Executive Summary

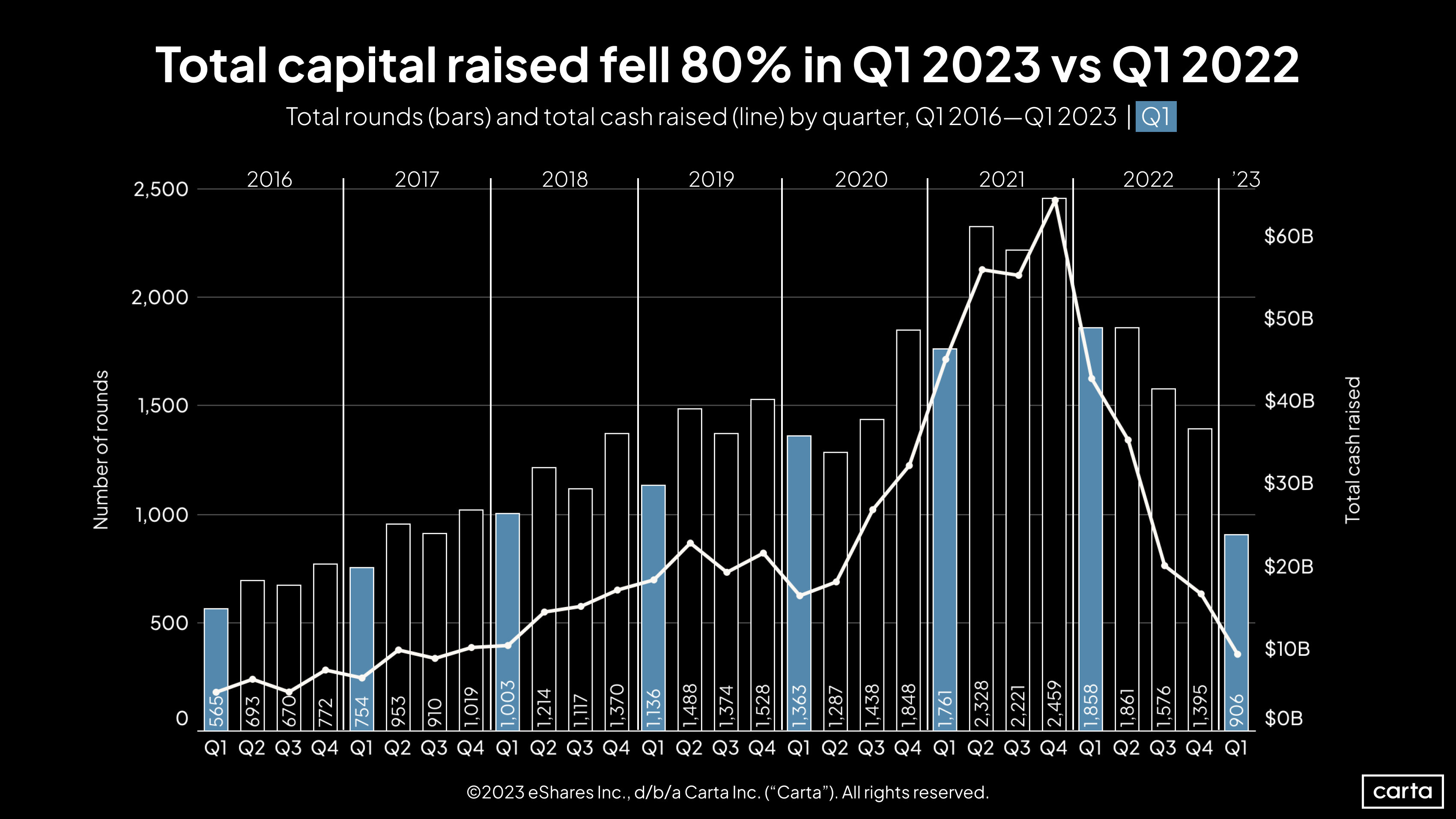

The transformation of the venture capital industry over the past year has been stark. Total venture capital raised by startups plunged 80% from Q1 2022 to Q1 2023. Venture deal count fell 45% over the same span. Overall, Q1 was the slowest quarter for both capital raised and deal count since 2017.

There are signs of a venture spring. Valuations from seed to Series C ticked up from recent lows. Median round sizes mostly stabilized. But these green shoots were overwhelmed by the decline in total rounds across all stages.

Other Q1 highlights

-

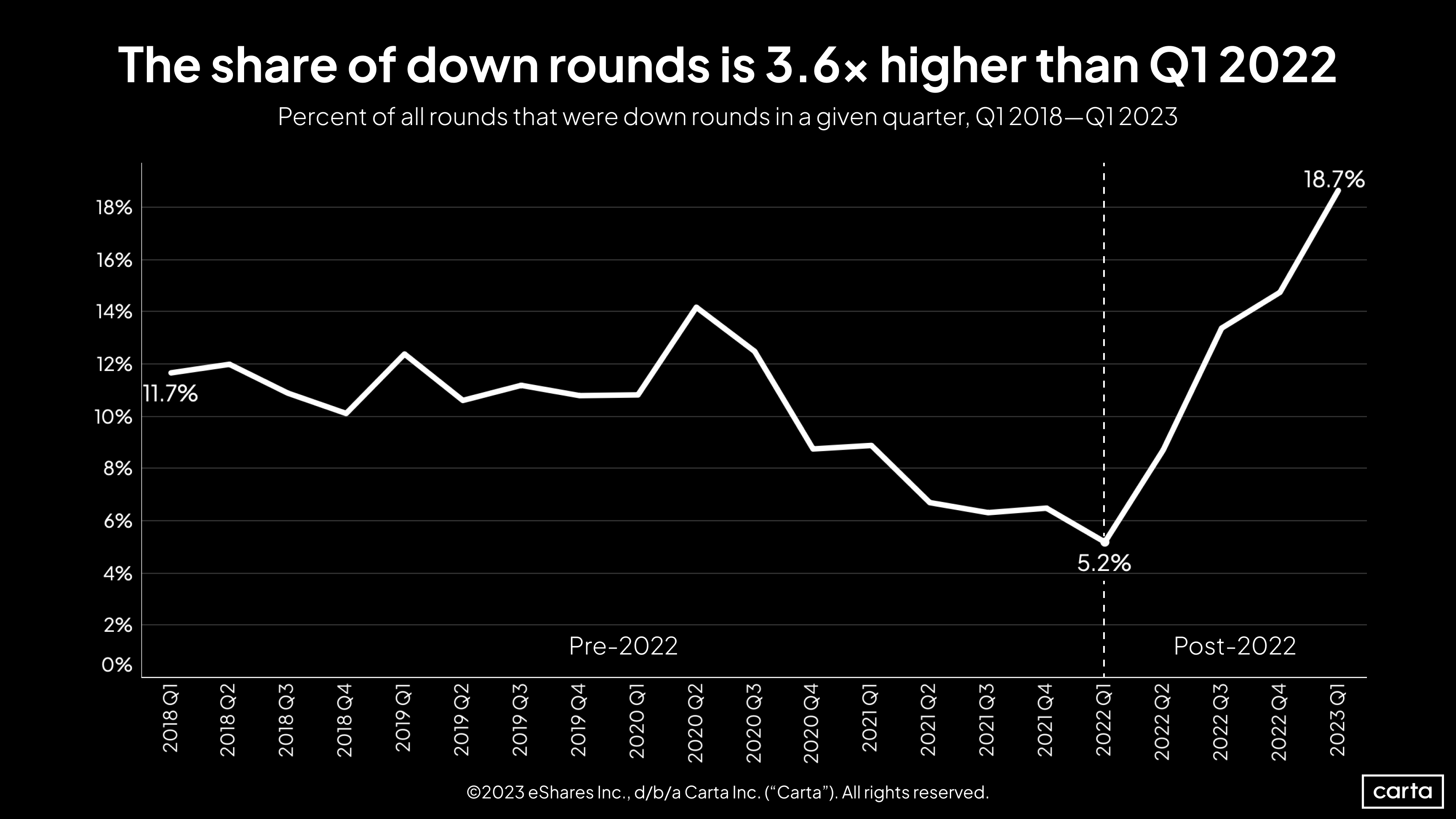

Down rounds spiked in frequency: Just shy of 20% of all venture investments in Q1 were down rounds, the highest proportion since at least 2018. A year ago, barely 5% of venture deals resulted in a reduced valuation. With median valuations having fallen so far from recent highs, many companies seeking a valuation increase are battling against the current.

-

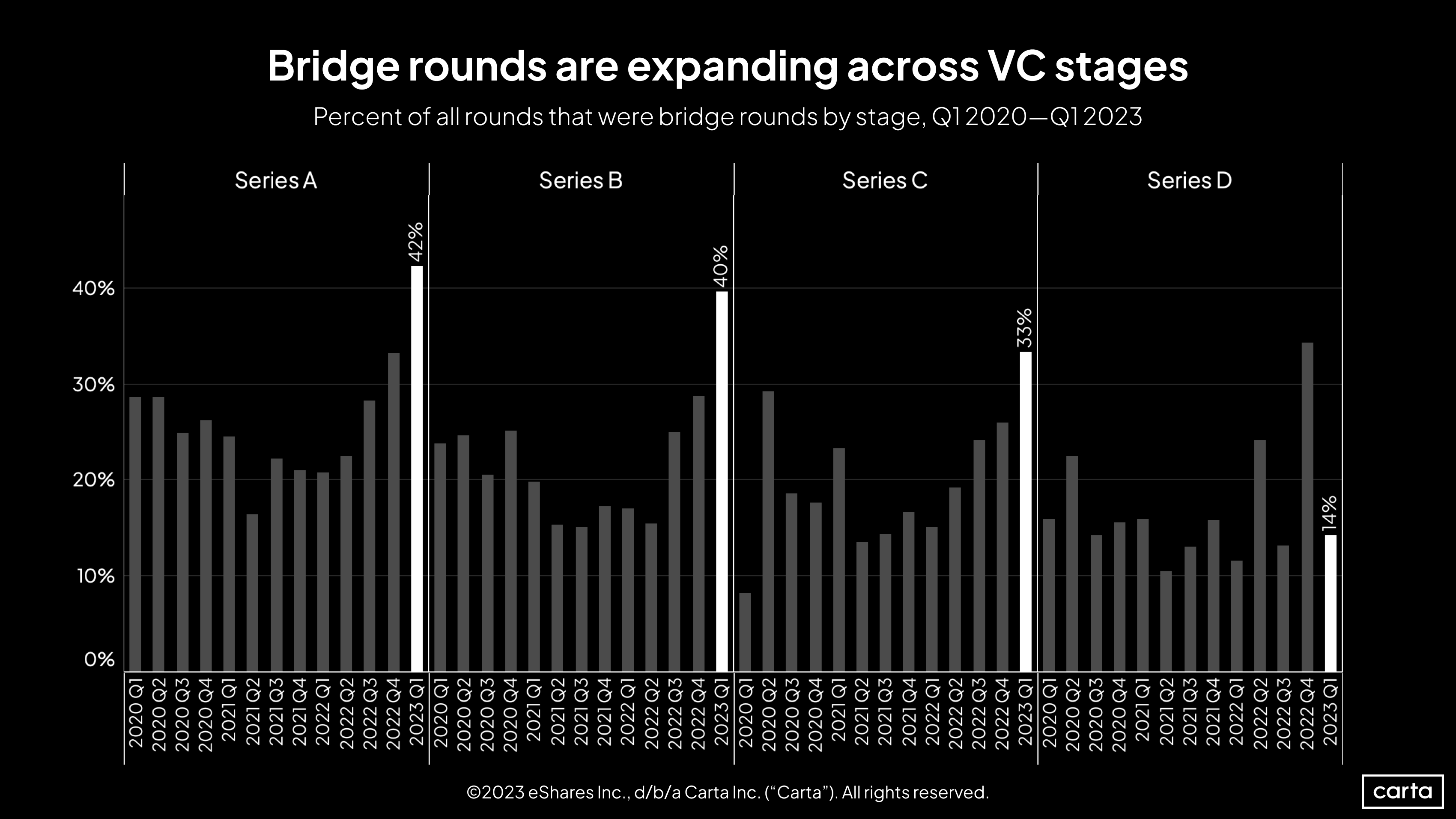

More companies chose bridge rounds: For companies ranging from Series A to Series C, bridge rounds have emerged as an increasingly attractive option. At least 40% of all investments in Series A and Series B companies were bridge rounds in Q1, the highest figures of the 2020s.

