Every quarter, Carta releases information on the startup ecosystem in our State of Private Markets report. It can take a few weeks for rounds to be recorded on our platform, so we produce a full analysis after we get the final numbers.

In the meantime, we publish a “first cut” of data as close to the end of the quarter as possible. This initial analysis focuses on round valuations and cash raised across the venture stages.

Preliminary look at Q3 data for U.S. startups:

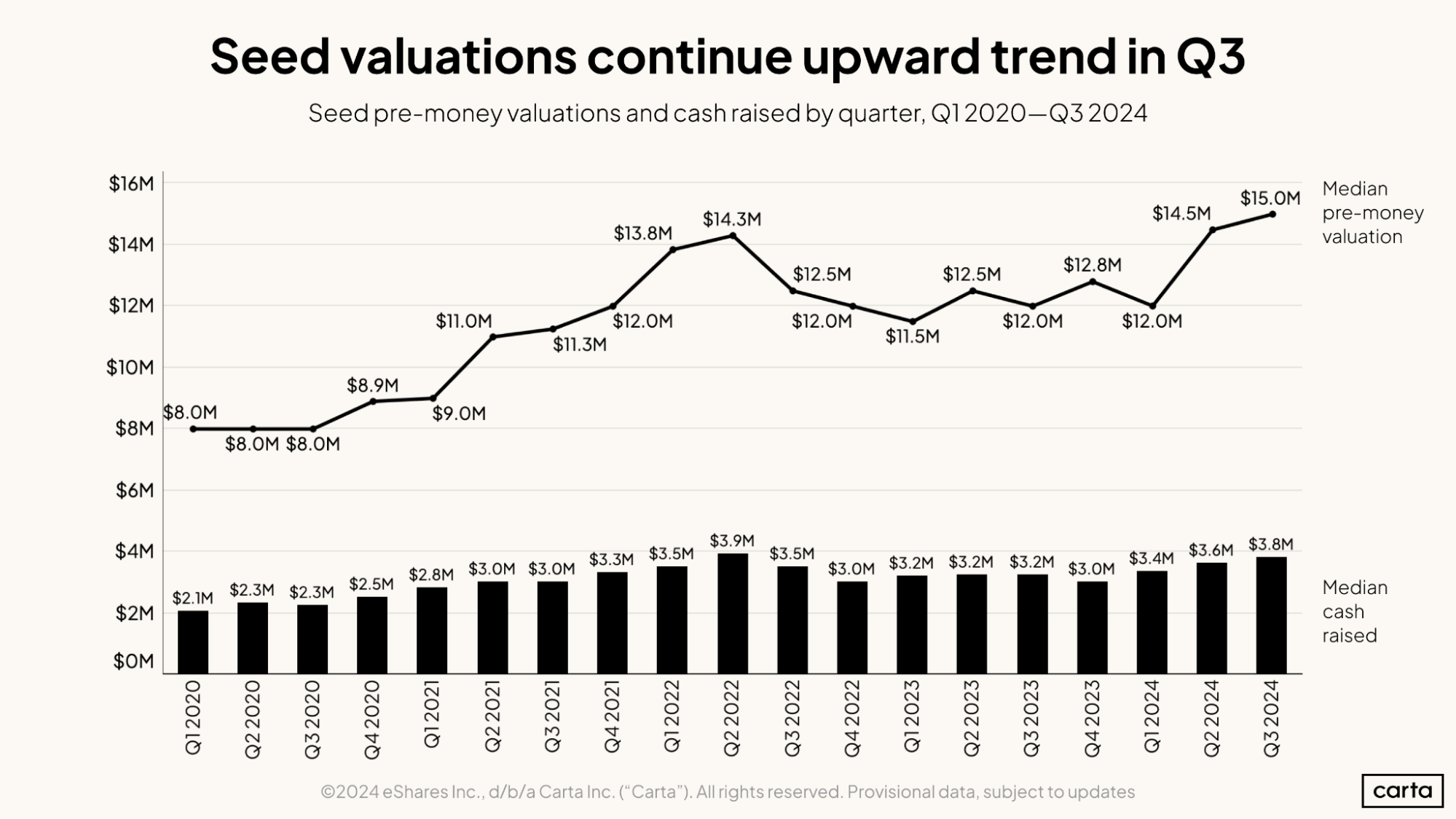

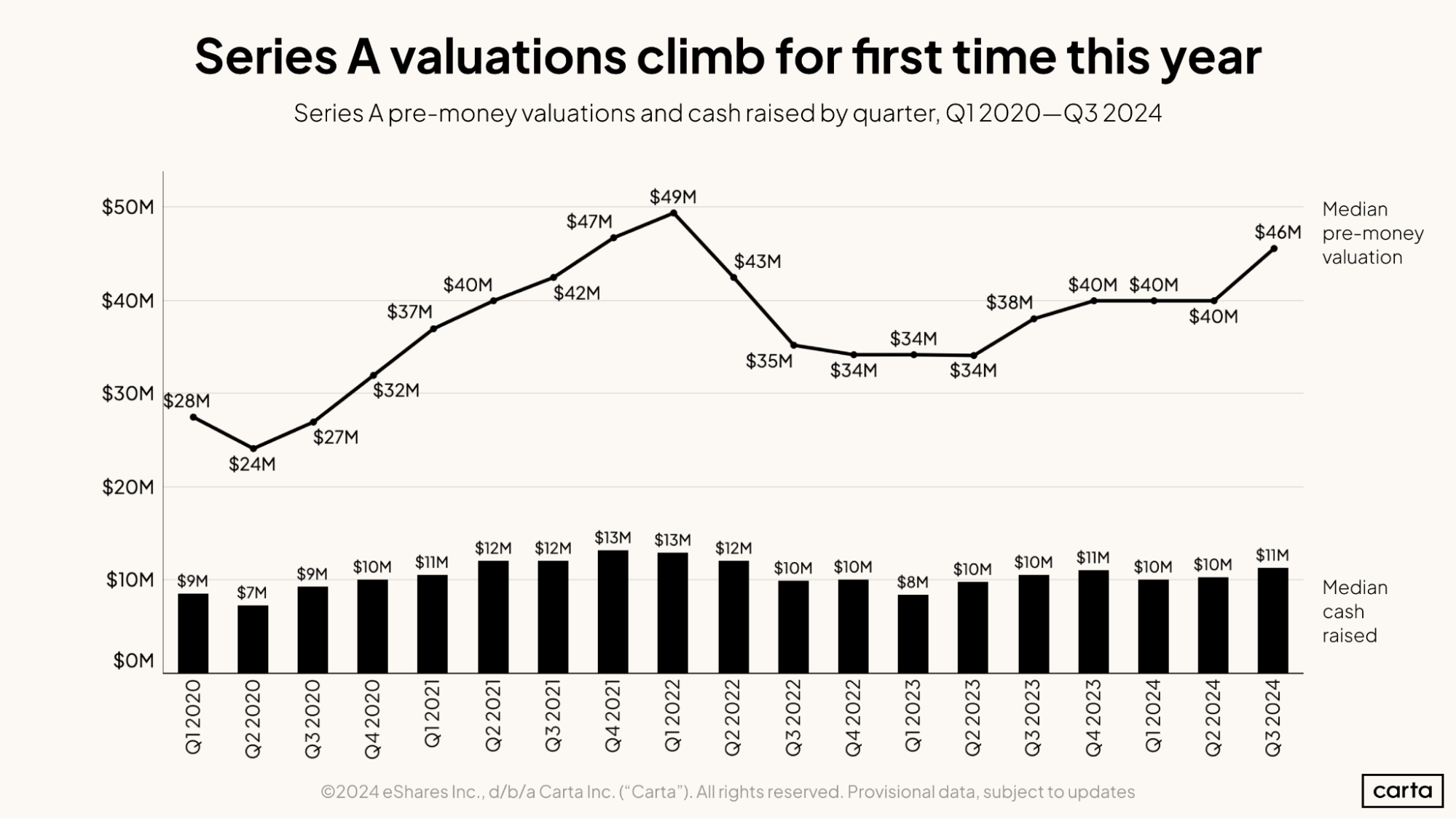

