- Healthtech shows signs of resilience amid venture downturn

- From frenzy to fallout to rebound: Healthtech venture shows signs of life.

- What’s behind the Q4 uptick in healthtech?

- Megadeals bounced back

- Public market resilience trickled down to growth-stage deals

- The healthcare industry still has tailwinds

- Learn more

- Get weekly insights in your inbox

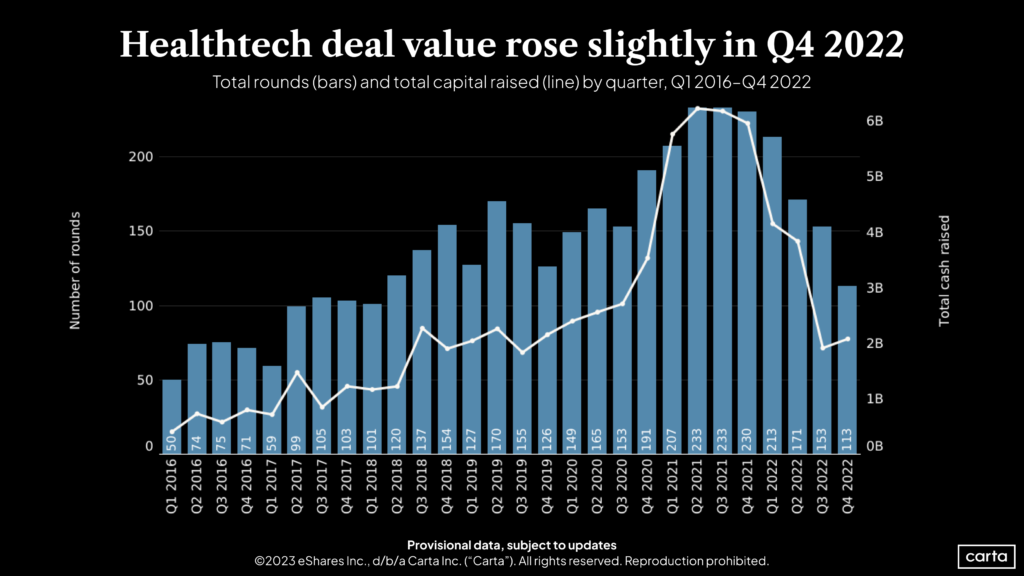

Venture capital’s appetite for healthtech rebounded slightly in Q4, following a sustained decline through much of 2022.

In Q4, investors poured roughly $2.1 billion into digital healthcare companies—a 10.5% quarter-over-quarter increase from Q3’s $1.9 billion. The uptick reversed five consecutive quarters of declining healthtech investments.

However, the total number of healthtech rounds declined for the sixth straight quarter, dropping from 153 rounds in Q3 to 113 during the final three months of 2022, a 26% dip. That was the lowest quarterly total of rounds raised in healthtech since Q1 2018.

Venture capital invested in healthtech companies has dropped 66% since Q2 2021, though that’s still a smaller dip than total venture capital invested, which has dropped 77% during the same timeframe.

From frenzy to fallout to rebound: Healthtech venture shows signs of life.

The digital healthcare ecosystem grew to $160 billion in market size by the end of 2021, with forecasts predicting the market would surpass $1 trillion by 2030. Healthcare providers have had to adapt to the increasing dominance of digital tools, paving the way for venture-backed healthtech companies that promise to ease the transition. VC investment opportunities in those startups became plentiful as a result, with investment dollars in healthtech companies on Carta peaking in Q2 2021.

