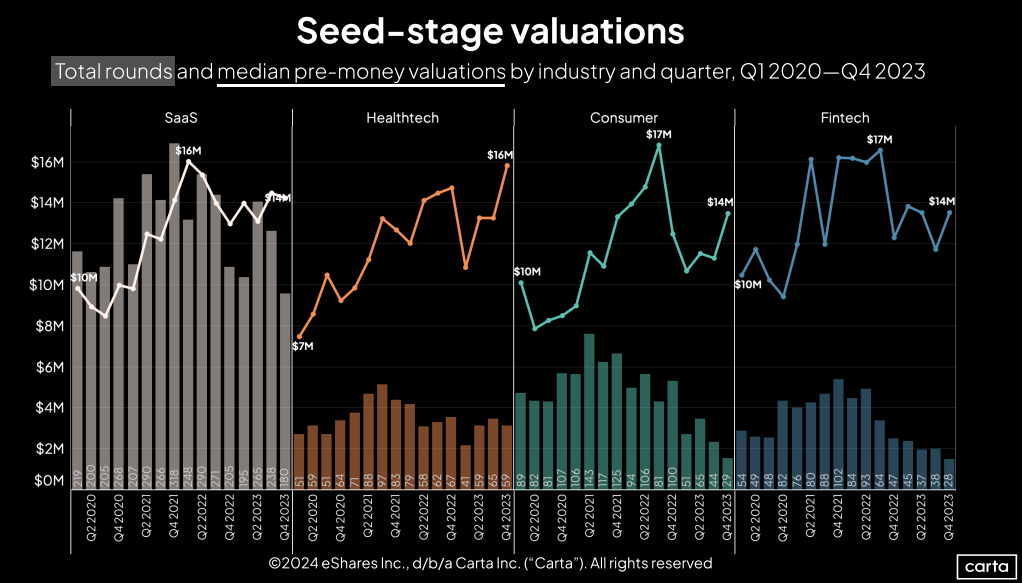

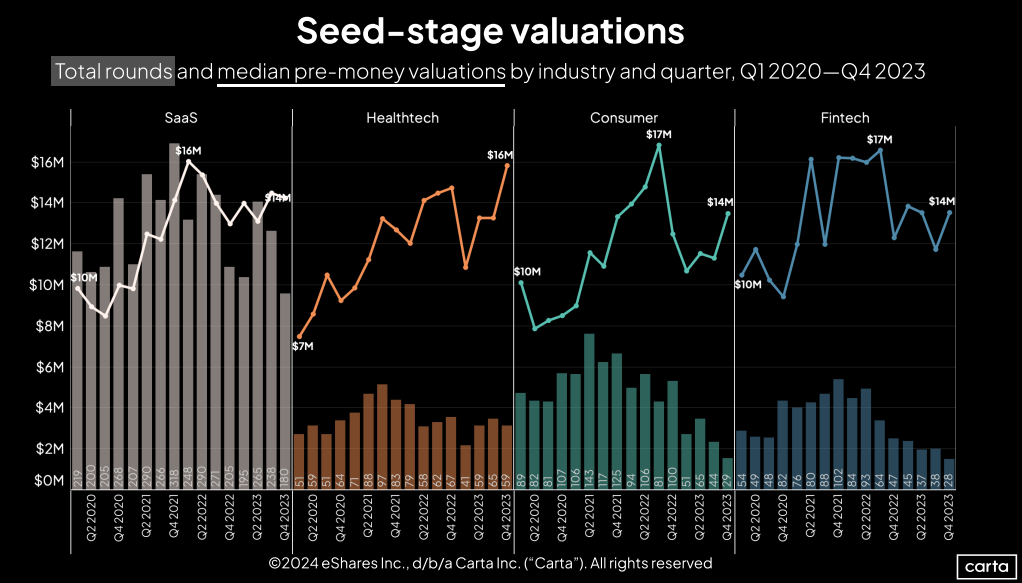

For young healthtech startups on the fundraising trail, last year got off to a worrisome start.

Across all sectors, Q1 2023 was a relatively static time in the seed market: The median seed valuation on Carta was $12.9 million between primary and bridge deals combined, a slight downtick from $13 million in Q4 2022.

But in the healthtech sector, seed valuations plunged: Q1’s median seed valuation of $10.9 million was 25% lower than the previous quarter’s mark of $14.5 million. Some founders surely worried: Are seed investors souring on healthtech?

As it turned out: Not so much. Over the next three quarters, seed valuations in healthtech recovered from Q1’s losses—and then some. By Q4, the median valuation in the sector hit $16 million, its highest point so far this decade and well above the median across sectors of $14 million.

It was a year of ups and downs for seed funding in several of the startup world’s most popular sectors. Here’s a closer look at how seed-stage trends shifted for SaaS, healthtech, consumer, and fintech startups in 2023, across four closely watched fundraising metrics.

Valuations

The healthtech industry saw the most movement in seed valuations over the course of 2023. But the consumer space wasn’t far behind. The median seed valuation for consumer startups jumped about 19% in Q4, rising to its highest point in the past five quarters.

Still, the latest seed valuations in the consumer sector lag behind the high-water mark reached in 2022. The same is true in SaaS and fintech, even though both of those sectors also saw year-over-year increases in median seed valuation. The only exception among these four industries is healthtech, where the median seed valuation hit a new high.

Deal count

Across all sectors, seed deal count declined by 21% in 2023 compared to 2022. Here’s how that combined metric compares to deal totals from these four separate sectors:

Sector | YoY decrease in seed deal count in 2023 |

SaaS | -13.4% |

Healthtech | -15.8% |

Consumer | -50.3% |

Fintech | -48.6% |

As you can see, in SaaS—which is by far the most active of these four sectors, with 878 seed deals in 2023—seed activity fell off by a smaller margin than other industries. The same is true for healthtech. Both the consumer and fintech sectors, meanwhile, saw seed activity decrease by a much larger percentage than the combined population of all seed companies.

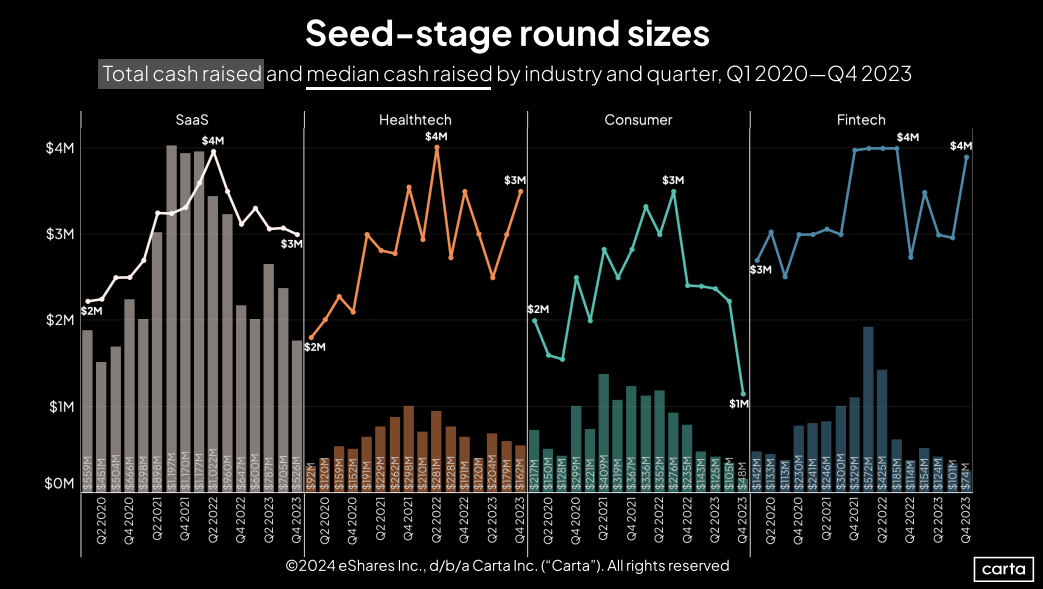

Round sizes

The good news: Seed round sizes in healthtech and fintech moved in a positive direction in the second half of 2023, with the median fintech seed size not too far off its recent bull-market highs of 2021 and 2022.

The bad news: Well, just look at that chart for the consumer sector. The median seed deal for consumer startups has gotten 67% smaller over the past five quarters, sinking from north of $3 million in Q3 2022 to barely $1 million in Q4 2023. It’s clear that investors have grown more hesitant about writing large checks to early-stage consumer startups.

The neutral news: Round sizes in the SaaS space have been less volatile and have mostly remained in line with overall trends in seed round sizes across all sectors.

Total cash raised

A combination of fewer deals and lower median deal sizes means that total cash raised declined significantly in all four of these sectors in 2023 compared to 2022. Here’s a look at the damage:

Sector | YoY decrease in seed cash raised in 2023 |

SaaS | -31.2% |

Healthtech | -26.9% |

Consumer | -64.9% |

Fintech | -65% |

As was the case with annual seed deal count, seed cash raised has declined the most in the consumer and fintech sectors. When fewer transactions take place, capital raised is likely to decline, too.

While the precise numbers differ across these common startup sectors, one overarching trend is clear: The rate of seed dealmaking has slowed down. Some experts think that might be for the best.

“The markets of 2021 and 2022 were not normal,” says Marcos Fernandez, managing partner at fintech investor Fiat Ventures. “The market that we’re in right now is a very healthy one, because it’s starting to get back to what is traditional between LPs and venture capitalists and founders. I anticipate 2024 is going to be a lot more of what we think of as a normal cycle, as opposed to what we’ve seen the past couple years.”

Get the latest data

For weekly insights into Carta's unparalleled data on the private markets, sign up for Carta’s Data Minute weekly newsletter:

DISCLOSURE: This communication is on behalf of eShares Inc., d/b/a Carta Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. All product or trade names, logos, and brands are property of their respective owners in the U.S. and other countries, and are used for identification purposes only. Use of these names, logos, and brands does not imply affiliation or endorsement. ©2024 eShares, Inc. dba Carta, Inc. ("Carta"). All rights reserved. Reproduction prohibited.