-

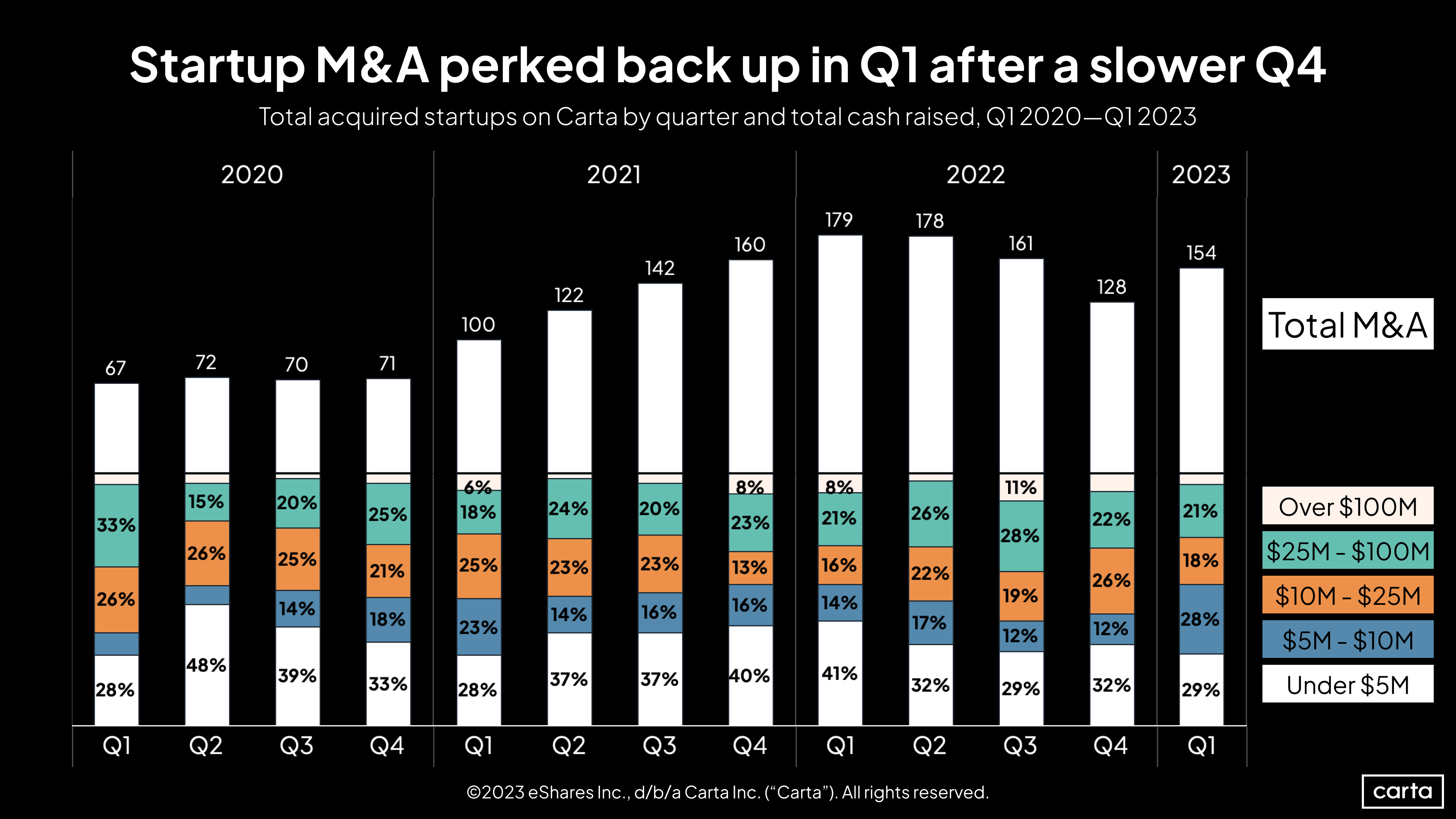

Startup M&A bounced back: The number of venture-backed companies that were acquired or merged with another company increased by 20% in Q1 compared to Q4 2022, with 57% of those M&A deals valued at $10 million or less. In a challenging environment for raising new venture capital, some smaller startups are instead opting for an exit.

Note: If you’re looking for more industry-specific data, you can also download the addendum to this report to get an extended dataset.

Key trends

What a difference a year makes. There were fewer investments and less capital raised by startups on Carta in Q1 2023 than in any first quarter since 2017—a sharp contrast to Q1 2022, which saw more deals and the second-highest total capital raised of any Q1 in recent history.

After several years of steady growth, the venture market is on pace for a second straight year of declines. Across all stages, Carta logged 906 venture capital investments in Q1, ending a streak of 21 consecutive quarters in which deal count had reached at least 1,000. That’s a 35% decline from Q4 2022, the largest quarter-over-quarter dip since at least 2016.

Nearly one in five venture rounds raised in Q1 came at a lower valuation than the company’s previous round. That figure is 3.6x higher than a year ago, and it’s far and away the highest rate of the past five years.

The recent spike is due in part to the fact that valuations have continued to decline across most stages of the startup lifecycle. But it’s also due to the fact that valuations have remained depressed for several consecutive quarters. Some companies that had delayed new fundraisings in hopes of avoiding a down round are nearing the end of their financial runways and have decided that a lower valuation is a lesser evil than running out of cash.

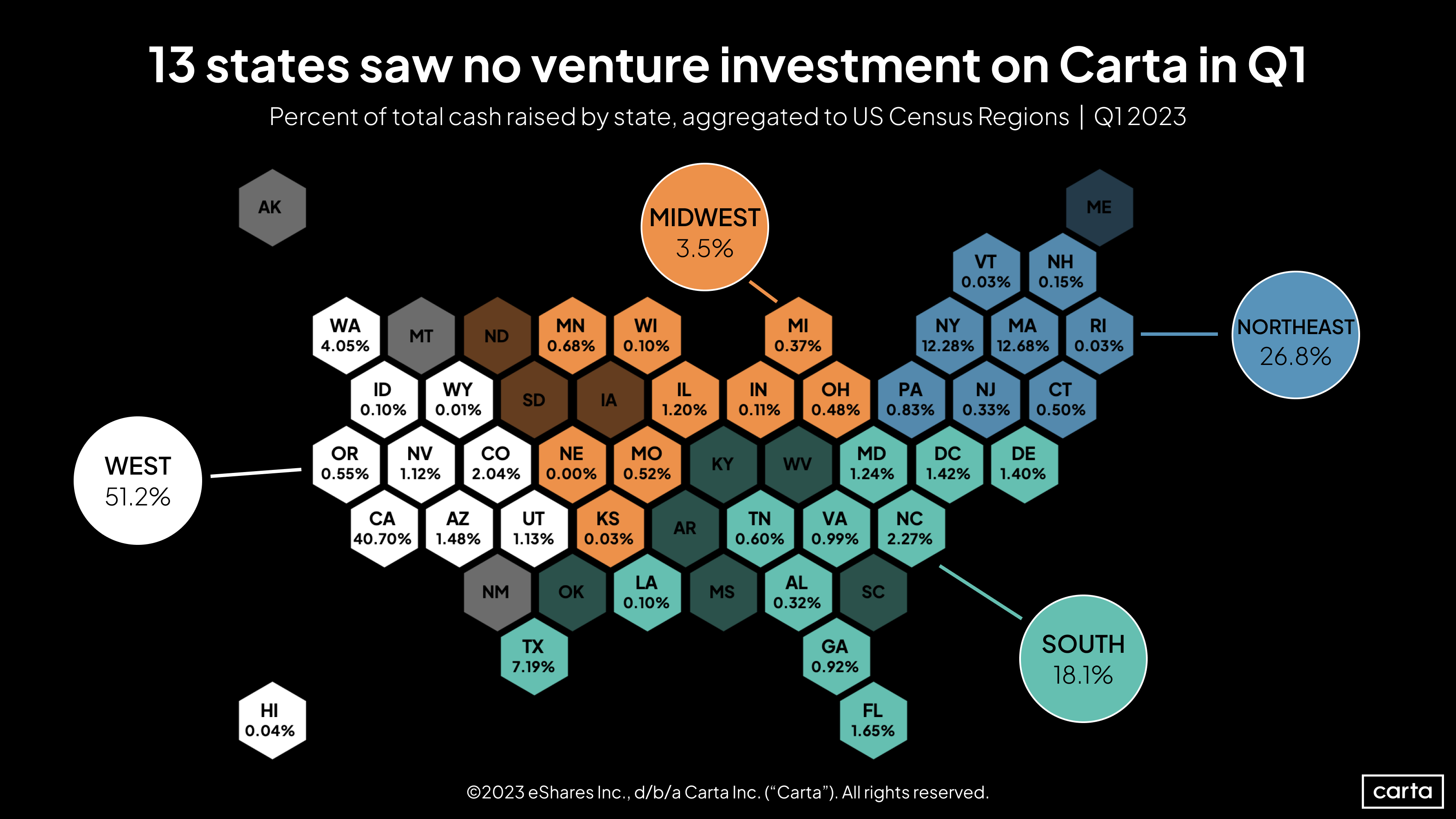

There was no venture capital activity to speak of in more than a quarter of the 50 states during Q1. That’s a notable shift from Q1 2022, when all but four states hosted at least one venture deal.

Compared to recent history, the investments that did get done were more tilted to the eastern half of the country than in past quarters. A combined 44.9% of activity was in the South and Northeast regions, up from an even 40% over the course of 2022.