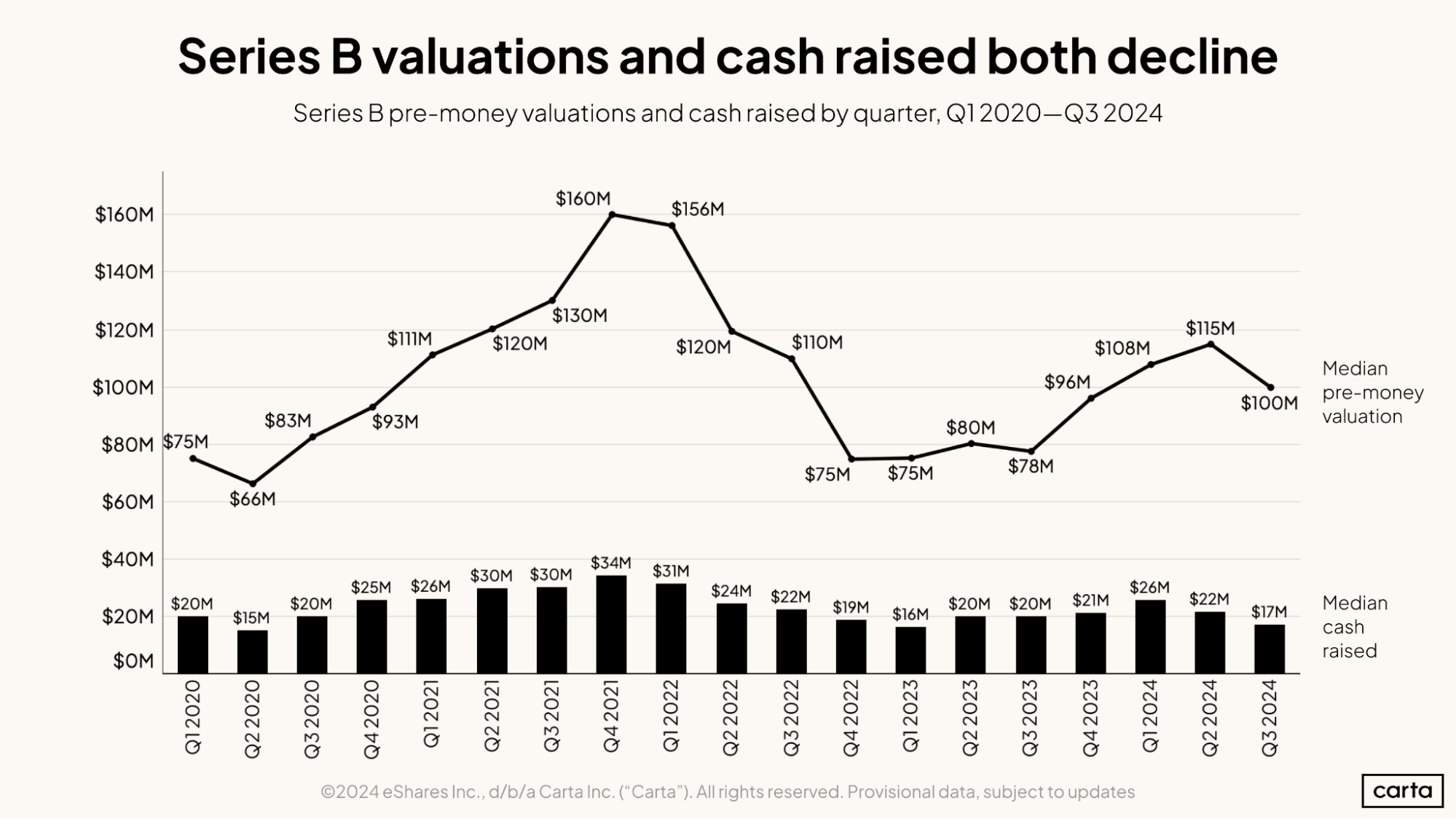

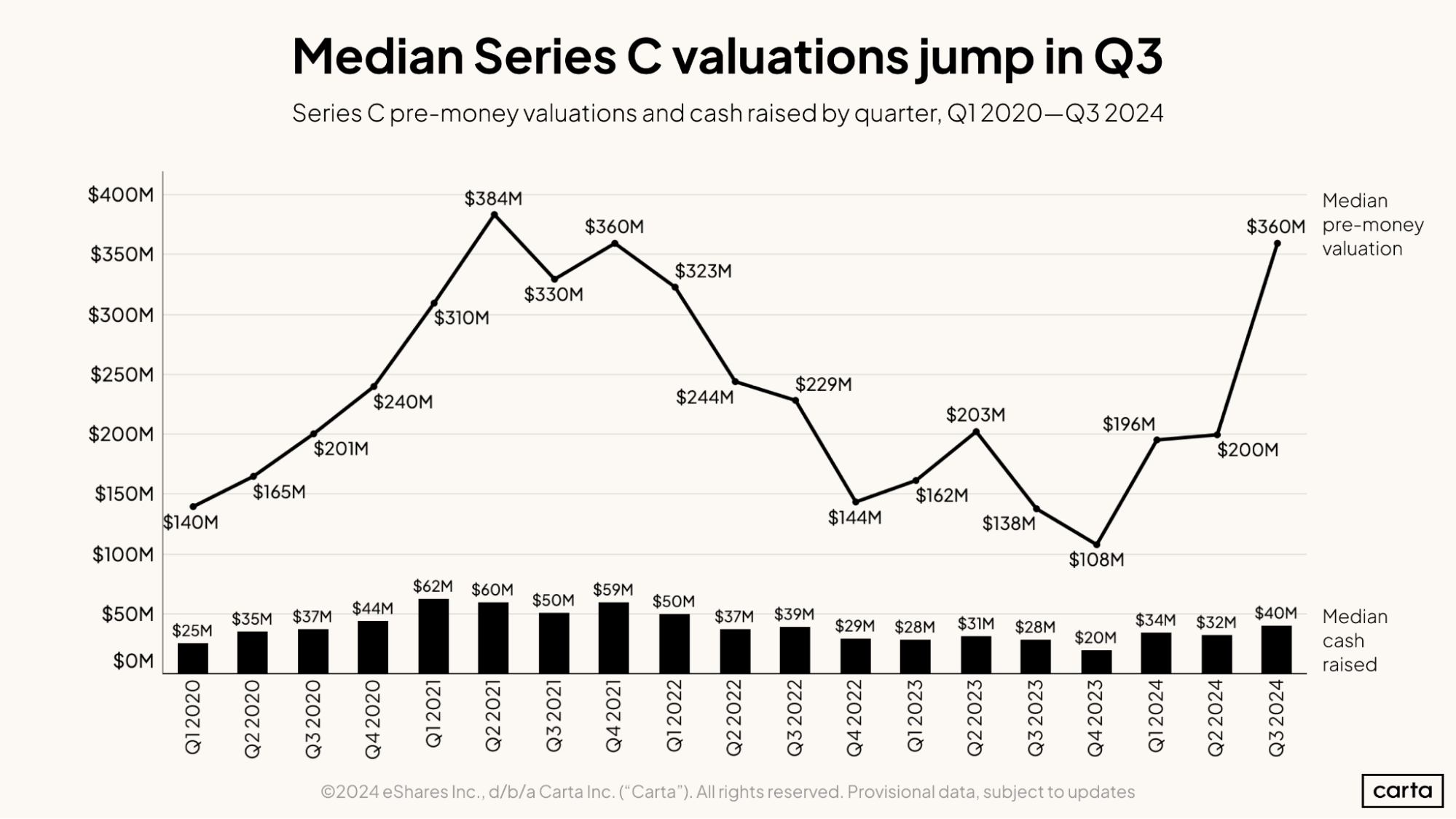

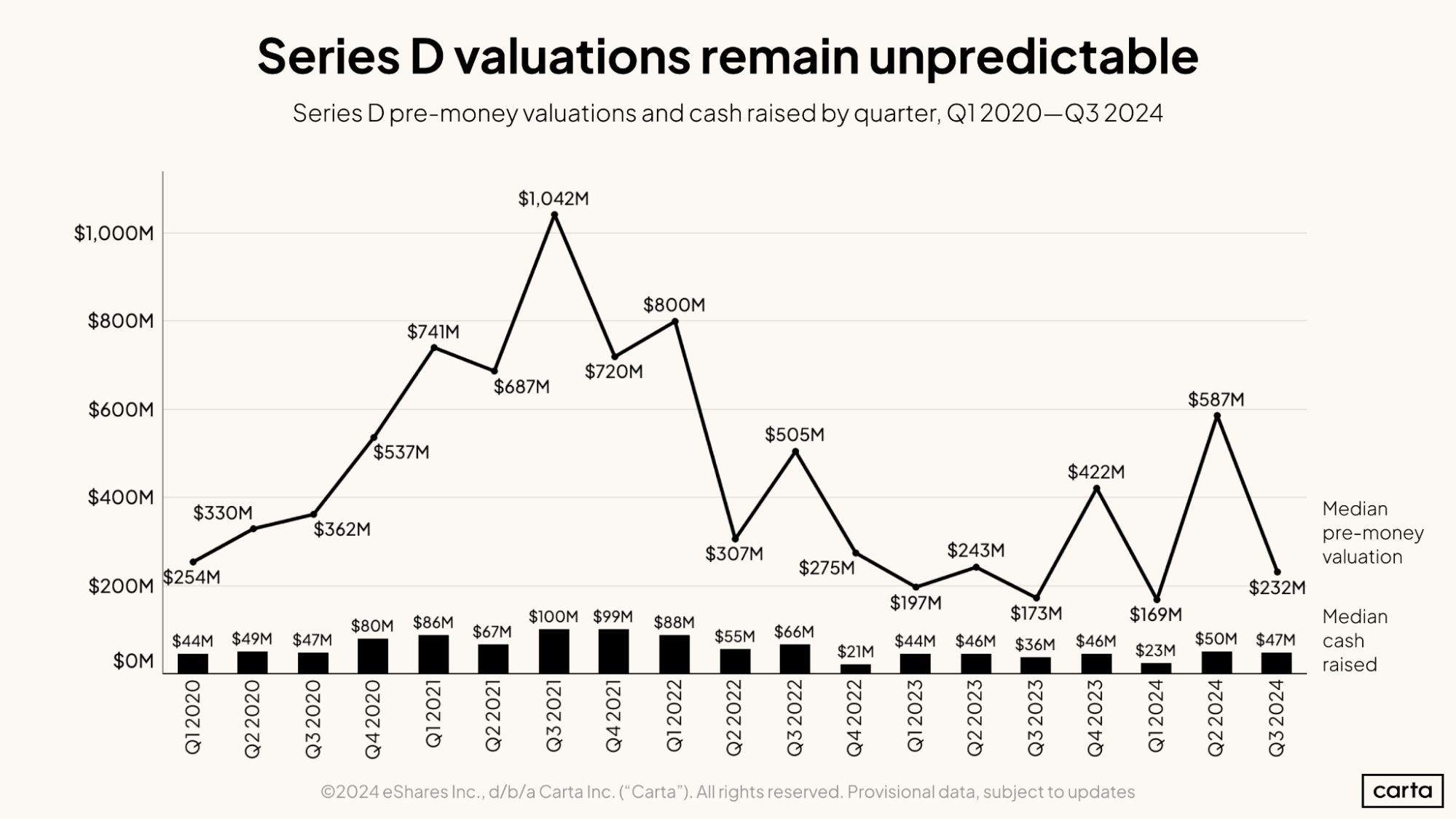

Cautious optimism in valuations: Following on modest gains in Q2, median pre-money valuations remained comparable with previous quarters. In rounds that experienced slight declines quarter over quarter, the median stayed above Q1 levels. Series C showed markedly positive movement.

