- VC funding in healthcare has been more resilient than other industries

- A less severe decline

- Growing long-term momentum

- Q1 was strong for biotech/pharma

- Health sector founders are raising with less dilution

- Bridge rounds surged in Q1

- Geographical trends

- The typical fundraising journey for health startups

- Get the latest data

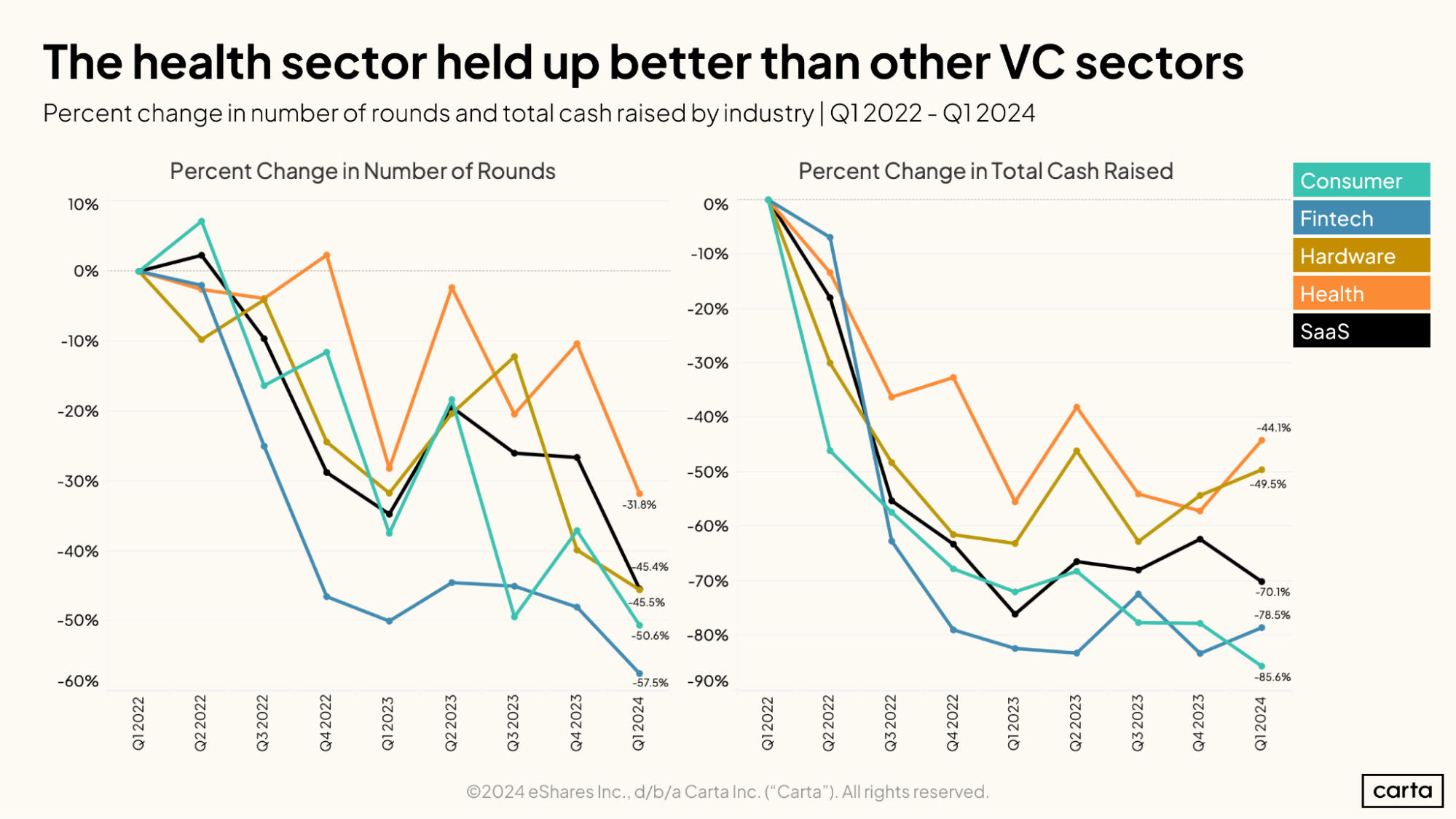

As Carta’s Q1 State of Private Markets report showed, venture capital had a slow start in 2024. The fundraising market seems to have settled down into a new normal after the boom-and-bust cycle of 2020 to 2023. However, the downturn that began in 2022 did not affect all industries equally. The health sector—including healthtech, biotech, pharma, and medical devices—has held up better than other major industries. Four years after the onset of the global COVID-19 pandemic, there seems to be durability in VC funding for health-related startups.

A less severe decline

While deal counts and cash raised have fallen off in each of the five largest industry categories on Carta since the start of 2022, the declines are smallest in the health sector. Through Q1 2024, the number of funding rounds decreased by 31.8% for health companies, but by 45.4% for SaaS and by 57.5% for fintech.

In terms of total cash raised, the health sector shrank by 44.1% since Q1 2022, compared to 70.1% for SaaS and 78.5% for fintech. Over the past quarter, though, there was a large increase in the amount of capital invested in health startups. Capital flowing to fintech and hardware also rose last quarter, but decreased for SaaS and consumer products and services.

Growing long-term momentum

Zooming out, we can see that the health sector’s share of all venture capital invested in companies on Carta has risen from 21% in 2018 to 32% in 2024 (as of Q1). This year is on track to be a bigger year for the health sector than 2020, the year the COVID pandemic began (and which currently holds the record for the highest portion of all cash raised in the health sector).

The lion’s share of the health sector’s growth can be attributed to the biotech/pharma segment, which has more than doubled its annual share of total capital invested since 2018. Healthtech and medical devices have held relatively consistent pieces of the pie.

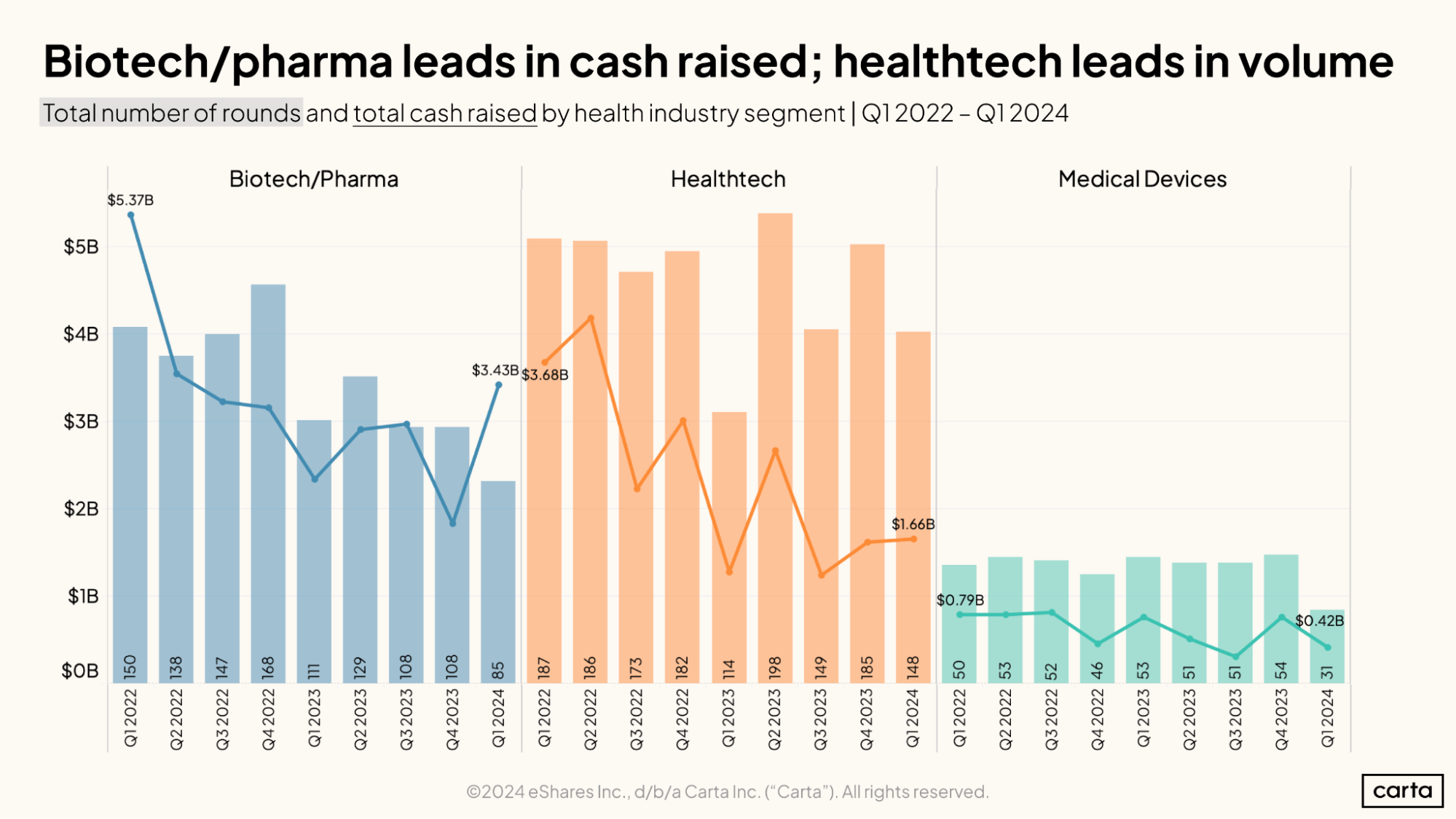

Q1 was strong for biotech/pharma

So far, 2024 has been strong for biotech/pharma in terms of total cash raised, surging 86% from Q4 2023 to Q1 2024. Cash raised was essentially flat for healthtech companies in Q1, inching up 2%, while it declined by 45% for medical device startups.

Although biotech/pharma has a big edge in cash raised, there is more deal activity in healthtech, meaning that the latter has a higher prevalence of smaller rounds. In Q1, healthtech companies on Carta completed 148 deals, more than biotech/pharma and medical devices combined.

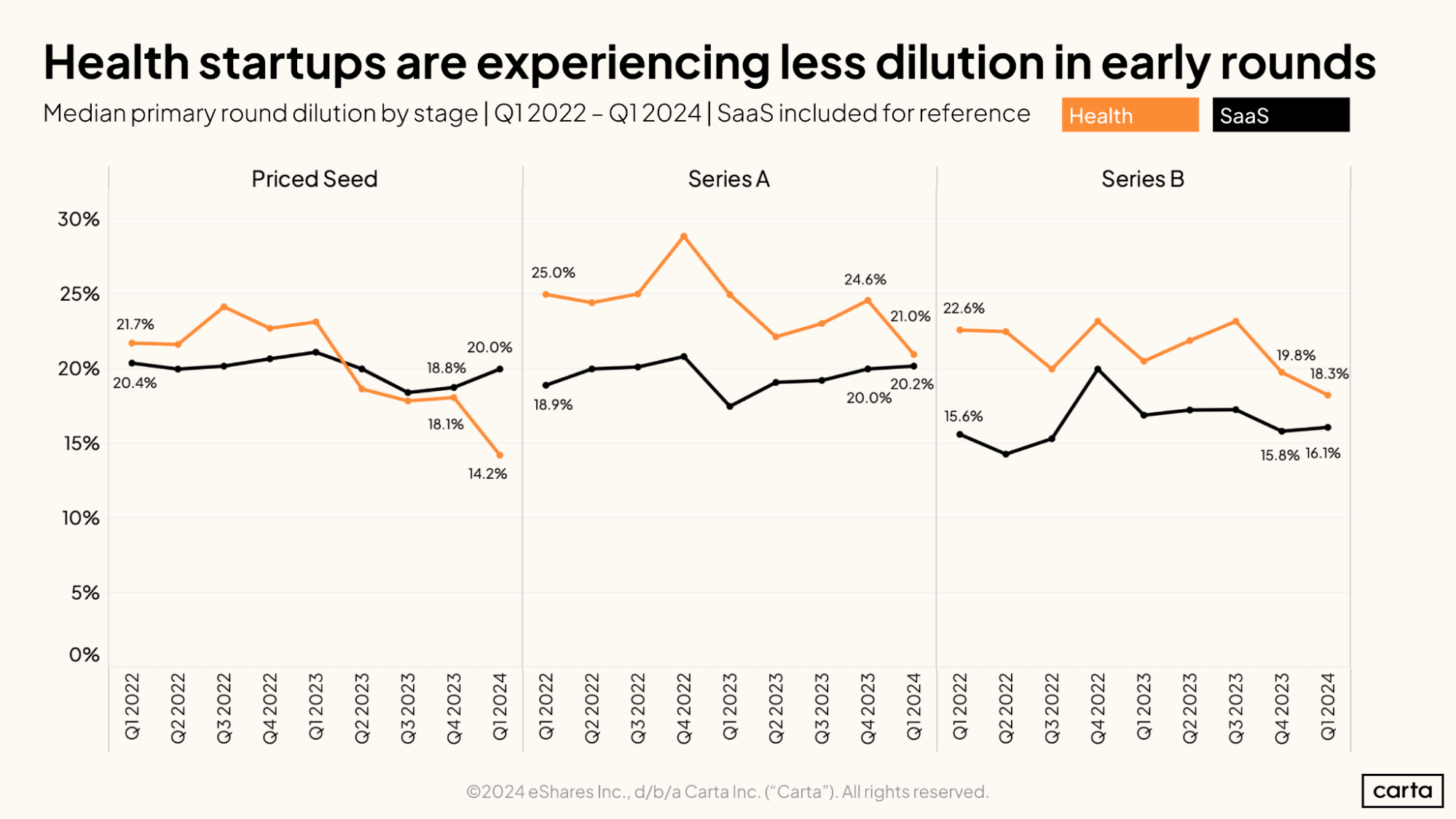

Health sector founders are raising with less dilution

Since Q1 2022, founders of early-stage healthcare companies have been selling less of their companies to investors in primary rounds. Dilution for SaaS startups during the same time period has stayed flat or even increased slightly.

During Q1 2024 in particular, there was a marked decline in median primary round dilution for health startups at seed, Series A, and Series B. In priced seed rounds, median dilution for health companies dipped down to just 14.2%, compared to 20% for SaaS.

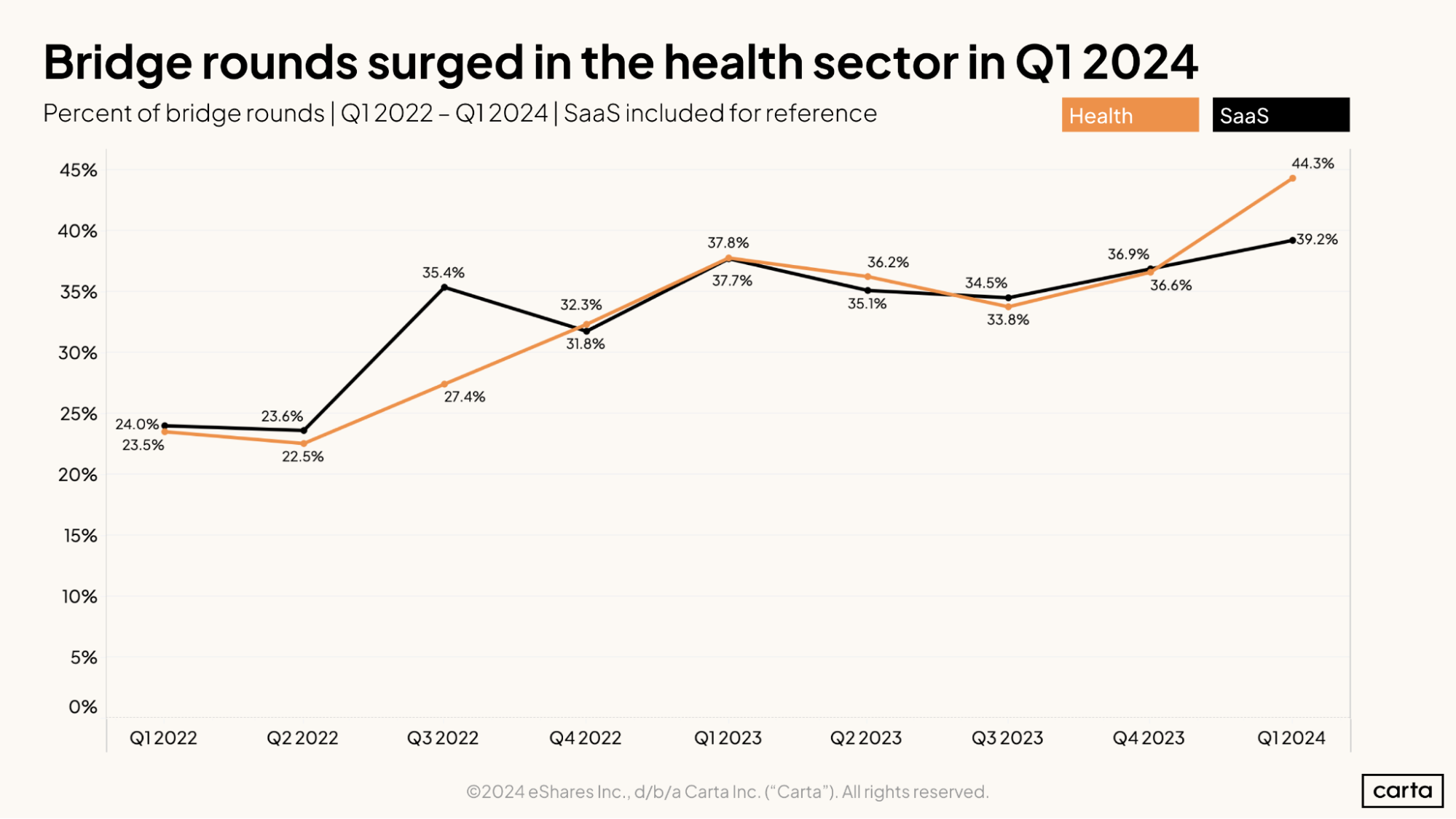

Bridge rounds surged in Q1

The frequency of bridge rounds surged in the health sector in Q1, jumping to 44.3% from 36.9% in Q4 2023. This was the first time since the start of 2022 that there was a significantly higher rate of bridge rounds in healthcare than in SaaS. Despite the health sector’s overall resilience in fundraising, the upswing in bridge rounds in 2024 suggests that certain founders are either not ready or not yet able to raise a primary round.

Geographical trends

In Q1, there was a general trend towards a higher share of venture capital being invested in the West, and this was even more so the case for health startups. The share of the health sector’s capital that was invested in companies in the West leaped to 60%, the highest of any major sector. Healthcare was the only sector for which the Midwest, Northeast, and South all saw their market share decline in Q1.

Deal counts show a different story. In terms of the number of deals, the Northeast now has the highest share within the health sector. For the other major industries analyzed, the West still leads in volume. The Northeast is home to many smaller deals in the health sector, while the bigger and later-stage deals are taking place in the West.

