The median seed valuation on Carta is at an all-time high. And the median Series A valuation isn’t far off.

In most respects, startup fundraising has cooled off from the sizzling days of 2021 and early 2022. But when it comes to early-stage valuations, the market is hotter than ever.

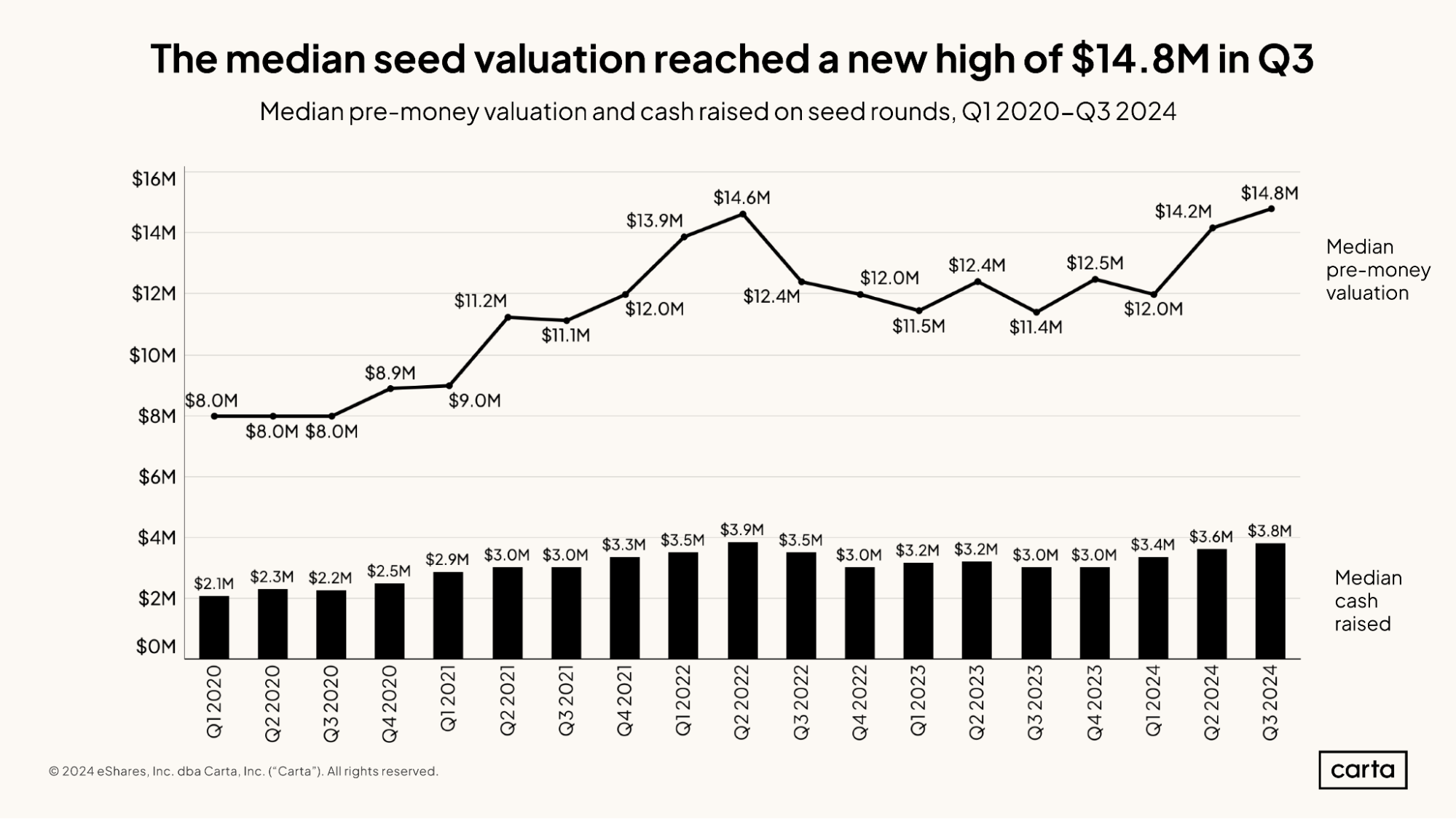

As shown above, the median seed valuation climbed to $14.8 million in Q3, surpassing the $14.6 million figure from Q2 2022 as the highest on record.