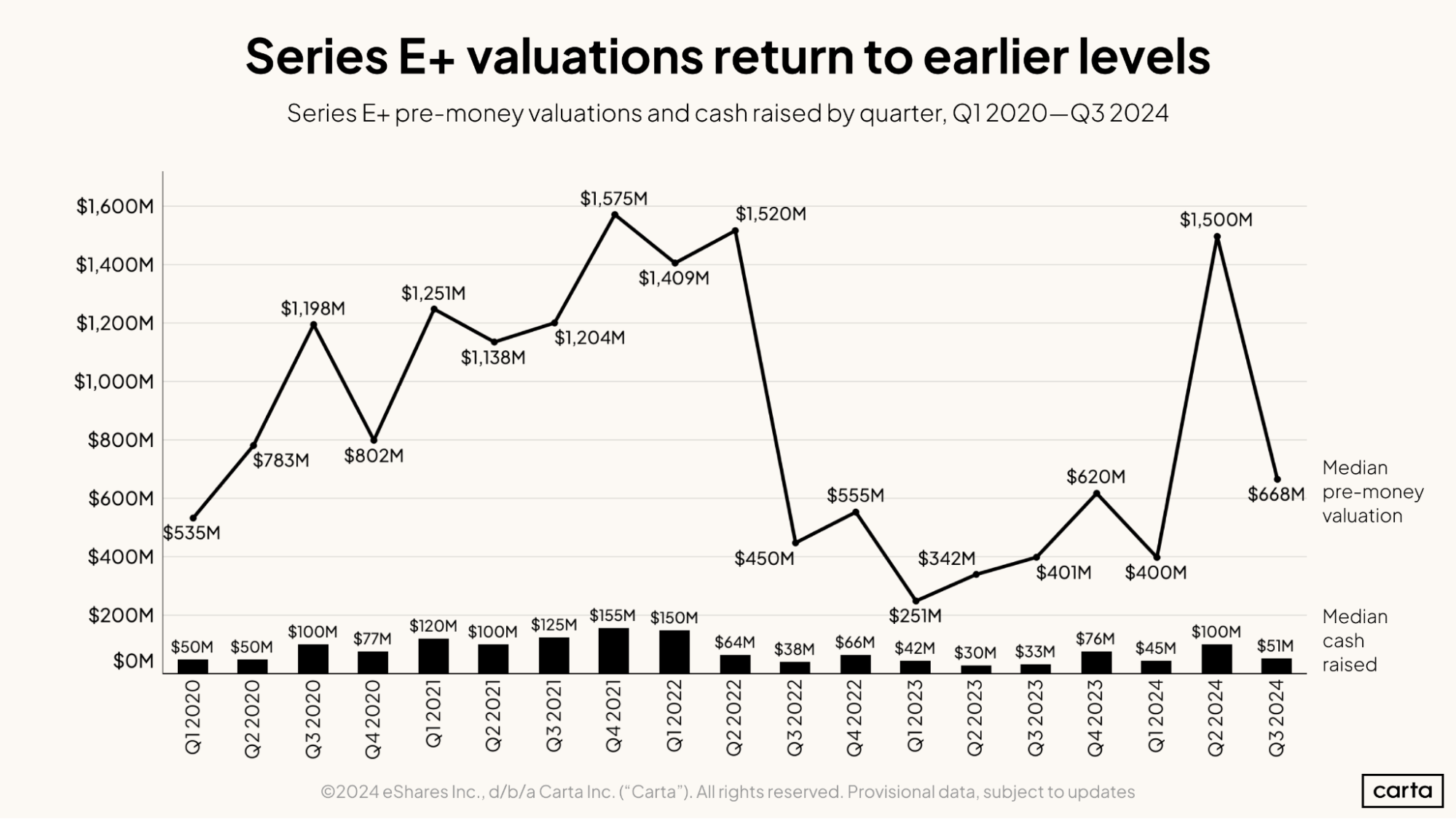

Consolidation in round sizes continues: The median cash raised last quarter remained consistent with figures from Q1 and Q2, hinting at stability in funding levels. Series E+ returned to Q1 levels after a notable spike in Q2.

While final numbers on total rounds and capital raised are not yet available for Q3, preliminary insights suggest that overall fundraising will stay in line with early 2024.

We’ll publish our full set of quarterly data in the coming weeks. To receive the full report direct to your inbox, sign up for our Data Minute newsletter.

To see the valuations and round size data below split into primary and bridge round figures, you can download this addendum now.

Seed

Series A

Series B

Series C

Series D

Series E+

Download additional data

For round valuations and round size data segmented by bridge and primary financings, download the addendum to our Q3 2024 First Cut: