In 2024, the median size of all seed rounds in the U.S. was $2.5 million. The median seed valuation was $14.8 million.

But the U.S. is a big, diverse place. In many ways, it is a single homogeneous market for venture capital investors. In other ways, it is many smaller regional markets rolled into one.

And across these regional markets, the typical seed round can look quite different.

Carta data shows that the typical round size and valuation on seed deals can vary widely depending on where the company is based. In California, for instance, the median seed round size last year was $3.2 million, and the median valuation was $17 million. In Florida, meanwhile, the median round size was $1.5 million, and the median valuation was $13.6 million.

The types of companies that are able to raise seed rounds can also differ significantly by state. In California, about 44% of seed deals last year were raised by SaaS startups and 19% went to startups in healthcare. In Florida, both SaaS and healthcare accounted for about 33% of seed-stage activity.

For this analysis, we examined how trends in round size, valuation, and industry compare across the seven states that have consistently been the largest U.S. markets for seed investment: California, Colorado, Florida, Massachusetts, New York, Texas, and Washington. As a supplement to the national fundraising data in our latest State of Private Markets report, this state-by-state look aims to offer more finely tuned context for founders and investors on the fundraising trail in 2025.

It’s worth noting that this is not a case where correlation proves causation. The simple fact that a startup is based in California does not mean it will raise more seed funding than a startup based in Florida. Geography is not destiny.

But the seed markets in California and Florida are undeniably different. They involve different founders, different investors, different advisors, different histories, and different local industries. In this sense, a company’s location can be a useful variable in assessing how fundraising trends differ across the U.S. seed landscape.

