As a startup founder, you're probably juggling plenty of acronyms and arcane terminology. From SAFEs and ISOs to 83(b) and more, there’s no end to the technical details you must master. But there’s one number that quietly sits at the center of it all that you really need to get right: your 409A valuation.

Think of the 409A valuation as your company’s annual "Price is Right" moment, except if you guess wrong, the IRS or your auditors aren’t handing out a consolation prize.

409A valuations determine the fair market value (FMV) of your company’s common stock, and they are necessary if you want to issue stock options without triggering painful tax consequences. They also give companies up to 12 months of “safe harbor” protections from the IRS (more on that below).

But the process can feel confusing, overly technical, and a bit mysterious. That’s why we’ve put together this no-fluff guide to help you understand what matters most, ask the right questions, and avoid costly missteps.

Let’s demystify the 409A once and for all.

What is a 409A valuation?

A 409A valuation is an independent appraisal of the FMV of a private company’s common stock. These valuations are performed by independent third-party providers, professional firms, or individuals that specialize in determining a company's audit-ready FMV at a given point in time. Think of it in contrast to a publicly traded company, where the FMV is simply the active market price.

409A valuations derive their name from IRC Section 409A, introduced under the American Jobs Creation Act of 2004. Section 409A established strict reporting and taxation guidelines that aimed to prevent the abuse of deferred compensation arrangements made by Enron executives before the company’s collapse in 2002.

While stock options can be exempt from the provision’s significant tax penalties, this exemption only applies if you grant those options at or above the FMV of your company’s common stock at the time of the grant.

This is why a 409A valuation is necessary: it provides an independent, defensible assessment of the FMV of your company’s common stock. With a valid 409A valuation in place, a private company can issue options that comply with tax regulations and avoid painful financial consequences.

Why and when do I need a 409A valuation?

You need a 409A valuation before issuing common stock options. Your FMV expires from Safe Harbor at the earlier of twelve months or upon a material event.

What is Safe Harbor: A 409A valuation is eligible for Safe Harbor when completed by an unaffiliated or independent party. Safe Harbor status places the burden on the IRS to prove that the valuation is “grossly unreasonable” if contested.

The penalties for a 409A valuation contested outside of Safe Harbor can be severe. They may include deferred compensation from the current and preceding years becoming taxable immediately, plus accrued interest on the revised taxable amount, plus an additional tax of 20% on all deferred compensation. Yikes!

What is a material event: It is best practice to speak with your legal counsel and valuation provider to determine whether an event is material. Below are a few examples of a material event.

A new round of preferred financing

A large secondary transaction

Significant revisions in forecasts

A meaningful acquisition

Serious consideration of a letter of intent (LOI) to be acquired

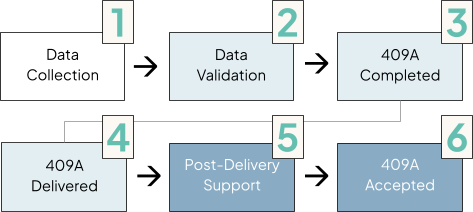

409A valuation process

Many valuation providers break their 409A valuation process into six steps.

You’ll submit all necessary information (requested valuation date, capitalization, historical and forecasted financials, company update, etc.) to your valuation provider via a secure, online portal. Your provider will review the submission, reach out for outstanding items, complete the 409A valuation, and deliver a draft.

We’ll add here that your forecasts, especially for early-stage companies, do not need to be robust. Simple estimates will suffice.

Communication with your provider up through this point may be limited to the initial submission, or there may be several points of interaction. The level of communication will vary depending on the complexity of the engagement, but you should be upfront about the frequency and form of communication that you expect throughout the process. You should also ask your firm how long they think the process will take so you can keep this mind and hold them to that timeline.

Once you receive the draft, your valuation provider should always be available to discuss. Whether you would like to suggest a revision, receive a walk-through to better understand what was done, share the feedback you hear from showing the draft to your investors or legal counsel, your valuation provider should be there! This is also a good time to share the valuation with key stakeholders like your board, investors, legal counsel, and auditors.

Your provider will finalize the 409A valuation once all parties understand and are comfortable with the conclusion. Additionally, most providers will offer unlimited audit coverage on the 409A valuation for financial reporting post-acceptance.

What actually matters in a 409A valuation?

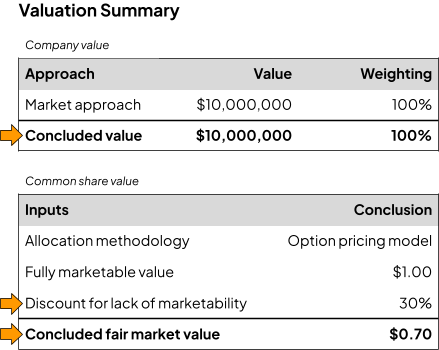

Your 409A valuation may be 50+ pages, but do not fear! Most 409A valuations have a summary page highlighting three key pieces of information: concluded value, concluded fair market value, and discount for lack of marketability (DLOM).

Concluded value (company value): The concluded value, typically an equity value, is the total value of your company for the purpose of IRC 409A. This is different from your post-money valuation, and it is not meant to represent the value of your company for fundraising or sale purposes. This value is a direct result of the methodology your valuation provider uses.

Concluded fair market value (value of common stock): Jumping to the concluded fair market value (FMV), the company can issue options with a strike price at or above that price, or $0.70 in this example. This represents the market value of common stock as of the valuation date. There are several factors that can influence the FMV outside of the total value of your company:

If the total value of your company is the numerator, and your capitalization table is the denominator, an increase in dilution detracts from the value of common stock

Overly punitive rights and preferences held by preferred stock holders also detract from the value of common stock

Greater uncertainty, as reflected by a higher volatility and longer exit horizon in the option pricing model (OPM), increases the value of common stock

Discount for lack of marketability (DLOM): The discount for lack of marketability quantifies the illiquid nature of equity in a private company, and also impacts the value of common stock. The longer the exit horizon, the higher the DLOM; the higher the DLOM, the lower the value of common stock. (Note: A longer exit horizon in the OPM creates a greater potential value for common stock, whereas a longer exit horizon in the DLOM signifies that your company is further from a liquidity event, which lowers the value of common stock.)

How does a changing 409A valuation affect the strike price?

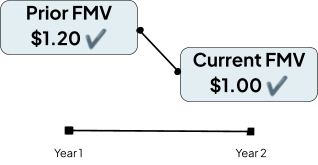

409A valuations are conducted at regular intervals and often lead to changes in your FMV. When that happens, you may need to adjust the strike price of the equity you issue, but it depends on how the FMV is changing.

For example, let’s assume your FMV, as determined by the 409A valuation, was $1.20 twelve months ago. Now, with a new 409A valuation, your FMV is $1.00 (there are a number of reasons why an FMV may decrease).

Your company can issue options with a strike price at or above the current FMV of $1.00, or you could even choose to maintain the strike price of $1.20 from one year ago. However, maintaining that price would be disadvantageous for employees, given that it would require them to pay a 20% premium on the determined fair market value.

What if the FMV increased to a price of $1.05 after another twelve months?

Your company could issue options with a strike price at or above $1.05, meaning it could choose to continue maintaining a price of $1.20, but it could not maintain a price of $1.00, given that is below the current FMV of $1.05.

What should I do upon receiving my 409A valuation?

First and foremost, talk to your valuation provider! Ask them four questions:

Can you walk me through the report?

How did you arrive at the company value, value of common stock, and DLOM?

Are my conclusions in line with industry peers at my stage of development?

What adjustments should we make, if any, to result in a more attractive strike price?

You can (and should!) also seek input from your company’s board of directors, investors, and legal counsel.

If this is not your company's first 409A valuation, you should also do a side-by-side comparison with the summary page of your prior 409A valuation. Ask yourself two questions:

How did the company value and value of common stock change, and does that meet my expectations? If not, what caused the difference?

As a rule-of-thumb for value progression, unless there have been material changes to your company’s capitalization table or rights and preference, the % change to the company value and % change to the value of common stock should be roughly the same. Said differently, if your company’s value increases by 10%, the value of your common stock should also increase by 10%.

How did the DLOM change? Do I believe that any change to my company’s exit horizon is reflected in a change to the DLOM?

As a rule-of-thumb, your DLOM should equal 10% x Exit Horizon (Years), with an exit horizon capped at five years. For example, if your exit horizon is four years, your DLOM should be around 40%.

Final thoughts

409A valuations aren’t just a box for founders to check, they’re a foundation for how you reward your team, maintain regulatory compliance, and set your company up for long-term success. Understanding the basics and finding the right provider can save you from costly missteps and give you more control over your equity strategy. If you have any questions, please reach out to Ryan O'Conor (ryan.oconor@carta.com).

This article is part of an educational collaboration between Carta and Andreessen Horowitz. The next entry in the series, "409A Valuations 102: Methodologies and Beyond," will appear in January.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.