The U.S. is actively watching for signs of recovery from the recession that began in Q2 2020, which was prompted by the onset of a global pandemic. No sector has been immune to the repercussions, and within private markets, venture capital in particular appeared to absorb the shock of the economic slowdown. Our Q2 report revealed that, following the shutdown in March, involuntary terminations exceeded voluntary terminations, casting a shadow on the health of the startup landscape.

To explore the long-term impact of this pause in deal flow and financing, Carta is continuing to examine its quarterly data1, including the cap tables of more than 16,000 companies, representative of over a trillion dollars in post-money valuation and reflecting more than 220,000 investors in the startup ecosystem.

In Q3, we saw the seeds of recovery in venture capital—but not an immediate acceleration back to where things were at the start of the year:

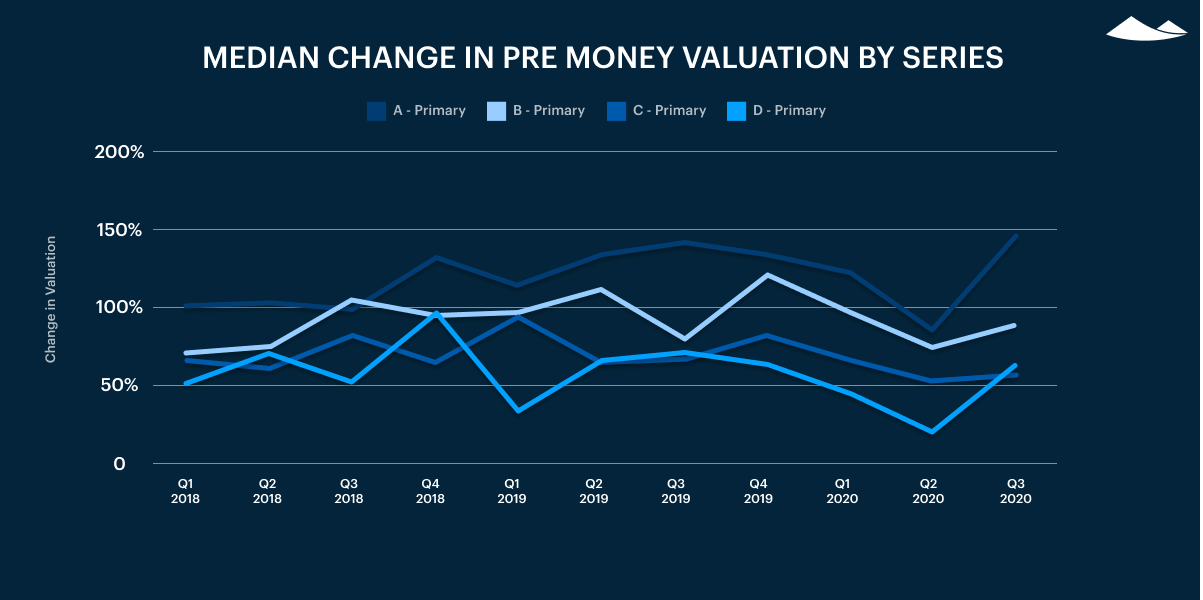

The median valuation increase during primary rounds made a strong recovery from a COVID slump in Q2;

