Throughout most of recent history, venture capital fund managers have tended to deploy more capital during the second year of a fund’s lifespan than in the first year.

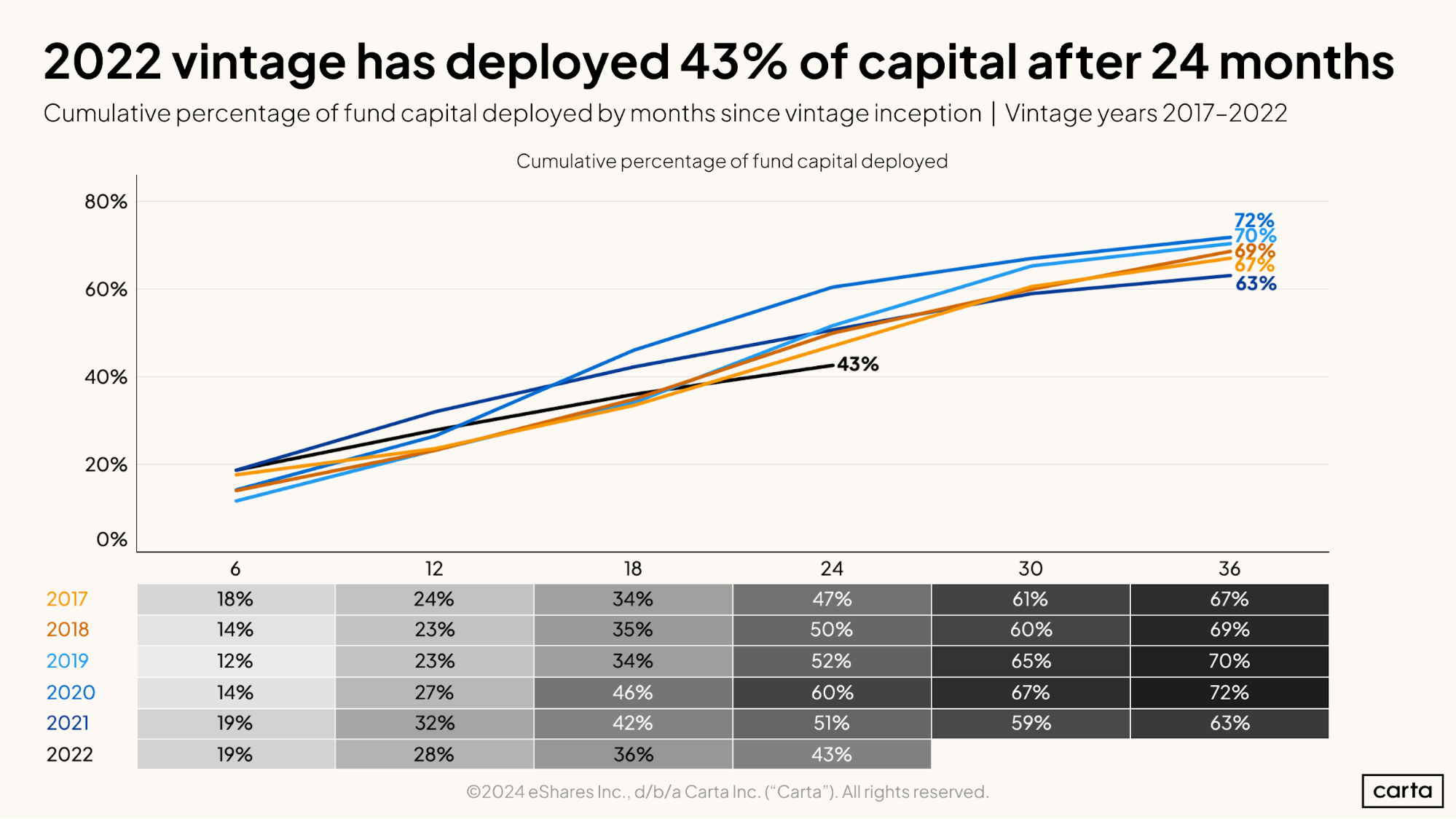

For instance, funds on Carta from the 2018 vintage deployed 23% of their available capital in their first year of existence and another 27% in the second year. Funds in the 2019 vintage deployed 23% of their cash in year one, then another 29% in year two. For the 2020 vintage, the deployment rate was 27% in the first year and 33% in the second year. In each of these three vintages, funds deployed at least half of their capital in the first two years.