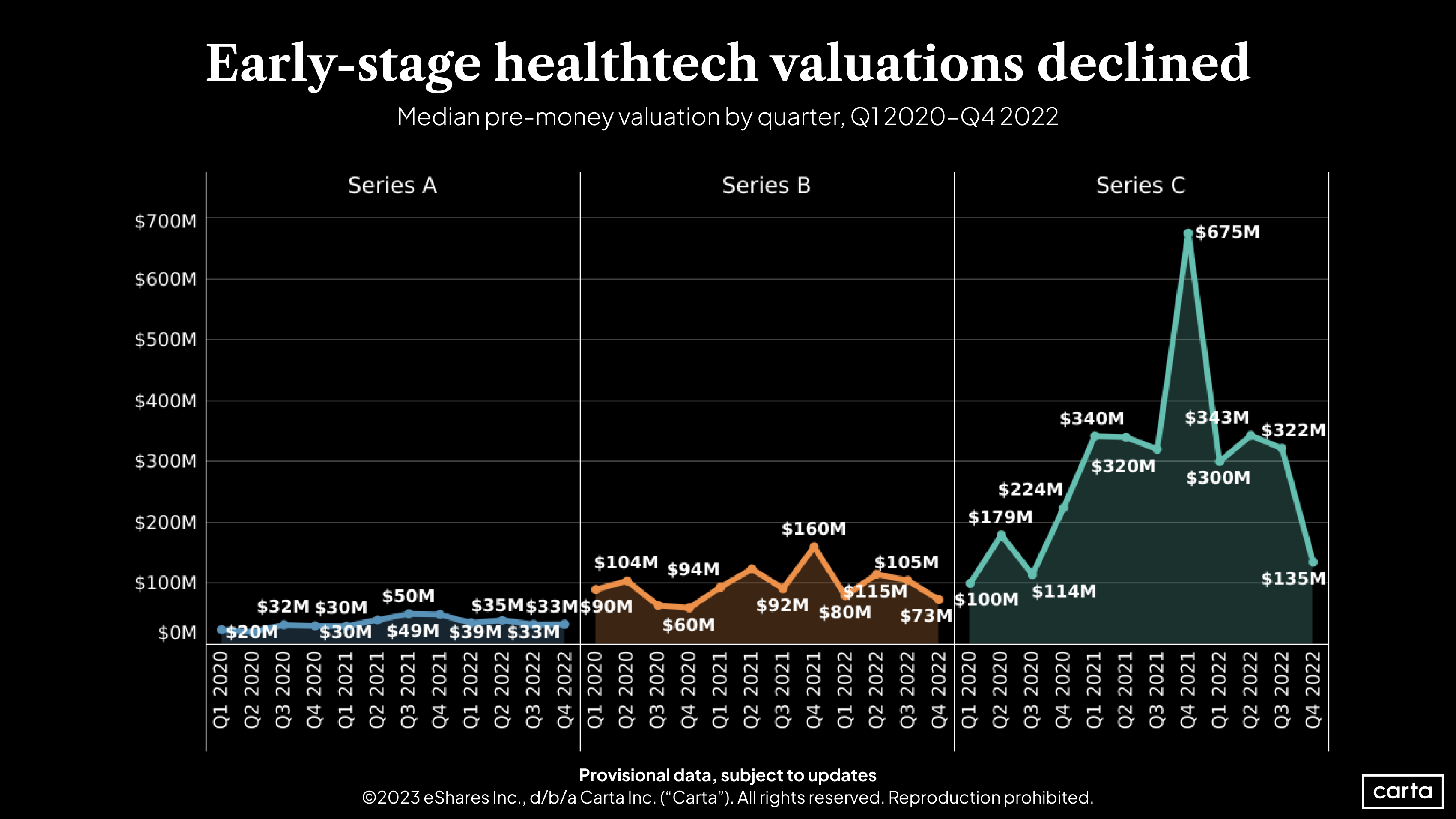

But trouble began in early 2022, when growth-stage healthtech valuations plummeted in response to macroeconomic pressures, mirroring a drop experienced across other sectors of the VC ecosystem. These falling valuations likely contributed to the pullback on the deal side, and healthtech founders came to grips with their new suppressed valuations. Some turned to unpriced bridge rounds to control cash burn and maintain enough cash runway to avoid raising a primary round until the capital-raising environment becomes more favorable.

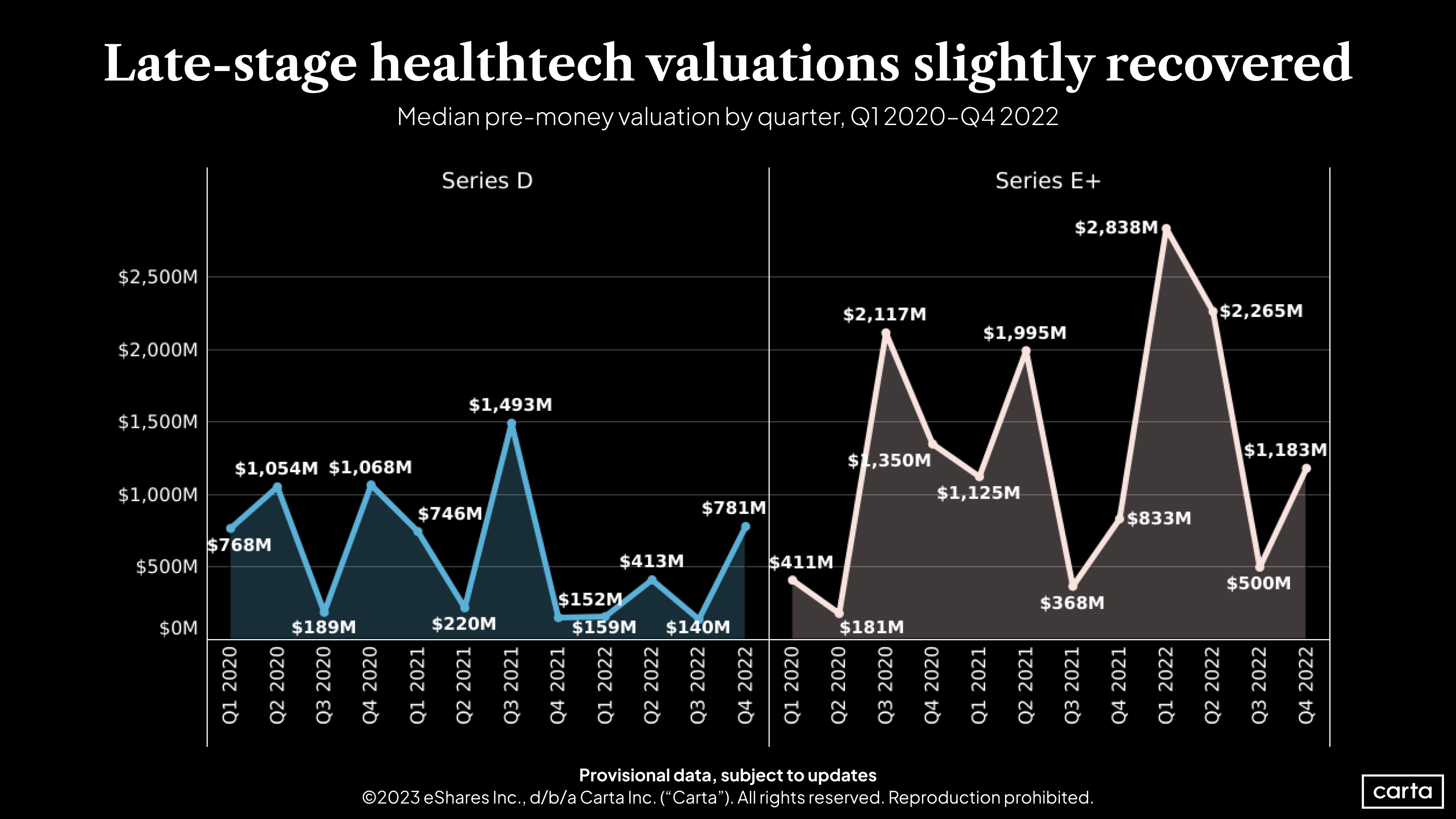

And it appears the dealmaking environment did improve late last year—slightly. Valuations rebounded at both the Series D and Series E+ stages, and VC investments in healthtech picked back up, albeit at a much smaller pace than any point in 2021.

What’s behind the Q4 uptick in healthtech?

A few factors combined to achieve the small uptick in healthtech venture financings:

Megadeals bounced back

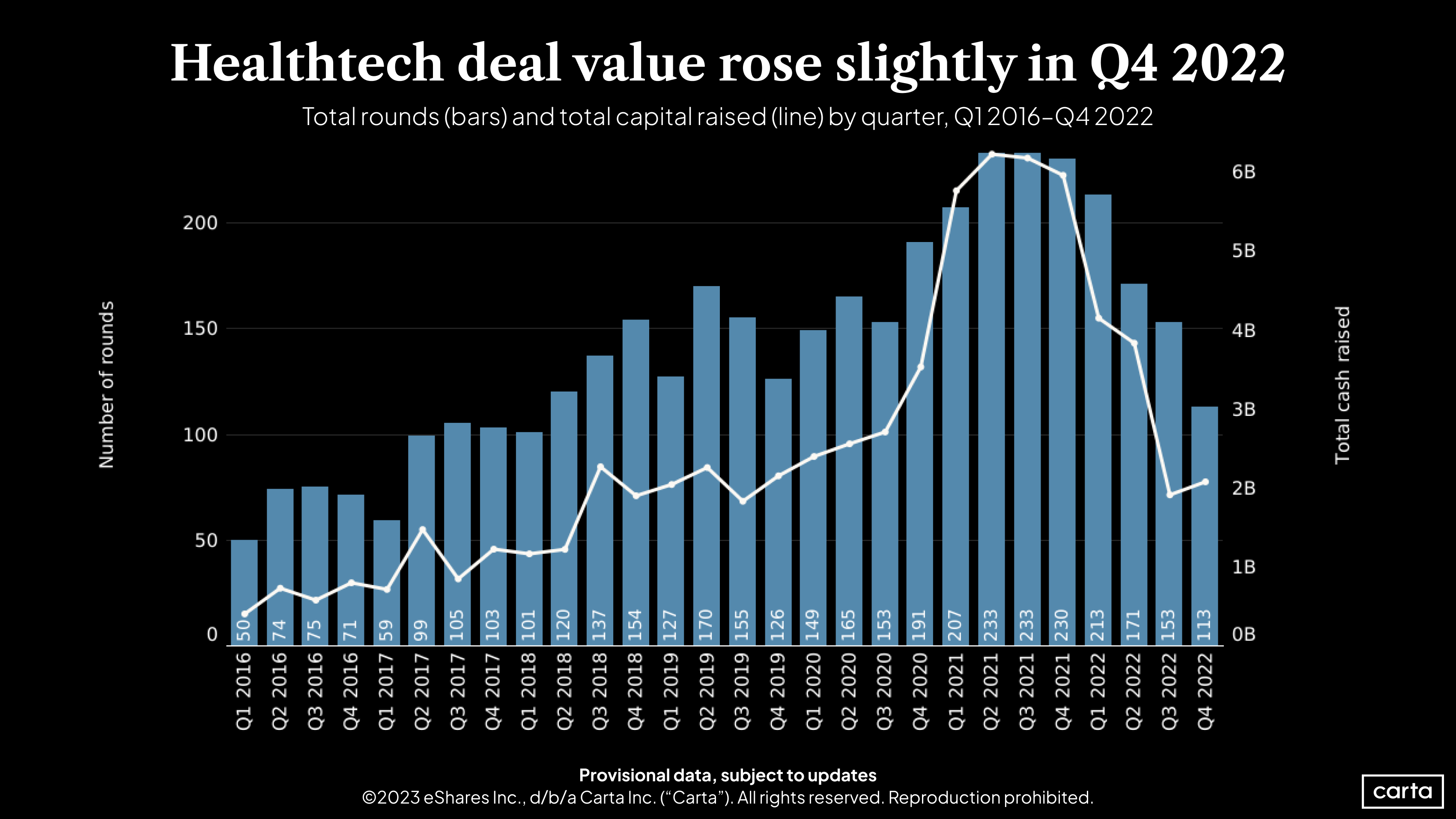

In Q4, 5% of healthtech rounds on the Carta platform were investments of $100 million or more, up from 1% in the previous quarter and matching the percentage in Q1, before dealmaking started to decline. That’s why we’re seeing an increase in total capital invested despite fewer deals—and it’s also why valuations are moving in the right direction for the deals that are getting done: In Q4, the median pre-money valuation for healthtech investments on Carta increased at every stage except for Series B and Series C. Series D led the increase, jumping 82%.

Public market resilience trickled down to growth-stage deals

The Nasdaq healthcare index (ticker symbol IXHC) outperformed the broader tech market over the final six months of 2022, jumping roughly 10% while the Nasdaq index dropped by some 5% during the same period. Why does it matter? Growth-stage company valuations and dealmaking are more closely tied to their public counterparts compared to early-stage startups. The resilience of the healthcare index may have given VCs confidence to continue their push into healthtech, especially at the later stages.

The healthcare industry still has tailwinds

Even when macroeconomic conditions are unfavorable, healthtech remains an attractive proposition for VC investors. Unlike fintech, SaaS, or crypto, healthtech has earned a reputation as a defensive industry to invest in—one where VCs can hedge against broader economic headwinds—because the industry serves basic human needs. An aging population is also driving the need for more healthcare solutions: The U.S. Department of Health and Human Services projects there will be approximately 81 million people 65 or older by 2040, more than double the total in 2000.

Healthtech is not totally immune from macro pressures, but so far, it’s shown greater resilience to the venture funding pullback than other sectors, in part due to the continued demand from providers trying to modernize the industry.

Learn more

Get weekly insights in your inbox

The Data Minute is Carta’s weekly newsletter for data insights into trends in venture capital. Sign up here:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. (“Carta”). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.