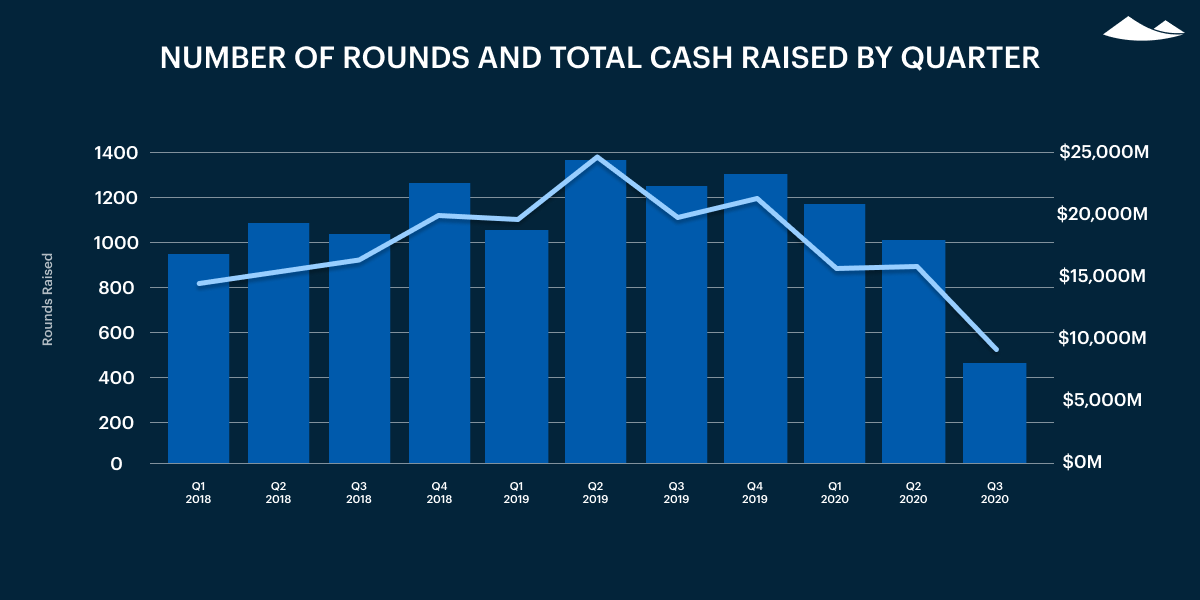

After considering reporting lag, early indications show deal volume still has not recovered since the onset of COVID. However, high valuations and founder-friendly terms indicate VCs are still willing to invest in strong companies;

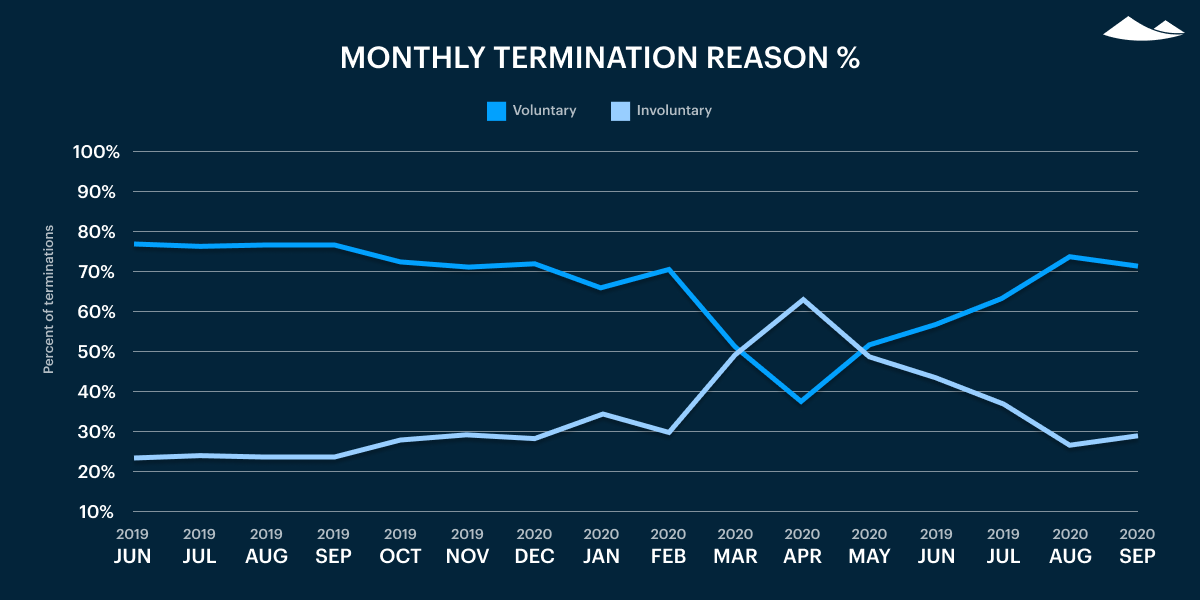

The ratio between involuntary and voluntary employee terminations has returned to pre-COVID levels;