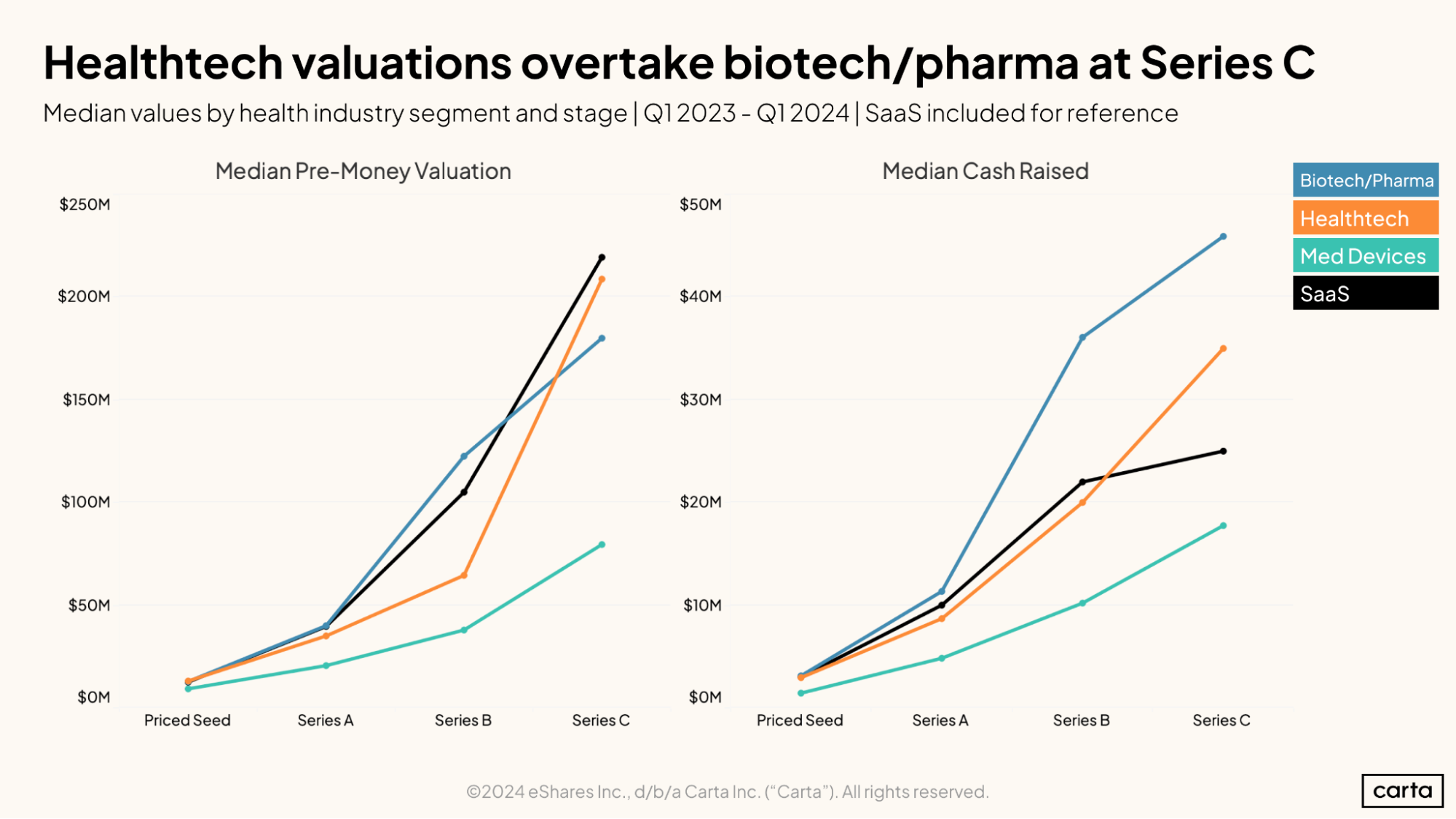

The typical fundraising journey for health startups

Data from rounds raised by Carta companies between Q1 2023 and Q1 2024 shows that the fundraising journey can vary greatly across different segments of the broader health industry. While amounts of cash raised and pre-money valuations are similar at the priced seed stage, they diverge over time. By Series C, medical device companies lag significantly behind the other health segments by both metrics.

Biotech/pharma companies track closely with SaaS companies in terms of pre-money valuation until Series B. At Series C, healthtech valuations overtake biotech/pharma. This is not the case for deal size, as biotech/pharma startups consistently raise the largest rounds across stages. By Series C, biotech/pharma and healthtech have larger median rounds but lower pre-money valuations than SaaS, an effect of the capital intensity of the health sector.

Get the latest data

For the latest data on venture capital fundraising, startup hiring, compensation benchmarks, and more, sign up the Carta Data Minute: