Latest updates

In August 2024, the SEC adopted amendments to the qualifying venture capital fund parameters. The change lifted the original $10 million ceiling on qualifying venture capital funds to $12 million. This amendment was expected: The law requires the SEC to revisit the dollar cap on qualifying venture funds at least once every five years, to index it for inflation.

While a 20% increase to the fund AUM limit is a move in the right direction, the $12 million cap remains too restrictive to be an effective mechanism for facilitating capital formation among new and emerging managers. Congress should pass legislation to increase the size and investor limits to enhance the utility of the qualifying venture capital fund exemption.

Issue

Congress created the “qualifying venture capital fund” exemption to Section 3(c)(1) of the Investment Company Act to make capital formation easier for emerging venture capital fund managers by increasing the number of permitted investors in venture capital funds under a certain size. In practice, the current parameters limit the utility of this provision.

To better support innovation and job creation in the venture capital sector, Congress can intervene to modernize the criteria for qualifying venture capital funds to account for existing market conditions.

How it works: Under Section 3(c)(1) of the Investment Company Act of 1940, a private fund may remain exempt from registering with the SEC as an investment company if it has no more than 100 investors.

Qualifying venture capital funds, however, may have up to 250 beneficial owners and still claim exemption under 3(c)(1), provided that they manage no more than $12 million in assets and meet the definition of a venture capital fund.

Why it matters: The higher limit of beneficial owners was intended to help emerging managers assemble competitive funds by collecting smaller contributions from a greater number of accredited investors. However, failure to meaningfully adjust the dollar threshold for existing market conditions has rendered their special status obsolete, and has stymied Congress’s intent to diversify beneficial ownership of venture capital assets.

Background

The vast majority of emerging venture capital funds seek exemption from registration under Section 3(c)(1). Congress added the definition of a “qualifying venture capital fund” to Section 3(c)(1) as part of the bipartisan Economic Growth, Regulatory Relief, and Consumer Protection Act (S. 2155). The objective was to make capital formation easier for emerging venture capital managers, but data shows the criteria for qualification were never right-sized for the market. Over time, they have become even more outdated.

The case for modernization

A $10 million ceiling for qualifying venture capital funds was never ideal and fast became obsolete. Raising the limit to $12 to index for inflation did not go far enough to modernize the provision.

Rising costs

Economic growth, technological sophistication, inflation, and other factors have contributed to a rise in the cost of doing business in venture capital. Put simply, entrepreneurs are raising more money at each stage of company development than they were in 2018, when qualifying venture capital funds were created by law. This is especially true of the early-stage, where most emerging managers operate.

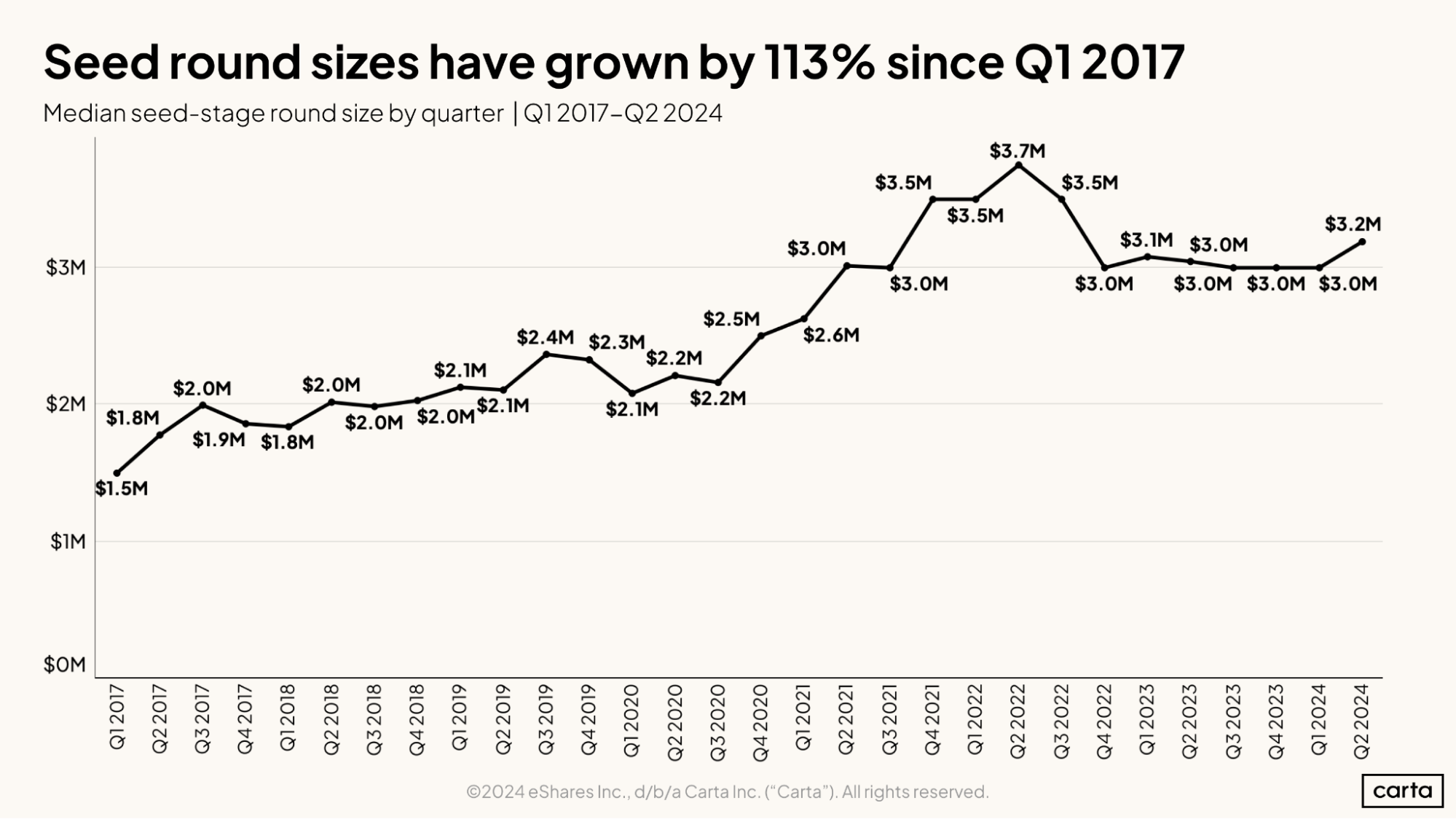

Carta data shows that throughout much of 2017 and 2018, the median seed-stage round hovered around $2 million. But since Q2 2021, the median seed-stage round has been at least $3 million. Over a seven-year period, the median size of seed financings rose by more than 100%.

Meanwhile, the $10 million ceiling on qualifying venture capital funds only rose by 20% in 2024—and it isn't due for reassessment until 2029. This means the provision will likely be even less useful in the coming five years than it was in the past.

Reduced ability to compete for deals

Why does this matter? Seed investors typically need to invest in 25-35 companies for their funds to be viable. Investors at the earliest stages need to take far more “shots on goal” than funds investing at the later stages, when companies already have product-market fit and viable business models. A doubling of the cost of seed-stage investment means that funds capped at $12 million are less able to keep up with rising costs. This can make them less attractive to investors and less competitive in the market.

Funds are foregoing qualifying status

The purpose of the special provisions for qualifying venture capital funds was to help more emerging managers raise funds that would be competitive in the market, and to allow more small-check inventors to gain exposure to the venture asset class. The caps on beneficial owners and fund size make qualifying venture capital funds, as currently defined, incapable of achieving these goals.

Not only does the $10 million or $12 million no longer support the number of portfolio companies it did just five years ago, but investors are also being left out: Recognizing the limitations of the fund size cap, funds are foregoing qualified status and raising larger funds from up to 100 larger investors, under the conventional 3(c)(1) limit. Less than half of the first-time funds launched on Carta since from 2016-2021 managed $10 million or less. And only 2% of first-time funds formed on Carta in 2021 had more than 100 LPs, which suggests that vanishingly few fund managers pursue exemption as a qualifying venture capital fund.

Potential changes

Congress has the ability to amend the criteria for qualifying venture capital funds. The SEC’s Small Business Capital Formation Advisory Committee has already recommended that the agency raise caps on both fund size and beneficial ownership.

Bottom line

The $12 million AUM cap and 250 beneficial owner limit for qualifying venture capital funds are both too low for the qualifying venture capital fund exemption to serve its intended purposes. Raising these thresholds will help foster innovation in the venture capital sector, particularly for emerging funds and founders.

Proposed legislation in the U.S. House (with caps of $150 million AUM and 600 beneficial owners) and Senate (with caps of $50 million AUM and 500 beneficial owners) would provide substantial and meaningful updates to the qualifying venture capital fund parameters.

Get involved

To learn more about how to get involved in Carta’s work to create public policy for tomorrow’s innovation economy, write us here.

Stay up to date on policy affecting the private markets by subscribing to Carta’s Policy Weekly newsletter:

DISCLOSURE: This publication contains general information only and eShares, Inc. dba Carta, Inc. (“Carta”) is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. All product names, logos, and brands are property of their respective owners in the U.S. and other countries, and are used for identification purposes only. Use of these names, logos, and brands does not imply affiliation or endorsement. ©2023 eShares Inc., d/b/a Carta Inc. (“Carta”). All rights reserved. Reproduction prohibited.