- Black-Scholes Model (BSM)

- What is the Black-Scholes Model?

- Understanding the value of a stock option

- Time value vs. intrinsic value

- How the Black-Scholes Model works

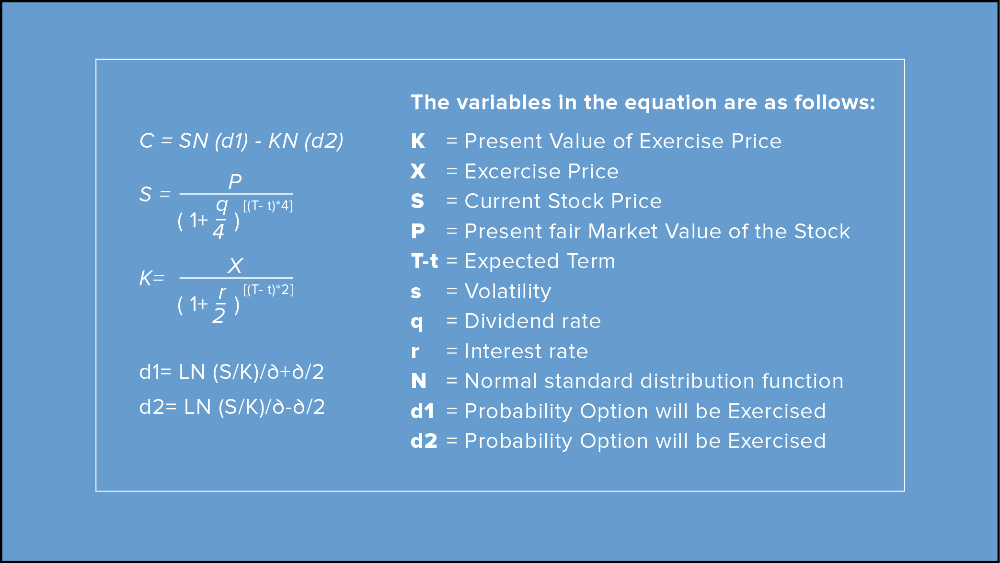

- Black-Scholes Model formula

- Black-Scholes assumptions

- Limitations of the Black-Scholes Model

- Performance conditions

- Capped limits

- How Carta uses the Black-Scholes Model

What is the Black-Scholes Model?

The Black-Scholes option pricing model (also called the Black and Scholes Model, the Black-Scholes-Merton Model, or simply “BSM”) is one of the most commonly used methods to value stock options and is generally accepted as the standard across all option-pricing models. The BSM formula uses only a few fixed parameters, which allows auditors to easily recalculate the value of stock options.

Understanding the value of a stock option

Historically, stock options were valued simply by “intrinsic value” —the difference between the stock price and the exercise price. Under that assumption, the intrinsic value of a stock option where the exercise price is the same as the stock price is zero.

A stock option with zero intrinsic value on the grant date does not literally have zero value. If the stock price increases, there is an advantage in being able to buy the stock at a lower exercise price.

Time value vs. intrinsic value

The Black-Scholes Model was the first widely used option-pricing model to consider the element of time value alongside intrinsic value. Time value is the value within the time period in which the option is exercisable in relation to potential interest earned and increase of the stock price (volatility).

For example, imagine a stock option with a 10 year life and an exercise price of $5. On the grant date, the company’s stock price is also $5, thus the option has zero intrinsic value ($5 - $5 = 0). Since the $5 exercise price is always the same, the holder may instead invest $5 in a risk-free treasury bond and earn 10 years worth of interest. When the bond matures 10 years later and the holder receives back the initial $5 plus interest, the holder can choose to exercise if the stock price has appreciated over the years. If the stock price has not appreciated, the holder would simply let the stock option expire unexercised. Essentially, the stock option allows holders to benefit from future appreciation of the stock without having to make an investment until the appreciation has occurred.

How the Black-Scholes Model works

The Black-Scholes Model is a mathematical formula that uses the following inputs:

Current Price/Present Value of the Asset (S): The market price of the underlying asset (for private companies, a 409A valuation is generally used to determine the fair market value of the common stock).

Strike Price (K): The price at which the option can be exercised.

Time to Expiration (T): The time remaining until the option's expiration date, usually expressed in years.

Risk-Free Interest Rate (r): The theoretical rate of return on an investment with zero risk.

Implied Volatility (σ): A measure of the asset's price fluctuations over time.

Black-Scholes Model formula

The Black-Scholes formula is expressed as:

Alternative option pricing models often involve complex “decision-tree” approaches and account for a wide scenario of possible outcomes. The Black-Scholes Model is easier for most people to understand than other types of models.

Black-Scholes assumptions

The Black-Scholes Model operates under several key assumptions:

Efficient markets: The model assumes that markets are efficient, meaning that asset prices fully reflect all available information.

Constant risk-free rate: The risk-free interest rate is assumed to be constant over the life of the option. In reality, interest rates can fluctuate due to economic conditions, but this assumption simplifies the calculation.

Log-normal distribution of returns: The model assumes that the returns of the underlying stock follow a log-normal distribution, which implies that the asset's prices cannot become negative and have a skewed distribution.

No dividends: The Black-Scholes Model originally assumed that the underlying asset does not pay dividends during the option's life. However, the model has since been modified to account for dividend payments.

No taxes or transaction costs: The model assumes the absence of taxes, transaction costs, and other frictions in the trading process, allowing for the seamless buying and selling of the option and its underlying asset.

Limitations of the Black-Scholes Model

Despite its widespread use, the Black-Scholes Model has limitations. When companies issue stock options where vesting is subject to performance conditions or have capped limits to the value (such as a floor or ceiling), the Black-Scholes Model does not consider these elements and a more complex option pricing model should be used.

Performance conditions

A performance condition is when an additional future event, milestone, or achievement is required to occur in order for the stock option to vest. This is often used to incentivize employees to perform in a manner that helps meet the performance condition requirement as opposed to a standard time-based vesting which primarily encourages employees to stay at the company. The Black-Scholes Model does not consider the likelihood of meeting the performance condition.

Capped limits

Companies may issue capped stock options which include a limit to the possible value the employee may receive. This limitation lowers the value of the stock option which then reduces the company’s compensation expense and potential dilution. A capped stock option exists when there is a defined limit to the amount of value the holder may receive upon exercise. For example, if the holder exercises a stock option where the intrinsic value (current stock price less exercise price) is greater than the capped amount, the number of options exercisable would then be reduced. The Black-Scholes Model assumes a constant volatility value for the price of an option and does not take into consideration elements that cap a stock option’s value.

How Carta uses the Black-Scholes Model

Companies who issue equity as a form of compensation are required under accounting guidance ASC 718 to recognize compensation expenses on their income statement. Carta has helped thousands of companies by automating the application of the Black-Scholes Model to determine the amount of expense the company is required to recognize for each grant.

As the industry’s leading provider of 409A valuations, Carta uses the Black-Scholes Model to determine a strike price that’s both reliable and beneficial for employees. It accurately reflects the complex liquidation structures of private companies in the venture ecosystem.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.