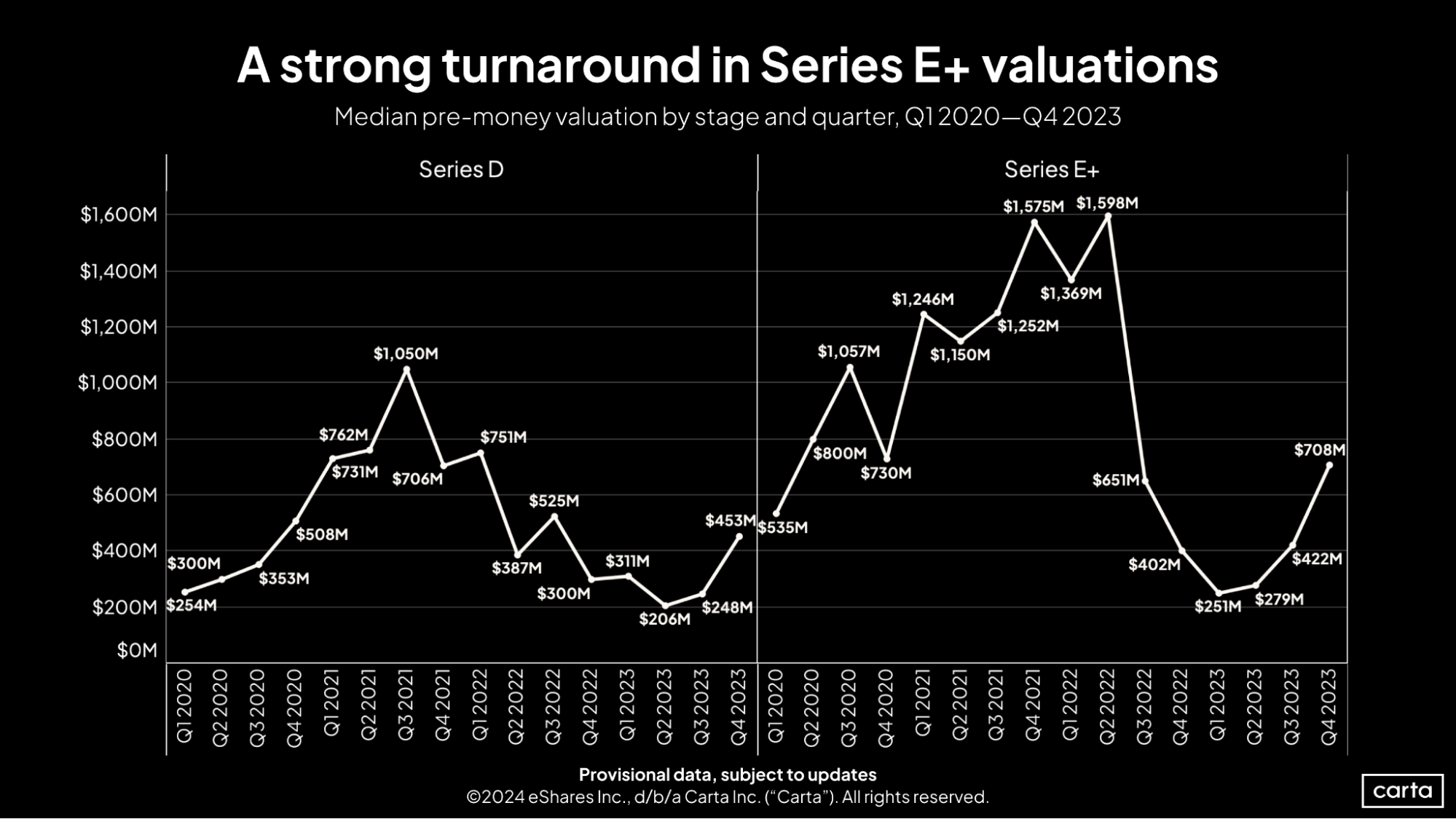

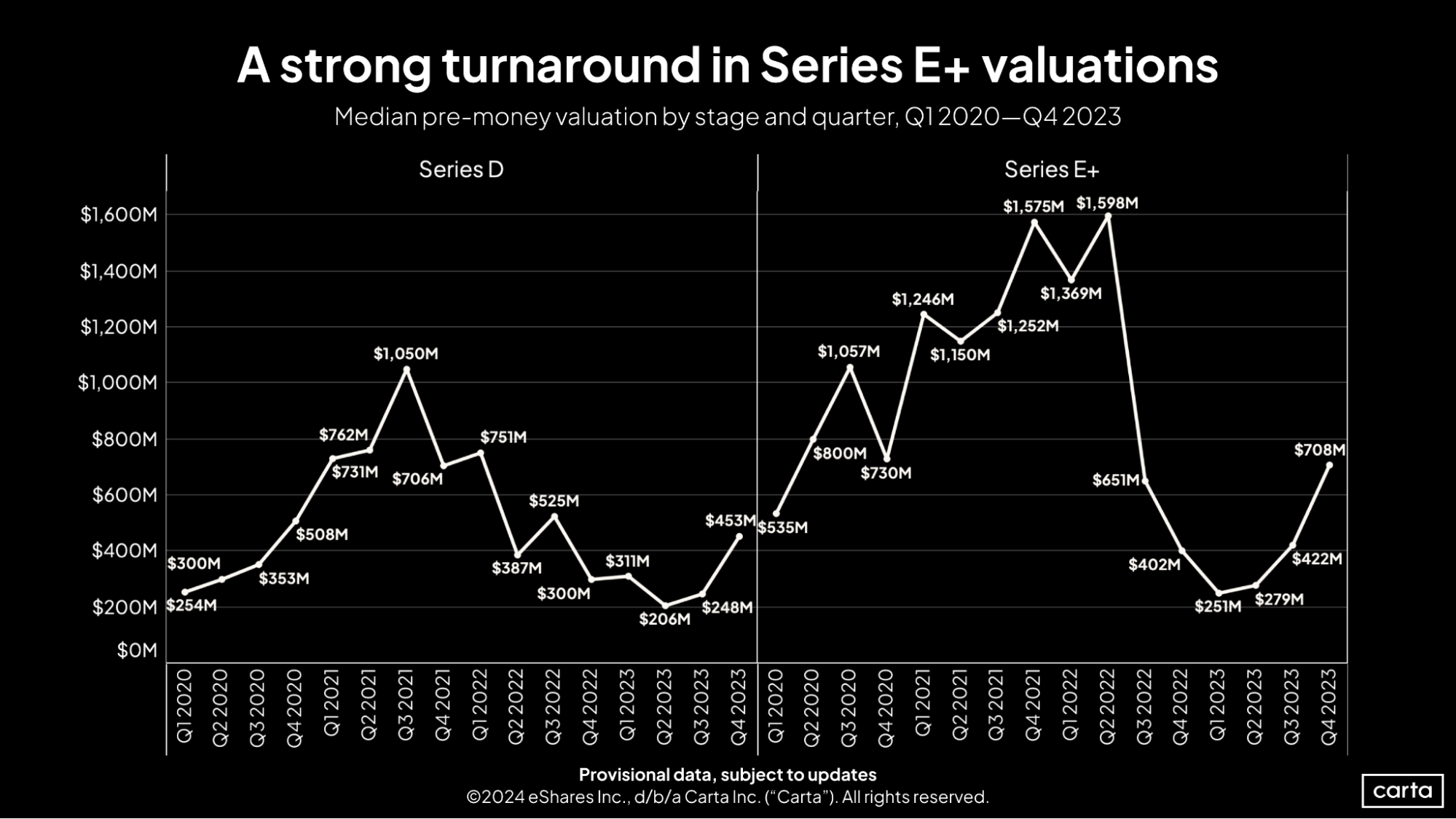

For the first time since the startup market’s peak in 2021, late-stage venture valuations are showing significant positive momentum.

The median Series D valuation across both primary and bridge rounds soared to $453 million in Q4 2023, an 83% increase over the prior quarter. And the median valuation at Series E and beyond rocketed to $708 million, a 68% quarterly climb.

As you can see below, valuations at both these stages fell off sharply during 2022 and the first half of 2023, declining to their lowest points in the past several years. But over the past two quarters, things have begun to look back up.

Valuations increased across most stages

This Q4 growth in valuations at Series D and Series E+ is part of a larger trend that extends to earlier stages in the startup lifecycle, too.

At seed, the median valuation across both primary and bridge rounds inched up by about 3% last quarter. At Series A, it was a 17% increase. The median Series B valuation got 21% larger in Q4. The only exception was at Series C, where the median valuation declined by 17%.

This was the second quarter in a row in which valuations increased at five of these six startup stages. In Q3 2023, the exception was at Series B, where median valuations fell by just 3%.

A positive year for valuations

On an annual basis, valuations are trending up at all six of these startup stages. Here’s a breakdown of how median valuations changed between Q4 2022 and Q4 2023:

Stage | Year-over-year valuation increase |

Seed | 5% |

Series A | 29% |

Series B | 29% |

Series C | 5% |

Series D | 51% |

Series E+ | 76% |

The biggest year-over-year increases came at the latest stages, as was the case with the biggest quarter-over-quarter increases in Q4. This makes some sense given the scope of the year-over-year declines that these later stages experienced in 2022: That year, the median Series D valuation declined by 58%, and the median valuation at Series E+ fell by 74%.

Late-stage valuations plummeted in 2022 to a degree that was unprecedented in the previous decade of startup investing. In Q4 2023, the market took a significant step toward its recovery.

Get the latest data

For weekly insights into Carta's unparalleled data on the private markets, sign up for Carta’s Data Minute weekly newsletter:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. ©2024 eShares Inc., d/b/a Carta Inc. ("Carta"). All rights reserved. Reproduction prohibited.