You may have seen one of Alex Clayton’s analyses of SaaS company S-1s floating around. With his banking and venture background, Alex is able to keenly dissect and interpret business models. Earlier this year, he presented an aggregate “ History of Public SaaS Returns and Valuations,” which is a must-read for any investor.

A little about Alex: After graduating from Stanford University, he worked at Goldman Sachs in investment banking focusing on M&A and equity financings for software, internet, and semiconductor companies. For the last eight years, he’s been a venture-growth investor focusing on later-stage technology companies—first, at Redpoint Ventures, followed by Spark Capital, and currently at Meritech, where he’s a General Partner and helps lead the firm’s enterprise software, infrastructure and fintech practices. Meritech manages $3B of total capital. (Note: Meritech is an investor in Carta.)

We caught up with Alex and asked him some questions about metrics, high valuations, and what it takes for companies to go public.

In your recent post, you pointed out that public and private high-growth B2B SaaS companies are valued based on a multiple of forward revenue over the next 12 months (NTM). Why is that the metric that we’re using to value these companies?

Most, if not all SaaS companies going public today are losing money. While they trade on a revenue multiple, such as enterprise value over NTM revenue, they’re really trading the assumptions that investors have made about their long-term margin profile.

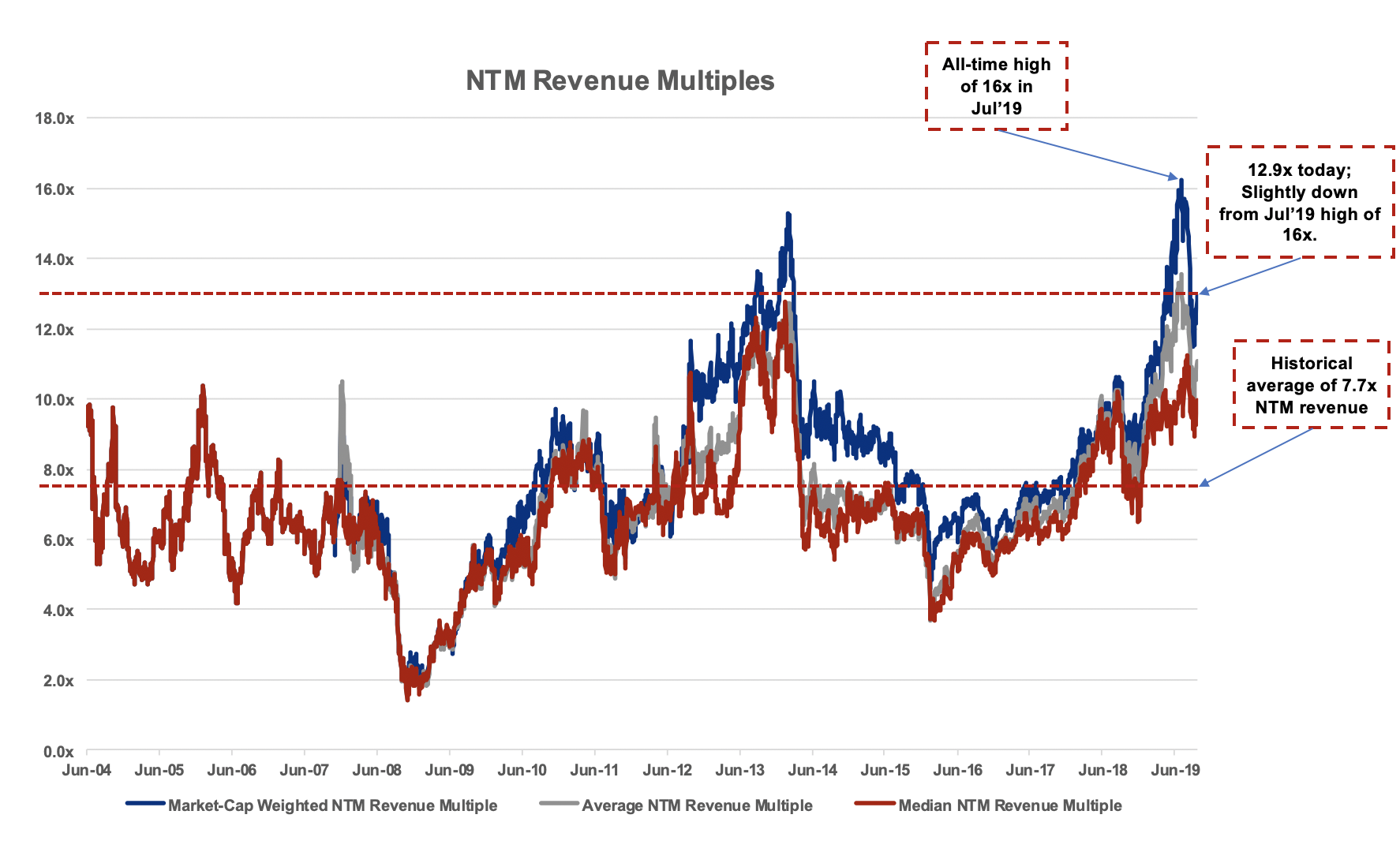

The value of the SaaS model is the potential for future cash flows. For example, if a company like a Zoom or Datadog stopped investing in growth and spent zero dollars to acquire new customers, they would quickly become very profitable. Software businesses have 80% gross margins in many cases and sticky subscription-based models. In many cases, the same customers pay more over time—hence SaaS companies often disclose their “dollar-based expansion rate” to show that $1 today is $1.25 in 12 months, $1.50 the next year, and so on. The high revenue multiples of SaaS companies today—which in some cases which are 20-30x NTM revenue—are proxies for the future earnings streams and assumptions about free cash flow generation over the long-term.

