Issue, track, and process payments for your company's equity securely

Enter audits with confidence with tailored, cost-effective valuations

Issue SAFEs, collect signatures, and move money securely on one platform

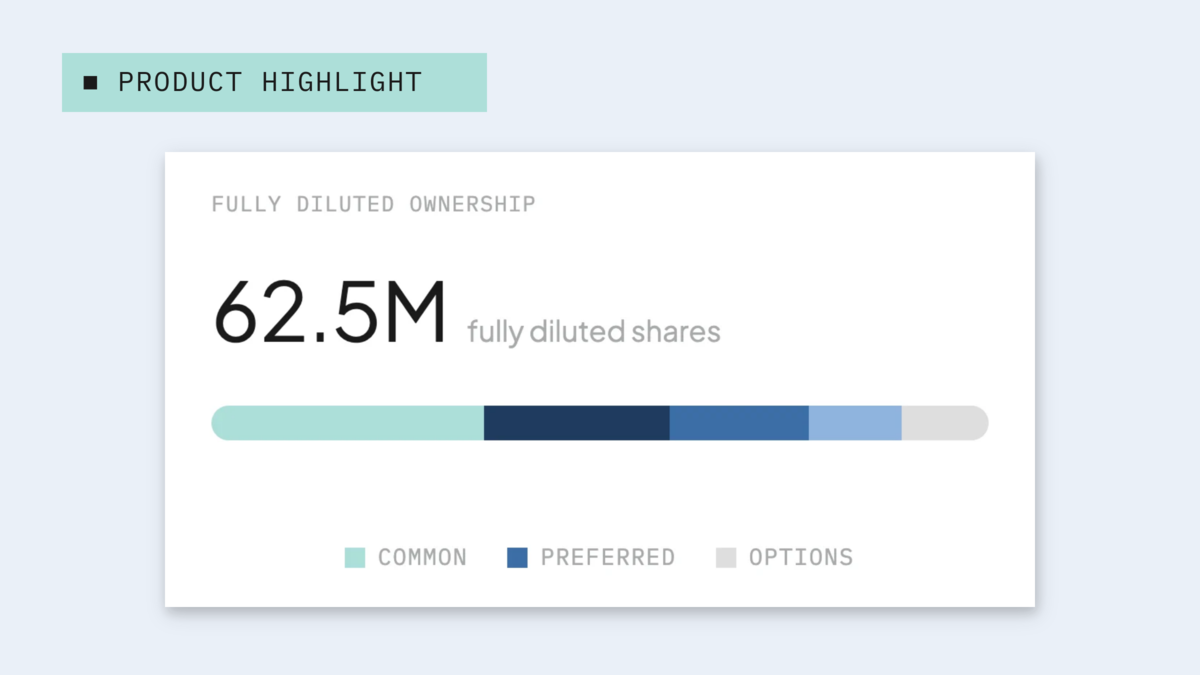

Generate your latest stock-based compensation reports in a few clicks

Empower your team with actionable tax and equity knowledge from real experts

Get reliable salary and equity benchmarks for every role, level, and region

Execute secondary transactions that fully integrate with your cap table

Optimize your equity tax benefit with the Qualified Small Business Stock (QSBS) tax exemption

Launch, scale, and manage a Carta 401(k), powered by Vestwell and Morgan Stanley

Automate your back office with solutions from reporting to closings

Guide your fund's strategy with data-driven precision from forecasting to modeling

Unlock a seamless tax season with your fund accounting and taxes in one place

Unlock accurate valuations with centralized data collection, calculations, and reporting

Form, close, and administer your SPV on a platform build for every investor

Automate every step and workflow with a connected loan solution

Turn your collective network into a deal-winning relationship engine

Centralize investor intelligence and automate your fundraising flywheel

Tap into private market AI to manage your alternative investment data

Capitalize on any investment with access to capital outside your regular call cadence

Run fund admin, portfolio analytics, and valuations in one intelligent system

Drive defensible decisions with automated AML, KYC, and investor onboarding

Eliminate deal friction with AI-powered redlining and rapid contract execution

Simplify complex transfers with a fully managed, expert-led LP transfer service

Transform transactional workflows with an AI-native law firm, powered by our acquisition of Avantia Law

The first unified software suite delivering precision and control

Find the solutions you need to drive your business forward at any stage

Scale funds of any size with unified, end-to-end workflows

For early-stage founders to manage equity and build their cap table

Data on how PE-backed firms use equity to attract and retain talent