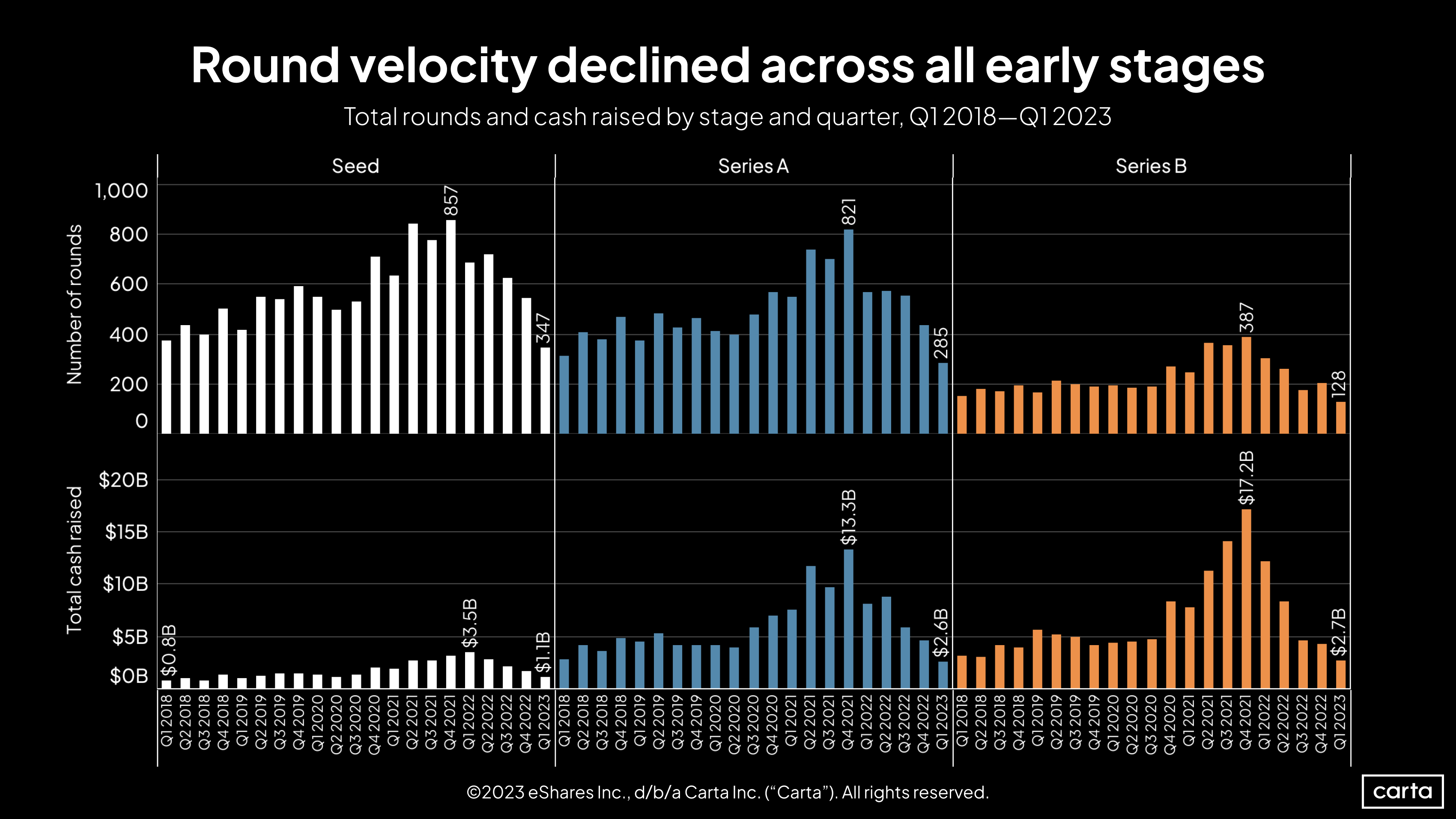

Both round count and capital raised have fallen off significantly at seed, Series A and Series B. Last quarter’s total seed capital raised of $1.1 billion is down 68% from the recent quarterly high, which is actually the smallest decline of any of the three early stages. Series B activity had shown signs of plateauing in Q4 2022, but round count and capital raised both fell again in Q1.

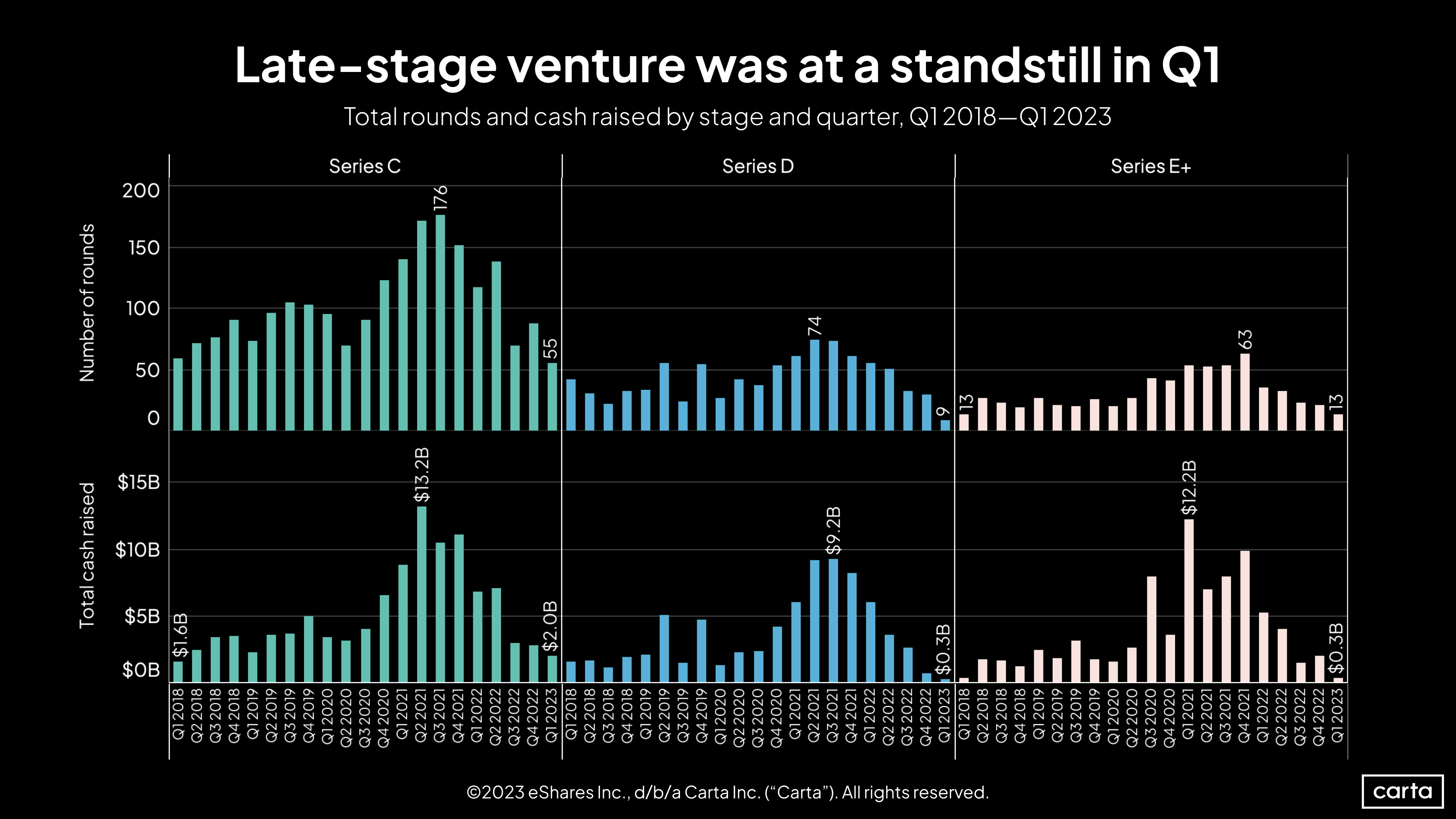

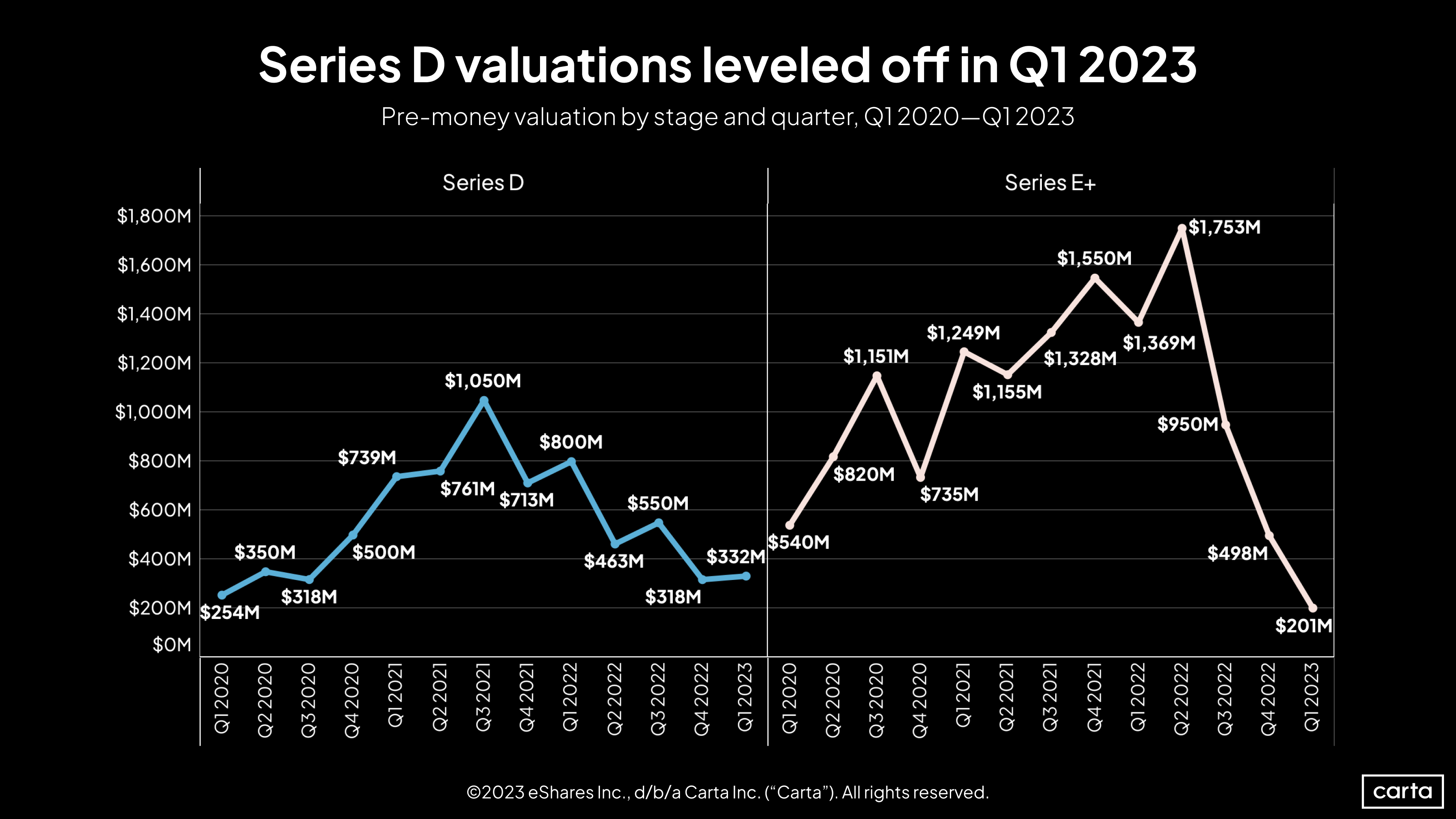

There were fewer than 15 investments and less than $500 million in capital raised at both Series D and Series E+ in Q1, easily the lowest totals of the past few years.

Lower deal counts at later stages make it difficult to draw broad conclusions from other aspects of the data. The relative scarcity of these deals might be the more important late-stage takeaway than any trends related to valuation and deal size.

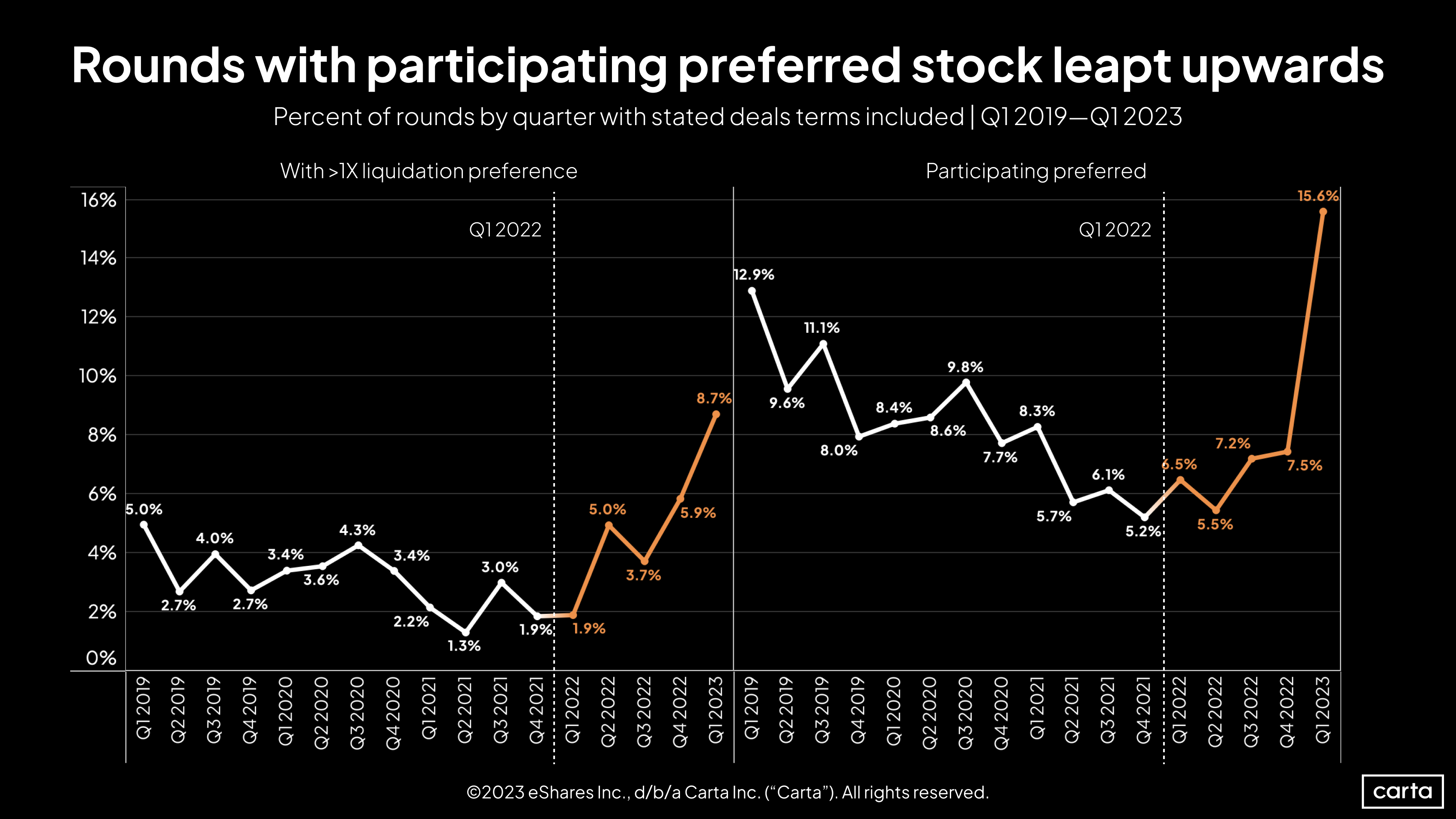

Q1 saw a serious spike in the frequency of VCs receiving both participating preferred stock and attractive liquidation preferences in their startup investments, a sign that the market is continuing to grow more investor-friendly. Participating preferred stock and liquidation preferences greater than 1x are both types of deal terms that guarantee investors a certain return in the event of a liquidation or sale.

These sorts of terms had grown slightly more common in 2022, but their growth in popularity in Q1 was a different phenomenon. With fewer deals and dollars to go around, investors are using their leverage in negotiation to improve their positions.

Fundraising & valuations

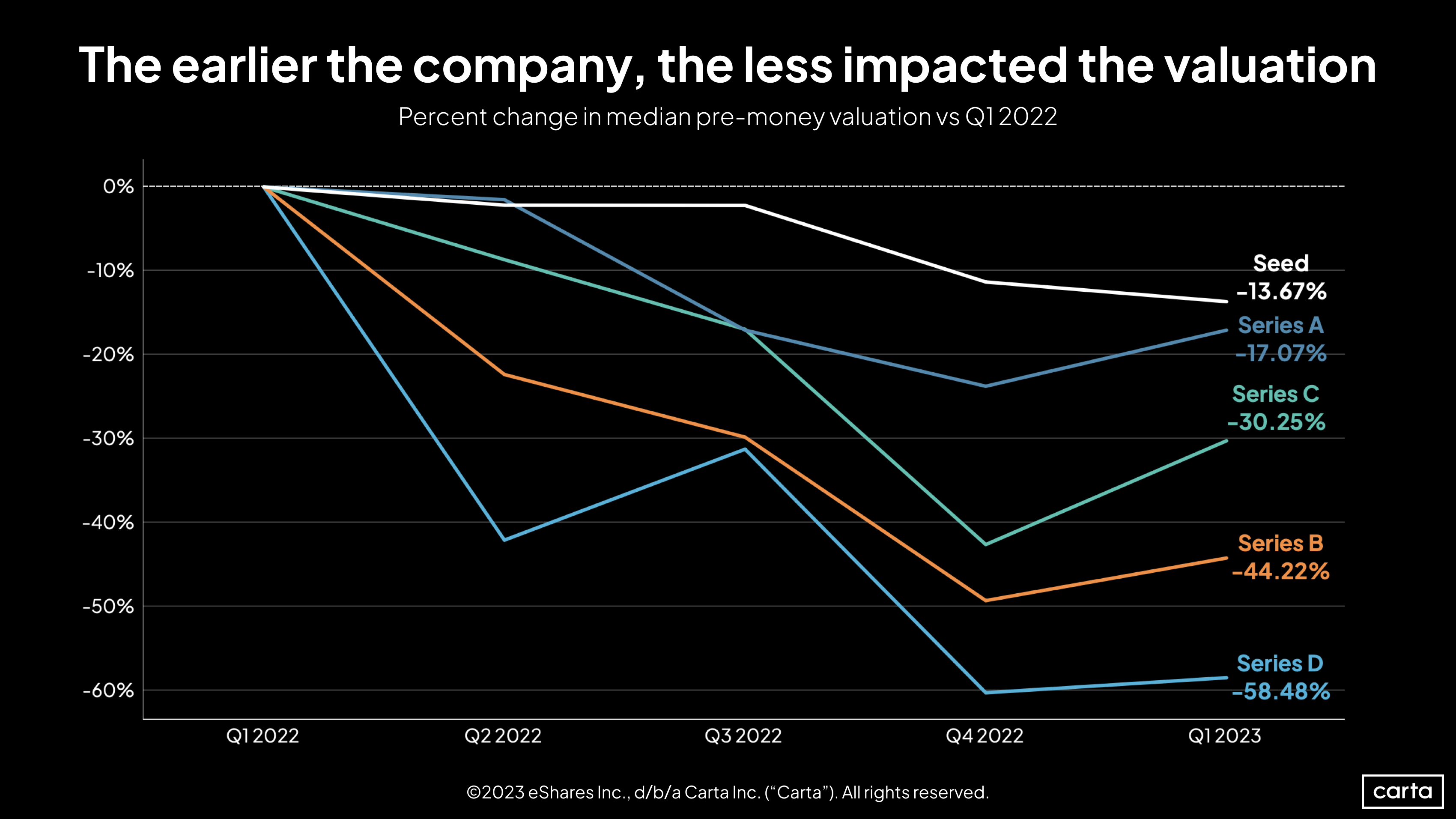

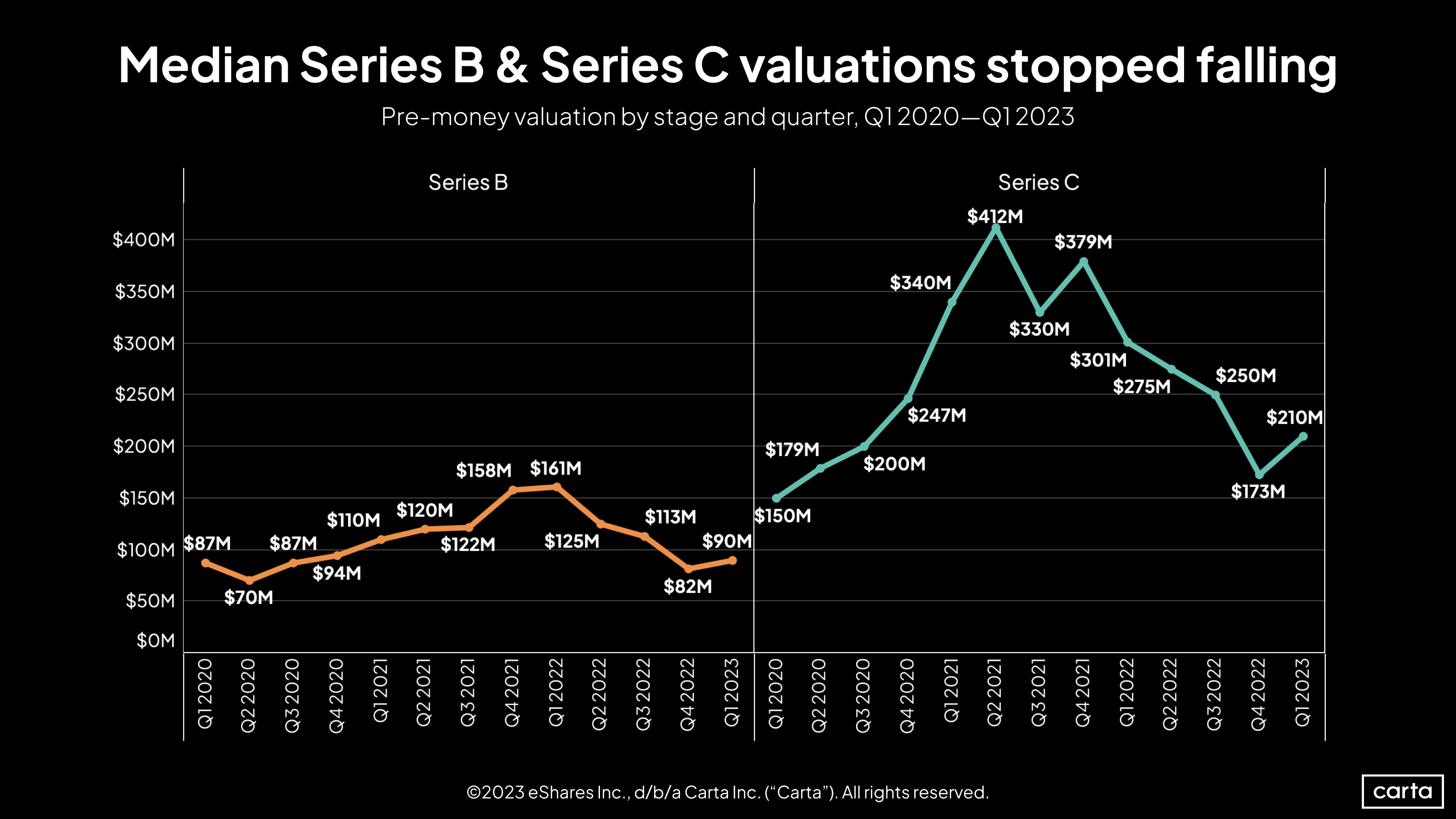

Median pre-money valuations have fallen at every stage over the past year, but that fall has generally been steeper at the later stages of the startup lifecycle. The exception is Series B, where valuations are down 44.22% from a year ago, a notably larger drop than the 30.25% falloff at Series C.

As you can see, however, valuations increased slightly or held steady at most stages during Q1. It’s far from certain, but there are indications that the valuation environment has settled at some stages after more than a year of volatility.

