I wrote the following post over three years ago. Three years later, we’ve helped fix a lot of capitalization tables, but almost every new cap table we get is still broken. I’ve updated the post to reflect what’s changed in the industry.

Most capitalization tables are wrong

Nearly all capitalization tables are wrong when they get to our onboarding managers. Most early and mid-stage company cap tables are manually tracked in Excel. The “truth” of these cap tables is held in the signed and dispersed paper documents (i.e. option grants) and the “model” is in Excel. Frequently, transactions happen but are not recorded in the cap table. And the further away from a financing round (when the cap table is normally cleaned up) the worse the entropy.

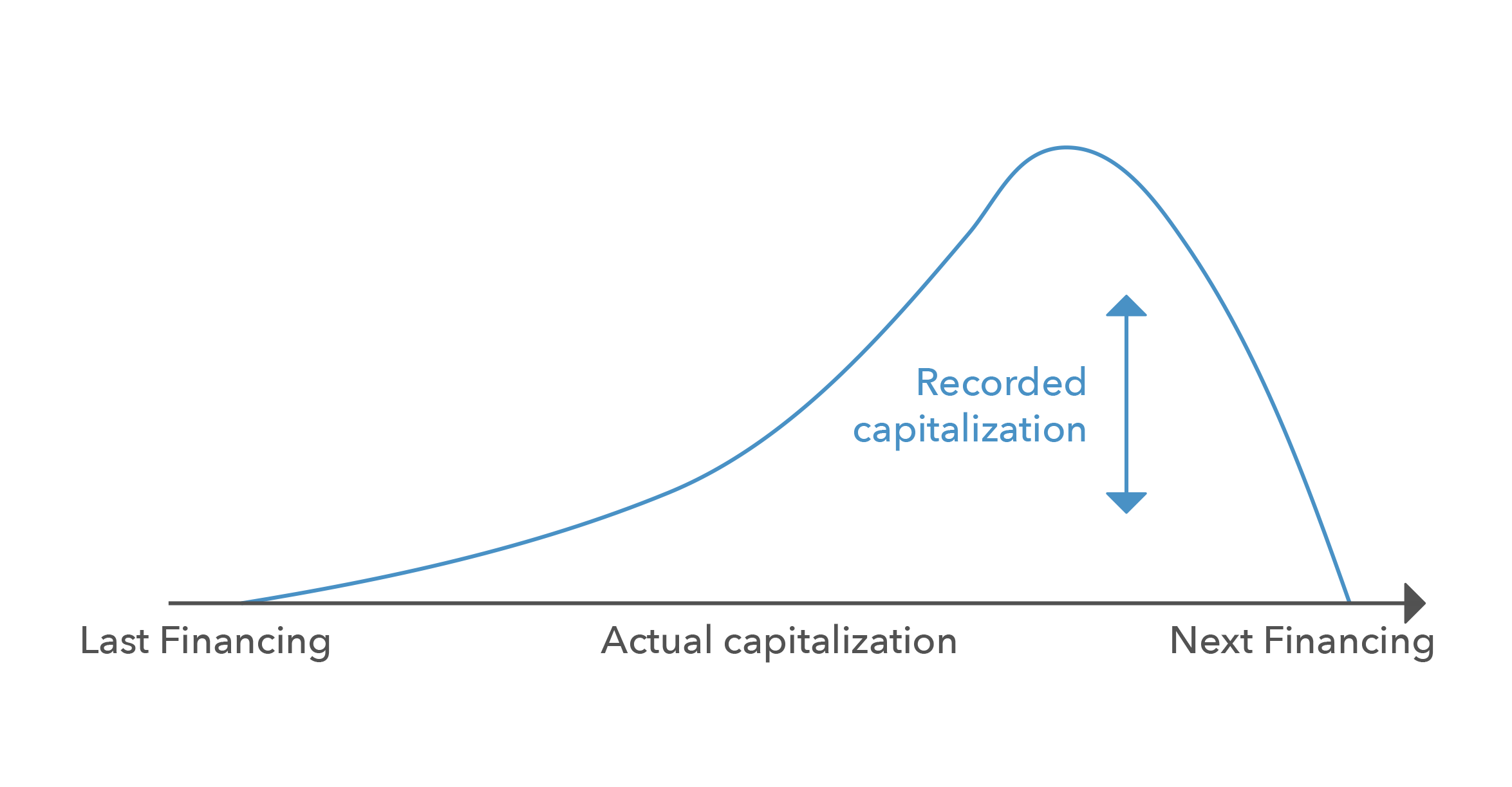

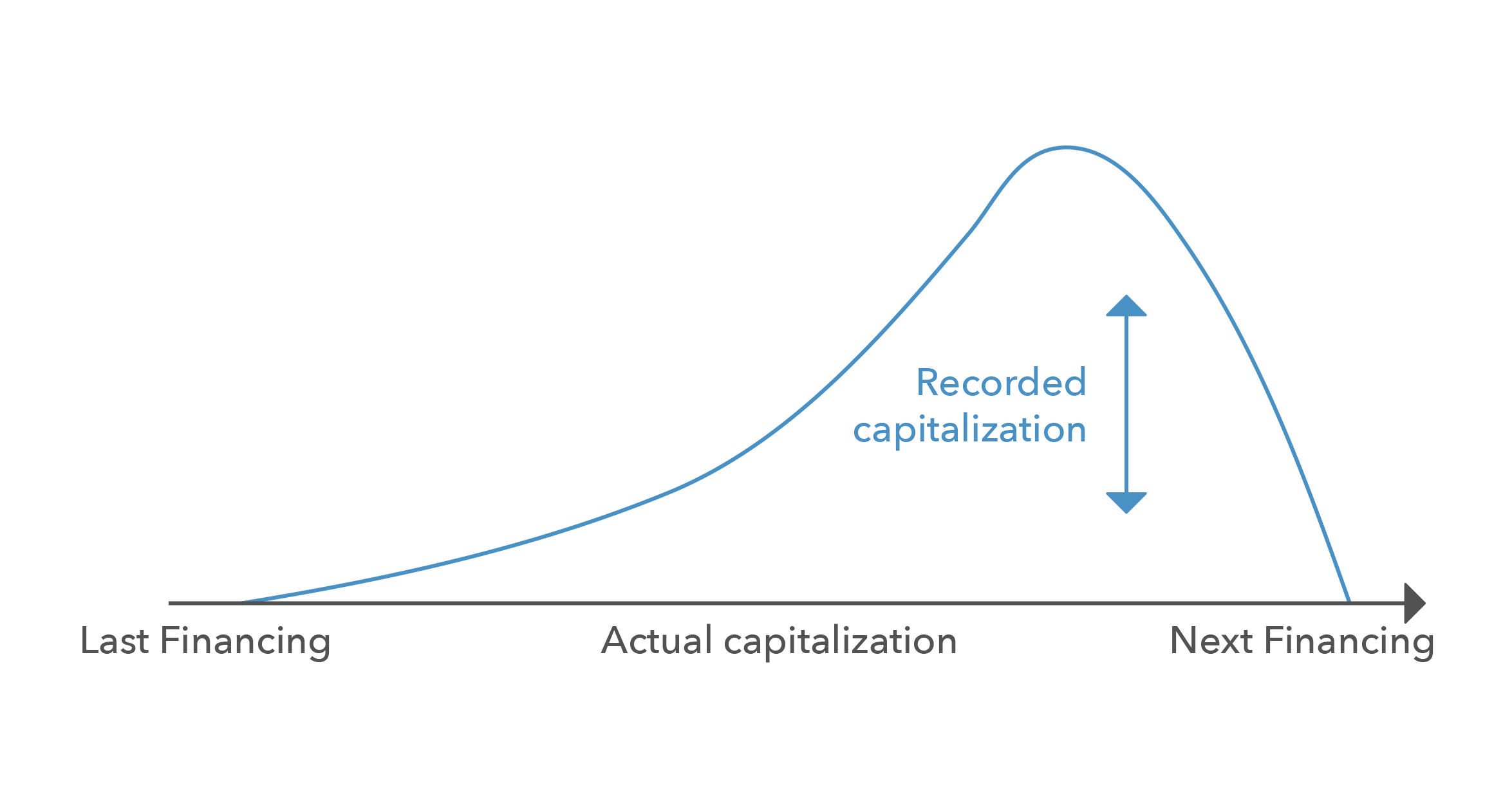

Cap table entropy grows between financings.

Entropy is amplified by the legal cost of maintaining the cap table. Law firms are pressured to defer cap table maintenance to a financing round when it is more natural to charge for clean up time. Capitalization table clean-up still costs up to $15K. And the cleanup is usually the majority of an early-stage company’s legal bill.

We continue to see a lot of mistakes. Vesting schedule errors are the most ubiquitous. We find terms where the wrong vesting schedule is used, the schedule is ambiguous, or the math doesn’t add up. Mistakes enter the legal documentation often and spread like memes through copy and paste. And because terms are captured in language rather than formulas they are difficult to verify. It is funny that mathematical expressions like vesting schedules, liquidation preferences, conversion ratios, and acceleration provisions are defined in prose. Generating a spreadsheet of vesting events would be more precise and less ambiguous than writing paragraphs.

Investors don’t track their shares

Cap table errors are a natural side effect of a manually recorded ledger without counter-party verification. Think of a cap table as a blockchain of a company’s liabilities. Every stock certificate, option grant, exercise, transfer, or debt issue is a transaction that updates the ledger. Every transaction should be verified by the counterparty and the network as a whole. And by network I mean all stakeholders in the cap table who are required to verify the aggregate correctness (fully diluted count) of the table.

When railroads were startups, stock certificates were the original “miners” for recording investments. They were the proof-of-work of the transaction for both parties. The issuer knew that few people had the resources to print an original watermarked copy of a stock certificate. Today you can buy a book of certificates and run them through a printer and they still serve as confirmation of the transaction, albeit a poor one.

The last vestigial use case for stock certificates is at an acquisition or IPO. The paying agent or transfer agent usually require investors to submit stock certificates as a check against the cap table record before transferring money. This is why institutional funds make a big deal about receiving stock certificates. They don’t get paid without them.

The majority of investors (especially angel investors) not on Carta never receive certificates. Delaware C-Corps frequently do not meet their legal obligations to issue stock certificates. Usually, the issuer’s law firm (not the investors) will tell shareholders they are holding the stock certificates for safe-keeping. There are obvious practical issues with this arrangement.

The other big problem with stock certificates as a two-sided record transaction is that the certificates don’t track the percentage ownership. An investor may know the number of shares but they don’t know the denominator. This is especially problematic when companies start doing things like splits and recaps.

It is standard practice not to issue new stock certificates after a stock split. Early investors of companies that have multiple stock splits have no idea how many actual shares they own in the current capitalization. At a liquidity event the shareholder has no way of knowing between which split the certificate was issued and what the multiplier or divider should be.

There are many semi-famous disaster stories of broken cap tables and lost stock certificates. There is the urban legend of Larry Ellison’s ex-wife putting up a $20M bond for her lost Netsuite stock certificate. More recent is the $100M cap table mistake by Tibco and the DTCC losing some of the 3.7M stock certificates they held during Hurricane Sandy. But as bad as these mistakes are for equity investors, it is worse for debt-investors.

Employees suffer most

Sam Altman described four problems with employee equity. I would like to add a fifth — the practice of equity administration is systemically biased against employees. Three examples:

Tax benefits are not offered to employees because processing early – exercise paperwork is too expensive

Former employees are not given an easy way to exercise options after termination

Employee-shareholders are treated as second-class to investor-shareholders

Tax benefits: Employees don’t receive the same preferential tax treatment as founders because most companies don’t allow them to exercise options early. Early exercise is especially valuable to early employees who have low strike prices in-line with the founder’s purchase price. It costs about $200–$300 per exercise in paralegal time to create the paperwork and stock certificates.

It is important to understand that the company is not the other side of the transaction i.e. it doesn’t cost them anything. The government provides the rebate via preferential tax treatment. Early exercise is a compelling option to early employees but most companies don’t allow it because of legal fees. If 10 early stage employees early exercise it would cost $2K-$3K. Better then to not allow it.

Former employees: Departing employees typically have 90 days to exercise their options or lose them. Approximately 6% of these employee option grants are exercised. The vast majority are forfeited and recycled back into the company’s option pool.

Employee-shareholders: A company has an economic and fiduciary duty to assist employees with understanding, valuing, and realizing their options. Shareholders are different. They are expected to care for themselves. Most employees have never been a private company shareholder and don’t understand their options or rights. Investors often co-invest alongside colleagues and friends, giving them a network of other shareholders with similar economic interests. They share information and collaborate both legally and as corporate influencers. They also have fund management attorneys to help guide them. Employee-shareholders don’t.

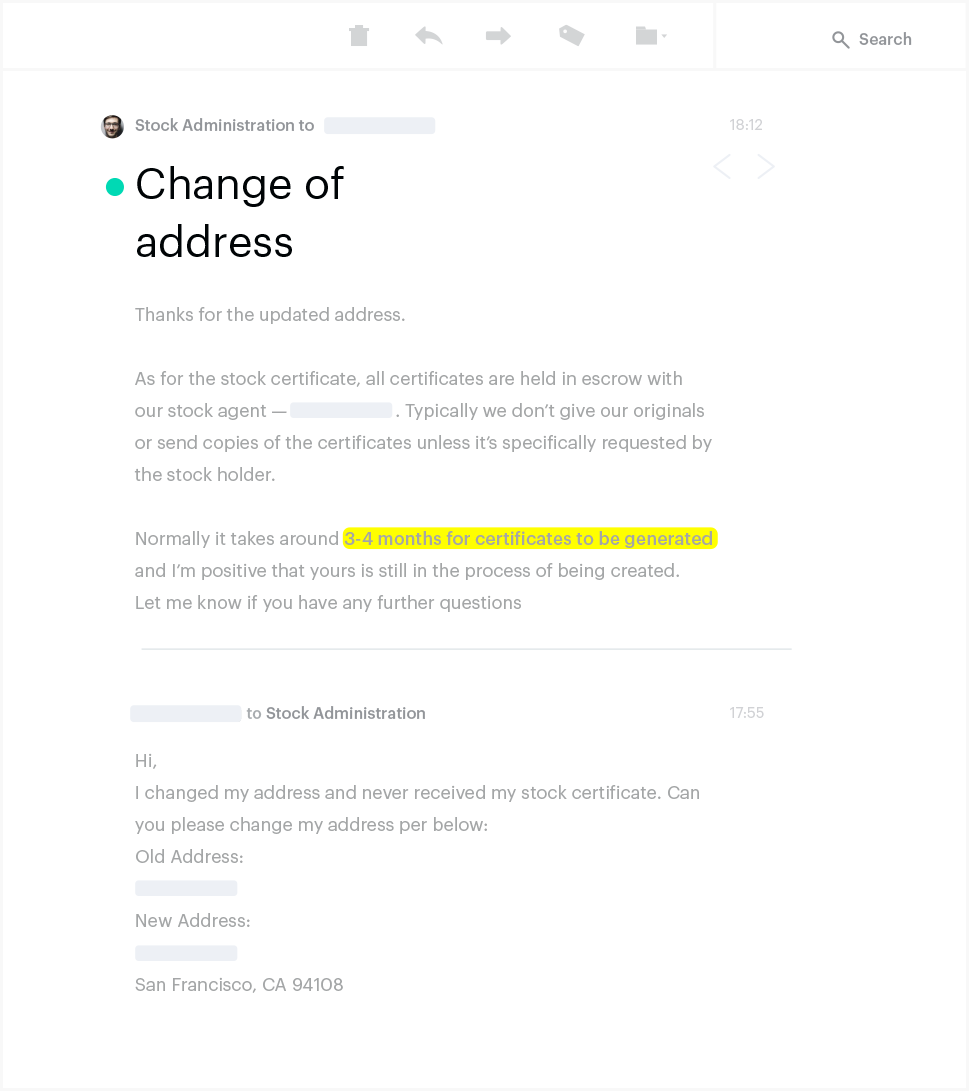

In situations where companies still maintain physical stock certificates, employees are in a weak position when they want proof of their ownership. They have little recourse or influence compared to investors. Below is an email from a former employee of a late-stage venture-backed company asking for his stock certificate after exercising.

Employee-shareholder asking for proof of ownership

The future

It is hard to envision a future where investments are recorded in Excel and stock certificates are kept in a filing cabinet. Admittedly, I am surprised that the current system has worked for this long. What is more surprising is that early-stage companies continue to operate this way. There is something paradoxical about funding companies building virtual reality, autonomous drones, and Bitcoin markets using Excel and paper certificates to track their ownership.

In concluding this piece three years ago, I wrote:

“It is easy to describe the problem but harder to predict how it will be solved. However, it is safe to say the days of Excel and paper stock certificates are numbered. It can’t scale with the growth of investment activity. The system will break. The question is what will replace it and when. Time will tell. Hopefully Carta will be part of the answer. But even if it isn’t us, somebody else will fix it. They just have to.”

Carta had less than 500 clients in January 2015. In three years, almost 7,500 new companies have joined our network. We have over 500,000 founder, investor, and employee shareholders that know their specific ownership percentage and can be confident that their holdings are accurate. We’ve strengthened the integrity of our network. So, yes, we have begun to replace the antiquated record of ownership for private companies. But the fact remains that cap tables are still broken.