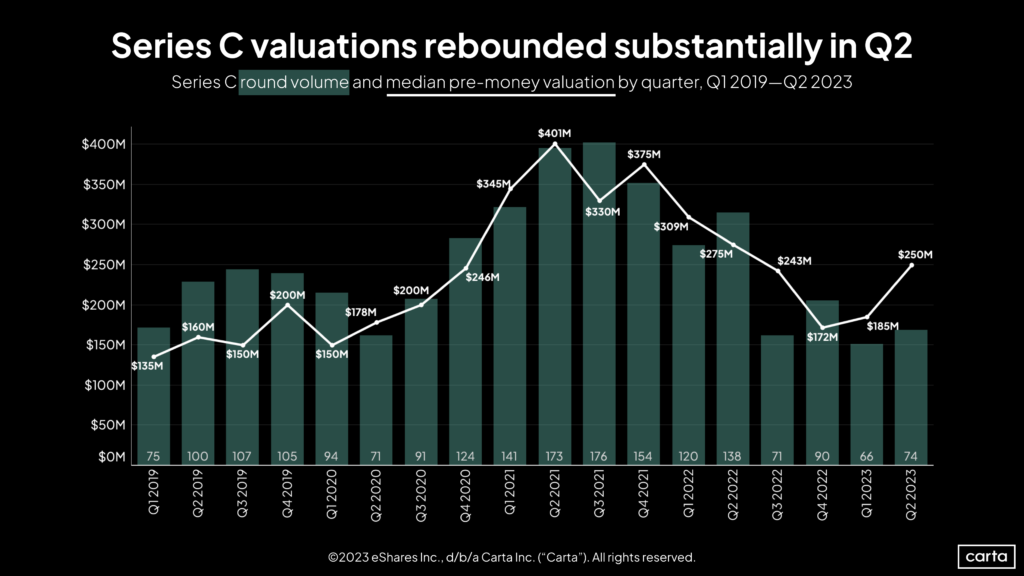

The median Series C valuation on Carta climbed for the second straight quarter in Q2 2023—and this climb was a steep one.

The median pre-money valuation reached $250 million for Series C startups in Q2, a 35% uptick from the Q1 median of $185 million. That’s the largest quarterly increase at Series C since Q1 2021, and it marks the highest quarterly median in the past year.

A second straight quarterly increase at Series C is an encouraging sign for companies that are eagerly waiting for the fundraising market to recover from the venture downturn that defined 2022. Last year, the median Series C valuation declined in all four quarters.

Median valuations also trended up at other phases of the startup lifecycle in Q2. The 35% increase at Series C was the second-largest leap of any stage, trailing Series E+, which rose by 48%.

The median Series C valuation was down slightly on an annual basis, falling 9% from Q2 2022’s median valuation of $275 million. However, in the context of the last several quarters, that modest year-over-year drop might be taken as a positive sign. In Q1, for instance, the median Series C was down 40% year over year. This is actually the smallest year-over-year decline for Series C valuations since Q4 2021, when the startup market was still riding high amidst a record-setting year for VC activity.

The juxtaposition of these two statistics—median valuations at Series C are still down 9% year over year despite a 35% increase last quarter—is an example of just how steeply valuations fell during the back half of 2022 and the early months of 2023. Even the serious gains of Q2 weren’t enough to offset the previous declines.

That trend holds true almost across the board. On a year-over-year basis, median valuations have declined at every stage of the startup lifecycle. Yet on a quarter-over-quarter basis, valuations trended up in Q2 at every stage except for Series D.

For the first time in a year and a half, valuations are moving in the right direction for founders.

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.