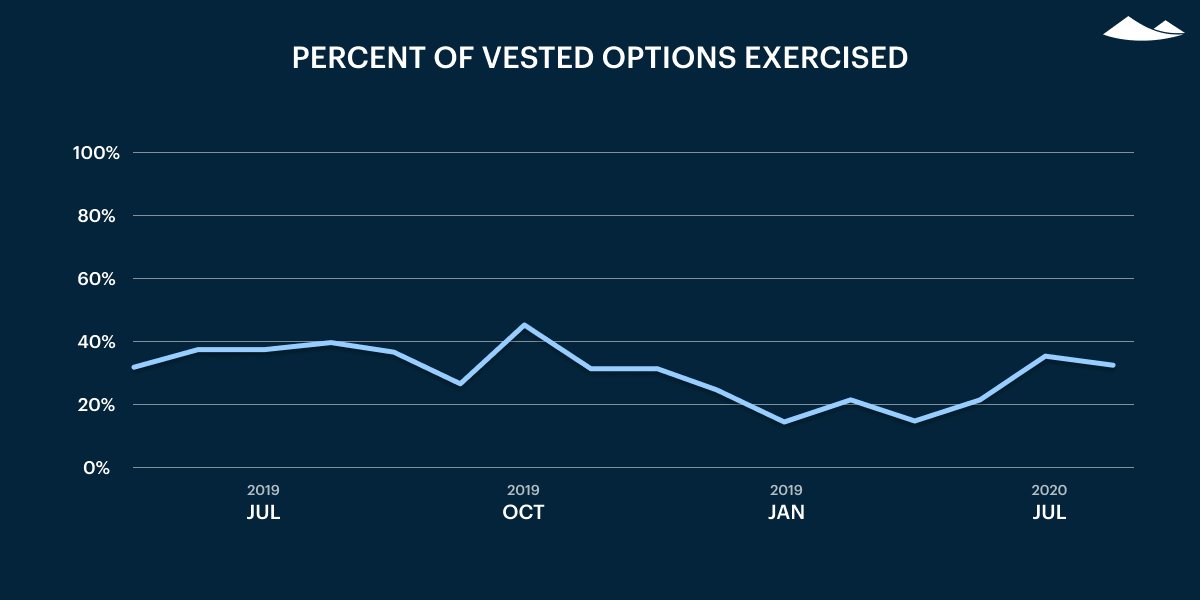

Employees are exercising vested options at pre-COVID levels once again, indicating renewed confidence in the market;

Despite a drop-off in involuntary terminations—a key indicator of the industry regaining momentum—there has not yet been a coinciding increase in hiring.

Carta’s Private Markets Quarterly Report examines trends across venture-backed companies and security holders in private companies to promote transparency between employers and employees, prompting fair equity management across private markets. More on methodology can be found at the end of the report.