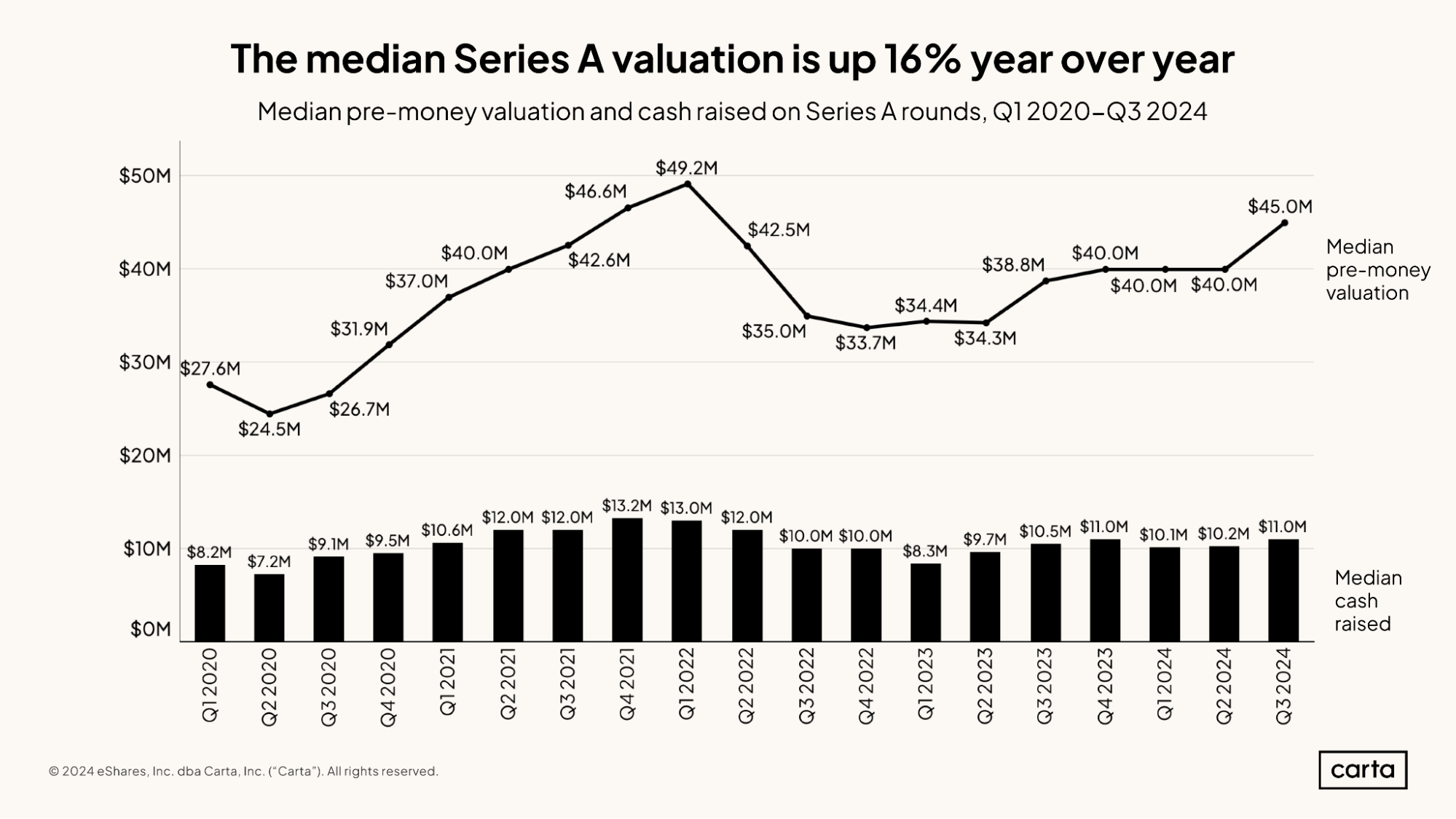

And as shown below, the median Series A valuation rose to $45 million in Q3. That’s the highest it has been since Q1 2022, when it reached $49.2 million.