It’s important to note that while most of these companies are not yet generating cash, investors still believe in their long-term potential. At some point I believe the rubber will meet the road and that these growth companies will actually have to demonstrate they can generate cash flow in the near-term, but in today’s public market, investors are willing to pay high multiples for revenue growth and the potential of future cash flows.

While we can get into some other metrics, enterprise value over NTM revenue is probably the most relevant metric. But the best companies—the ones that trade at the highest multiples—are companies that not only are growing quickly, but also have high efficiency. For example, when Zoom went public (with $430M of implied ARR), it was not only profitable, it was the fastest-growing public SaaS company ever based on their ~150% dollar-based net expansion rate. Moreover, they had the best sales efficiency of any 2019 SaaS IPO. It’s no wonder the company trades at 27x NTM revenue (as of October 15th, 2019).

You mention that public SaaS companies have been recently trading at a price based on 15x EV/NTM revenue compared to the average of 8x all time. What do you think is powering this high multiple?

Public market investors have realized how big the market opportunity is for these businesses. We now have companies (like Zoom and others) that can sustain double to triple-digit year-over-year growth at scale. Investors are paying forward for that growth, but since the Great Recession, most SaaS companies that have grown by at least 30 to 40% year-over-year have seen massive value creation and in many cases are up many multiples of their IPO price. The public markets are taking notice, and more and more public investors are allocating more of their portfolio towards this asset class.

Looking at the recent wave of software IPOs and their respective returns, it’s no surprise that investors are willing to pay higher than historical average multiples. The almost 75 previous SaaS IPOs are up 5x on average from their IPO price, as of October 15. Given the market opportunity, investors are willing to pay forward because they believe in the long-term growth opportunity.

What would be your advice to a founder or CFO of a SaaS company if they’re considering going public in today’s market? What do you think are the important factors for them to consider?

If you look at the historical numbers from those almost 75 companies, they each averaged around $150M of LTM subscription revenue, growing over 55% year over year and were not generating profits. I believe once companies reach $40M+ GAAP revenue in a quarter, they’re at IPO scale.

Another important factor that a lot of people don’t think about is: how predictable is your business? There are really three different plans that companies must build when they go public. There’s an internal plan, which is what the team thinks they can hit on a stretch goal. There’s the board plan, which usually gives some cushion on their stretch goal. And then there’s a street plan. The street plan is the only one the public sees—and in particular for SaaS companies that have recently IPOed, they need to “beat and raise” every quarter. The key is predictable growth.

There are many other factors that go into investor relations and preparing to be a public company CEO, but I suggest companies start to think about it when they’re approaching $100M in ARR. CEOs need to embrace the idea of under promising and over delivering at every stage of company’s growth, but once they’re under the microscope of “The Street,” delivering consistently is crucial. It’s important to think about this when you’re still private.

Are macro-market conditions still important to consider?

You can’t control the macro markets. I tend to believe that once companies are ready to go public, going public is a great option. This is another area where some people might not realize it, but the act of preparing to go public makes you a better company. You have to be compliant. You have to understand the importance of predictability. And you have to understand board governance because your board changes once you go public, too. VCs are usually off the board at IPO or within a year.

Are there things companies can do to prepare themselves to go public and deal with public market investors?

I’ve seen one company—they’re getting ready for an IPO—and the CEO and the executive team do mock earnings calls every quarter, and they invite investors to join the calls. I got to join and hear how the company responds to analyst-like questions. It’s a small exercise, but at the same time, they’re preparing the documentation and they’re running these calls as if they’re a public company. By the time they go public, they’re going to be ready for public sell-side analysts.

Another thing companies can do is a “non-deal roadshow” where they meet with public market investors, pitch their businesses, and get feedback. It’s not just about the numbers but about the vision and story. I found that it’s really helpful for companies to understand what public market investors are looking for. It’s a great learning experience because at the end of those two or three weeks, they’re not actually putting an order in your book (unlike a traditional IPO roadshow)—they’re just learning more about the business.

With several high-growth SaaS companies struggling post-IPO lately, do you think the market’s been under or over valuing these companies?

No doubt, valuations are very rich. Like I mentioned, we’re trading at some of the highest multiples that SaaS companies have ever traded at in history. It’s only been 15 years. At the same time, if you look at the public market returns of the almost 75 pure play SaaS companies that have gone public, the average return from IPO price for standalone companies is about 5x, and that’s just over three years.

For context, most venture funds strive to return 3x their fund size—so if you put a dollar into every SaaS company upon their IPO, you’d be up around 5x. So while valuations are high, the staggering returns have made it worth it for the time being, which could obviously change at any time.

How do you think SaaS companies should weigh their options when it comes to considering a direct listing versus a traditional IPO?

This is an interesting topic, and there’s been a lot of discussion around what is the best route. I personally don’t think there is a right or wrong answer; there are pros and cons to either approach.

An argument I’ve seen used in favor of direct listing is that it eliminates the first day “IPO pop,” where a company’s stock price will rise 20 to 50%+ on the first day because the bankers “intentionally” priced it low. From being on the banker side of multiple IPO transactions, there are dozens of moving parts and negotiation between potential public market investors, executives, the board of directors, and others. Moreover, soon-to-be public companies want long-term shareholders in the public markets. What if you sold most of your stock to hedge funds that, in turn, sold it all on the first day and the stock price plummeted? That wouldn’t be a good outcome for the IPO and employee base. I’ve seen that a first day “pop” has a hugely positive impact on the employee base and acts as a “shot in the arm.” On the other hand, if you’re a well-known company and don’t need additional cash since you’re already fully capitalized, a direct listing could be a good path since there’s no IPO dilution. The other argument I’ve seen pitching direct listings is that it cuts out the bankers and the companies don’t have to pay fees, which is just not true. The few companies that have pursued direct listings have paid bankers tens of millions of dollars in fees. The best companies will generate value in the public markets if they perform well regardless of what path of IPO they choose to take. At the end of the day, the executives and their respective board of directors should pursue the strategy that makes the most sense for the company.

How do you look at private markets and how they affect public markets? How do you see that evolving?

They’re intertwined. Let’s talk about SaaS companies in particular: If you’re investing at the Seed or Series A stage, you probably don’t care about the macro as much or what Zoom or Datadog is trading at. By the time this company could go public, you’ll probably be in two different market cycles. If you’re investing at the growth stage and the company might be public in one or two years, it’s important to understand what’s going on in the macro environment because your outcome could be affected dramatically. If SaaS multiples go down 20% today, it’s likely that the funding environment is not going to change unless they keep going down for a quarter or two. I think the private and public markets are highly correlated, and there’s a ripple effect for sure, but it takes a couple of quarters. I’ve seen a couple of cycles where public SaaS multiples corrected significantly but it still took time for it to make a difference in the private markets. As I mentioned earlier, on average multiples are down 20% over the past few months, but the private market funding environment for SaaS hasn’t changed from what I can tell. There needs to be sustained pain in the public markets for it to make a difference.

Do you have any thoughts on the format or standards required for S-1s? They require so much material and leave room for companies to present distorted KPIs. The much mocked “community-adjusted EBITDA” from WeWork is the most recent example of this.

Your S-1 is the story you tell the world about your company. In the US, you must conform with GAAP financials. At the same time, companies are allowed to release certain non-GAAP metrics they think are important KPIs for their business (and that the SEC allows). That’s where we get all these things like community adjusted EBITDA from WeWork, which they ended up pulling toward the end.

One thing that companies need to consider is that if you’re disclosing metrics in the S-1, you will likely have to do so over time, so make sure it’s a metric that’s both predictable and a good KPI for the business. Companies tend to come up with these different metrics to make their business look the best. If the SEC set standards like “every company has to report net dollar retention this way,” it would be a lot easier to evaluate companies. But I don’t know if that’s going to happen.

If you could choose a few metrics that every company had to release, whether they’re public or private, what would you pick?

I wish every public SaaS company had an ARR schedule. Beginning ARR, new ARR, expansion, upsell, churn, contraction, net new ARR, ending ARR—and a consistent definition around what ARR is. With that data, you could isolate sales efficiency across every single SaaS company. You would know that, for every new dollar of ARR/ACV, we know the best companies spend X dollars in sales and marketing. This is very unlikely to happen. With that said, I agree with the current SEC reporting standards—they’re there to protect investors.

Today, only a few companies actually report ARR. I think CrowdStrike might’ve been the first SaaS company in their S-1 to report annual recurring revenue as a non-GAAP metric. With some of the new reporting standards around RPOs (remaining performance obligations), people will be able to back into ARR.

You can get Alex’s S-1 analyses by subscribing to his newsletter here.

DISCLOSURE: This communication is being sent on behalf of eShares, Inc. dba Carta, Inc. (“Carta”). This communication is not to be construed as legal, financial or tax advice and is for informational purposes only. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein.

This post contains links to articles or other information that may be contained on third-party websites. The inclusion of any hyperlink is not and does not imply any endorsement, approval, investigation, or verification by Carta, and Carta does not endorse or accept responsibility for the content, or the use, of such third-party websites. Carta assumes no liability for any inaccuracies, errors or omissions in or from any data or other information provided on such third-party websites.