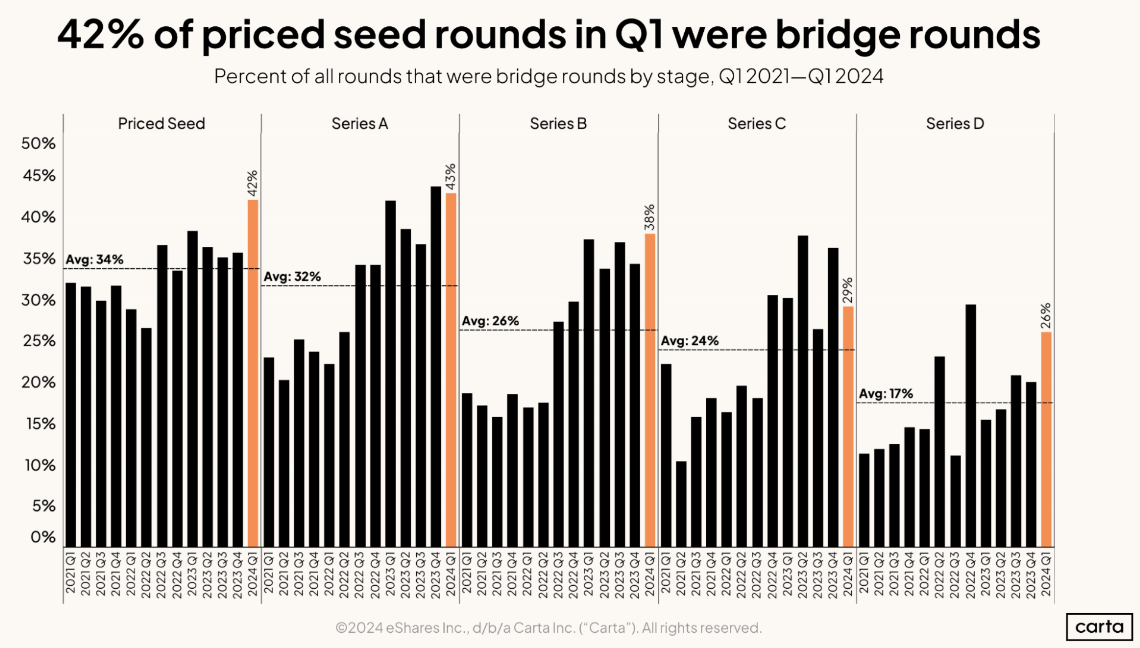

Bridge rounds are still booming.

In the first quarter of 2024, 42% of all seed-stage investments on Carta were bridge rounds, a higher percentage than in any other quarter so far this decade. At Series A, bridge rounds accounted for 43% of all activity, the second-highest rate of the 2020s. The rate of bridge rounds was also above the three-year average in Q1 at Series B, Series C, and Series D.

Bridge rounds are interim financing events often structured as extensions or follow-ons to the first round in a primary fundraising series, such as Series A. They often involve some of the same investors as the first primary round. They’re usually smaller than primary funding rounds. And right now, they’re more popular than ever.

Download bridge round data“On the company side, I’m seeing more bridge financing instruments than I’m seeing priced rounds right now,” says Jared Brenner, a senior counsel at Stubbs, Alderton & Markiles who works with a roster of venture-backed tech startups. “Even for some of the more successful companies on my client list, with nine-figure valuations and such, I’m not really seeing them very eager to kick off a priced round right now, but rather to raise notes and wait and see.”

A bigger slice of the pie

The number of combined venture deals—both bridge and primary—has declined over the past several quarters at every stage. But bridge rounds have been much more resilient to the market slowdown.

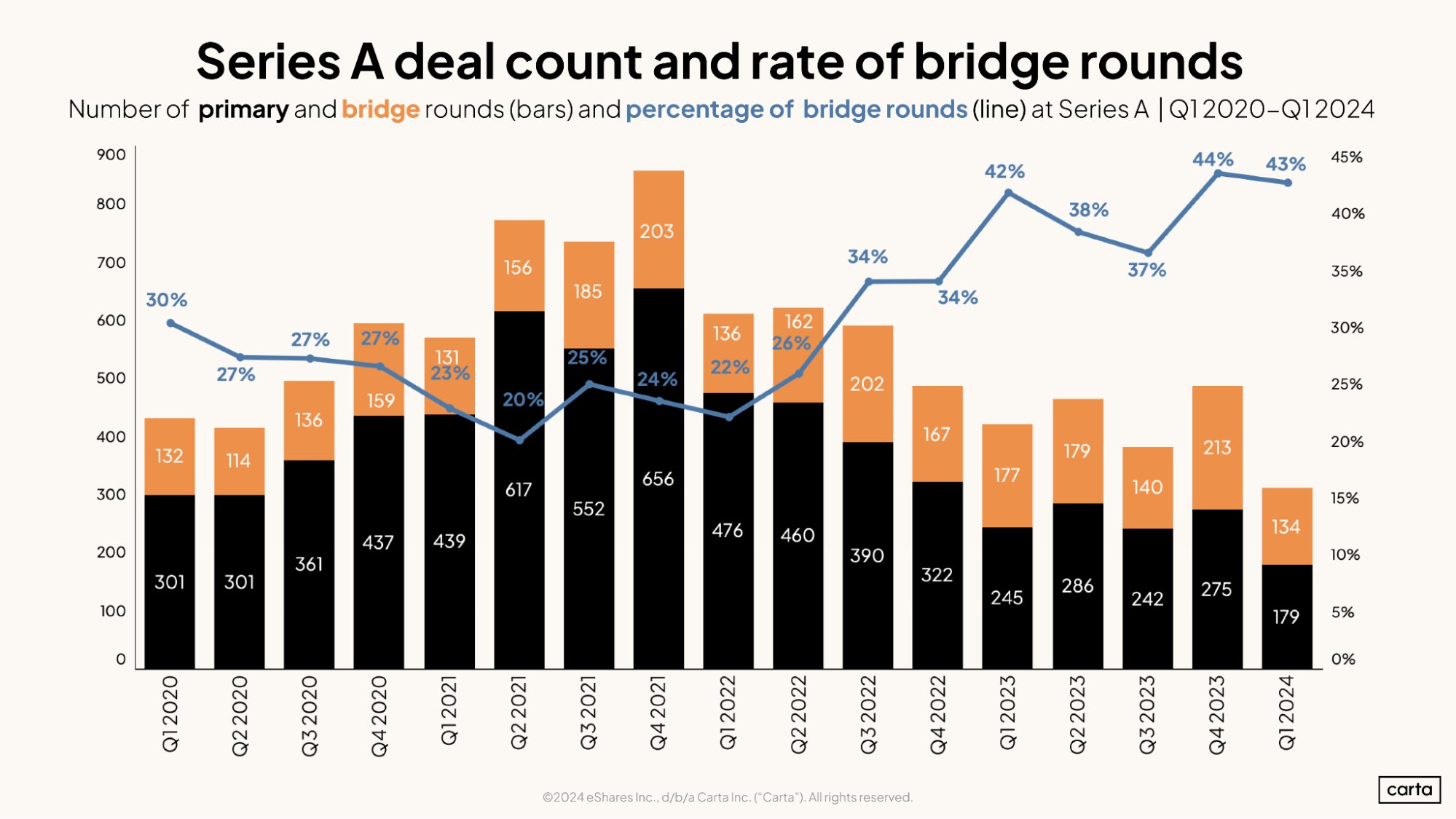

For instance, consider the chart below, showing Series A deal activity over the past four years. From the peak of deal activity in Q4 2021 through Q1 2024, the number of overall deals declined by 64%. The number of primary rounds declined by 73%. The number of bridge rounds, meanwhile, fell by a much less dramatic margin of 34%.

As a result, the rate of bridge rounds among all Series A activity increased from 24% in Q4 2021 to 43% in Q1 2024.

This trend of bridge rounds being more resilient to the recent drop-off in deal activity is consistent across seed, Series A, Series B, and Series C. You can view the data for the other three stages in this downloadable addendum.

What bridge rounds look like in 2024

Not every bridge round is alike. In some cases, bridge rounds take the form of new equity financing. In other cases, they’re a type of convertible debt funding, often in the form of convertible notes.

Most of the time, the investors in a bridge round already own a stake in the startup. They’re investing to give their existing portfolio company some more time (and some more capital) to meet certain growth targets or financial goals.

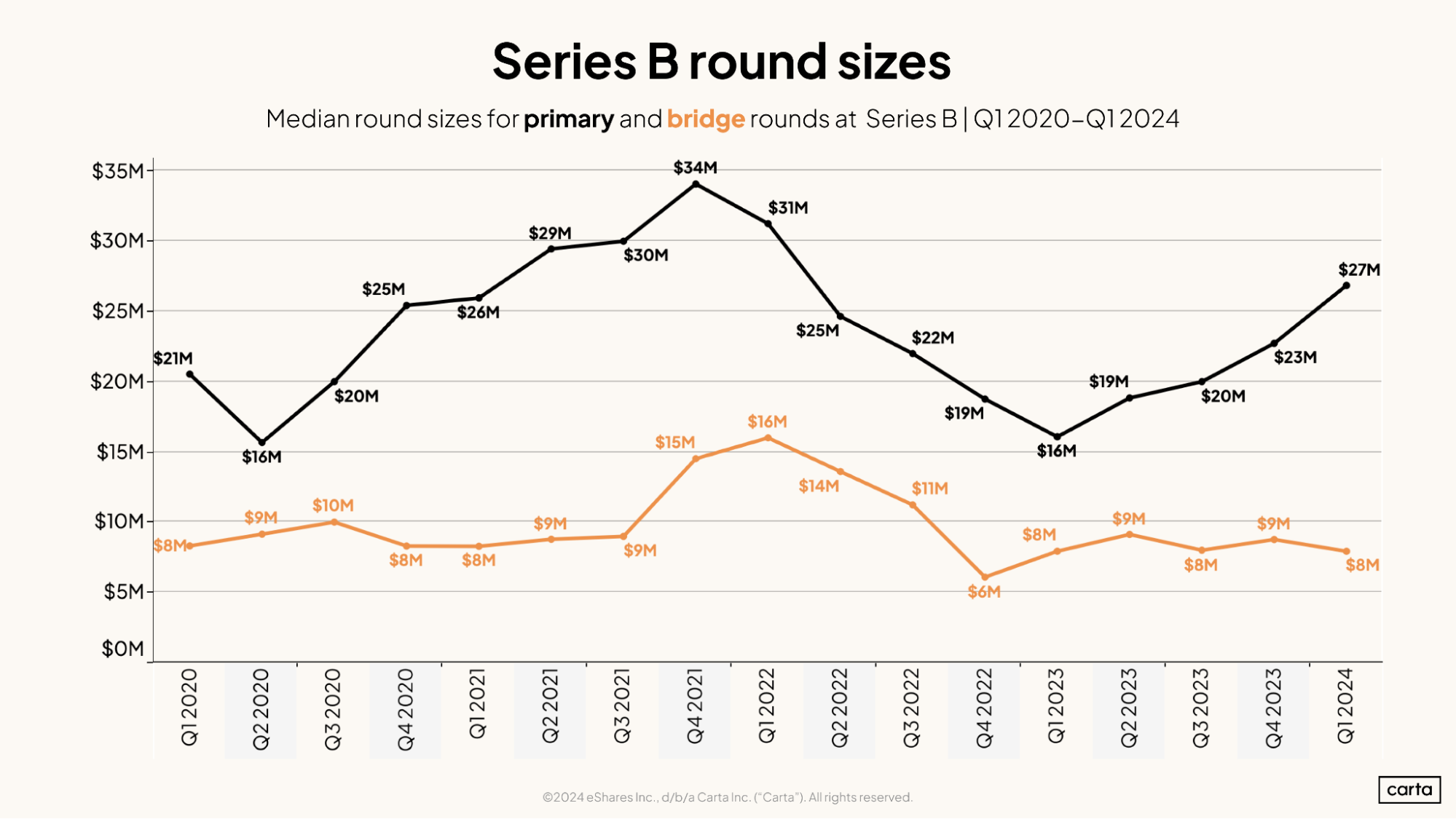

Round sizes

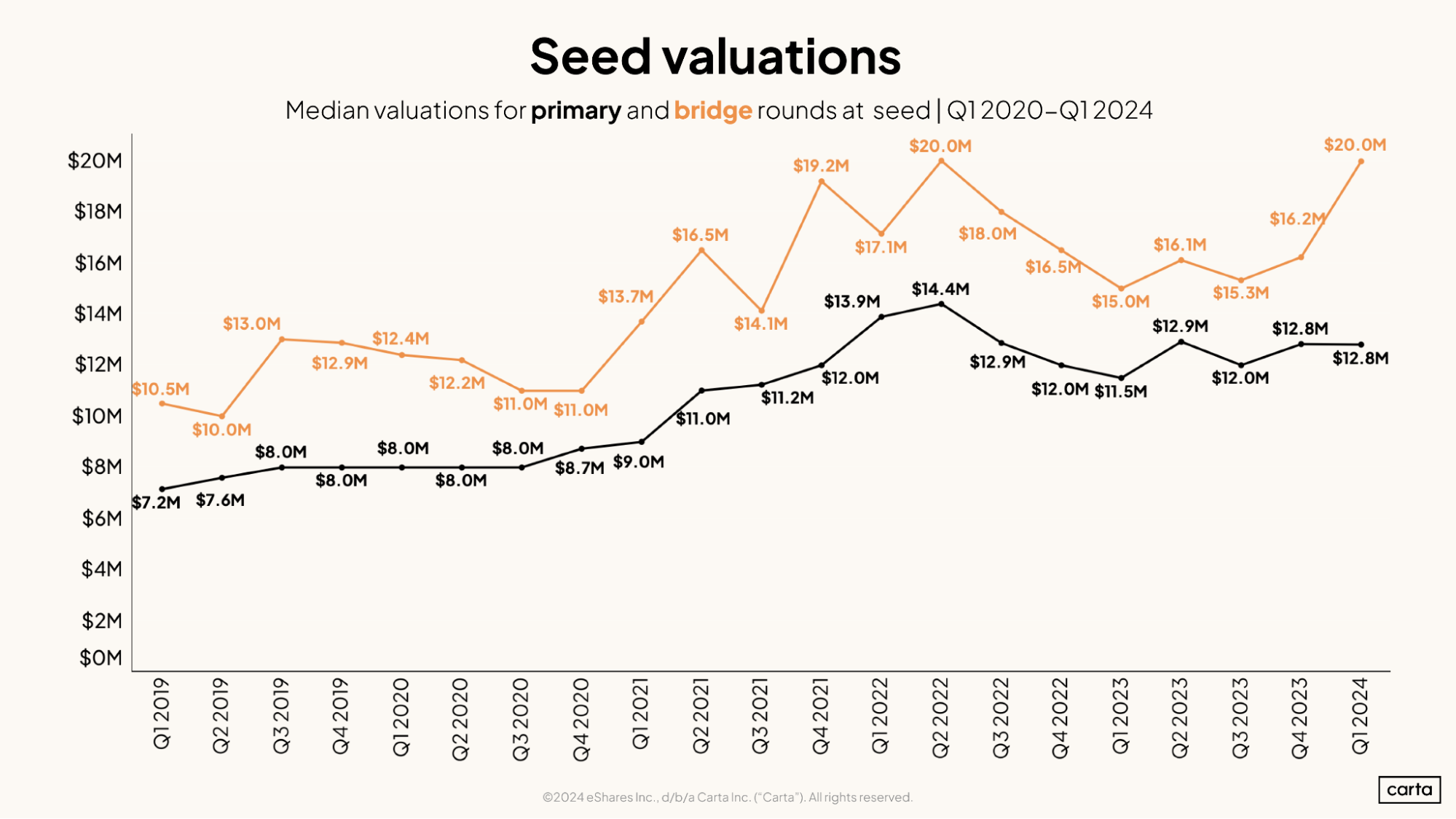

At the seed stage, primary rounds and bridge rounds are typically of similar size. But a bit of a gap emerged between the two in Q1 2024. In fact, the difference in size between primary and bridge rounds at the seed stage was wider last quarter than in any other quarter this decade.

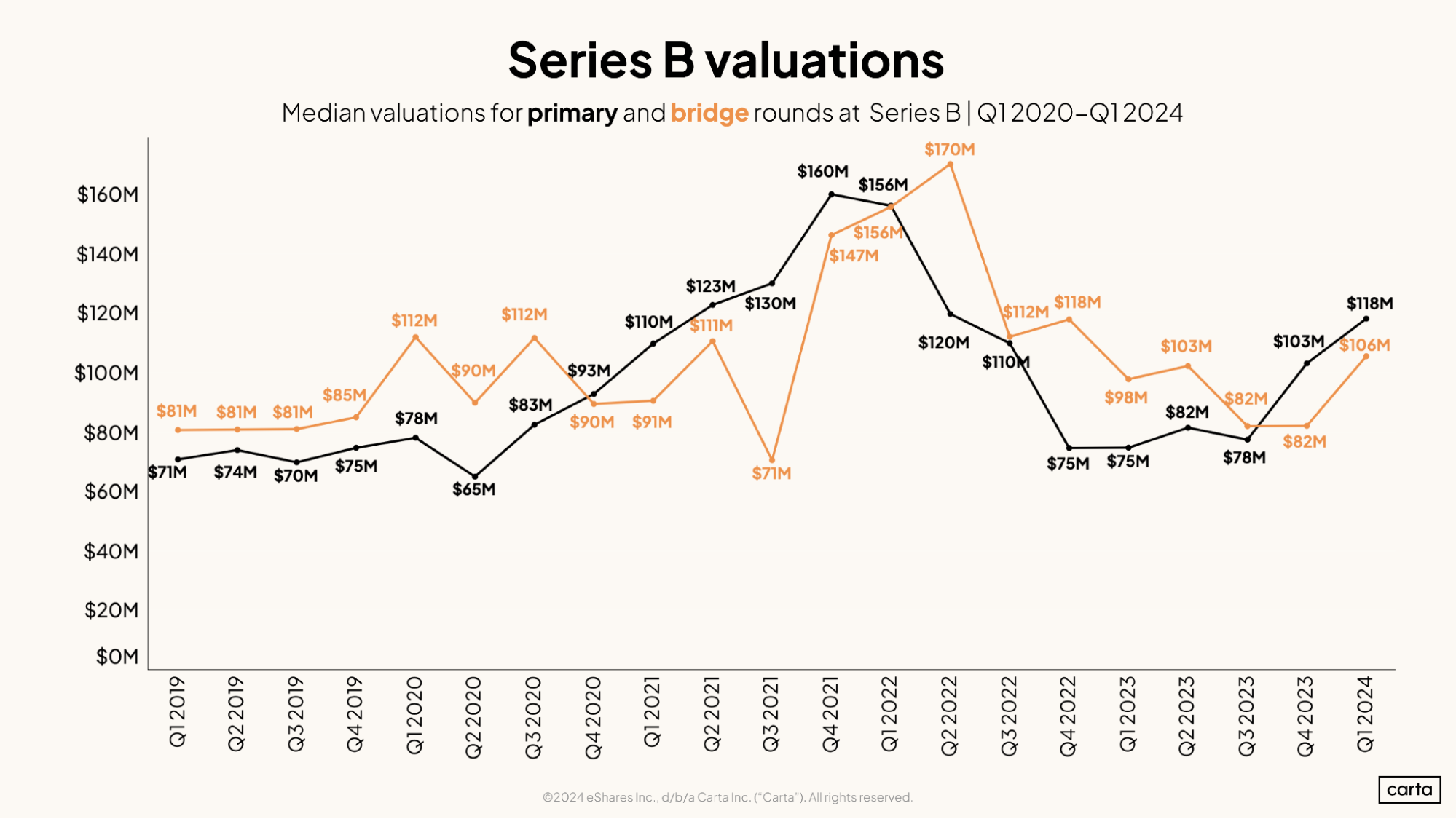

At later stages, primary rounds tend to be significantly larger than bridge rounds. For example, here’s how the two financing types stack up at Series B. (You can find the charts for Series A and Series C in the downloadable addendum.)

Valuations

At the seed stage, the median bridge valuation has been higher than the median primary valuation for more than 20 consecutive quarters.

It’s a different picture at Series A, Series B, and Series C. At these later stages, median valuations in bridge rounds and primary rounds are typically close, with neither financing type consistently netting higher valuations than the other.

At Series B, for example, the median primary valuation has now been higher than the median bridge round in back-to-back quarters. Before that, the median bridge valuation was higher in the six previous quarters.

At the level of individual companies, dealmakers say that it’s rare for the valuation in a bridge round to be higher than the valuation in the company’s previous primary round.

This is largely due to the nature of bridge rounds, which are often seen as something of a stopgap measure between major milestones. The buzziest, fastest-growing startups with several VC suitors are still much more likely to raise a new primary round than a bridge round.

“I don’t think valuations in the bridge rounds are going up. It’s more likely to be flat,” says Frances Mosley, a counsel at WilmerHale, where she works with startups on fundraising and a range of other corporate matters. “For investors, the thought process is like: We’re just trying to help you stay afloat, and you’re going to do us a favor by not making us negotiate with you for a higher valuation.”

‘Kicking the can down the road’

The recent rise of bridge rounds is a factor of the current fundraising environment. The venture market has cooled off considerably after a record-setting flurry of deal activity in 2021 and early 2022. Deal counts, deal sizes, cash raised, and valuations have all declined.

With fewer deals and fewer dollars on the market, many startups have struggled to raise new primary rounds at attractive terms—or struggled to raise them at all. In Brenner’s experience, companies typically turn to a bridge round after finding that raising a new primary round will be more difficult than they might have thought. “Sometimes, companies think a bridge round will be easier to get investors to ‘yes,’” Brenner says. “Or sometimes, they simply want to wait for better economic conditions. It’s usually one of those two reasons.”

But don’t think of bridge rounds as throwing in the towel. Sometimes, they’re sound strategy. Brenner uses a different metaphor to describe raising a bridge round in an unfriendly fundraising environment.

“In some cases, we recommend that a bridge round is a good way of kicking the can down the road on the economic uncertainty that we’re dealing with,” Brenner says.

Download additional data

Download the addendum to see bridge rounds by deal count and valuations.