The typical round size is also rising at both of these stages. The median seed deal was $3.8 million last quarter, and the median Series A reached $11 million. Each of those figures is as high as it’s been in at least two years.

Over the past several quarters, many investors had practiced patience, willing to wait out the market until more certainty arrived on pricing and other key venture variables. For some, that wait is over.

“As a founder, I see investors being much more proactive in the past three to six months,” says Adam Nash, a veteran tech executive and angel investor who’s now the founder at Daffy, a fintech startup focused on charitable giving. “The outreach has started again. Instead of it being founders trying to network to get the investors, I’m starting to see investors reach out to founders that they’re excited about. And that’s a great sign for the market.”

A divergence in deal counts

An increase in enthusiasm among investors may be driving early-stage valuations higher, particularly in the case of buzzy sectors like AI. But at this point, at least, it’s not leading to a concurrent increase in deals.

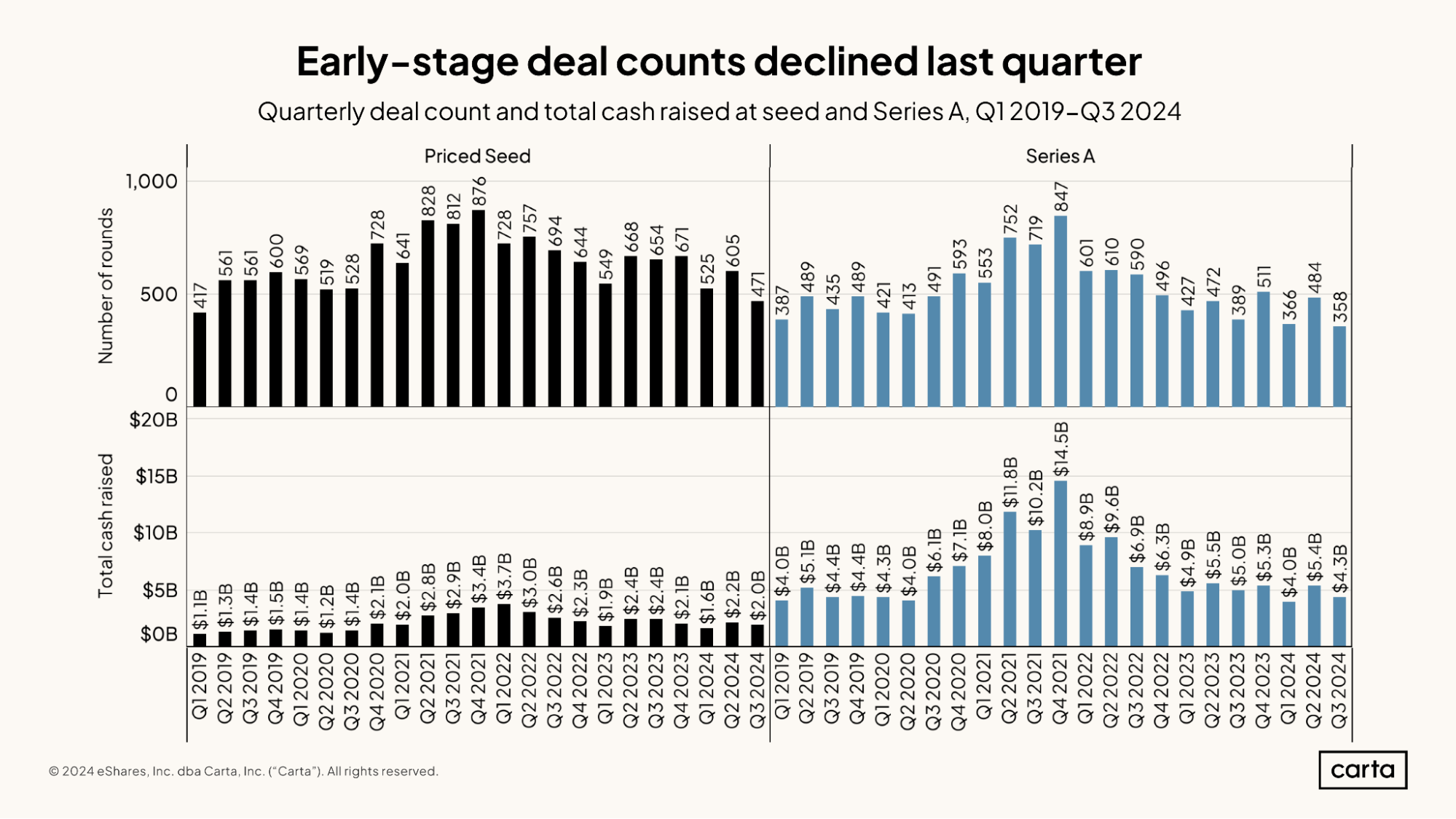

At the moment, startups have logged 471 new seed investments from Q3 on Carta and 358 new deals at Series A. Both of these figures will continue to increase in the weeks to come as more transactions are reported. For now, though, they represent a downward trend. Seed deal count is down 22% quarter over quarter and 28% year over year, while Series A count is down 26% quarter over quarter and 8% year over year.

At both stages, it had appeared in previous quarters that deal numbers were beginning to recover from the recent slowdown. In particular, Q2 showed promising signs. But activity at both stages continues to display some quarter-to-quarter volatility.

In his work as both an investor and founder, Nash says there’s been no shortage of deals to consider, however. That’s true at the earliest stages of venture life, and increasingly at later stages, too.