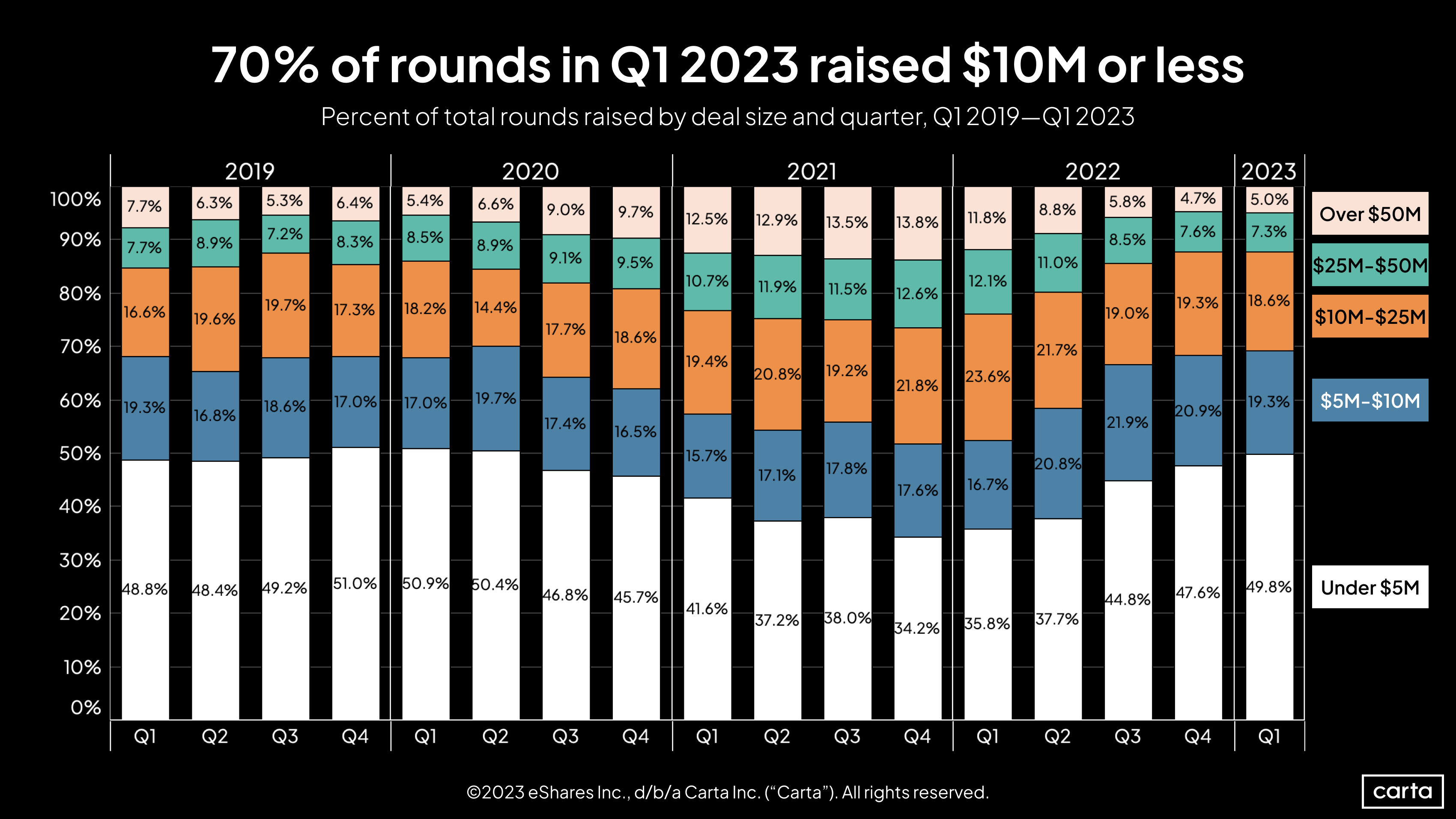

Just shy of 70% of all venture rounds raised in Q1 were $10 million or smaller, the highest rate since Q2 2020, immediately after the onset of the pandemic. In an environment of reduced valuations, it makes sense that smaller rounds have proliferated.

On the other end of the spectrum, the percentage of deals larger than $50 million ticked up slightly in Q1, the first increase in the past five quarters. As in other segments of the startup landscape, Q1’s results here look quite different from the numbers of 2021’s bull market, but not far off the pre-pandemic environment of 2019.

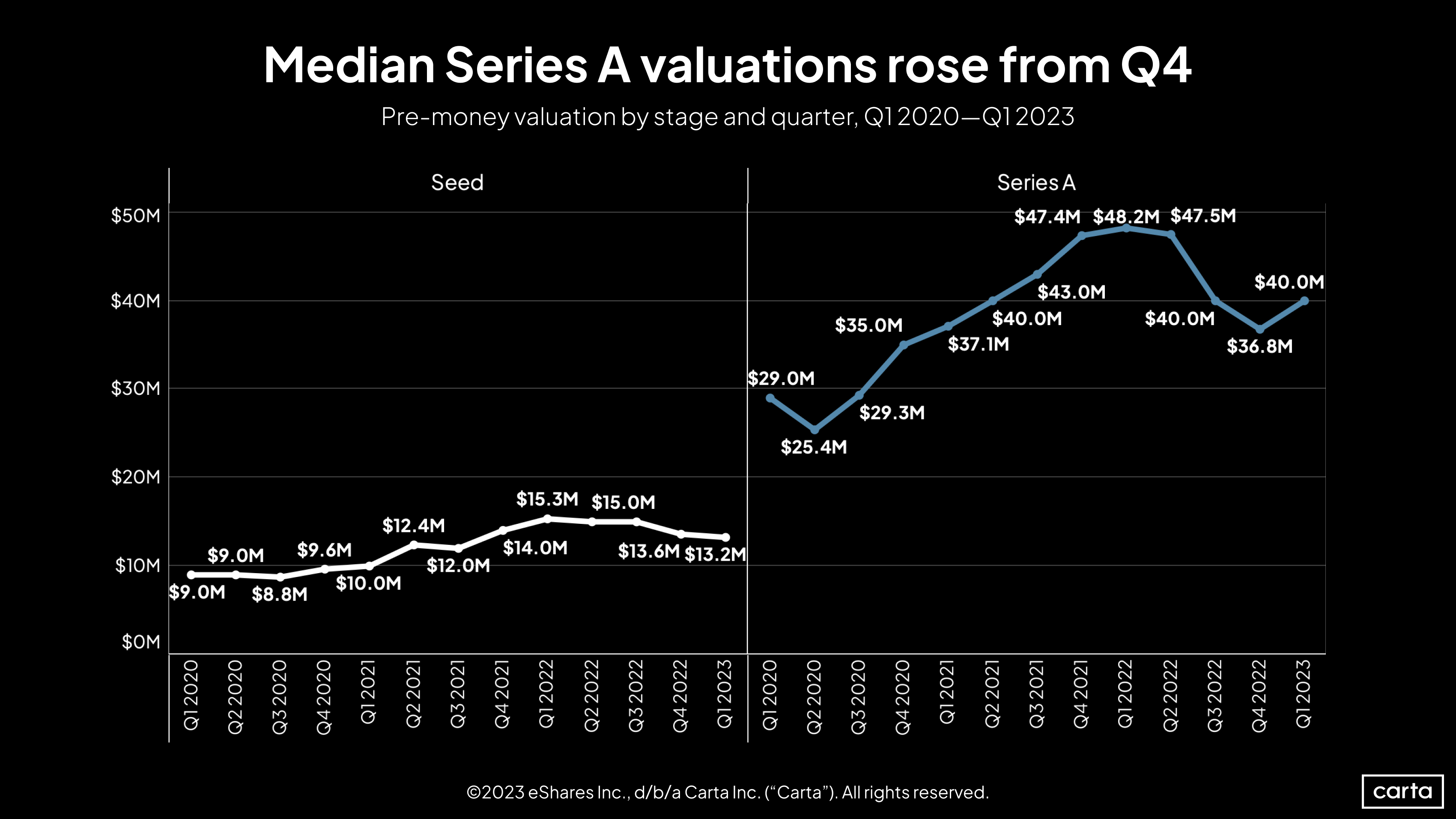

The median Series A valuation returned to $40 million in Q1, ending three straight quarters of declines. Year over year, the median Series A valuation is now down 19%, compared to the 47% drop in median Series A round size.

Seed valuations continued to slide, with the median falling to its lowest point since 2021. Still, seed valuations remain well above 2020 levels.

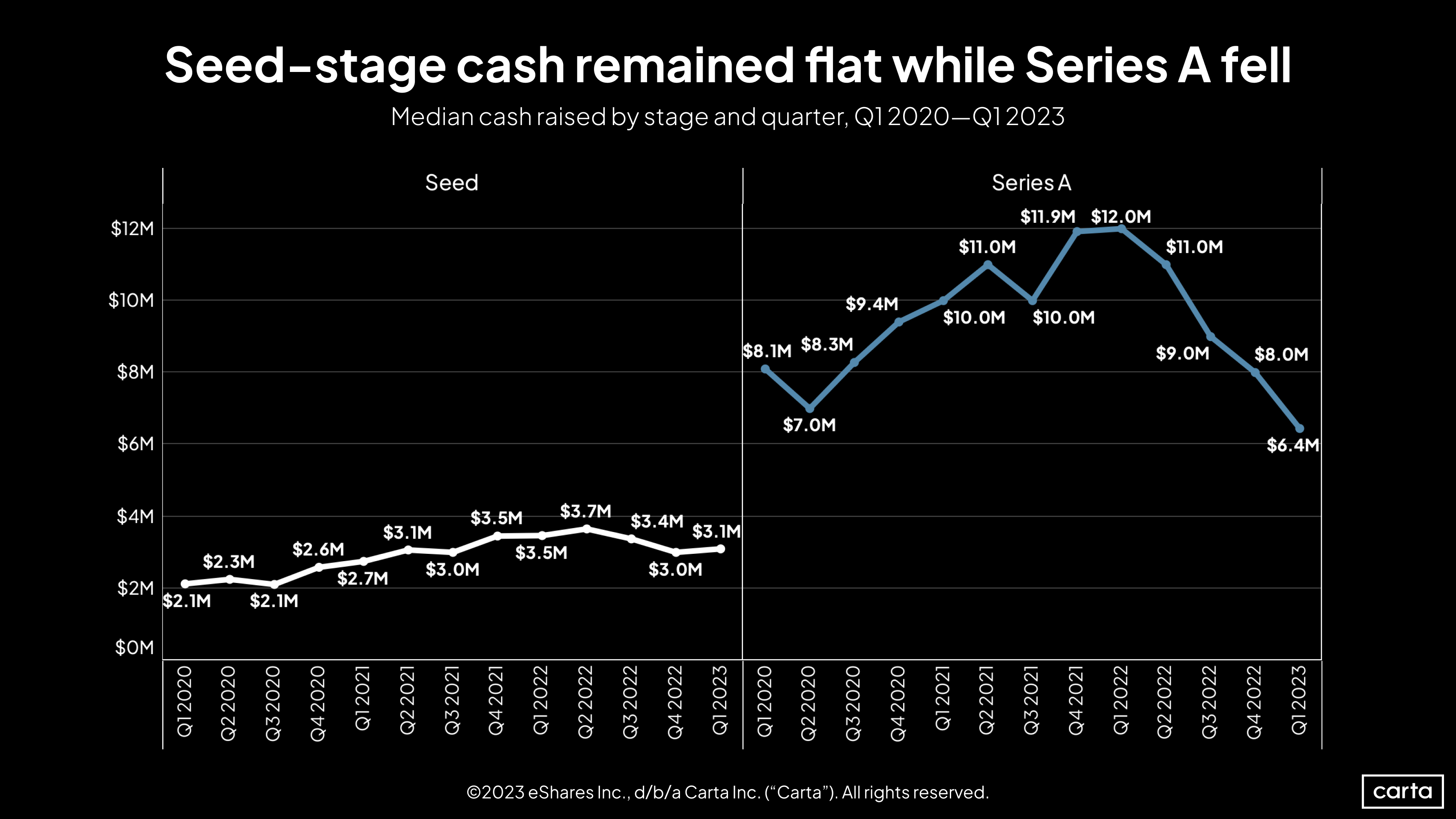

The median seed round ticked up slightly in Q1, reversing a recent trend of declines. The median Series A, however, sank to $6.4 million, its lowest point since at least the start of 2020. This marks four consecutive quarterly declines for median Series A size.

The difference between these two early stages amid the ongoing venture downturn is growing more stark. The median seed round is down 11% year over year, while the median Series A has fallen by 47% over that same span. Compared to three years ago, in Q1 2020, the median seed round has grown by 48%, and the median Series A has shrunk by 21%.

The median Series B pre-money valuation was up nearly 10% in Q1, while the median Series C was up 21%. Both of those are the largest quarterly increases at their respective stages since Q4 2021.

Both are also still down significantly year over year, and they’re paired with declining deal counts, which could temper some optimism. But after several straight quarters of declines, these upticks are still a welcome sign for founders who might be seeking to raise capital at these middle stages in the quarters to come.

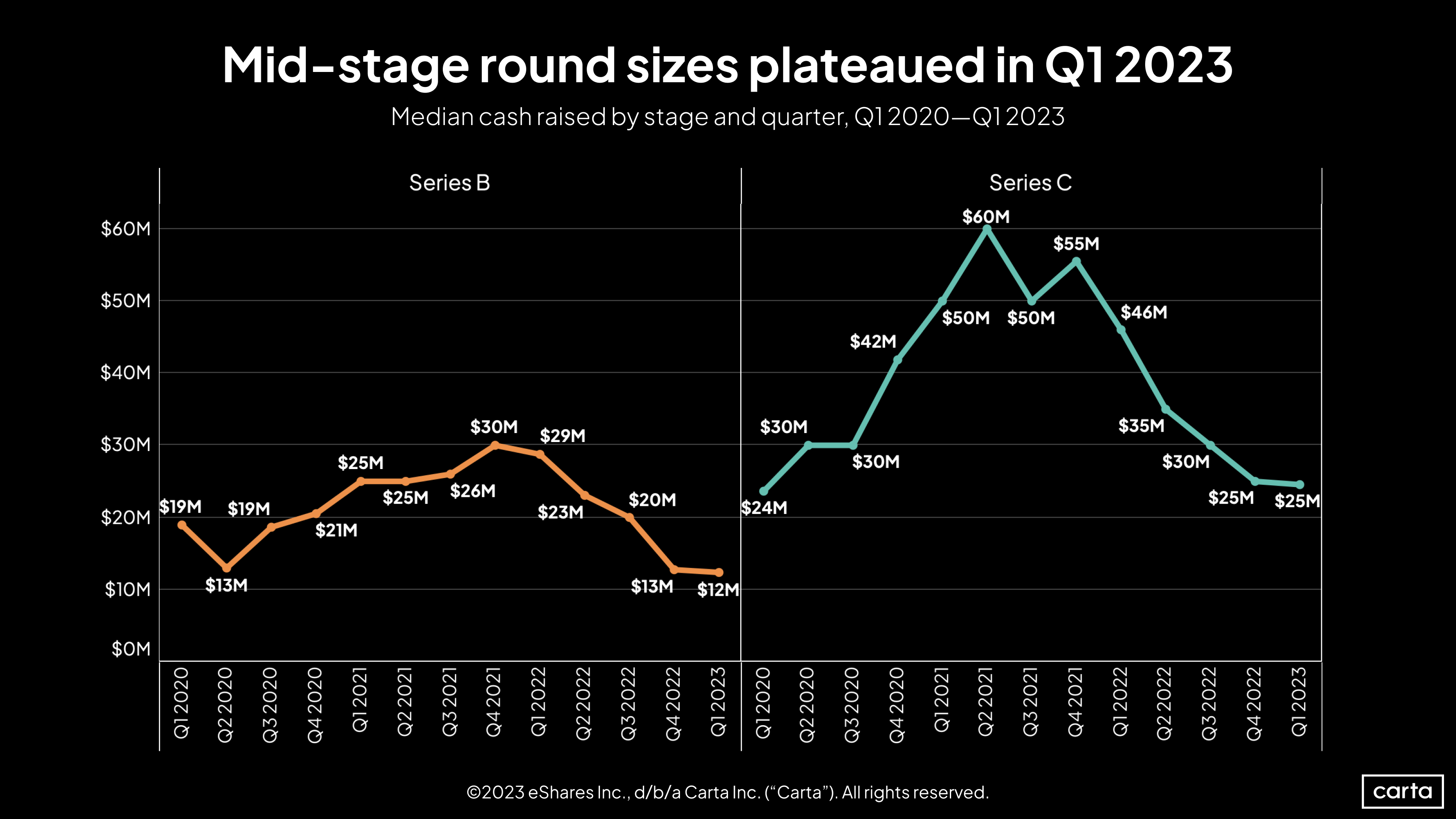

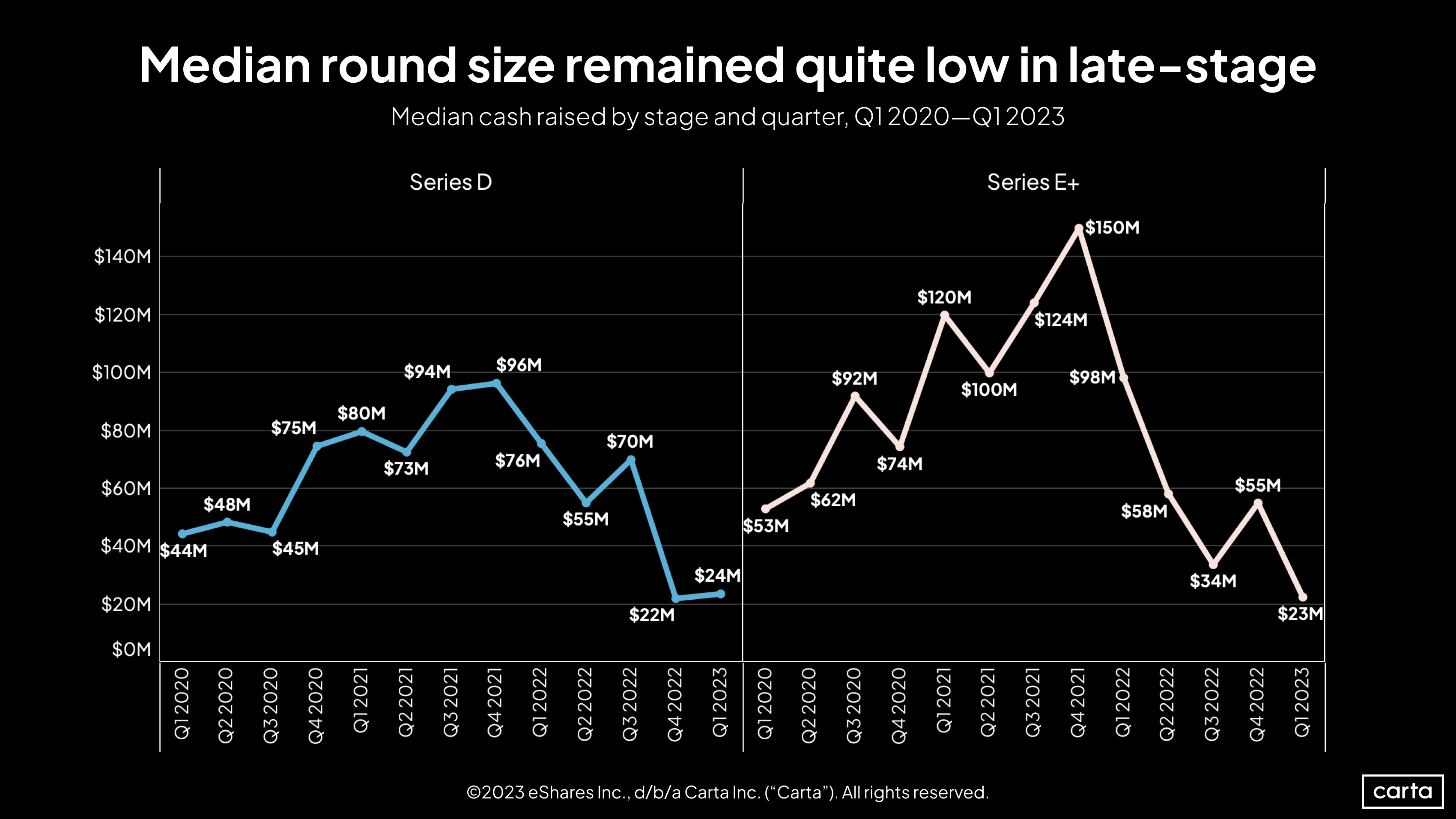

Round sizes got slightly smaller at Series B and stayed level at Series C, with the Series B median at falling to its lowest point so far this decade. However, the median Series B slipped by just $1 million from the prior quarter, which could be a sign that the recent slide at that stage is ending.

The median pre-money valuation inched up slightly at Series D in Q1, just as it did at Series B and Series C. Valuations at Series E+, meanwhile, continued to plummet from 2021’s highs. However, the relatively low number of deals at Series D and beyond means that Q1 medians are based on a smaller statistical sample.

Last quarter’s recovery in the median deal size at Series E and beyond proved ephemeral: That figure sank back to $23 million in Q1, its lowest point in the past three years.

The median Series D round was smaller than the median Series C for the second straight quarter, a rare inversion that demonstrates just how difficult fundraising has been at later stages. The median Series D is down 68% year over year.

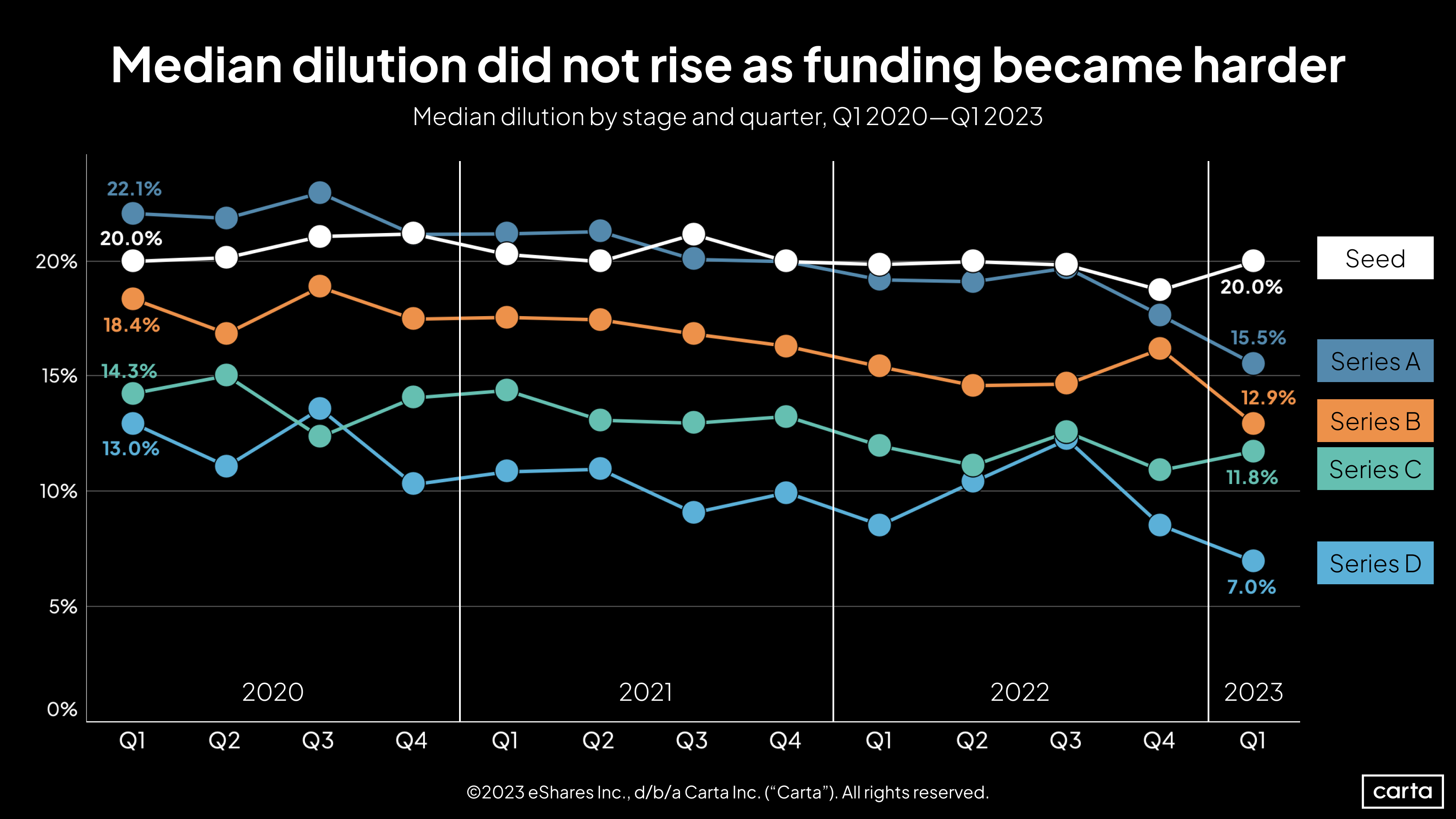

The median dilution in venture deals declined at Series A, Series B, and Series D, signaling that founders were giving up smaller portions of their companies in venture deals at these stages during Q1. This continues an overarching trend over the past few years. Dilution has declined at every stage of the startup lifecycle since the start of 2020, in some cases significantly—median Series A dilution, for instance, is down 30%.

