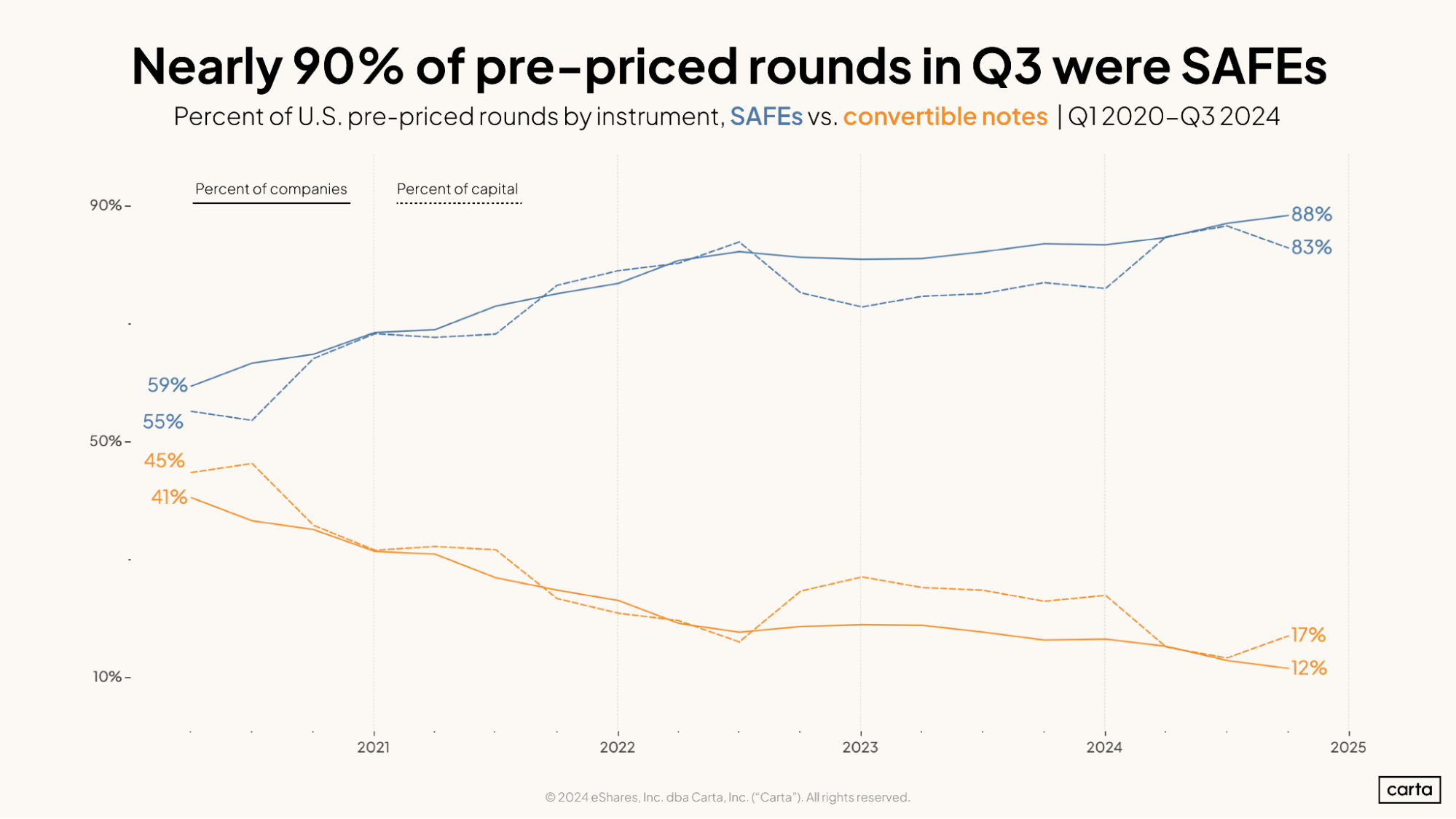

Startups on Carta raised 4,611 pre-seed rounds during the third quarter of 2024. About 88% of these rounds were SAFEs, and just 12% were convertible notes.

A dozen years ago, the SAFE—Simple Agreement for Future Equity—didn’t exist. In the 2020s, it’s become the dominant mechanism used by early-stage companies to raise capital at the pre-seed stage.

The SAFE was developed at Y Combinator in 2013 as a more-straightforward alternative to convertible notes, the traditional tool for pre-priced fundraising. Like convertible notes, SAFEs give investors the right to acquire equity in a startup when the company raises a priced round at a later date. Unlike convertible notes, SAFEs don’t act as debt, which can make them more appealing to founders seeking financial simplicity.

Ever since they surfaced as an option for raising early-stage cash, the SAFE has been growing in popularity among pre-seed startups. Increasingly, it’s a standard fundraising structure for seed startups, too.

“SAFEs are so much more common than they were 10 years ago,” says Julia Gudish Krieger, managing partner at Pari Passu Ventures, an early-stage venture firm and angel-investing platform that focuses on seed and Series A. “I think it’s become the standard for pre-seed and seed in many ways, unless you’re doing a really sizable seed.”

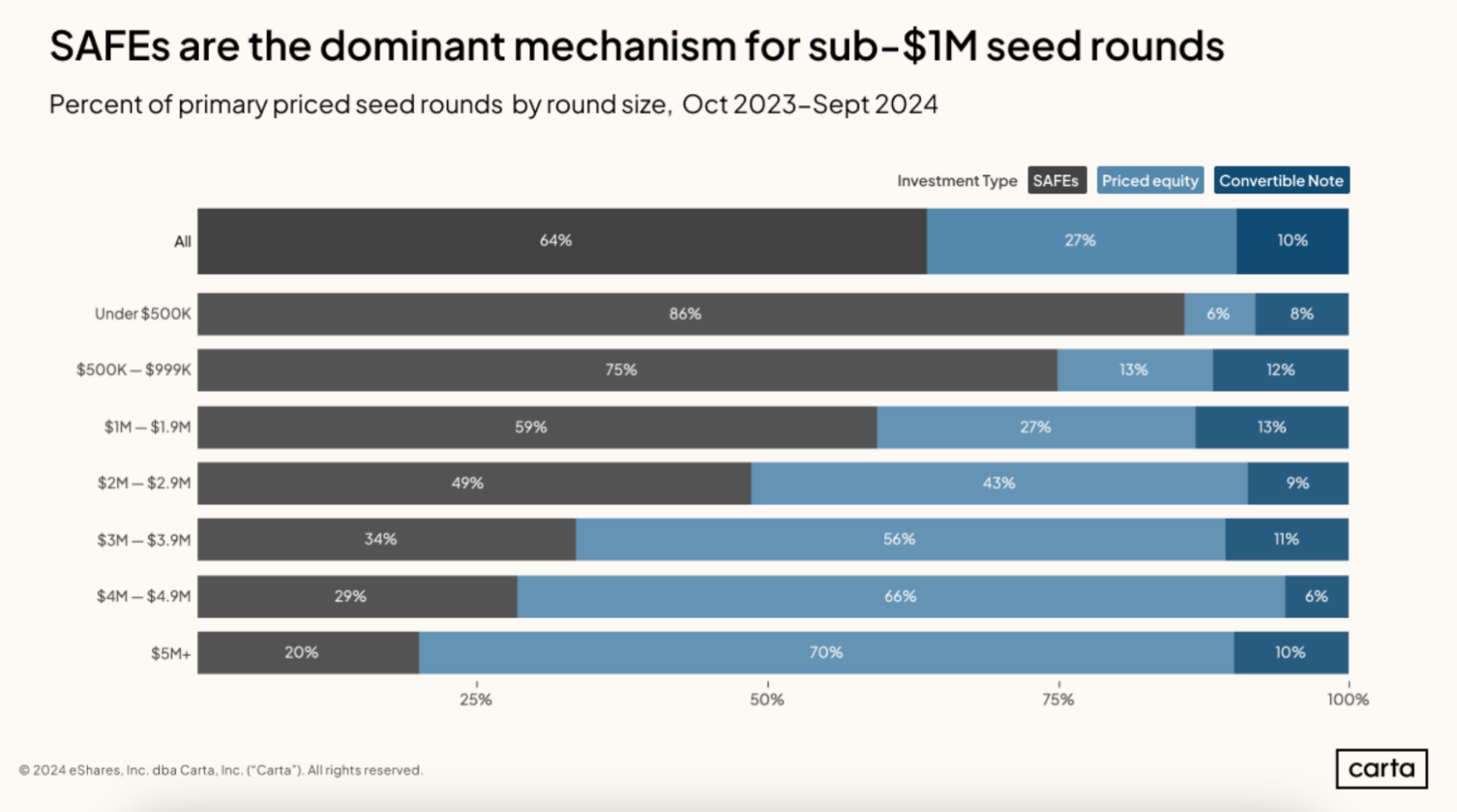

Seed-stage SAFEs

At the seed stage, startups have another structural option in addition to SAFEs and convertible notes: raising a priced equity round. Still, SAFEs are clearly the most popular choice.

From the start of Q4 2023 through the end of Q3 2024, about 64% of all seed rounds raised on Carta were SAFEs. Priced equity rounds made up 27% of the sample, and convertible notes about 10%.

The smaller the seed round, the more likely it is to be a SAFE—some 86% of seed rounds smaller than $500,000 were SAFEs. Up to $2 million, a seed round is still more likely than not to be structured as a SAFE.

Among larger deals, priced rounds predominate. Just 20% of seed deals larger than $5 million over the past year were SAFEs, while 70% were priced equity.

Given the roots of the SAFE as a relatively quick-and-easy fundraising structure, it makes sense that SAFEs are more common on smaller deals. As investments get larger, they can also tend to get more complicated.

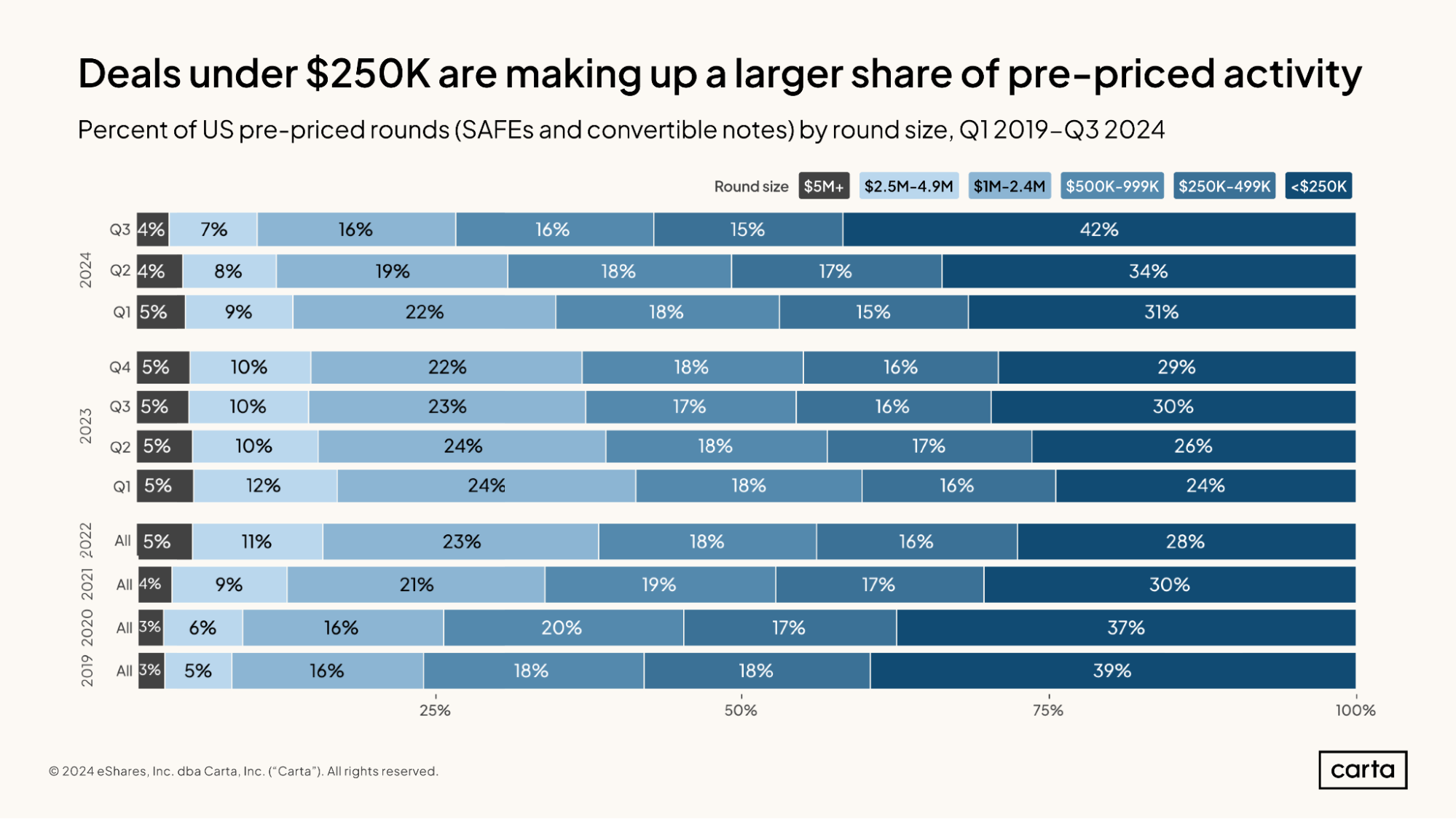

Pre-seed SAFEs get smaller

Within the pre-seed market, SAFEs aren’t only growing more common. They’re also getting smaller.

Last quarter, 42% of all pre-seed investments on Carta were smaller than $250,000, which would be a higher frequency than any full year since at least the start of 2019. And about 73% of investments were smaller than $1 million. The rate of pre-seed deals that fall below the $1 million mark has now increased in six straight quarters.

Krieger believes this statistical shift may be tied to broader trends in the early-stage market. During the venture slowdown that began in mid-2022, investors began to prioritize efficient spending and a focus on profitability over breakneck growth at all costs. In response to what was being asked of them, many young startups have scaled back their fundraising needs.

During the boom years, many startups raised as much cash as they could. These days, Krieger says, they’re more likely to raise only as much as they need.

“It’s positive to see companies focusing more from the get-go on the fundamental elements of the business and the unit economics,” Krieger says. “Back in the hype years, when everyone was getting funding, sometimes pre-seed or seed companies didn’t even have a model.”

Krieger isn’t always concerned with any specific numbers in a pre-seed startup’s model. Those sorts of projections will surely change as time goes by. She’s more concerned with other questions: How does the company see the market? What are its drivers? What are its assumptions? What are the things it doesn’t yet know?

“I always say, I know the model is wrong at this point,” Krieger says. “I just want to understand how you think about the drivers to your business.”

Get the latest data

Sign up for the Carta Data Minute newsletter to receive the latest data on VC financings, valuations, compensation, and more:

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.