"I’m seeing quite a few rounds happen at the seed stage and pre-seed, but that started earlier this year, even at the end of 2023,” Nash says. “What has been interesting to me in the past three to six months is the strength that was starting to form at seed seems to be extending now into the As and the Bs and even some Cs.”

The past few months have indeed seen a rise in later-stage activity on Carta. Year over year, deal counts are up 23% at Series B, flat at Series C, and up 72% at Series D.

The macro picture

Many factors contributed to the overall slowdown in venture valuations and deal counts that began in 2022 and continued throughout 2023. A primary one is the rise in interest rates.

Rates were at or near zero through much of the 2010s and early 2020s. In that sort of environment, LPs are less likely to park their capital in low-yielding bonds or other fixed-income assets and more likely to invest in venture capital, which holds the potential of higher returns. Once the Federal Reserve began to increase rates, in 2022, bonds and similar asset classes began to offer better returns, and VC lost some of its appeal.

But the Fed cut rates by half a percentage point in September, then by another quarter point in November. While the macroeconomic future is of course impossible to predict, these cuts would seem to bode well for the broader VC landscape.

“The rate cut is a very good sign for our market,” says Jared Brenner, a senior counsel at Stubbs Alderton & Markiles who works with tech startups across a range of sectors. “I’m hopeful that rates will continue to come down in a cautious way, a disciplined way that’s not too aggressive.”

Emphasis on cautious and disciplined. In some ways, many VCs and founders believe that the recent comedown in the venture market was a good thing—a reminder that building successful companies is hard, and that steady growth and immediate success are not guaranteed.

The fact that early-stage valuations are again on the rise is a sign of the market’s strength. But Brenner doesn’t have to look too far into the past to see a time when an unbridled boom led to negative outcomes.

“We don’t want to create a bubble-type environment or some kind of feeding frenzy where valuations are ridiculous,” Brenner says. “Because that sets up a lot of companies to fail.”