Employee shareholders in Q3 2020

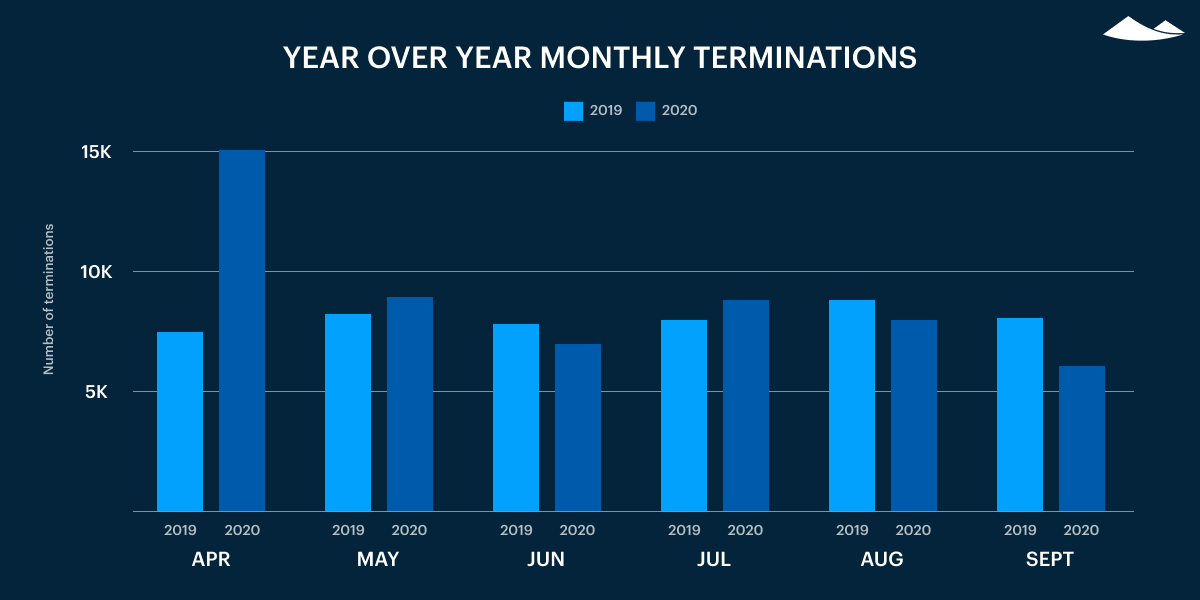

Monthly terminations, spiking in March and April, have now returned to pre-COVID levels.

The ratio between involuntary and voluntary terminations have returned to pre-COVID levels. However, data shows that average headcounts have not yet returned to pre-COVID levels, indicating a prolonged pause in hiring.

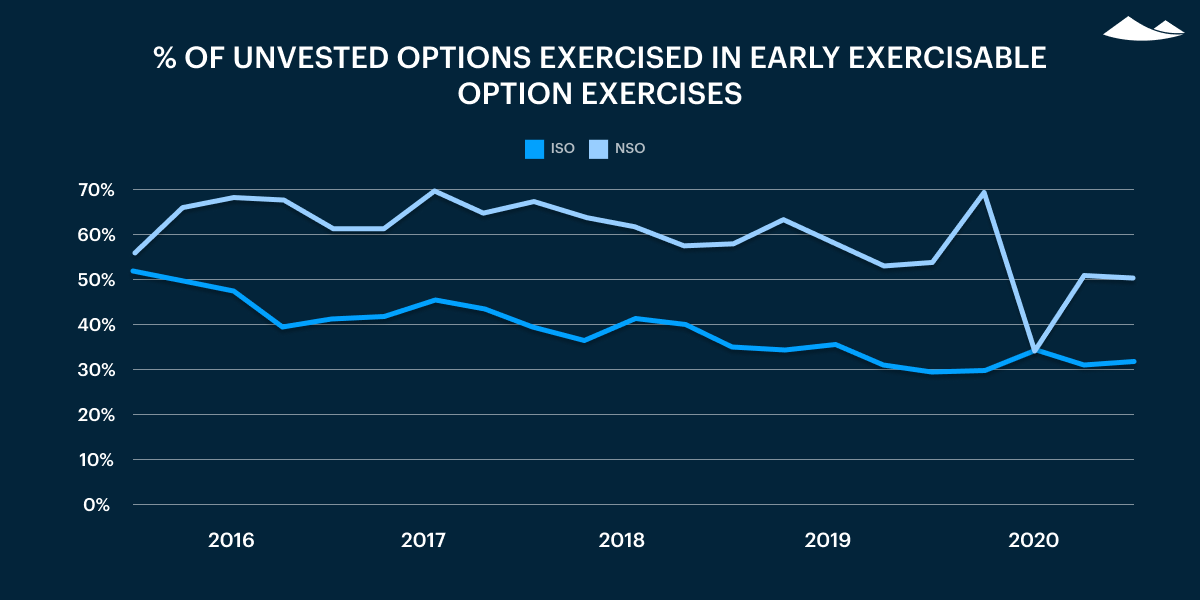

The percentage of unvested options exercised in early exercise transactions for ISOs was not affected by COVID. However, the percentage for NSOs declined sharply in Q1 and remained below historical averages in Q2 and Q3.

The percentage of vested options exercised has returned to pre-COVID levels, but employees are still leaving more than 65% of vested options on the table. This is an ongoing problem that we believe is a result of a lack of liquidity options, education, and resources.

Private company equity in Q3 2020

While median cash raised (the median amount a company raised in each series) is up YoY, the total $ value and rounds this quarter are down compared to Q3 2019 and Q3 2018.

Seed | ||

Series A | ||

Series B | ||

Series C | 32.60% |

*Note: Reporting on the number of rounds raised could be impacted by a reporting lag.

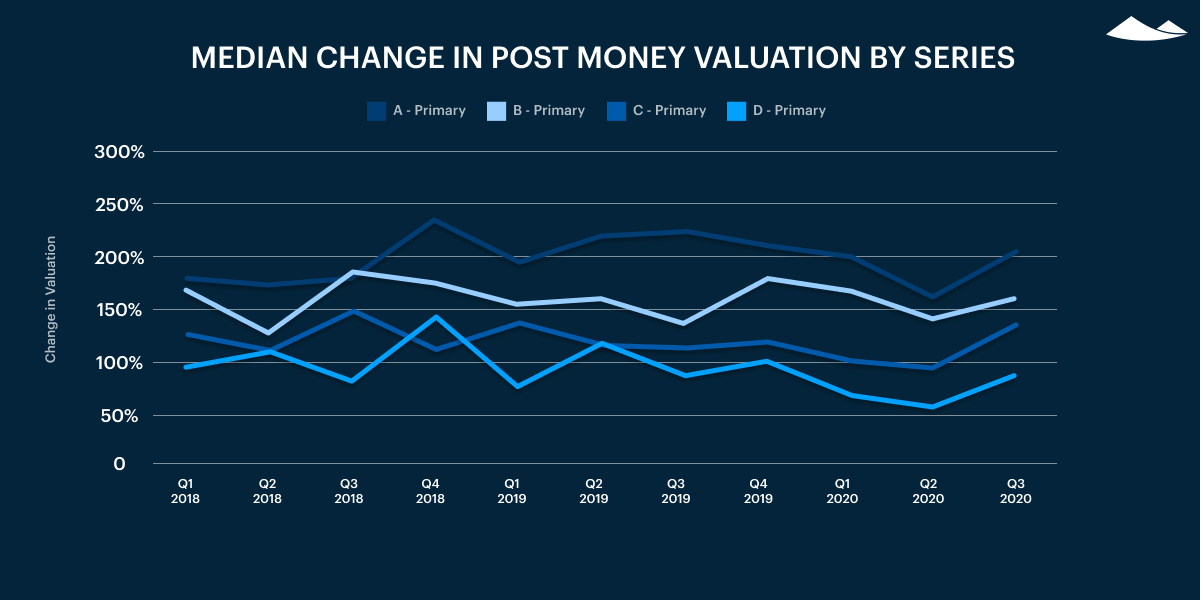

We saw a rise in post-money and pre-money valuations across the board. Valuations are now close to pre-COVID levels.

Q3 median pre-money valuation | Q3 median post-money valuation | YoY post-money change | |

|---|---|---|---|

Seed | |||

Series A | |||

Series B | |||

Series C |

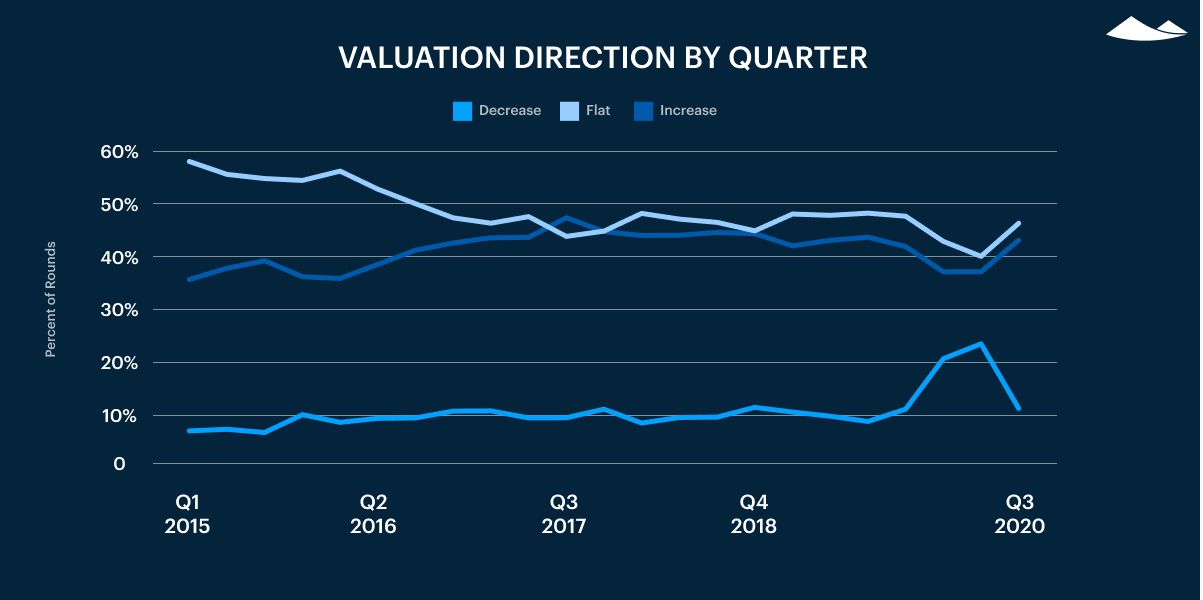

The direction of 409A valuations has returned to pre-COVID levels. With down rounds remaining relatively rare during the pandemic, the biggest driver of this recovery was public company revenue multiples, which hit all-time highs in Q3 and are frequently used when the company hasn’t raised financing recently.

Venture capital investors in Q3 2020

In Q3 2020, the overall number of deals decreased, but the proportion of deals by size stayed roughly the same.

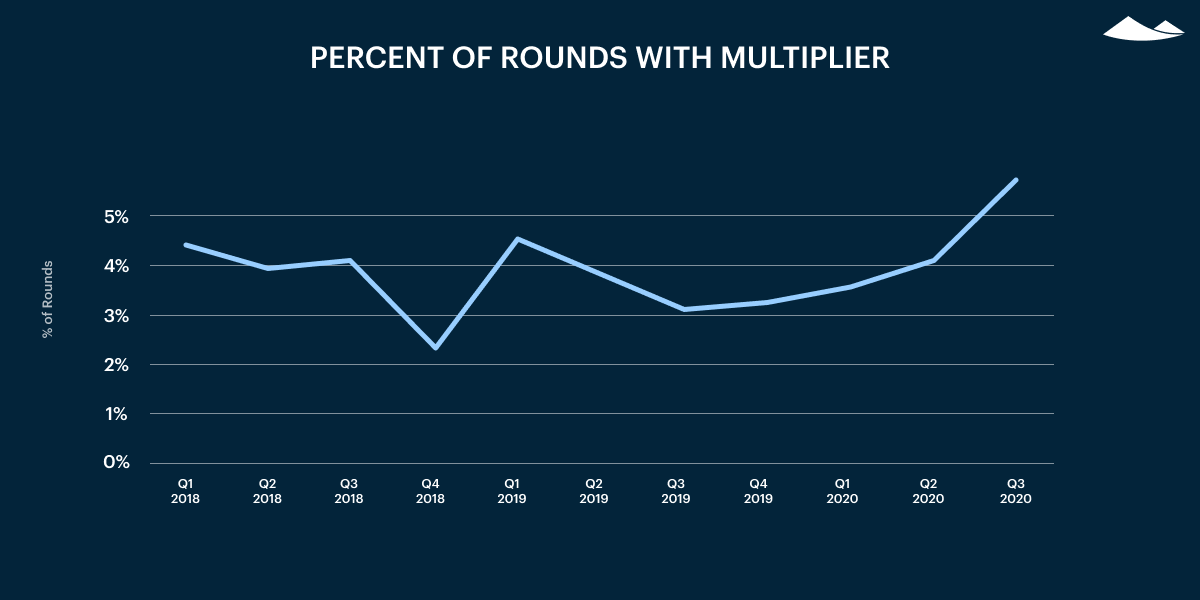

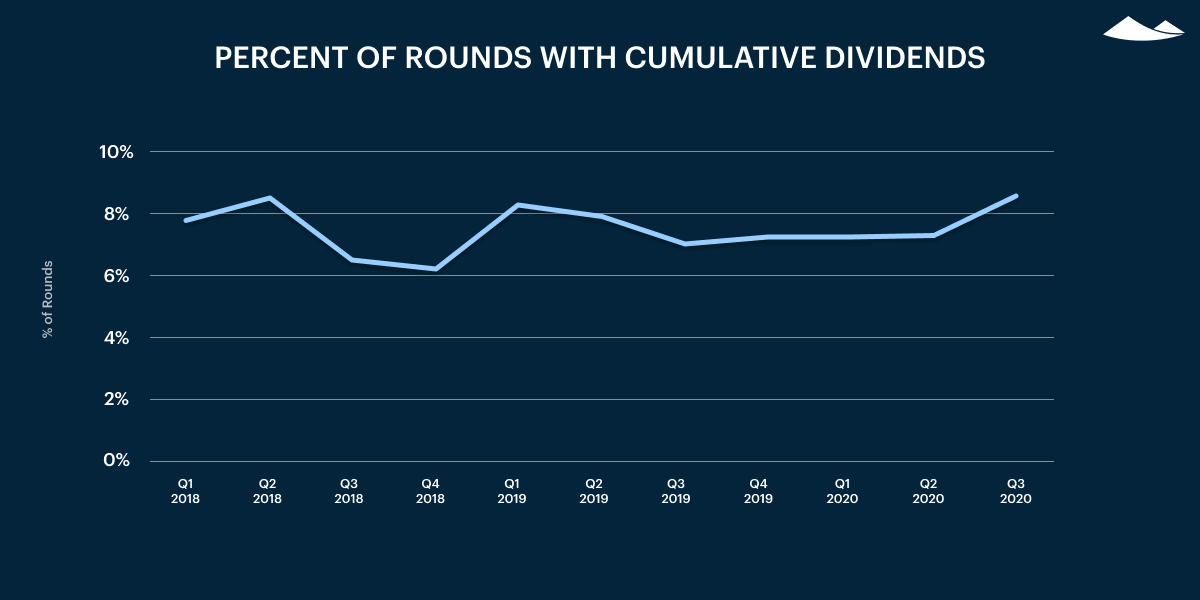

The percentage of rounds with nonstandard terms, cumulative dividends, or a multiplier went up slightly. This could indicate that investors are looking for additional protection as they continue to invest.

Carta’s data provides insight into private equity and venture capital. We will continue to report on the state of private markets in an ongoing series.

Methodology

Overview

Carta helps over 16,000 primarily venture backed companies and 1,000,000 security holders manage equity. This study uses an aggregated and anonymized sample of Carta’s cap table data. Companies who have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

The data presented in this private markets report was taken as of October 12, 2020. Historical data may change in future studies because there is typically an administrative lag between the time a transaction took place and when it is recorded in Carta. In addition, new companies signing up for Carta’s services will increase historical data available for the report.

Financings

Financings include equity deals raised in USD. The financing “Series” (e.g. Series A) is taken from the legal share class name. Financing rounds that don’t follow this standard are not included in any data shown by Series but are included in data not shown by Series.

Primary rounds are defined as the first equity round within a Series. Bridge rounds are defined as any round raised after the first round in a given Series. If there is no indication that a round is a Primary or Bridge round, both are included.

In some cases, convertible notes are raised and converted into multiple share classes within a Series at various discounted prices (e.g. Series A-1, Series A-2, Series A-3). In these cases, converted securities are not included in Cashed Raised and only the Post Money Valuation of the new money is included.

Terminations

Terminations entered into Carta must include a reason. Involuntary terminations include both terminations for performance and company layoffs. Voluntary terminations are employees that decided to leave of their own accord. Other termination reasons, including For Cause, Death, Disability, and Retirement were not included in the data and make up less than 1% of all terminations combined.

1 This study uses an aggregated and anonymized sample of Carta’s cap table data. Companies who have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta, Inc. (“Carta”). This communication is not to be construed as legal, financial, accounting or tax advice and is for informational purposes only. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein.