What’s New, What’s Next: Optimize How You Run, Raise, and Close Your Fund

The MENA Private Markets Playbook: Cap Tables, SPVs, and the Infrastructure Behind the Deal

Australian Budget 2026: New Caps, New Rules and Your Next Move

Introducing Carta Law: AI-Native Legal & Compliance Operations for Private Capital

The Non-Dilutive Capital Stack

Running a Smarter Fund with AI: From Fund Data to Faster Decisions

Congress, Compliance & Venture Capital: A Fund Manager's Guide to the Shifting Policy Landscape

Founder Insights on the New Era of Software as an Action

From First Meeting to Final Close: The Power of a Connected CRM

Capital Is Up. Hiring Is Down. The New Rules of Startup Comp.

PE Compensation Series with Davis Polk, Part 3: Management Rollovers and Incentive Equity Structures for Portfolio Companies

VC Masterclass: Navigating Liquidity and LP Communication in 2026

What’s New, What’s Next: The Connected ERP for Private Capital

Cap Tables and Dilution for Startup Founders

Q1 Venture Capital Review: From SAFEs to Exits

From Paper to Portfolio: The Executive’s IPO Playbook to Shift from Private‑to‑Public

FA Certification Program

![[VE Cover] Automating the Middle Office: Solving the Data Gap Between Assets and LPs](https://images.ctfassets.net/y88td1zx1ufe/79w0VzZzj9moQYLbuMKF2k/6a64dd1a6d094c4d09c9cc1d5aec3c27/Event_Cover.png)

Driving Digital Transformation in the Middle Office

Startup Taxes 101: Strategies for Navigating Equity and Startup Growth

![[VE Image] Driving Fund Decisions with Visual Accounting](https://images.ctfassets.net/y88td1zx1ufe/5salNQS8FnIpHXqV96lf1Q/dc17483e377a661f97ad163396c97864/20260219_VisualAccountingVE_EventCover.png)

Driving Fund Decisions with Visual Accounting

![[VE] Fundraising in 2026: Benchmarks, Trends, and What’s Different Now](https://images.ctfassets.net/y88td1zx1ufe/42AfmTCJPSb47uULKTDwlX/62da89c6fac105977816a73d4754703b/Event__1200x675___2_.png)

Fundraising in 2026: Benchmarks, Trends, and What’s Different Now

The 2026 Comp Playbook: Precision Budgeting, AI Skills, and Data-Driven Hiring

Fund Economics: Demystifying Operations, Fees, and Expenses

RAISE Emerging Manager Fund Analysis

What's New, What's Next: Delivering Firm-wide Clarity

The Liquidity Blueprint: How Secondaries Are Shaping Africa’s Private Markets

Inside Carta FA: Driving Efficiency in Fund Operations and Investor Relations

The New Dynamics of Venture, Private Equity, and Credit: Five Trends Shaping the Private Market

Beyond the Spreadsheets: Achieve Clarity with LP Portfolio Analytics

VC Masterclass: Sourcing and Nurturing LP Relationships

PE Compensation Series with Davis Polk & Ownership Works: The Power of Broad-Based Ownership in Private Equity

VC Fund Performance 2025

Unlock Fast, Audit-Defensible Portfolio Valuations

Startup Taxes 101: Tax Essentials for Every Founder

Navigating the New QSBS to Maximize VC Gains

![[VE] The Modern Audit Playbook: Roles, Valuations, and Platform Power](https://images.ctfassets.net/y88td1zx1ufe/6beSyqWJ2kSmEy7vUJ7GmG/68a58917950b14690b1c167b362a3f33/Speakers__1200x675___87_.png)

The Modern Audit Playbook: Roles, Valuations, and Platform Power

![[VE] Tax Ready, Already: A New Standard for Fund Taxes, Powered by AI](https://images.ctfassets.net/y88td1zx1ufe/q1XUdQDaFT4nGjt1Goyl0/94c33aacc89f7fdf180c9a34aa621bdc/Speakers__1200x675__20250925_TaxVE.png)

Tax Ready, Already: A New Standard for Fund Taxes, Powered by AI

Transform Tax Savings into Startup Growth with QSBS

![[VE] Startup Compensation in H1 2025](https://images.ctfassets.net/y88td1zx1ufe/2b3ZZDAU8Xnvh5djBwEAqG/f12275d7d744453678ad552fb6de40a7/Speakers__1200x675___82_.png)

Startup Compensation in H1 2025

What’s New, What’s Next: The Future of Visibility and Control in Fund Accounting

Driving Operational Speed, Accuracy, and Scale Through Integrated Fund Admin Workflows

Q2 Venture Capital Review: Startup Rebound?

Founder’s Journey 101: Preparing for a Strategic Exit

Unlock Firm Insights and Clarity with Carta’s Data Warehouse

VC Masterclass: Setting a Target Fund Size

How to Construct Your Fund for Long-Term Success

VC Fund Performance Q1 2025

A VC & Founder’s Journey from Fundraising to Strategic Partnership

How to Map Your Investment Structures with Carta

What's New, What's Next: Building Connected Fund Admin

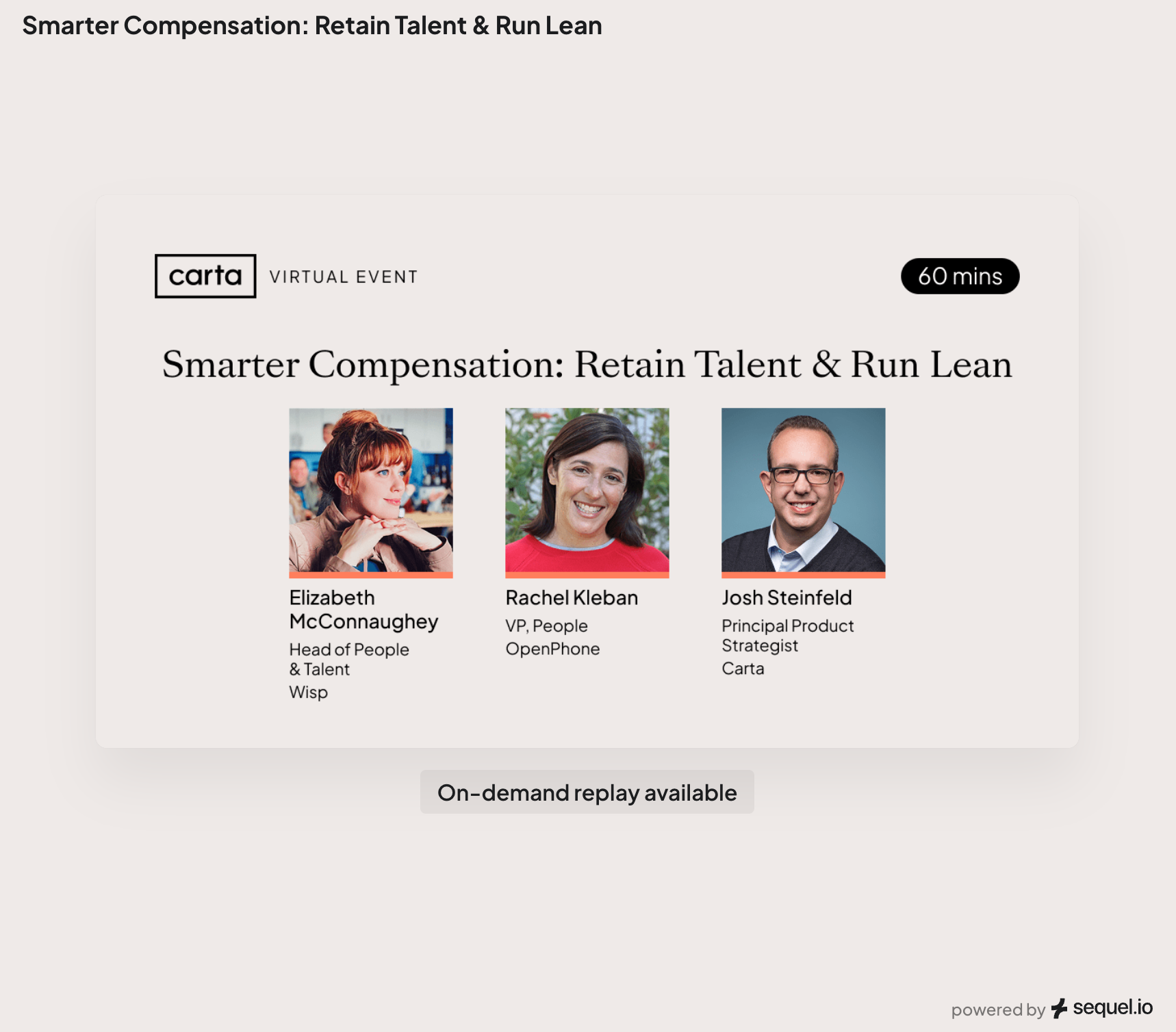

Smarter Compensation: Retain Talent & Run Lean

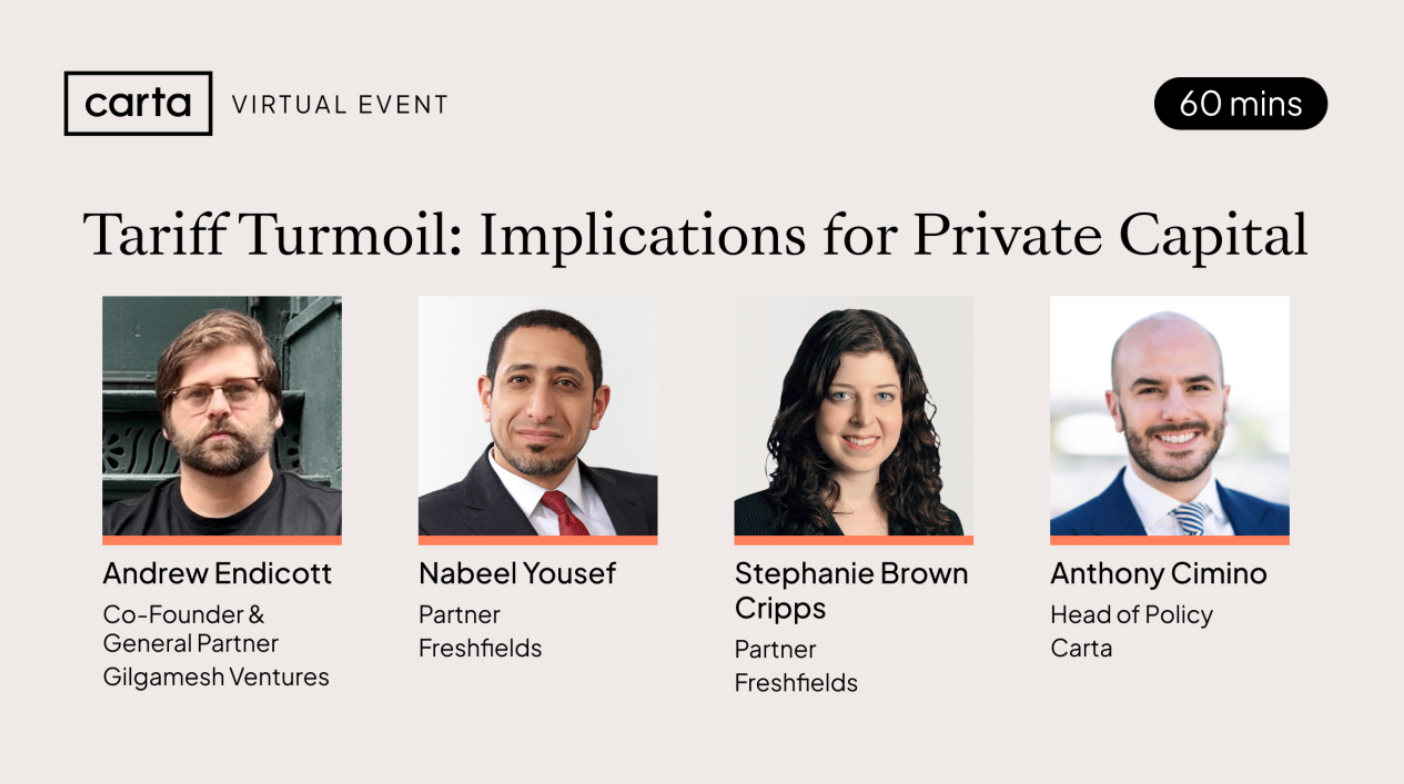

Tariff Turmoil: Implications for Private Capital

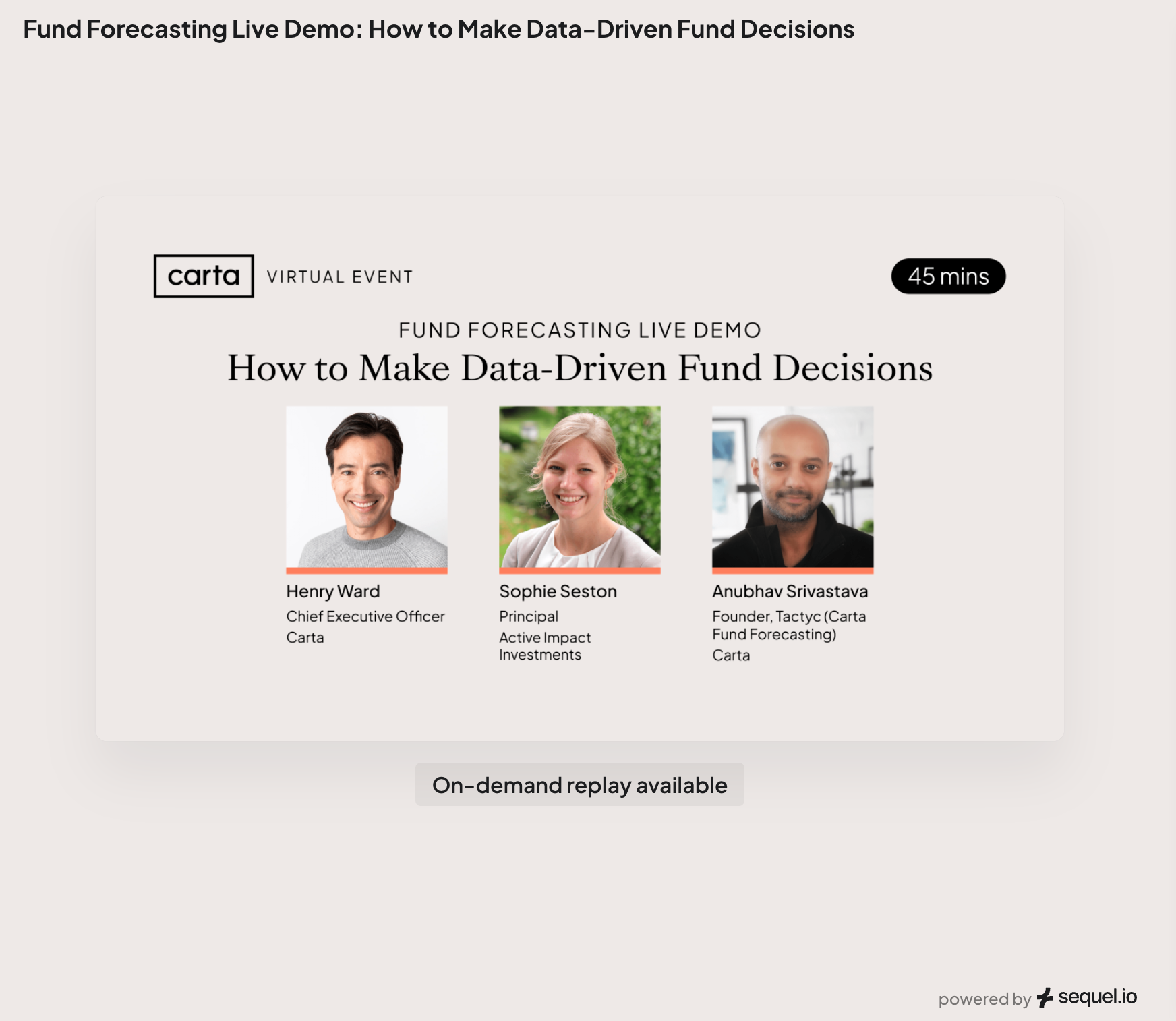

Fund Forecasting Live Demo: How to Make Data-Driven Fund Decisions

IPO Readiness in 2025: Market Signals, Timing, and Looking Ahead

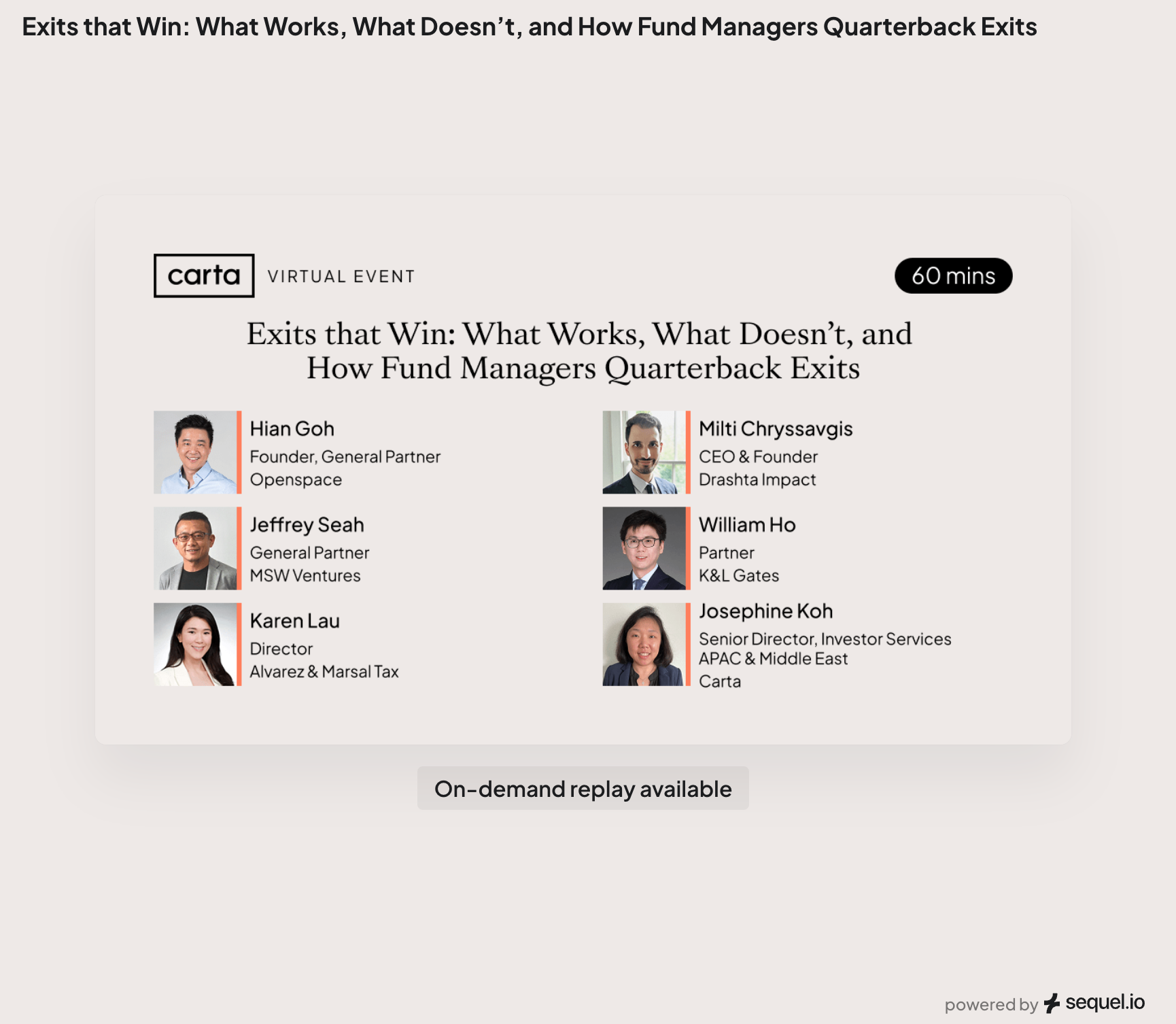

Exits that Win: What Works, What Doesn’t, and How Fund Managers Quarterback Exits

Private Equity Portfolio Companies & Funds: Connecting the Dots for the Audit Cycle