The story of the 2022 vintage, however, is very different. After one year, funds that closed in 2022 were 28% deployed, in line with recent history. Yet in the second year—which roughly corresponds to the past 12 months, depending on the specific fund’s close date—managers of 2022 vintage funds spent just 15% of their available capital, leaving them 43% deployed after two years.

It was the slowest second year for fund deployments of any vintage dating back to 2017. No other year is within seven percentage points.

Because of this sophomore slump, the 2022 vintage is now trailing all of its recent predecessors when it comes to the rate of capital deployment after 24 months. Framed from a slightly different perspective: After two years of existence, the 2022 fund vintage retains a higher percentage of its dry powder than any other vintage in recent history.

Symptoms of a slower market

At least in part, this change in deployment speed during a fund’s early days is likely a response to shifts in the broader venture market. Venture-backed valuations have trended down since the bull market’s peak in 2021. It’s grown more difficult for companies to find attractive exits. And deal counts have declined across all venture stages.

Funds that closed in 2022 aren’t the only ones that have deployed capital more slowly in the past year. As shown in the chart above, the amount of capital deployed by funds in the 2021 vintage went from 51% after 24 months to 63% after 36 months, an increase of just 12% during the period that roughly corresponds to the past 12 months. That’s less activity than we typically see in the third year. Funds in the 2017 vintage, for instance, invested about 20% of their total capital in the third year.

Why have deal counts declined and deployments slowed? Investors say that the biggest reason is a shift in their own expectations. As valuations declined and exits grew harder to find, some companies that might have easily raised funding in 2021 no longer looked so attractive. VCs grew more selective about their investments, asking for higher revenue totals and clearer paths to profitability. This increased selectivity leads to a slower pace of deals.

Investors believe that recent fund vintages might eventually produce stellar returns. But that performance is about quality, not quantity.

The difference between the 2017 vintage deploying 20% of its capital in year three and the 2022 vintage deploying 12% might not seem enormous. But in an industry where consistency and predictability are valued traits, it signals a notable shift in spending habits across the VC landscape.

“When you raise a fund, you tell your LPs what you think that deployment period is going to look like, and you try to stay consistent to it,” says Aziz Gilani, managing director at Mercury, an early-stage firm that closed its fifth flagship fund last year with $160 million in commitments. “As veteran players in this space, we all understand it’s an industry that goes up and down. Our job is to maintain consistency in deployment and not get too phased by the gyrations of the market.”

Short-term shifts, long-term thinking

While fund managers do try to stick to their plans, they also have to play the cards they’re dealt. Gilani says that he would never write a check just to meet a certain deal quota that he had communicated to LPs. He also wouldn’t pass on an attractive investment solely because his fund was deploying capital more quickly than expected. To at least some degree, all VCs react to market conditions.

We can see some of this reactivity in the data. For the 2020 fund vintage, the period between 12 months and 24 months of existence overlaps with the high point of the venture market in late 2021. Over that span, the 2020 vintage went from 27% deployed to 60% deployed, spending about one-third of its available capital in just a year. That’s the fastest rate of deployment over any 12-month stretch for any vintage shown above.

“I’ve heard anecdotally—and it seems like the data supports this—that when there was a ton of liquidity in the market, some folks accelerated their deployment cycles,” Gilani says. “And look, that might seem like a rational approach to take, right? I’m generating all this liquidity, so I should deploy faster to take advantage of the window.”

But in Gilani’s view, that line of thinking is incomplete. An early-stage venture fund operates on a long lifespan, often around 10 years. It can take a long time for a single portfolio company to go from investment to exit—long enough for the exit market to go from red hot to ice cold, as it has in recent years. Or, long enough for it to heat back up again.

Plus, ramping up deployments when valuations are on the rise runs afoul of investing’s one inescapable maxim: buy low, sell high. There’s a reason that, historically, some of the best performing VC fund vintages have occurred in the immediate aftermath of market downturns.

Instead of redirecting their deployment strategy in recent years to account for the latest macro trends, Gilani and his colleagues have tried to stay the course.

“I guess we took a more conservative approach,” Gilani says. “Knowing that our hold times are five to seven years, you don’t want to be thinking about deployment based on what the current liquidity environment looks like. Because whatever market we’re in right now, it’s going to look completely different in five years.”

Get the latest data

Sign up for the Carta Data Minute newsletter to receive the latest data on VC financings, valuations, compensation, and more:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2024 eShares, Inc. dba Carta, Inc. ("Carta"). All rights reserved. Reproduction prohibited.