In a time of market upheaval, many startups are coming to an impasse. And a growing number are choosing to cross it with a bridge. At least 40% of all new fundings at both Series A and Series B were bridge rounds in Q1, which in the case of Series B is more than double the rate of a year ago.

This increase in bridge rounds surely plays some role in the decrease in priced venture rounds that we covered earlier. In a lower-valuation environment, many companies are opting for unpriced bridge rounds instead of a new priced funding that could come with a lower valuation.

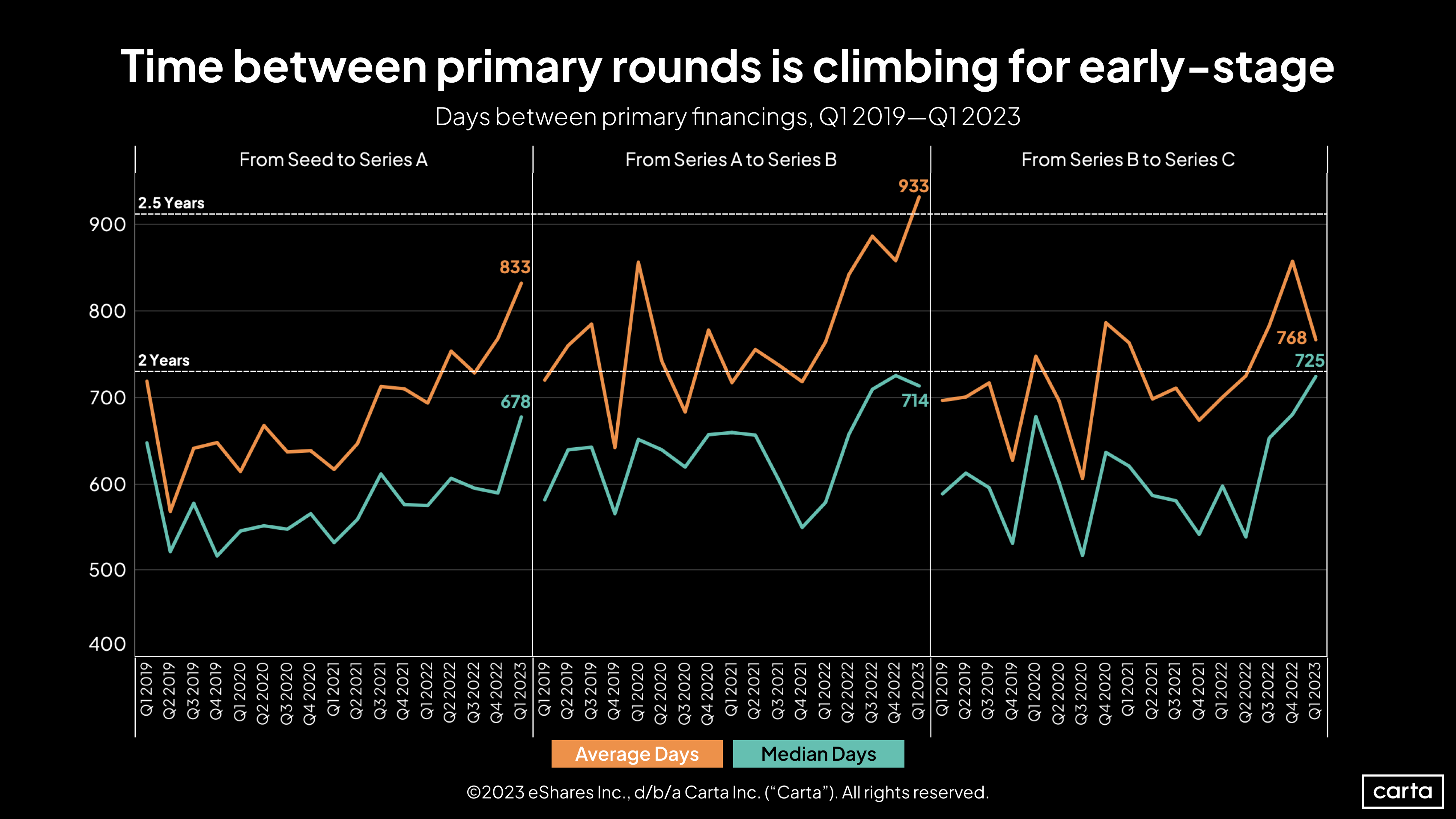

For startups, a longer wait between primary rounds requires more financial runway. At every stage, both average and median wait times have been generally trending up in recent years. But there were some signs of a shift in Q1. The median time between a Series A and Series B ticked down slightly, while the average time between a Series B and Series C declined for the first time in months.

The number of venture-backed startups that were acquired through M&A increased by 20% in Q1, the largest quarter-over-quarter uptick since Q2 2021. There were few megadeals, however, and most transactions—about 57%—were $10 million or less.

That increase runs counter to trends in the broader M&A market, which experienced its worst dealmaking quarter in more than a decade. Different factors are at work in the venture market, where smaller startups can quickly run low on cash reserves. If some of those startups are struggling to raise new venture capital, a merger or acquisition might be an appealing alternative, which could make them more motivated sellers than the rest of the M&A market.

Employee equity & movement

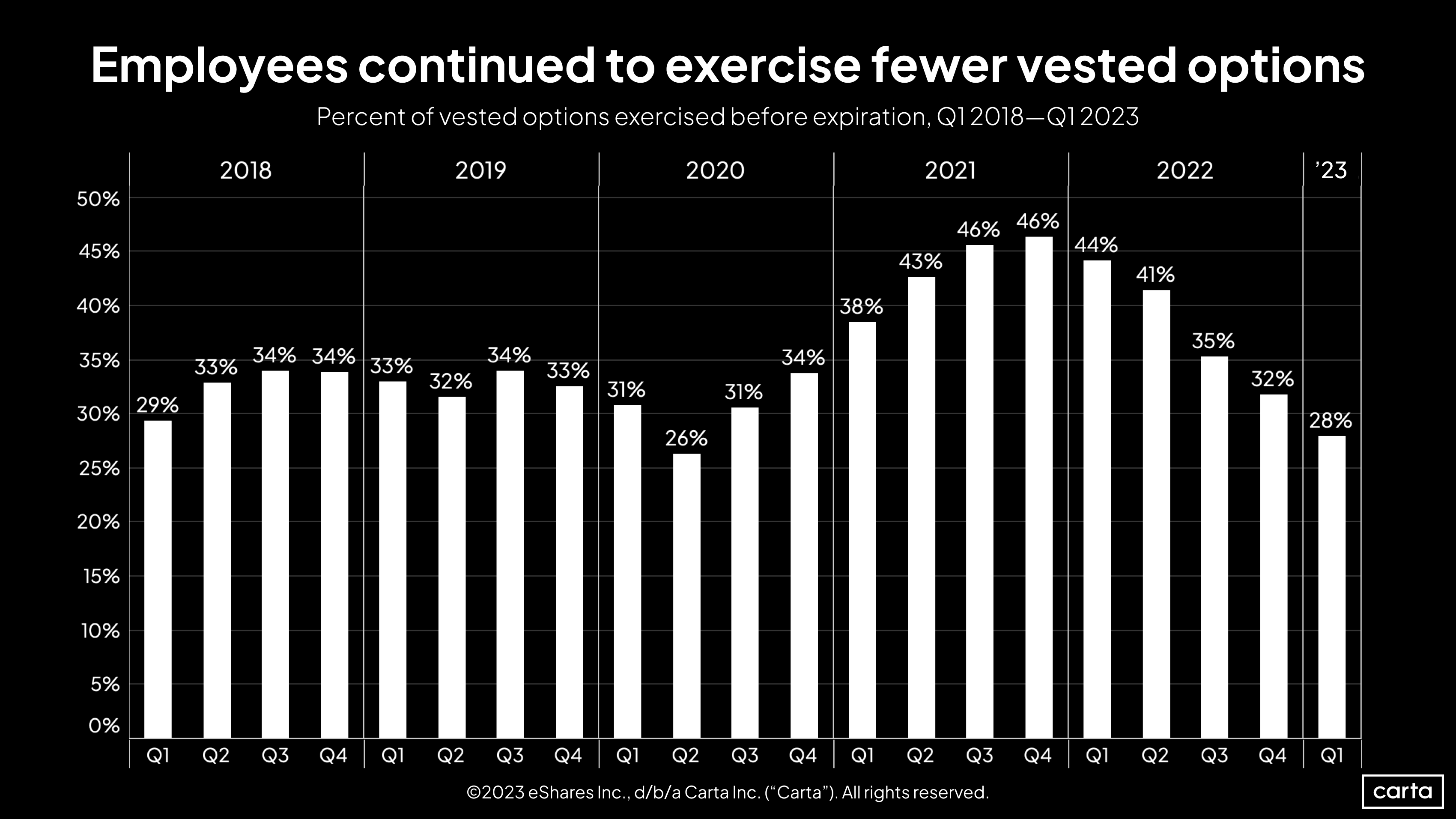

The percentage of employees who exercised their vested options before expiration has now declined for five straight quarters, with the rate falling from 46% to 28% over that span. Last quarter saw the second-lowest rate of exercised options since the start of 2018, trailing only the early pandemic days of Q2 2020.

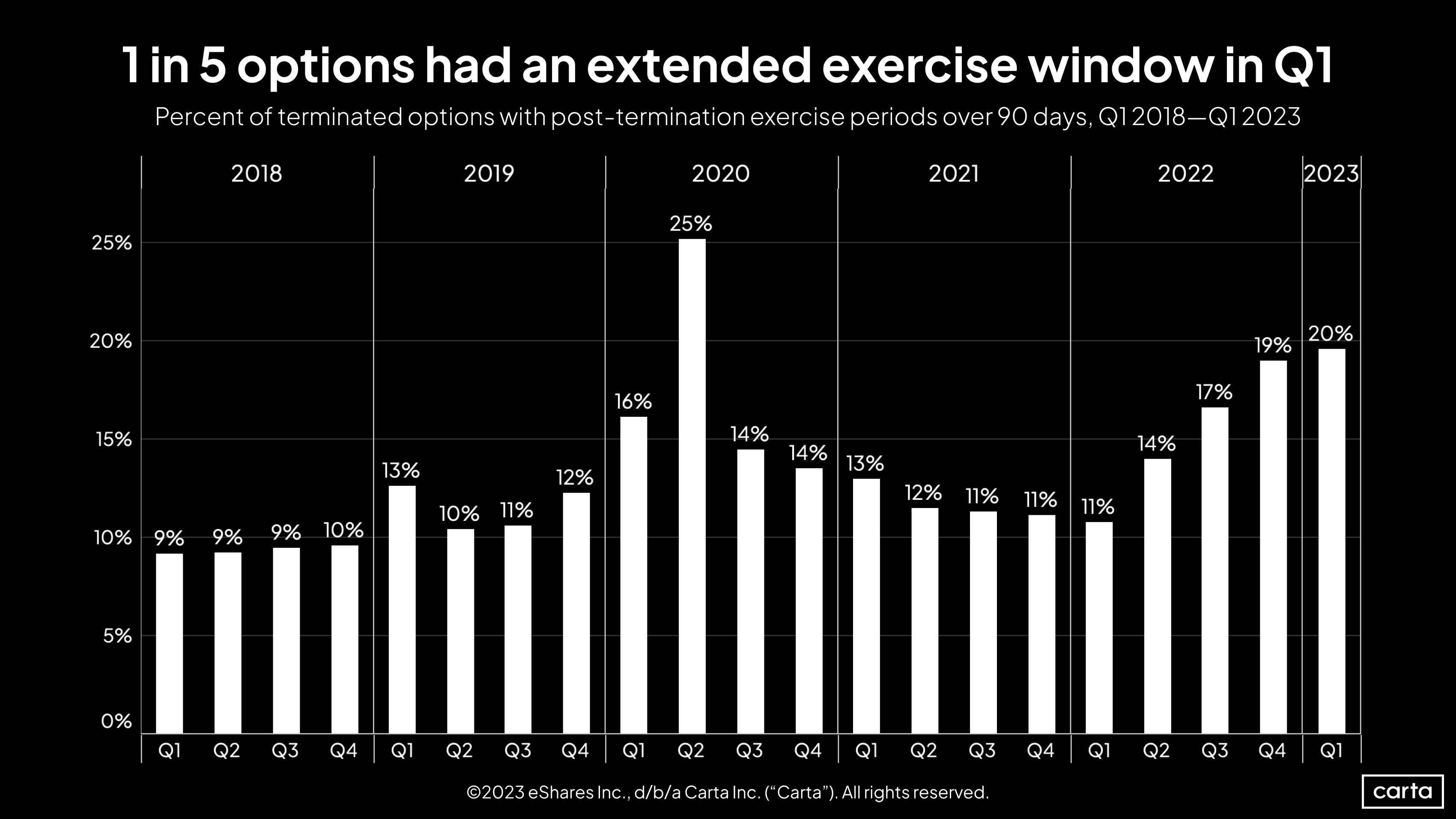

The trend of companies giving departing employees longer than the standard 90 days to exercise any vested options continued in Q1, with the rate of longer PTEP windows rising to 20%. This may be tied to the wave of tech-industry layoffs that washed over the market during the early months of 2023. Higher layoff rates tend to correlate to higher rates of extended PTEP, as companies aim to offer more financial flexibility to laid-off employees.

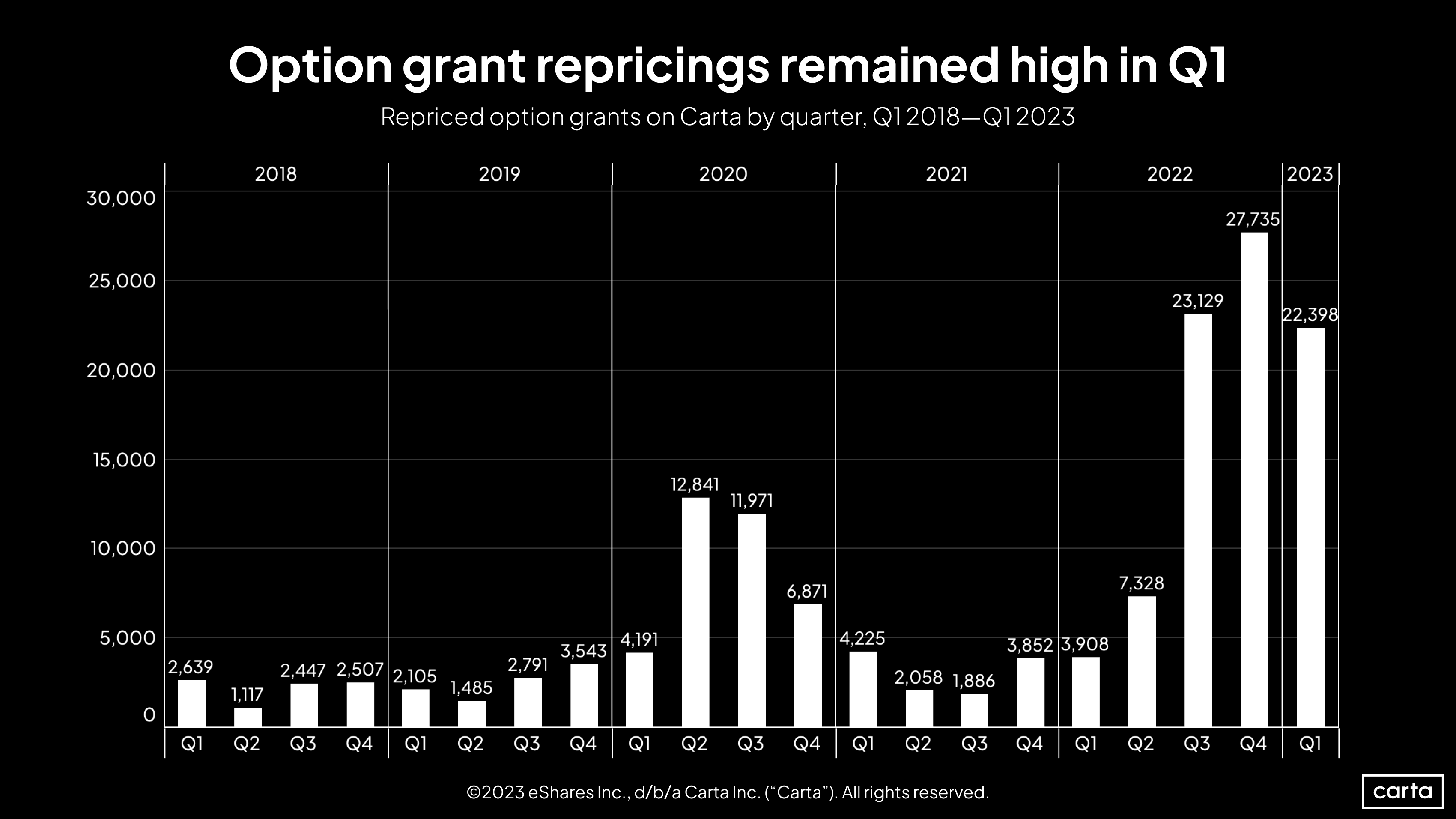

Companies on Carta repriced more than 22,000 option grants in Q1. That’s the third-highest quarterly figure since the start of 2018, trailing only the two preceding quarters. The recent spike is tied to the valuation reset unfolding across the tech market—companies typically reprice options after a valuation decrease in order to make those options more attractive to employees.

In addition to priced venture valuations, 409A valuations are also trending down to flat. Just 29% of all new 409A valuations on Carta last quarter came at an increased valuation, the lowest figure in more than five years, while the percentage of 409A valuations that stayed flat approached a five-year high.

The rate of new 409As with decreased valuations fell from the recent high point it reached last quarter. But 409A decreases are still nearly three times more common today than they were five years ago.

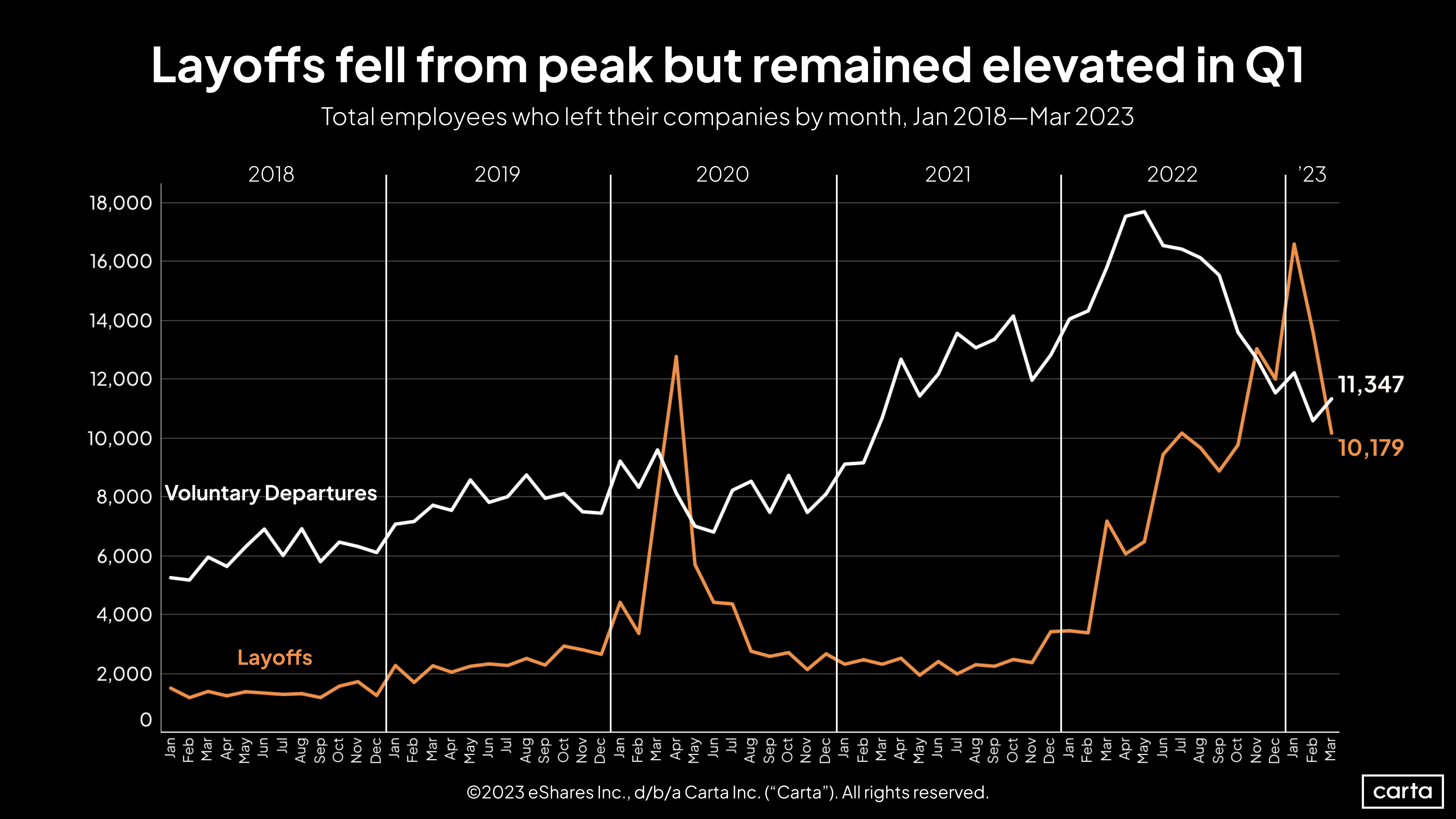

The number of layoffs is still quite high compared to most of the past five years, but figures have fallen significantly since peaking in January. Once again, there were more voluntary departures than involuntary layoffs in March, returning to the historical norm after a few months of a statistical inversion.

The number of employees on Carta has increased significantly over the past five years, which accounts for some of the long-term rise in job departures. Still, the combined number of voluntary and involuntary departures in Q1 remained high relative to the past few years.

Industry-specific data

For more industry-specific details on Q1 fundraising, download the addendum to the Q1 report.

Methodology

Carta helps more than 36,000 primarily venture-backed companies and 2,200,000 security holders manage over $2.9 trillion in equity. We share insights from this unmatched dataset about the private markets and venture ecosystem to help founders, employees, and investors make informed decisions and understand market conditions.

Overview

This study uses an aggregated and anonymized sample of Carta customer data. Companies that have contractually requested that we not use their data in anonymized and aggregated studies are not included in this analysis.

The data presented in this private markets report represents a snapshot as of April 26, 2023. Historical data may change in future studies because there is typically an administrative lag between the time a transaction took place and when it is recorded in Carta. In addition, new companies signing up for Carta’s services will increase historical data available for the report.

Financings

Financings include equity deals raised in USD by U.S.-based corporations. The financing “series” (e.g. Series A) is taken from the legal share class name. Financing rounds that don’t follow this standard are not included in any data shown by series but are included in data not shown by series. Primary rounds are defined as the first equity round within a series. Bridge rounds are defined as any round raised after the first round in a given series. If there is no indication that a round is a primary or bridge round, both are included.

In some cases, convertible notes are raised and converted at various discounted prices within a series (e.g. Series A-1, Series A-2, Series A-3). In these cases, converted securities are not included in cash raised, and only the post-money valuation of the new money is included.

Terminations

Terminations entered into Carta must include a reason. Involuntary terminations include both terminations for performance and company layoffs. Voluntary terminations are employees who decided to leave of their own accord. Other termination reasons, including for cause, death, disability, and retirement were not included in the data and make up less than 1% of all terminations combined.