PE Executive Equity: Data-Backed Insights

Tax Season Recap & What’s Next for Startup Taxes

VC Masterclass: Designing a Fund Thesis

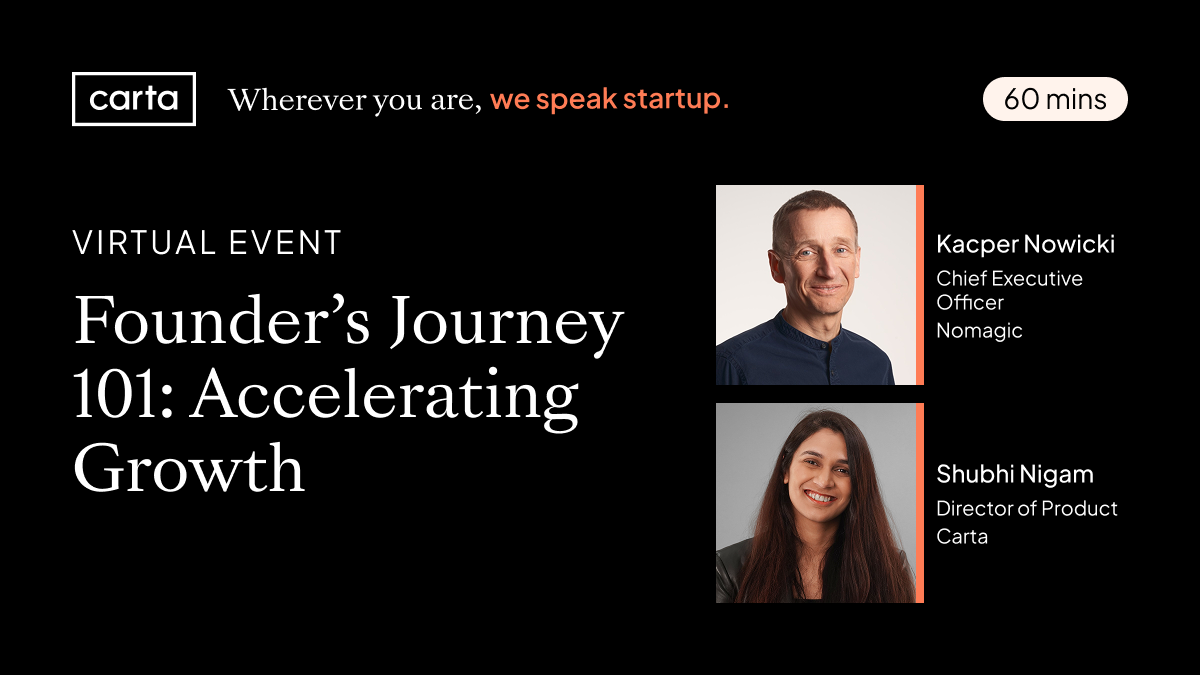

Founder's Journey 101: Accelerating Growth

VC Fund Performance in 2024

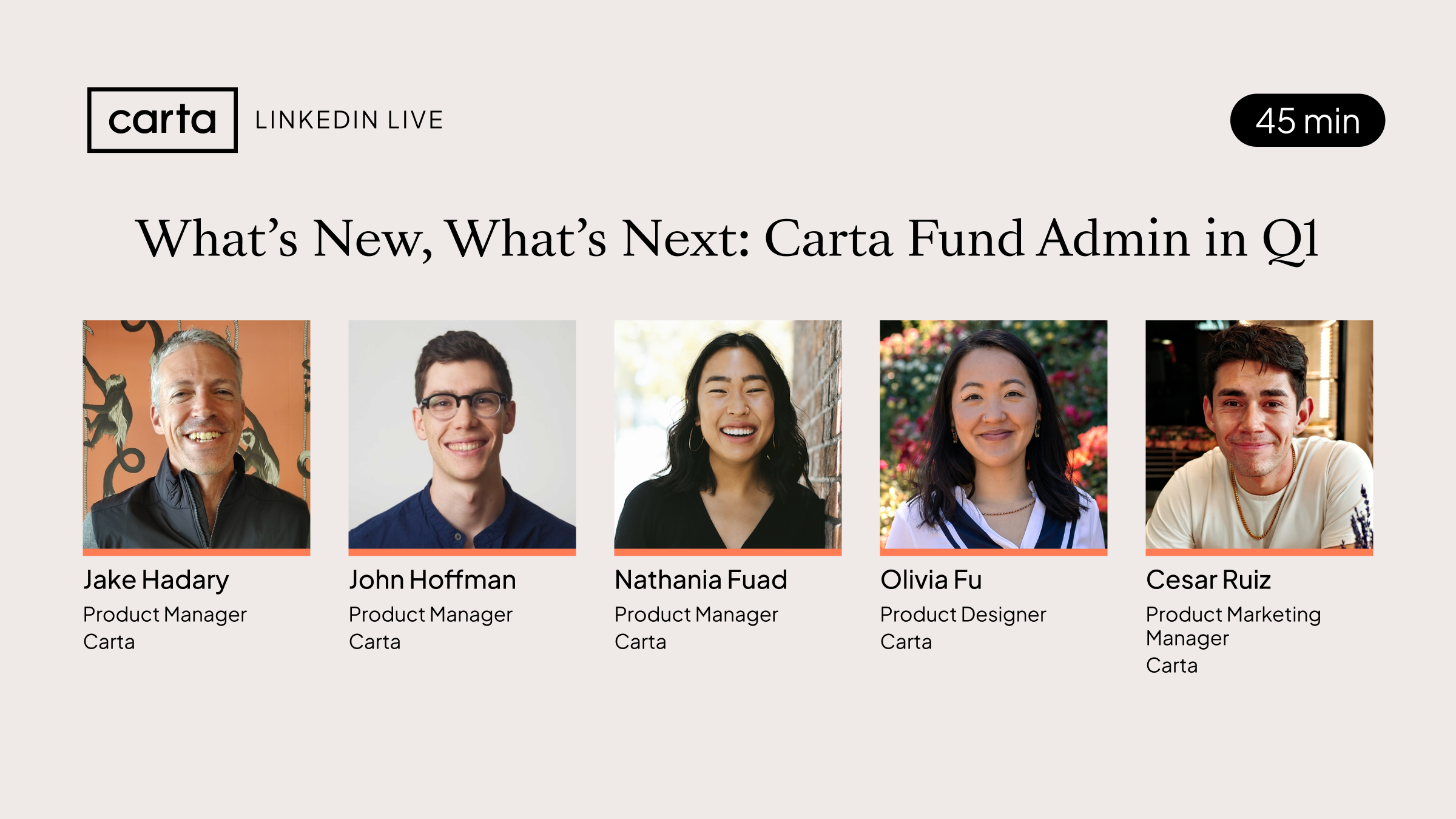

What’s New, What’s Next: Carta Fund Admin in Q1

Founder’s Journey 101: Scaling for Impact in Australia

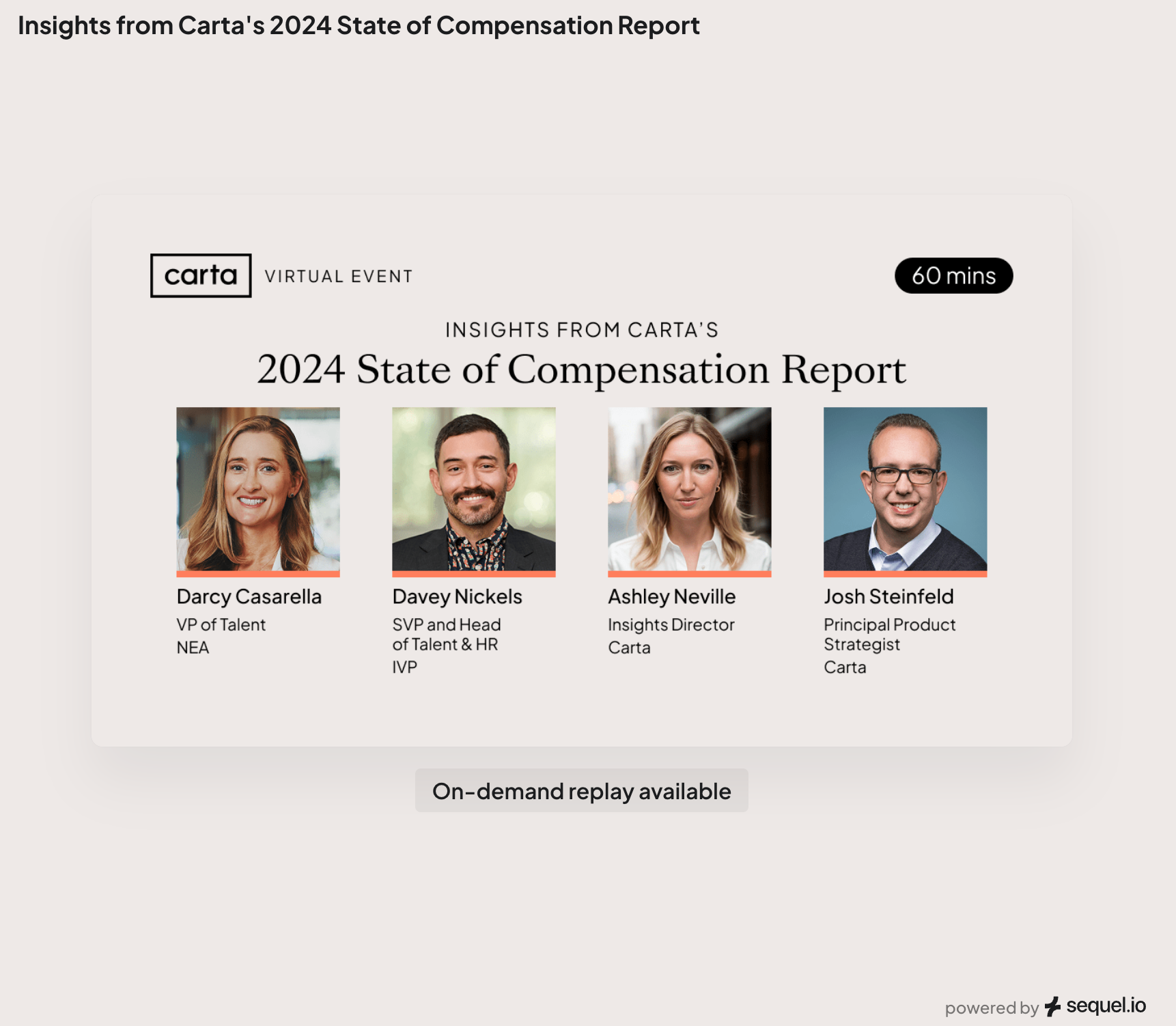

Insights from Carta's 2024 State of Compensation Report

![[Regional Replay] Shaping the Future of Venture Capital: Women in VC](https://images.ctfassets.net/y88td1zx1ufe/2bmzZvEtJoVm5311pVlW8a/6511da5c7c6c180b4442b6ccc3c58556/Screenshot_2026-03-12_at_14.23.01.png)

Shaping the Future of Venture Capital: Women in VC

Shaping the Future of Venture Capital: Women in VC

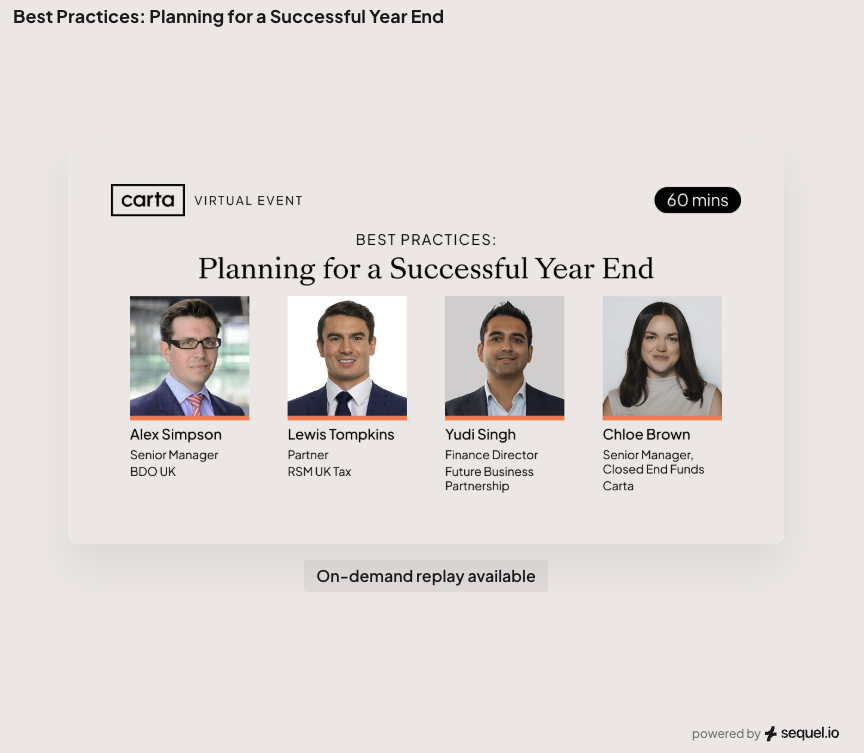

Best Practices: Planning for a Successful Year End

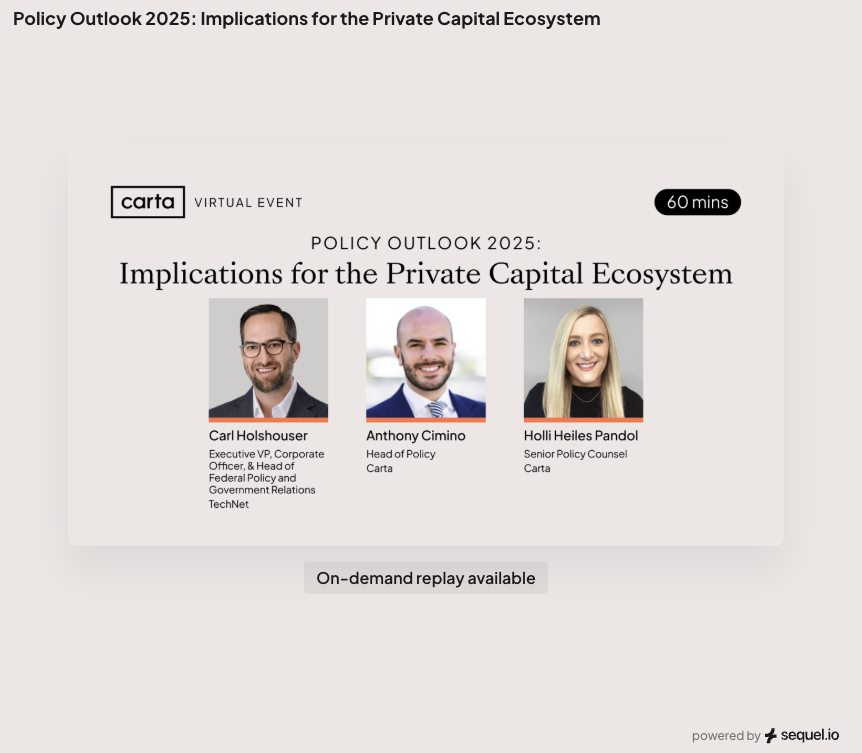

Policy Outlook 2025: Implications for the Private Capital Ecosystem

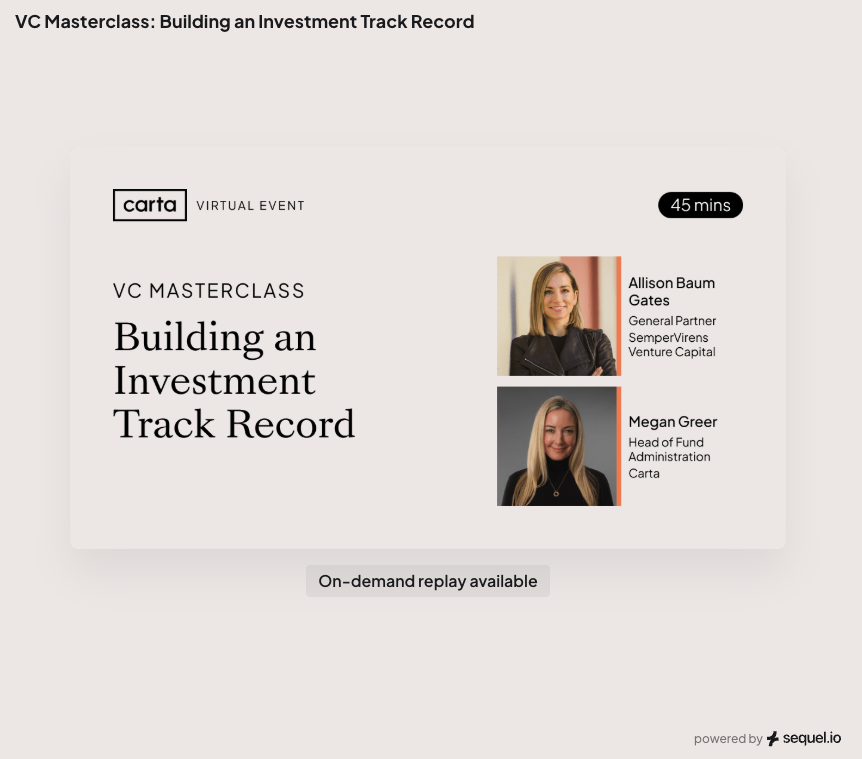

VC Masterclass: Building an Investment Track Record

Singapore The Global Hub: 2025 Regulatory and Tax Changes for Fund Managers

2024 Venture Capital Review: Insights and Implications for the Coming Year

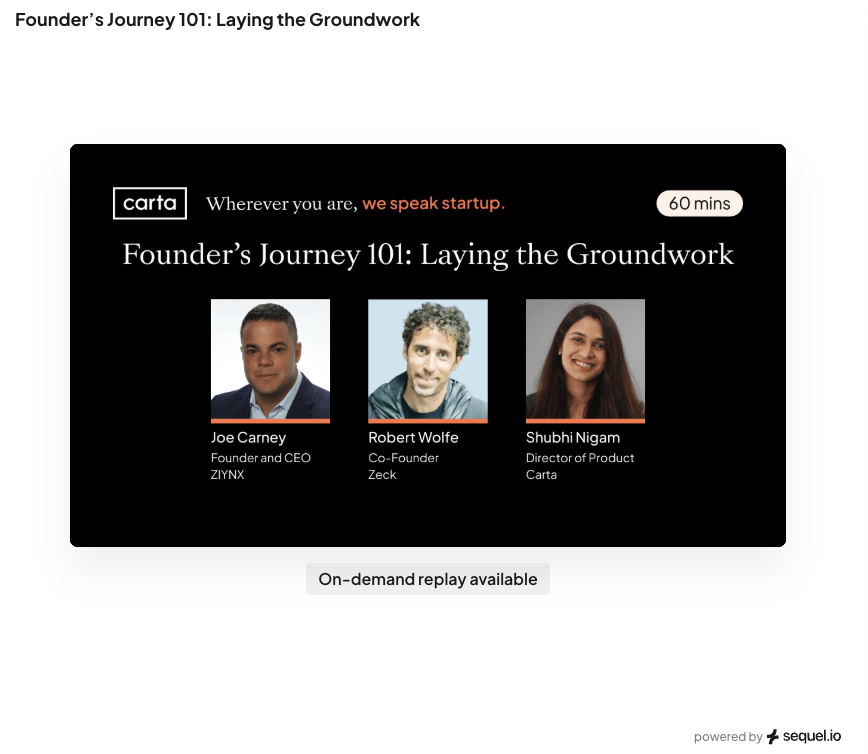

Founder’s Journey 101: Laying the Groundwork

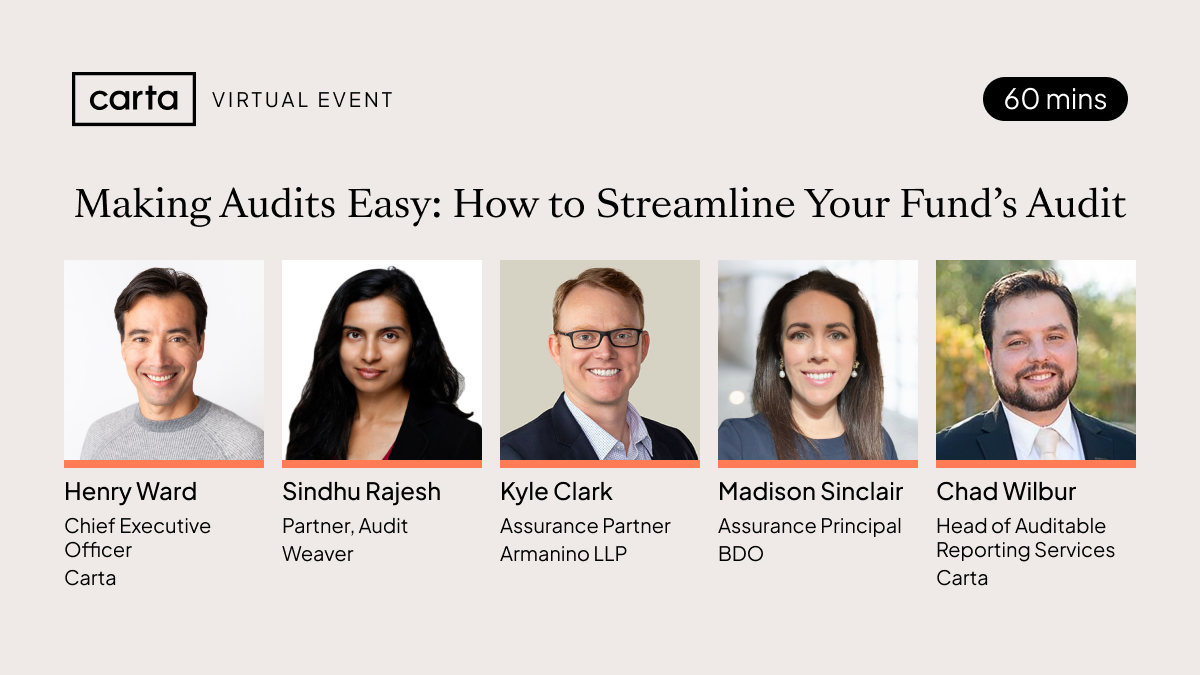

Making Audits Easy: How to Streamline Your Fund’s Audit

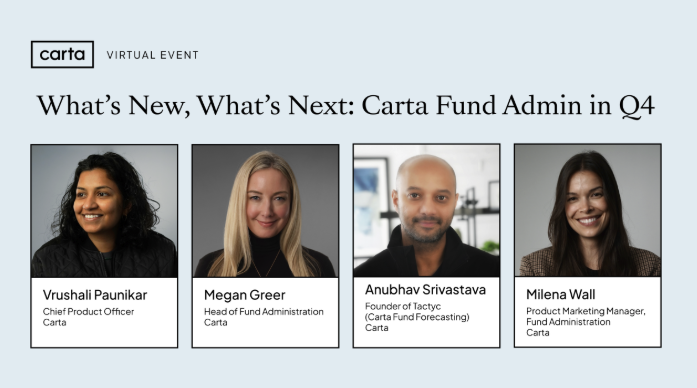

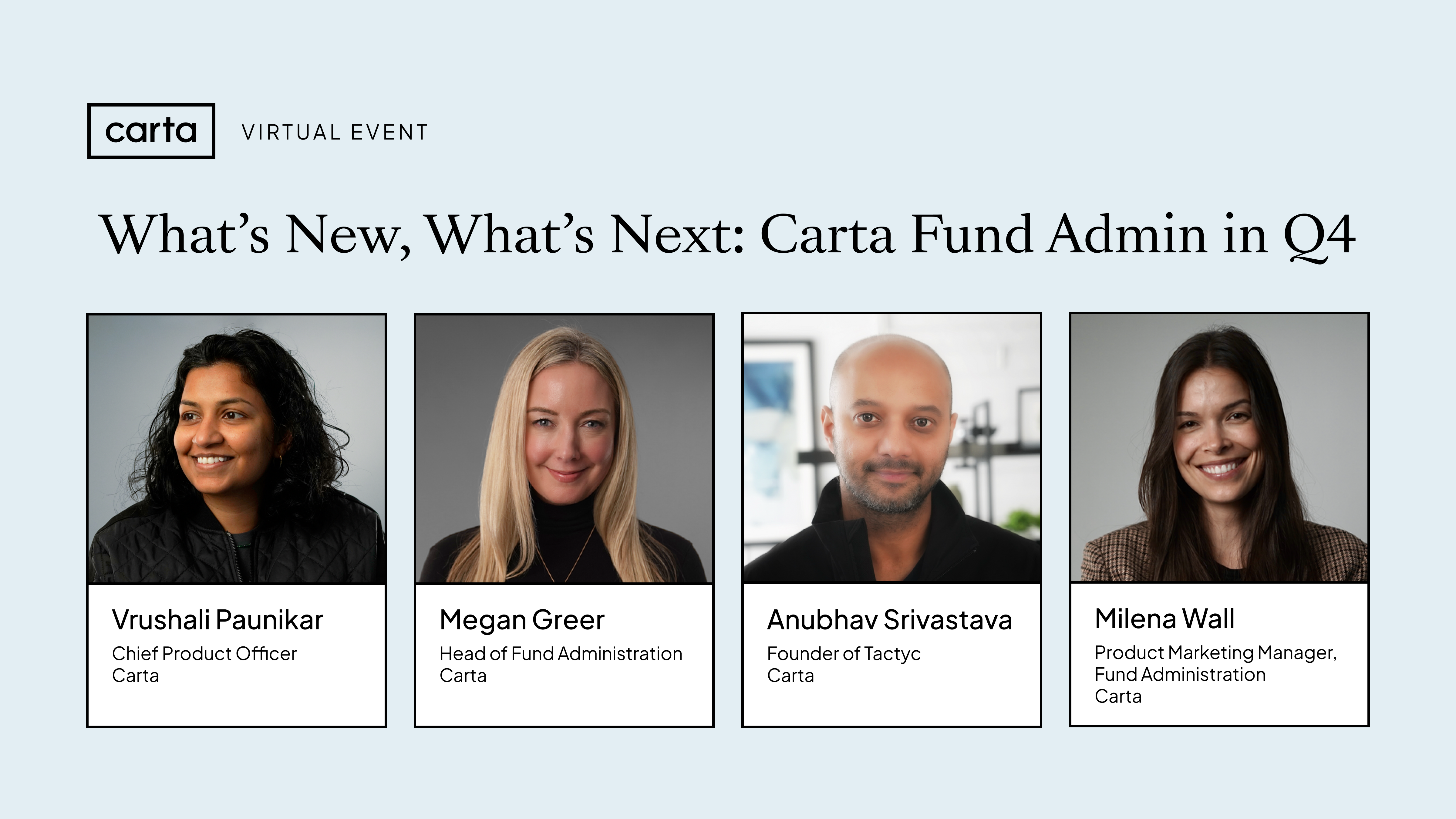

What’s New, What’s Next: Carta Fund Admin in Q4

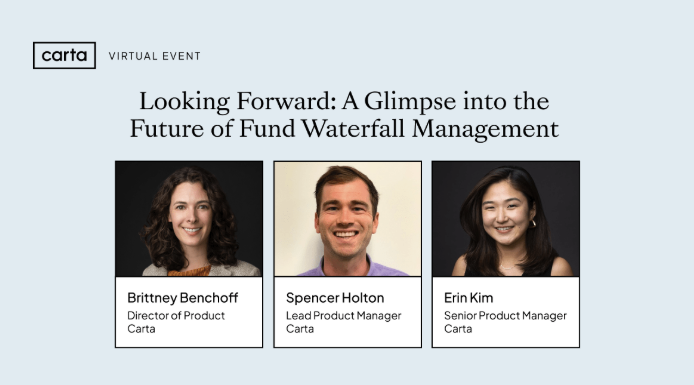

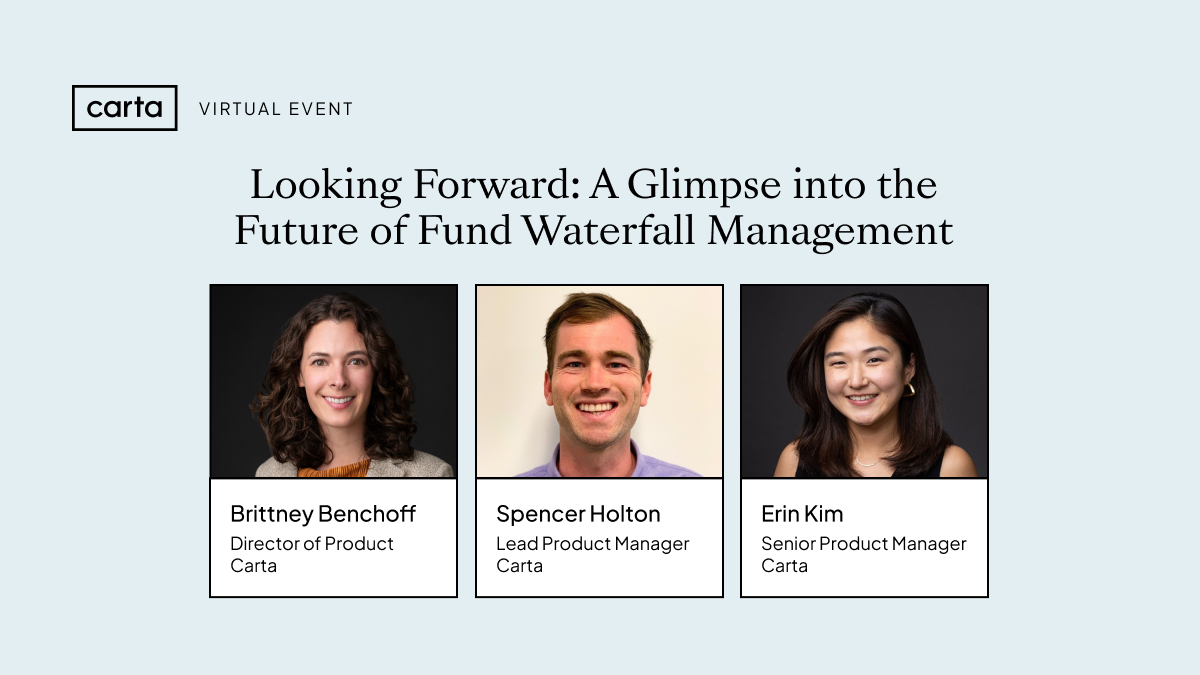

Looking Forward: A Glimpse into the Future of Fund Waterfall Management

Election 2024: Policy Implications for the Private Market Ecosystem

2024 Fund Performance Data: A European Perspective

Fund Forecasting Demo

State of Private Markets: End of Year Predictions

The Lifecycle of a Private Equity Deal with Weil

Essential Tools for Startup Success: QSBS Attestation

Essential Tools for Startup Success: Elevate Your Compensation Strategy

![[Bonus Event] Startup Fundraising 101: Close Your Priced Round with Confidence](https://images.ctfassets.net/y88td1zx1ufe/47l09aZJnak15MVm54yYNh/8a5b4a22f9be6c7b24c0b506116bb44a/Screenshot_2026-03-13_at_17.24.41.png)

[Bonus Event] Startup Fundraising 101: Close Your Priced Round with Confidence

Audit Mastery: The Essentials You're Not Thinking About

Healthcare and Life Sciences: Growth and Funding Insights

Best Practices: How to Prepare for Year-End (Audit & Tax)

Startup Fundraising 101: Post-funding Success

Value Creation through Employee Equity: Insights from the 2024 Private Equity Ownership Trends Report

Deep Dive: European Data Insights

The Startup Guide to UK Fundraising: EIS and SEIS

What’s New, What's Next: Carta Fund Admin in Q3

VC Fund Performance: New Benchmarks for 2024

Founders Guide to Board Management

Equity Compensation: Three Essentials You're Not Thinking About

Preparing for EOY: Get Ahead of Your Next Audit

Startup Compensation in 2024

GP Secrets: Fundraising & Investing in the Middle East & Asia Pacific

Pre-Seed Fundraising: Fresh Data from Q2 2024

Policy Playbook: How the 2024 Election Could Shape Private Market Policy

Essential Tools for Startup Success: Equity Management

Carta | NYSE: Getting Your Company IPO Ready

Startup Fundraising 101: Crafting a Winning Pitch

Policy Briefing: What Does the UK Election Mean for VC?

First Close: From Managing SPV’s to Launching a Fund

What’s New & What’s Next: Carta Alternative Assets Product Updates in Q2

Forecasting Employee Compensation Accurately

What’s New, What’s Next: Carta Fund Admin in Q2

FA Certification Program: Auditor Portal Overview

FA Certification Program: Fund Tax Process

FA Certification Program - Downloading SOC Reports

FA Certification Program - Scenario Modeling Overview

Business Guide to Taxes: Expiring Tax Incentives

Private Equity Firm Operations: In-House v. Outsourced

Emerging Trends & Key Insights for Asset Allocators

Startup Fundraising 101: Mastering Fundraising Strategy

First Close: Optimising for Your First Close

Advisory Boards Unveiled: Elevating Australian Startups to Global Heights

State of Private Markets: Q1 Venture Spring?

Policy Playbook: Navigating the Shifting VC Regulatory Landscape

Startup Fundraising 101: Building Strategic Partnerships

How Did 2023 Change Valuations?

First Close: Acing Your Fund Operations Stack

Navigating the Corporate Transparency Act as a LatAm Based Business Owner

Pre-Seed Benchmarks: Fundraising Data for New Startups

Building Lasting Limited Partner (LP) Relationships

Best Practices: EOY Tax & Audit Planning

Equity Essentials: Making the Leap From Seed to Series A

Tender Offers 101

What’s New, What’s Next: Carta Fund Admin in Q1

State of Compensation: 2024 Outlook

First Close: Formations

Navigating Opportunities: State of Venture in the Middle East

Corporate Transparency Act: Simplify Filing With Carta

What’s New, What’s Next: Effortless Distributions Modeling

State of Private Markets: 2024 Predictions

Corporate Transparency Act: What Business Owners Need to Know

Unlocking ASC 820 Valuations for Funds: Best Practices & Recent Trends

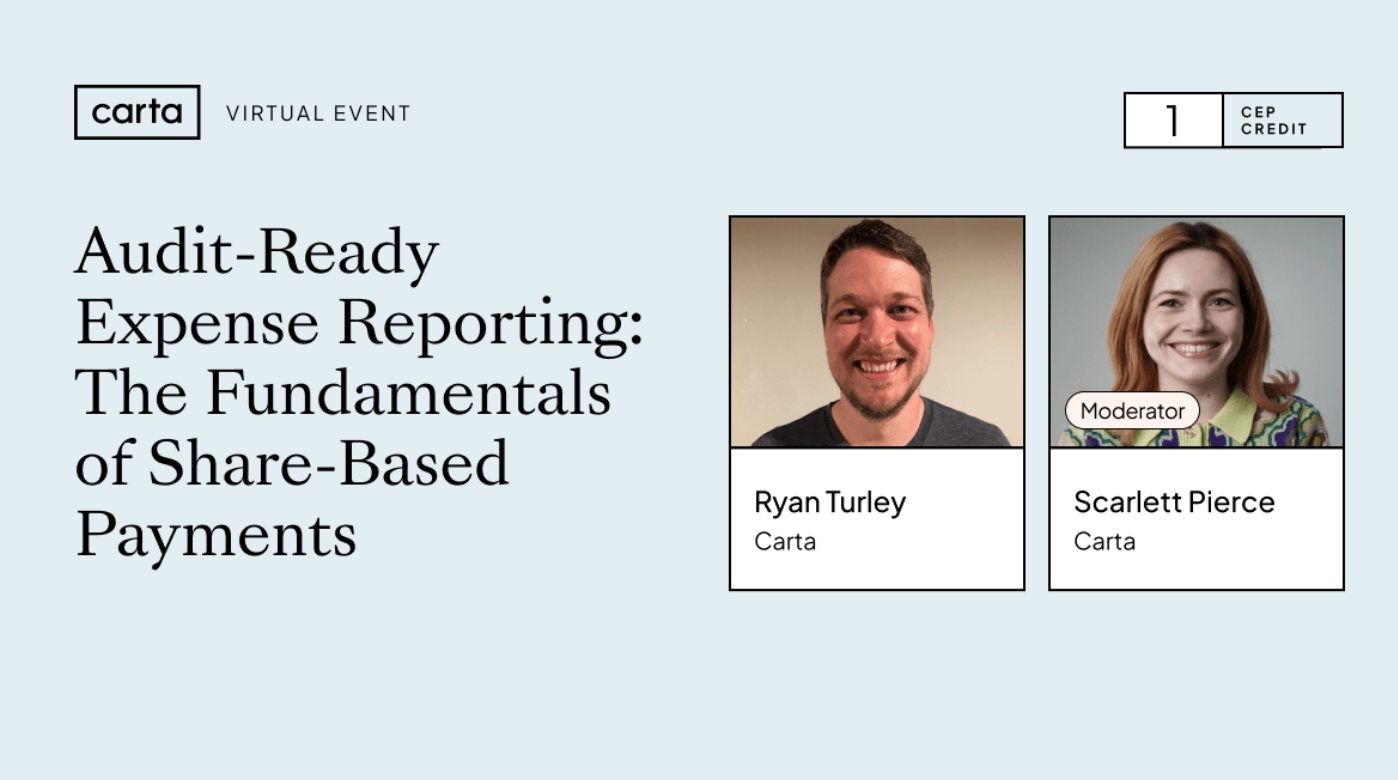

Audit-Ready Expense Reporting: The Fundamentals of Share-Based Payments

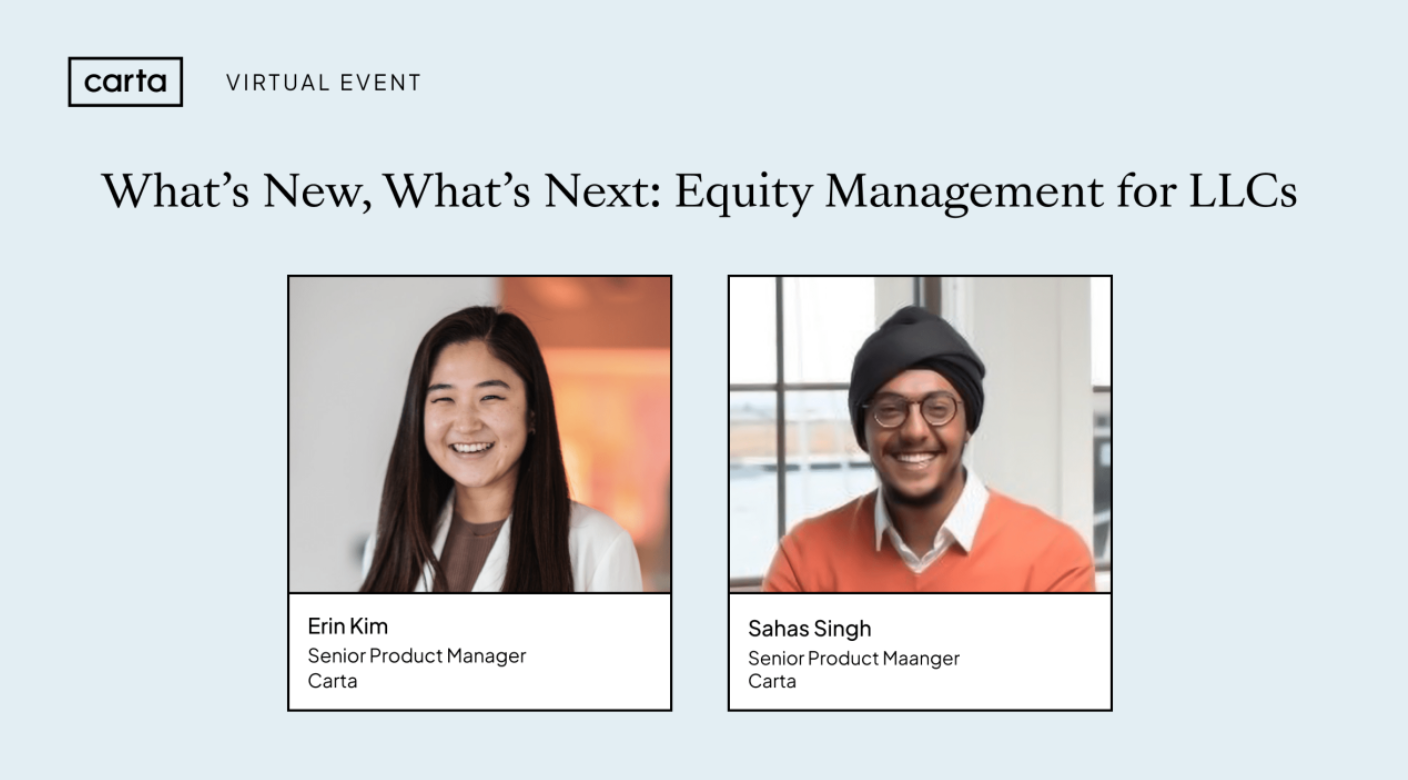

What’s New, What's Next: Equity Management for LLCs

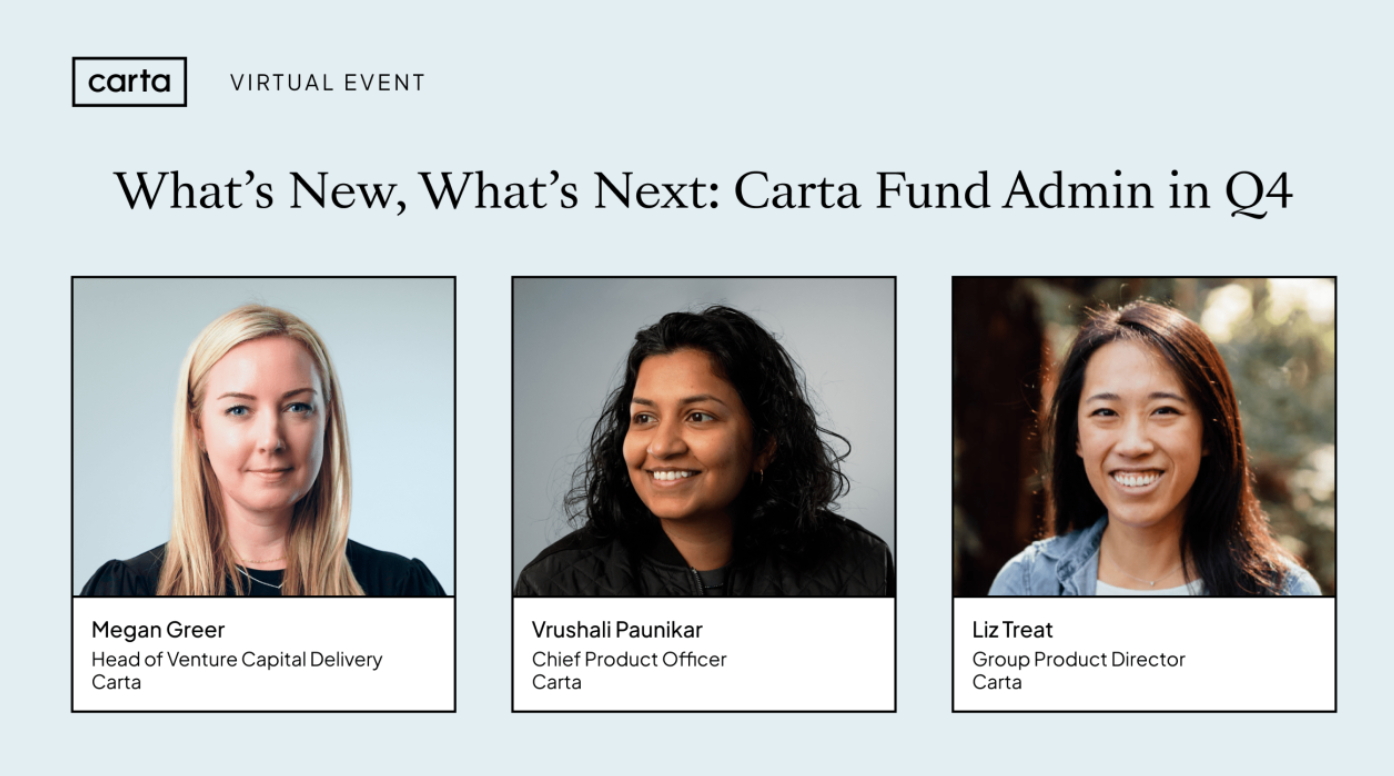

What’s New, What's Next: Carta Fund Admin in Q4

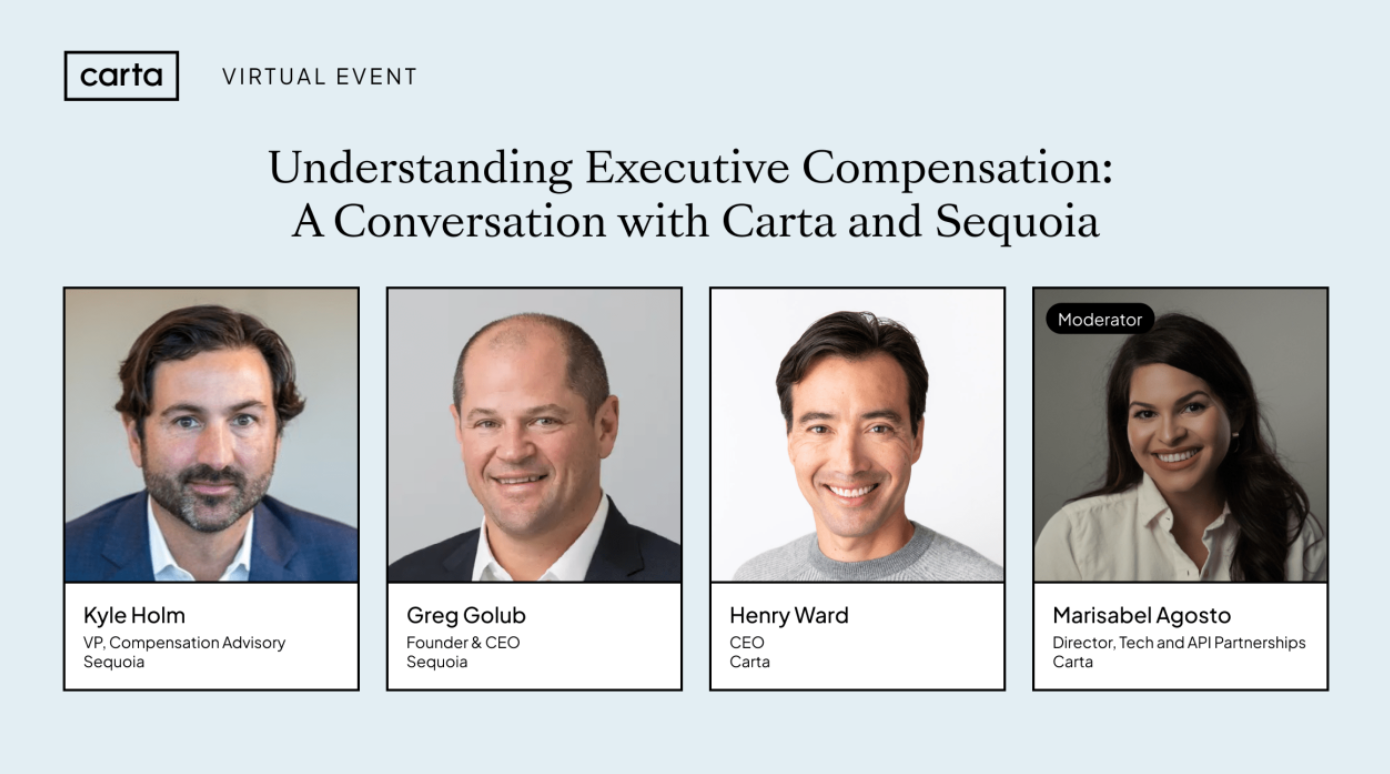

Understanding Executive Compensation: A Conversation with Carta and Sequoia

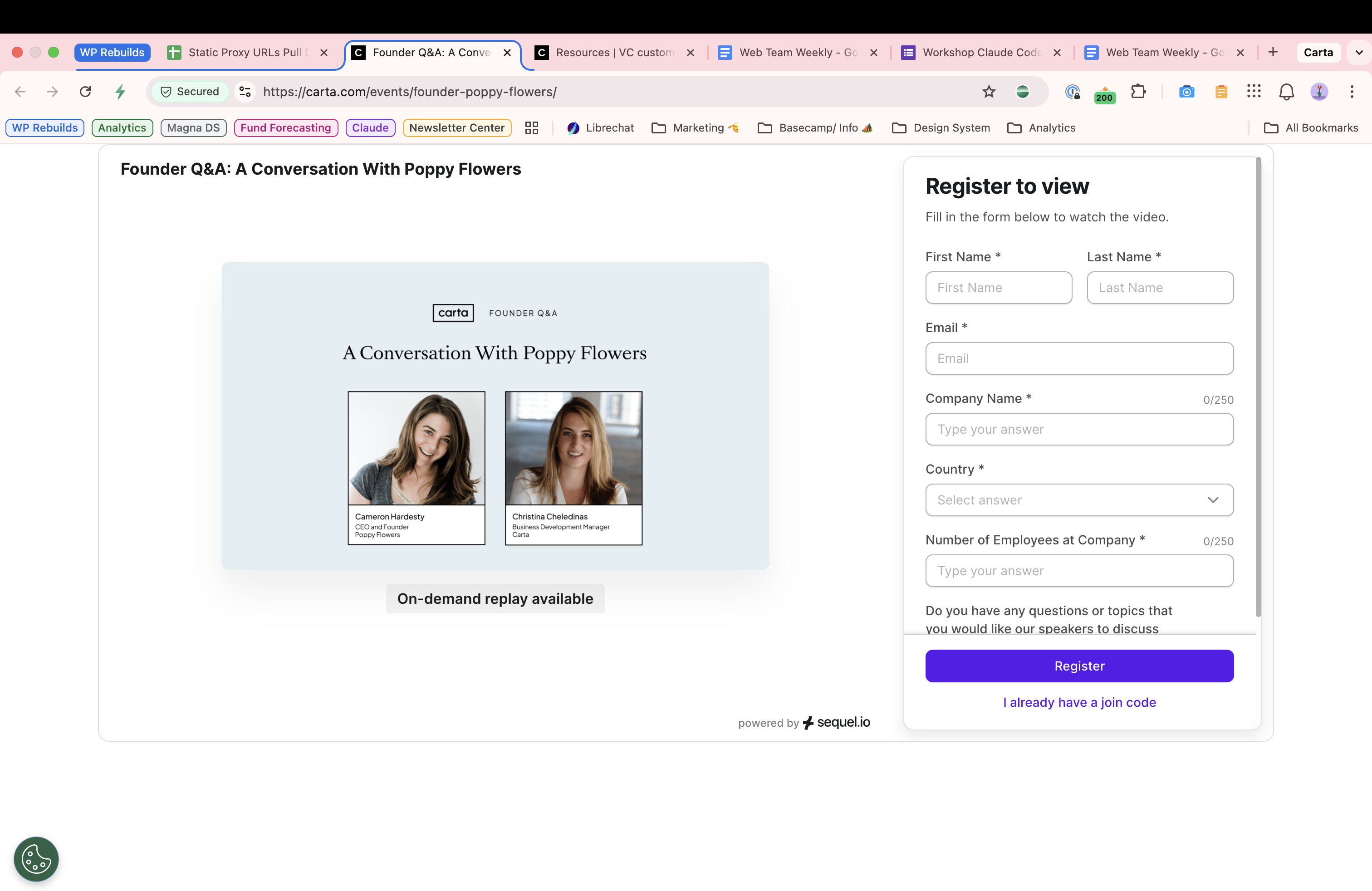

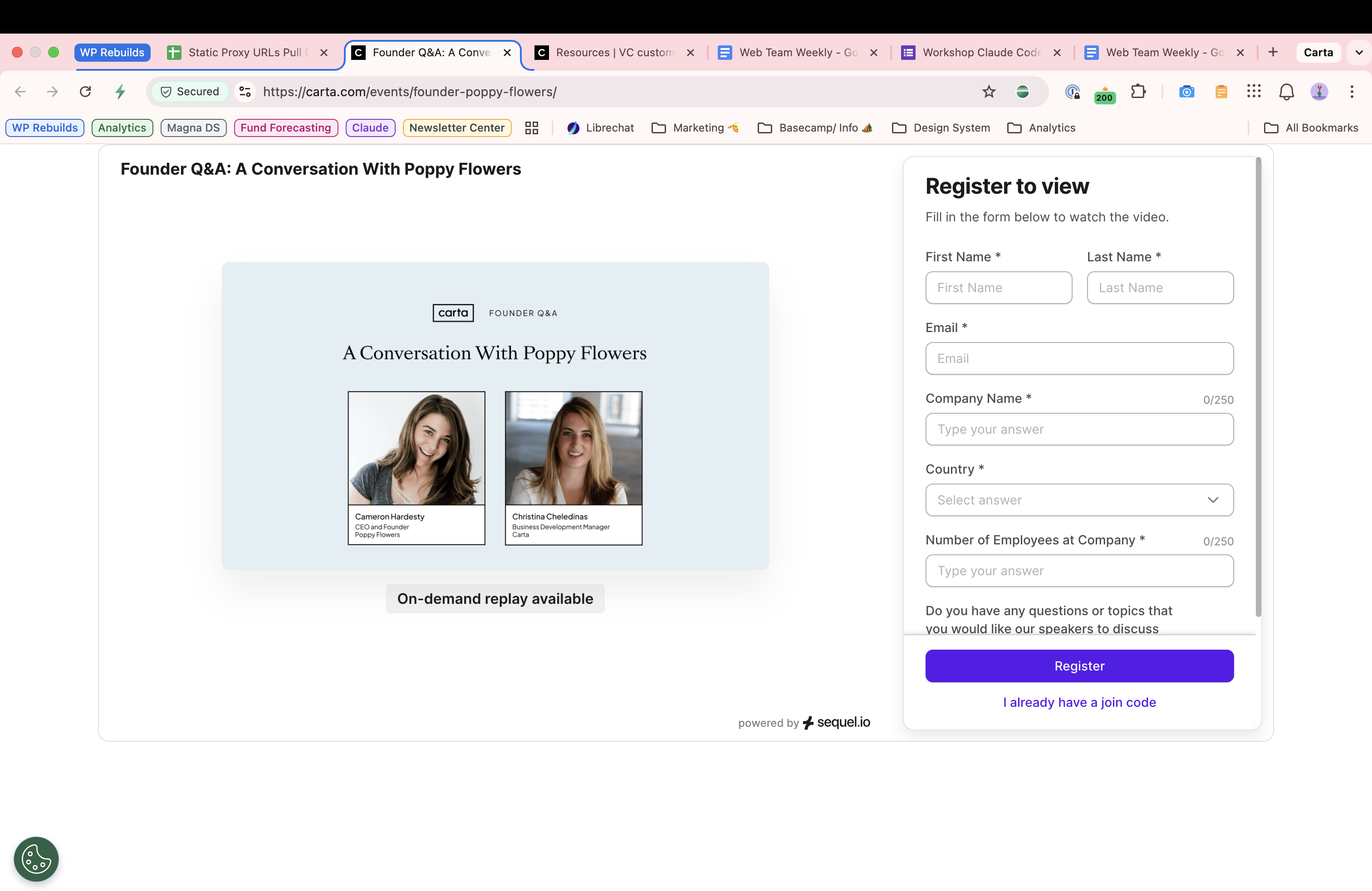

Founder Q&A: A Conversation With Poppy Flowers

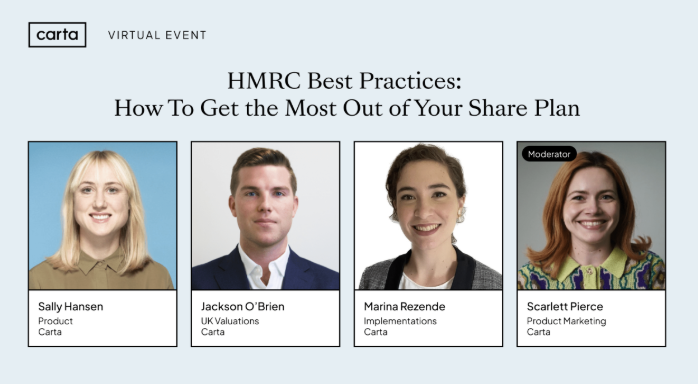

HMRC Best Practices: How To Get the Most out of Your Share Plan

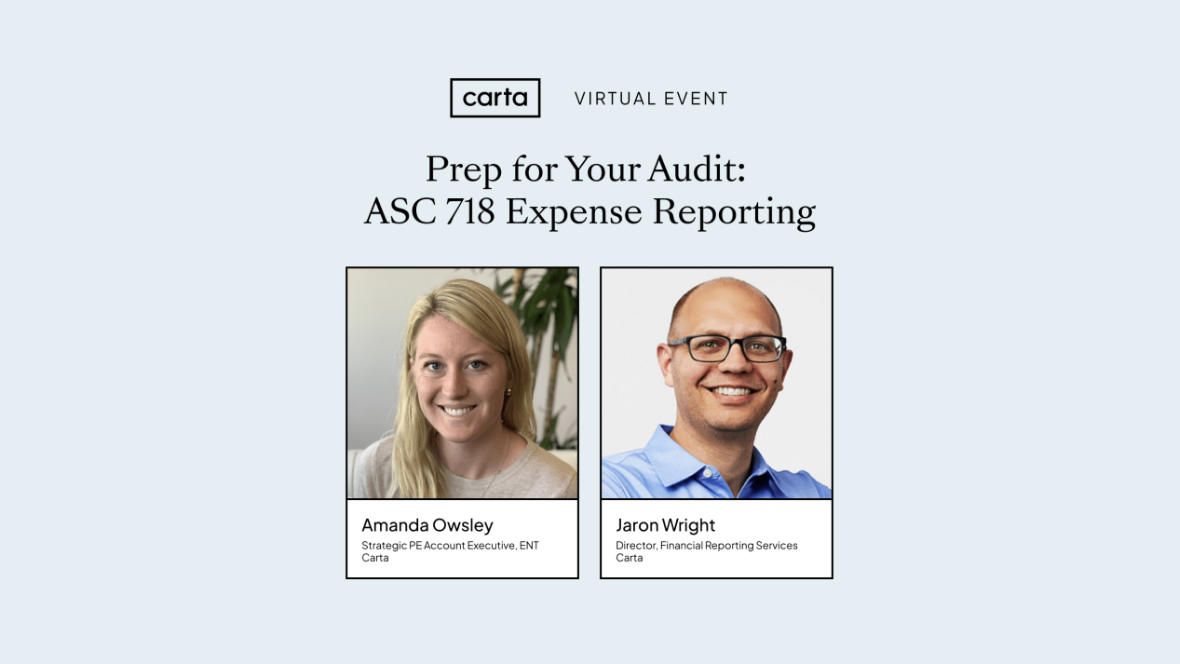

Prep for Your Audit: ASC 718 Expense Reporting

How To Get Your VC Fund Audit Ready

State of Private Markets: Q3 Headwinds

The Startup Guide to Taxes: Year-End Strategy for Success

SPV Structures: Which One Is Right for You?

FA Certification Program - Management Fees

FA Certification Program - Distribution Workflow

FA Certification Program - K1 and Tax

FA Certification Program - SOI Approval and Update

FA Certification Program - Distributions: Send Wire Instructions Request

FA Certification Program - Reviewing Financials

FA Certification Program - Cash Forecasting Overview

FA Certification Program - Day One Financials

FA Certification Program - Bulk Notices and Capital Call Reminders

FA Certification Program - Requesting Transfers/Submitting General Requests

FA Certification Program - Capital Call Workflow

FA Certification Program - Reviewing Capital Calls

Fund Administration - Subsequent Closings/Messaging

FA Certification Program - Fund Metrics

FA Contacts and Permissions

How to Map Your Investment Structures with Carta

Smarter Compensation: Retain Talent & Run Lean

Tariff Turmoil: Implications for Private Capital

Q1 Venture Capital Review: From SAFEs to Exits

Tactyc by Carta Live Demo: How to Make Data-Driven Fund Decisions

IPO Readiness in 2025: Market Signals, Timing, and Looking Ahead

Exits that Win: What Works, What Doesn't, and How Fund Managers Quarterback Exits

Private Equity Portfolio Companies & Funds: Connecting the Dots for the Audit Cycle

PE Executive Equity: Data-Backed Insights

Tax Season Recap & What's Next for Startup Taxes

VC Masterclass: Designing a Fund Thesis

Founder's Journey 101: Accelerating Growth

VC Fund Performance in 2024

What's New, What's Next: Carta Fund Admin in Q1

Founder's Journey 101: Scaling for Impact in Australia

Insights from Carta's 2024 State of Compensation Report

[Regional Replay] Shaping the Future of Venture Capital: Women in VC

Shaping the Future of Venture Capital: Women in VC

Best Practices: Planning for a Successful Year End

Policy Outlook 2025: Implications for the Private Capital Ecosystem

VC Masterclass: Building an Investment Track Record

Singapore The Global Hub: 2025 Regulatory and Tax Changes for Fund Managers

2024 Venture Capital Review: Insights and Implications for the Coming Year

Founder's Journey 101: Laying the Groundwork

Making Audits Easy: How to Streamline Your Fund's Audit

What's New, What's Next: Carta Fund Admin in Q4

Looking Forward: A Glimpse into the Future of Fund Waterfall Management

Election 2024: Policy Implications for the Private Market Ecosystem

2024 Fund Performance Data: A European Perspective

Tactyc by Carta Demo

State of Private Markets: End of Year Predictions

The Lifecycle of a Private Equity Deal with Weil

Essential Tools for Startup Success: QSBS Attestation

Essential Tools for Startup Success: Elevate Your Compensation Strategy

[Bonus Event] Startup Fundraising 101: Close Your Priced Round with Confidence

Audit Mastery: The Essentials You're Not Thinking About

Healthcare and Life Sciences: Growth and Funding Insights

Best Practices: How to Prepare for Year-End (Audit; Tax)

Startup Fundraising 101: Post-funding Success

Deep Dive: European Data Insights

Value Creation through Employee Equity: Insights from the 2024 Private Equity Ownership Trends Report

The Startup Guide to UK Fundraising: EIS and SEIS

What's New, What's Next: Carta Fund Admin in Q3

VC Fund Performance: New Benchmarks for 2024

Founders Guide to Board Management

Equity Compensation: Three Essentials You're Not Thinking About

Preparing for EOY: Get Ahead of Your Next Audit

Startup Compensation in 2024

GP Secrets: Fundraising; Investing in the Middle East; Asia Pacific

Pre-Seed Fundraising: Fresh Data from Q2 2024

Policy Playbook: How the 2024 Election Could Shape Private Market Policy

Essential Tools for Startup Success: Equity Management

Carta | NYSE: Getting Your Company IPO Ready

Startup Fundraising 101: Crafting a Winning Pitch

Policy Briefing: What Does the UK Election Mean for VC?

First Close: From Managing SPV's to Launching a Fund

What's New & What's Next: Carta Alternative Assets Product Updates in Q2

Forecasting Employee Compensation Accurately

What's New, What's Next: Carta Fund Admin in Q2

Business Guide to Taxes: Expiring Tax Incentives

Private Equity Firm Operations: In-House v. Outsourced

Emerging Trends & Key Insights for Asset Allocators

Startup Fundraising 101: Mastering Fundraising Strategy

Carta LP/GP Summit

First Close: Optimising for Your First Close

Advisory Boards Unveiled: Elevating Australian Startups to Global Heights

State of Private Markets: Q1 Venture Spring?

Policy Playbook: Navigating the Shifting VC Regulatory Landscape

Startup Fundraising 101: Building Strategic Partnerships

How Did 2023 Change Valuations?

First Close: Acing Your Fund Operations Stack

Navigating the Corporate Transparency Act as a LatAm Based Business Owner

Pre-Seed Benchmarks: Fundraising Data for New Startups

Building Lasting Limited Partner (LP) Relationships

Equity Essentials: Making the Leap From Seed to Series A

Best Practices: EOY Tax; Audit Planning

Tender Offers 101

What's New, What's Next: Carta Fund Admin in Q1

State of Compensation: 2024 Outlook

First Close: Formations

Navigating Opportunities: State of Venture in the Middle East

Corporate Transparency Act: Simplify Filing With Carta

What's New, What's Next: Effortless Distributions Modeling

State of Private Markets: 2024 Predictions

Corporate Transparency Act: What Business Owners Need to Know

Unlocking ASC 820 Valuations for Funds: Best Practices; Recent Trends

Audit-Ready Expense Reporting: The Fundamentals of Share-Based Payments

Using Data To Plan for Employee Compensation

What's New, What's Next: Equity Management for LLCs

What's New, What's Next: Carta Fund Admin in Q4

Understanding Executive Compensation: A Conversation with Carta and Sequoia

HMRC Best Practices: How To Get the Most out of Your Share Plan

Founder Q&A: A Conversation With Poppy Flowers

Prep for Your Audit: ASC 718 Expense Reporting

How To Get Your VC Fund Audit Ready

State of Private Markets: Q3 Headwinds

The Startup Guide to Taxes: Year-End Strategy for Success

SPV Structures: Which One Is Right for You?

![[VE] IPO Readiness in 2026: The Market Outlook and How AI Is Rewriting the IPO Timeline](https://images.ctfassets.net/y88td1zx1ufe/4IBI8TSYW7xUq49TIUKjrh/d1d1a6d18b67e1942585766d8b8ca25b/Event__1200x675___13_.png)

![[VE Image] Introducing Carta's Plugins for Claude](https://images.ctfassets.net/y88td1zx1ufe/6EHDtGb5MG91kChscWatI1/75edc2243bd32f59c1e477ff3b6b623b/Email_v1_20260729_PluginGA.png)