Seed valuations by state

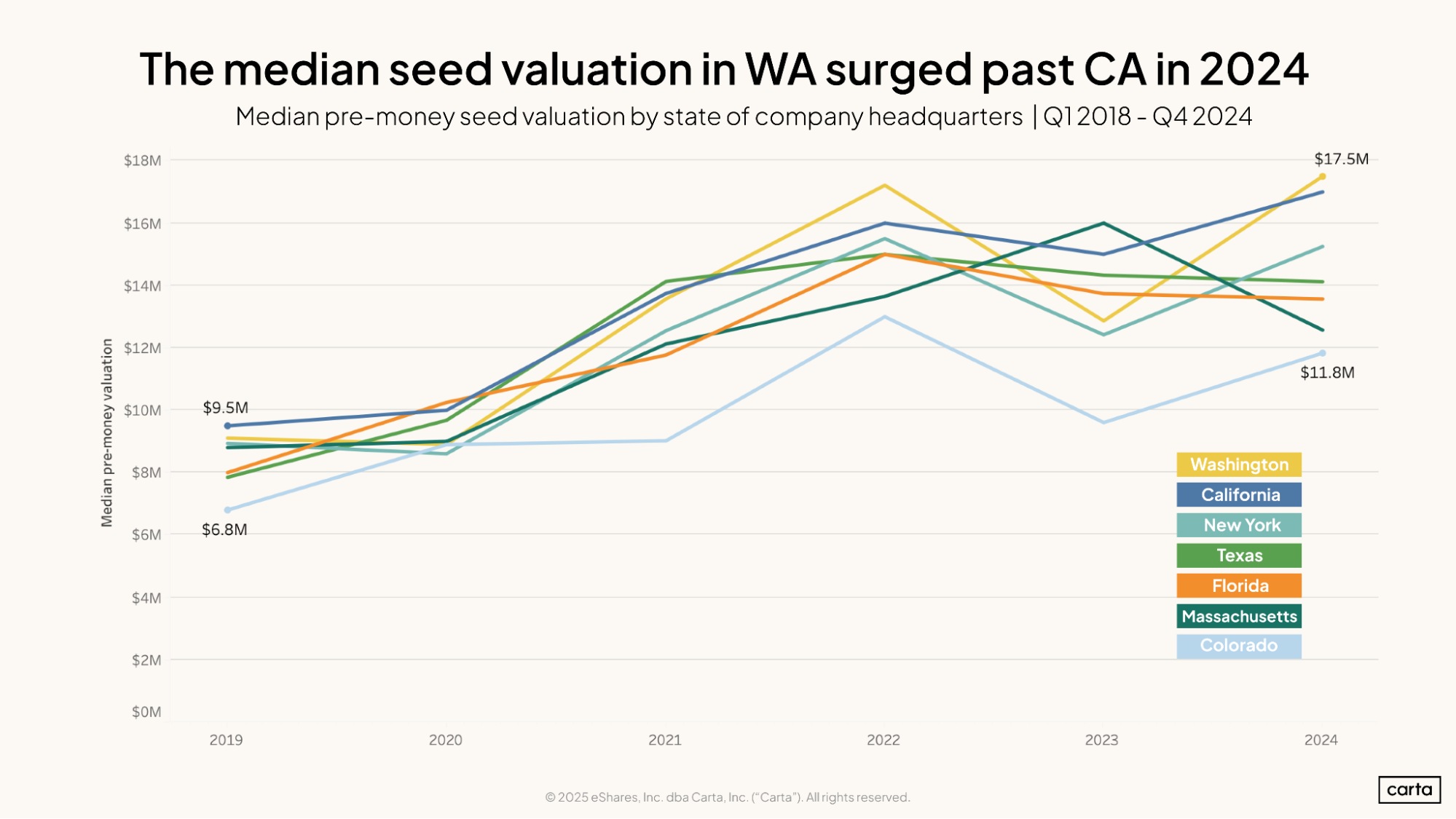

Among the seven top states for seed activity, Washington had the highest median valuation in 2024, at $17.5 million, with California close behind, at $17 million.

This was the second time in the past three years that the highest seed valuations could be found in Washington. The exception was 2023, when the state’s median seed valuation sank to $12.9 million.

California has consistently claimed one of the highest median seed valuations over the past several years, which makes sense given the state’s highly professionalized startup ecosystem. States where the startup industry is a little less firmly established, such as Florida and Colorado, have traditionally had lower median valuations.

Over the past several years, the relative difference between the highest and lowest seed valuations out of this sample have remained relatively consistent. In 2019, the highest median valuation ($9.5 million in California) was about 40% higher than the lowest median valuation ($6.8 million in Colorado). In 2024, the highest median valuation ($17.5 million in Washington) was 48% higher than the lowest ($11.8 million in Colorado).

State | 2024 median seed valuation | 2023 median seed valuation |

Entire U.S. | $14.8M | $13.1M |

Washington | $17.5M | $12.9M |

California | $17M | $15M |

New York | $15.3M | $12.4M |

Texas | $14.1M | $14.3M |

Florida | $13.6M | $13.7M |

Massachusetts | $12.6M | $16M |

Colorado | $11.8M | $9.6M |

Seed round sizes by state

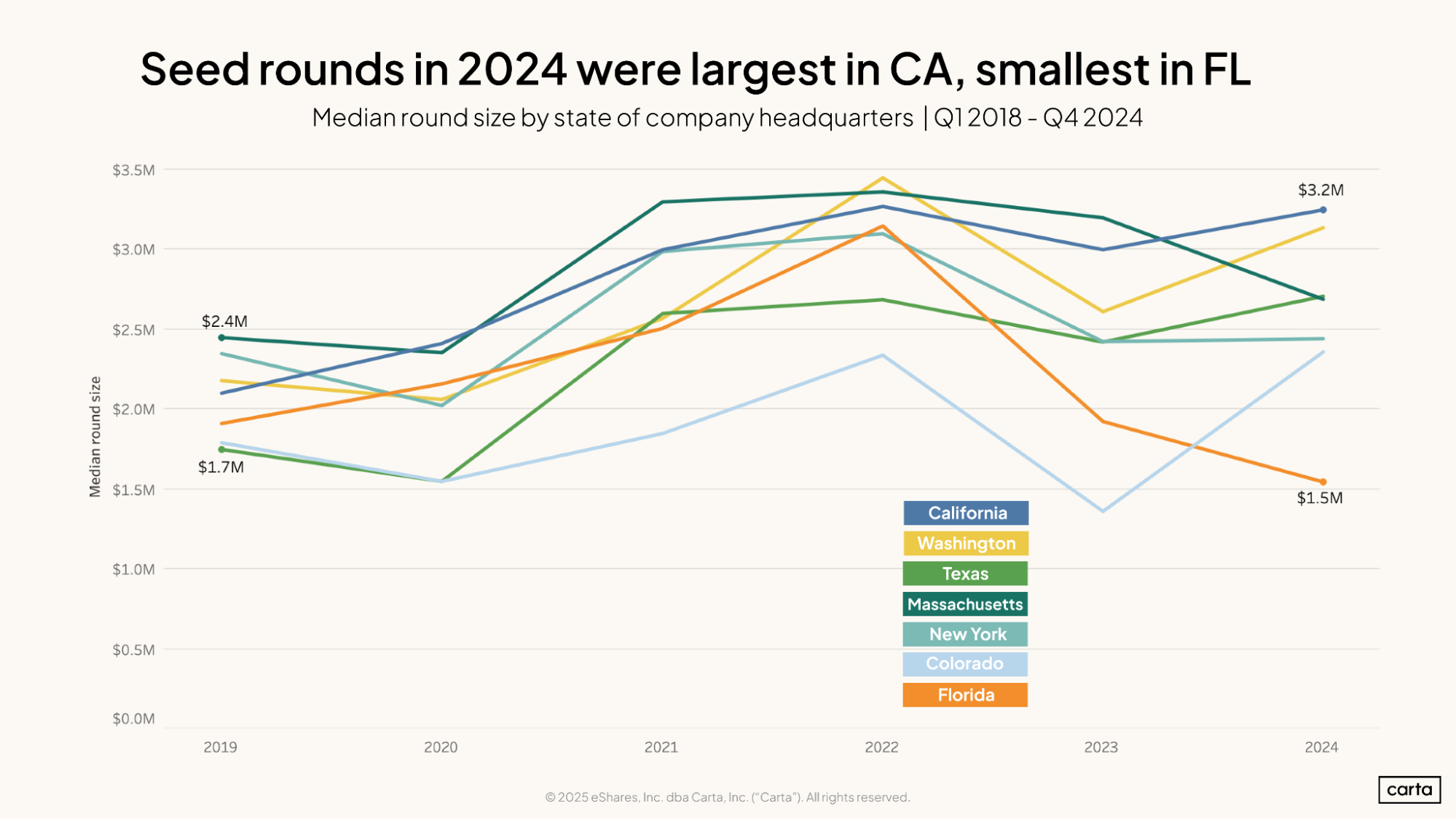

Washington and California were also the top two states in terms of median seed round size last year, but in inverted order. California finished atop the board, with a median round size of $3.2 million, and Washington was close behind, at $3.1 million.

In six of the seven states included here, the median round size in 2024 was either near or above the national median of $2.5 million. The obvious exception was Florida, where the median seed deal last year was just $1.5 million.

Between 2019 and 2022, the size of the median seed round in Florida increased for three consecutive years. Now, it’s fallen in back-to-back years, with a cumulative decline of more than 50%.

Deal numbers have been more steady in Texas, the other largest market for seed investment in the South. The median seed round size in Texas increased to $2.7 million in 2024, up from $2.4 million the year prior, while the median seed valuation declined only slightly, falling from $14.3 million to $14.1 million.

The median seed round got bigger in 2024 in four of the seven states included here. It held steady in one—New York—and got smaller in the other two.

State | 2024 median seed round | 2023 median seed round |

Entire U.S. | $2.5M | $2.4M |

California | $3.2M | $3M |

Washington | $3.1M | $2.6M |

Texas | $2.7M | $2.4M |

Massachusetts | $2.7M | $3.2M |

New York | $2.4M | $2.4M |

Colorado | $2.4M | $1.4M |

Florida | $1.5M | $1.9M |

Seed industries by state

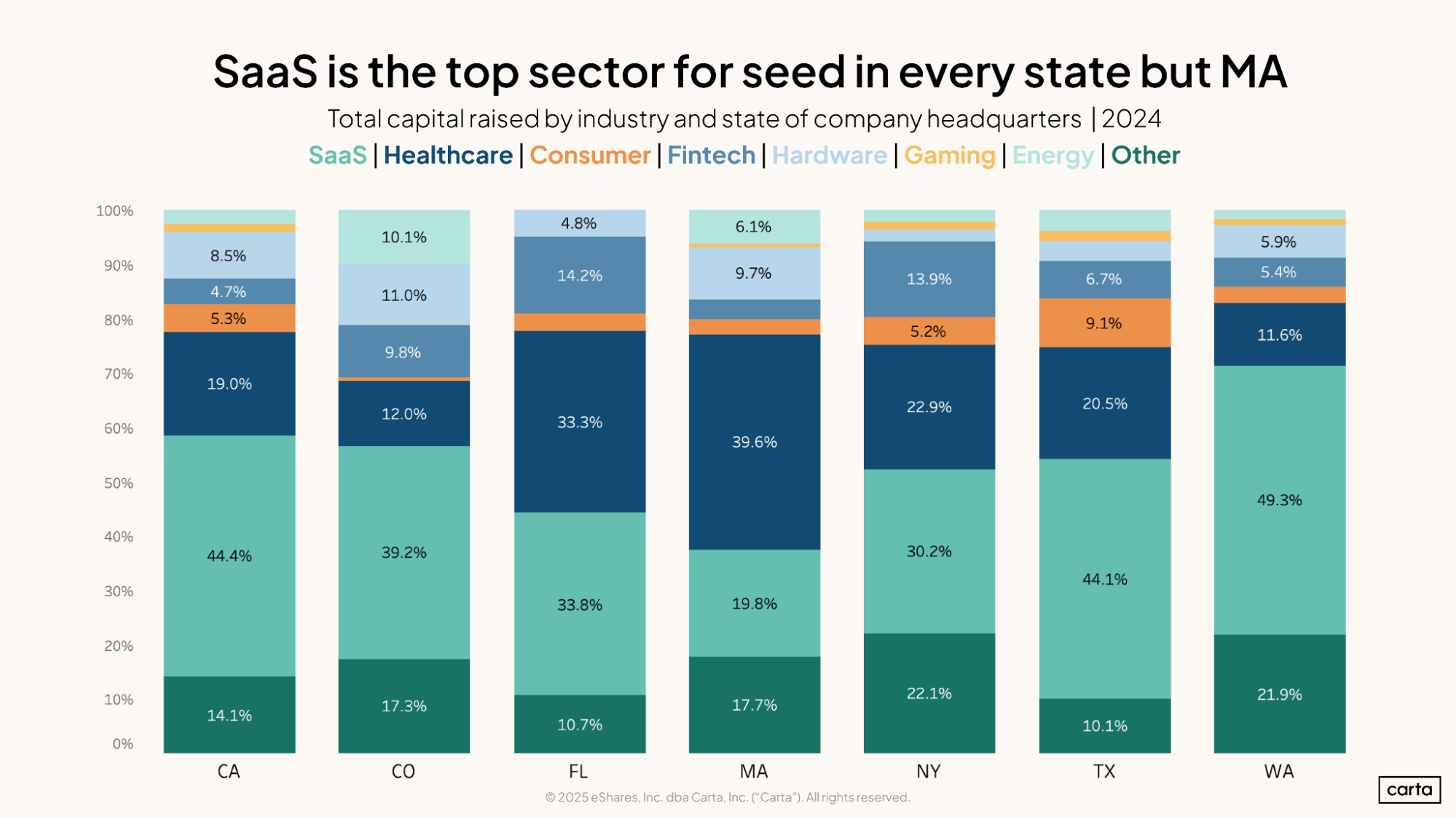

The SaaS sector is the most popular industry for new seed investment in six of the seven states included here. The exception is Massachusetts, where healthcare makes up a plurality of all deal activity.

SaaS investments are most dominant in Washington, where they were responsible for 49.3% of all capital raised in 2024, and California, where they accounted for 44.4% of cash raised. It’s not a coincidence that the two states with the highest incidence of investment in SaaS are also the two states with the highest median round sizes and valuations: Software companies consistently garner some of the highest prices in venture capital, including many AI-powered companies that were on the fundraising trail in 2024.

Massachusetts is the state where healthcare makes up the largest portion of new seed investment, at 39.6%, followed by Florida, at 33.3%. Florida is also the top state for the fintech sector, with 14.2% of all seed capital invested, with New York next, at 13.9%.

In terms of sectors, Colorado is an outlier in two respects: It is the only state where at least 10% of seed capital last year went to the hardware sector, and it’s also the only state where at least 10% of capital went to energy deals. Massachusetts—which has emerged as something of a hub for a nascent nuclear energy sector—ranks second among these states in terms of the proportion of seed capital going to energy startups, at 6.1%.

Sign up for the Data Minute newsletter:

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.