- RSU vs. stock options

- RSUs vs. stock options: Key differences

- When are companies switching from stock options to RSUs?

- Download the option and RSU grant calculator

- What to consider before switching from options to RSUs

- Taxes

- Liquidity

- Other considerations:

- What happens if you switch too soon

- Get help with this big decision

- Give your employees a clearer view equity ownership

Startups move from issuing employee stock options to restricted stock units (RSU) as a form of equity compensation as they become larger for at least the following reasons:

The value of RSUs are easier to understand compared to the upside of stock options

The cost to exercising stock options becomes too large of a burden for employees

The company wants to limit dilution

Clear alignment between company and exit strategy (i.e: there’s a plan to IPO soon)

In a tougher economic climate, it may make sense for companies to switch to offering RSUs instead of stock options because, unlike options, RSUs will still be worth something even if the stock price goes down. Option grants become “underwater” if their fair market value (FMV) falls below the strike price). However, if the 409A valuation of the company drops significantly for a temporary time and then rises, it may make options seem like a good deal in comparison to RSUs.

Generally, later stage companies are the ones that look to switch to RSUs. Early on, options make sense for a company because of the relatively low strike price and higher anticipated growth rate.

So if you’re a CFO of a mid- to late-stage company, when do you switch? Timing matters. You want to ensure you aren’t late (or early) to the game. This RSU vs. stock options guide is here to help make sure you get this important decision right, because it has deep ramifications for your company and employees.

RSUs vs. stock options: Key differences

RSUs have benefits for both existing and newer employees. Including some major simplifications:

Less dilution

No cost to exercise

Less risk if stock price goes down

But RSUs often have a certain type of vesting condition, called triggers, which can be performance or time-based. Most private RSUs have “double-triggers,” meaning they only vest after two conditions are met. Time-based triggers are like your standard vesting schedules. But performance-based triggers are tied to company milestones, like going public or undergoing a change in company ownership.

Here’s a list of the key differences between RSUs vs options:

Equity | Value proposition | Pros | Cons |

|---|---|---|---|

RSUs | The value of RSUs is much easier to measure. They’re worth whatever the company stock is worth at the time of issuance. They don’t need to be purchased so there’s less risk. | RSUs will require less equity burn (from the company) to provide similar value to the candidate. | Employees have no control over the timing of the taxes or the tax rate (compensatory). Employees might even lose any RSUs they have “accrued” if they leave before both triggers are met. Results in less alignment between workers and company. Offering RSU liquidity is currently really difficult. |

Options | Provides more upside for those employed at high growth companies. Employees can optimize for taxes in a way they cannot with RSUs. | Allows employees to have control over the timing of their tax obligation and allows for participation in liquidity programs such as tender offers. | Results in more equity burn in order to provide similar value to RSUs.As companies mature, exercise costs become a barrier and the gap between preferred and strike price will fall, reducing inherent value. |

When are companies switching from stock options to RSUs?

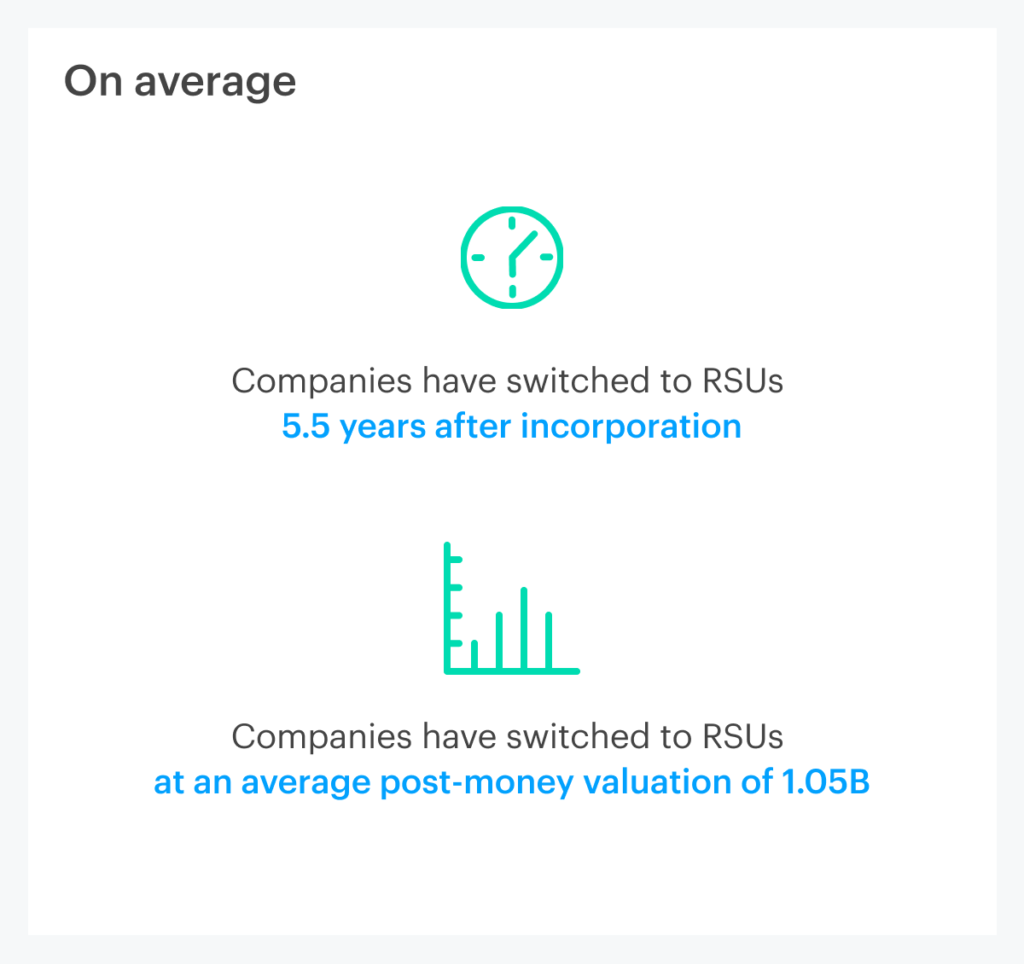

Here are some trends we’ve seen, although this is based on limited data*:

On average, companies switch to RSUs 5.5 years after incorporation

On average, companies switch to RSUs at an average post-money valuation of $1.05B

This might seem too soon or too late for your company. A lot depends on your individual company’s needs.

If you want to know when is the right time for your company to switch, download our free option and RSU grant calculator. This calculator lets you look at a specific grant and compare how it may change the total payout for the employee based on if they were granted options or RSUs (it does not account for taxes).

Download the option and RSU grant calculator

If you want to dive deeper, here are some aspects to consider before making the decision to move from options to RSUs:

What to consider before switching from options to RSUs

Taxes

Most late-stage company RSUs have performance-based triggers, so you don’t receive them (or get taxed) until there’s some possibility of liquidity. Most public companies already have RSU programs, and their stock is already liquid to some degree, so employees are taxed upon vesting.

Here’s how RSUs and options compare in terms of taxes:

Security type | When are security holders taxed? | What type of tax? | Tax implications |

|---|---|---|---|

RSUs with performance trigger | At vest | Ordinary income tax | Higher tax rates, no choice on taxable event |

Options | At exercise or sale (depends if options are Incentive Stock Options (ISO) or Non-Qualified Stock Options (NSO)) | Ordinary income tax but with potential for capital gains and Alternative Minimum Tax (AMT) | Potential for lower tax rates, choice on when to exercise |

Liquidity

Because most private companies have that RSU performance trigger (sale or initial public offering (IPO) of the company), the ability to have private market liquidity is difficult. While companies can remove the performance-trigger, they need to be ready to cover tax obligations of time-vested RSUs. Currently, there is no easy platform that enables companies to do this. Thus, private liquidity with RSUs is a real challenge.

If you plan to stay private for the majority of the lifetime of the awards you are issuing, think twice about switching. Moving to RSUs too early can be costly and can trap companies, like what occurred with Airbnb. Since switching, Airbnb has likely not run any tender offers for employees that have RSUs. Employees have reportedly been unhappy with this and in addition, Airbnb is coming up against the IRS limit of how long an RSU can be in place before vesting.

You have to think about your company’s future here. If you’re considering a direct listing and currently issue RSUs, a good portion of your stock plan will not be liquid as a private company (the portion issued as RSUs). This makes it tough to get the transaction volume needed to price the initial offering. If you stick with options you will have more choices offering private liquidity and increasing transaction volume on the private side and better price discovery as a result.

Security type | Liquidity options | Limitations |

|---|---|---|

RSUs with performance condition | IPO/acquisition | Can’t easily run private liquidity events. At the point of IPO or acquisition, all accrued RSUs would be taxed, regardless if employees want to sell the vested shares or not. |

Options | Private secondary transaction, IPO, direct listing, acquisition | The only limits here are how often you and your company’s board want to run liquidity events. At Carta, we’ve historically done them every 12 to 18 months. |

Other considerations:

Before moving to RSUs, you need to forecast your accounting ahead of a potential IPO as you’ll see a larger expense recognition when shares become liquid. For example, Snapchat had to pay more than $2 billion in a stock compensation expense charge. While option expense is spread out over the life of the award, double trigger RSUs are expensed at vest. This means finance teams should plan for a potential large expense number following their listing. This type of expense is non-cash and is simply an accounting entry that impacts your reported GAAP numbers, which can make the company look less profitable (or having lower net income).

RSUs also require more employee equity education, as they are different from stock options. RSUs add a new layer of complexity for finance, HR, and stock administration teams.

What happens if you switch too soon

At Carta, we hear about lots of companies who are considering switching to RSUs. While there is a point where it may make sense, more often than not, we see companies switch too soon. Here’s how switching to RSUs too soon can box a company in:

Can’t change existing RSU grants to options

Can’t easily offer private liquidity

Big employee tax bill at vest (if planning to go public)

Switching while there is still room for a lot of growth limits employee upside

If you switch and realize RSUs aren’t a fit for your company, you can change back to issuing options, but existing RSU grants can’t be changed. This is why you need to think critically about this moment and what it means for your business.

Get help with this big decision

Talk to your outside counsel about each of these items regardless of your company structure. They’ll have advice on what might be best for your business. They’ll be able to help you plan ahead for unique cases such as international RSUs, liquidity events, and more. Moving to RSUs is a huge decision for any company and it needs to be done carefully.

If you have any questions about this switch, reach out to your Carta customer success manager.

Thank you to Aaron Jacobs, Mischa Vaughn, Grace Erickson, Charly Kevers, Gerald Lou, and Alex Farman-Farmaian for helping with this post and calculator.

* Customer data that Carta does not have a right to use in anonymized and aggregated studies is excluded from this analysis.

Give your employees a clearer view equity ownership

Equity Advisory, an addition to Carta’s cap table, provides your employees with personalized equity-based tax support.

DISCLOSURE: This publication contains general information only and eShares, Inc. dba Carta, Inc. (“Carta”) is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein.

This post contains links to articles or other information that may be contained on third-party websites. The inclusion of any hyperlink is not and does not imply any endorsement, approval, investigation, or verification by Carta, and Carta does not endorse or accept responsibility for the content, or the use, of such third-party websites. Carta assumes no liability for any inaccuracies, errors or omissions in or from any data or other information provided on such third-party websites.