- What is a cap table? A founder's guide

- What is a cap table?

- The structure of a cap table

- Key components

- Common formats

- Cap table example

- How to create a cap table

- The initial setup

- Add founders’ equity

- Add investor equity

- Add an option pool

- Cap table management best practices

- Maintain accurate records

- Use an organized format

- Update your cap table regularly

- Plan for dilution

- Ensure compliance

- Tools for cap table management

- Cap table template

- Why spreadsheets don’t scale

- Cap table software

- Free cap table software

- Frequently asked questions about cap tables

What is a cap table?

A cap table, short for capitalization table, is a document that details your company’s equity ownership structure. It is the official record of who owns what, listing every shareholder in the company, the number of shares they own, and the types of equity they have. For founders, investors, and employees, the cap table is the single source of truth for your company's ownership.

Maintaining an accurate cap table is especially important for startups and high-growth companies where ownership percentages can change dramatically following funding rounds, employee option pool creation, and secondary transactions. Cap tables also play a major role in due diligence for potential investors who are considering investing in your startup.

Think of it as the foundational document for building trust and appearing professional, especially when you're a first-time founder navigating the fundraising process. A clean, accurate cap table shows potential investors that you are organized and serious about managing your company's equity—an important signal in a tough fundraising environment where global deal activity has plunged 19% YoY. It tracks ownership from the day you incorporate through every funding round, new hire, and change in ownership.

This video gives an introduction to cap tables as part of Carta’s free Cap Table 101 curriculum.

The structure of a cap table

A cap table’s structure can vary depending on the size and stage of the company. As a company matures, its cap table evolves from a simple record of founders’ shares into a complex document detailing funding rounds, employee equity plans, and convertible instruments. No matter how complex it becomes, the goal is to maintain a clear and accurate record of equity ownership.

Key components

A cap table is organized into categories that detail ownership details, transaction history, and other financial information. Common components of a cap table include:

Ownership details

This is the most basic part of the cap table, answering the fundamental question: “Who owns what?” It’s the starting point for understanding your company’s ownership breakdown.

This section outlines who owns all types of equity in the company (such as shares, options, warrants, and convertibles), the total ownership stake, and what percentage of the company that stake represents.

Shareholder information: Shareholder names, entities, and roles like founders, investors, employees, and advisors.

Number of shares: Total shares owned by each shareholder.

Ownership percentage: The percentage of the company owned.

Types of equity

Not all equity is the same, and your cap table distinguishes between the different types you issue and the terms of each. As a founder, you'll encounter several common forms of equity.

Common stock: These are the basic ownership shares in a company. Founders and early employees typically hold common stock as part of their initial employee equity.

Preferred stock: This class of stock is usually issued to investors during funding rounds. It often comes with special rights, like getting paid back first in a sale and special voting rights.

Stock options: This is the right for an employee to buy a set number of shares at a fixed price in the future.

Restricted stock: These are shares granted to employees or service providers that are subject to vesting and other restrictions.

Warrants: These are similar to stock options but are often granted to investors, lenders, or partners as an incentive.

Convertible instruments: These are investments that turn into equity at a later date. The most common types of convertible securities are SAFEs (Simple Agreements for Future Equity) and convertible notes.

Share classes

Different types of equity are organized into share classes, and each class can have different rights. The most important distinction for a startup founder is between common and preferred shares.

Preferred shares, held by investors, often include a liquidation preference. This means investors get their money back before common stockholders in the event of a sale. Share classes can also have different voting rights, which affects control over company decisions and overall board management.

Transaction history

This section operates as the official logbook of your company’s ownership. It tracks every single event that changes who owns what on your cap table.

Maintaining a detailed transaction history is important for valuations audits and due diligence, as even advanced industry indicators rely on accurate deal-level data to assess market health and company momentum. Examples of transactions you'll need to record include:

Funding rounds where new shares are issued to investors.

Stock grants issued to new hires or advisors.

Employees exercising their stock options to purchase shares.

Valuations

Valuations give your company's shares a monetary value, which is a key piece of information for both investors and employees. The cap table tracks these values as they change over time. These are some of the types of valuations you might include in your cap table:

Pre-money valuation: The value of the company before a new funding round.

Post-money valuation: The value of the company after the funding round.

409A valuation: This is an independent appraisal of a private company’s fair market value (FMV). The 409A value is used to set the strike price for employee stock options.

Price-per-share: The value of each preferred share sold in the funding round (share price), which is calculated using the valuation divided by the total number of fully-diluted shares. It is worth noting that the valuation of the latest preferred share class does not necessarily imply that common shares have the same FMV.

Dilution analysis

When you issue new shares to investors or employees, the ownership percentage of existing shareholders decreases. This is called share dilution, and your cap table is where you track it.

Dilution analysis helps show your existing shareholders how issuing new shares or securities impacts their percentage of ownership. A well-maintained cap table allows you to use scenario modeling to understand how new funding or hiring will impact everyone's ownership stake.

Dilution is a normal and necessary part of growing a startup through fundraising and hiring, and it must be managed alongside key metrics like burn rate. The key is to manage it strategically.

Exit scenarios

One of the most powerful uses of a cap table is modeling exit scenarios. This involves running a waterfall analysis, which projects how the money from a future sale, initial public offering (IPO), or other liquidity event would be distributed among all shareholders.

This analysis is based on the specific rights of each share class, especially the liquidation preferences of your preferred stock. It shows who gets paid, in what order, and how much they receive, providing clarity on liquidity for founders, employees, and investors alike.

Common formats

Choosing the right format for a cap table depends on your company’s needs. Early-stage startups often use simple Excel spreadsheets or tables to track ownership, which are cost-effective and sufficient for straightforward ownership structures.

However, as your company grows, raises new funding rounds, creates an employee stock option pool, and adds new share classes, a cap table software solution is usually needed to remain up-to-date, reduce errors, and enable scenario modeling.

Even early-stage companies with simple ownership structures can benefit from creating their cap table on a dedicated software from the beginning. Carta offers free cap table software for startups with under 25 stakeholders and less than $1 million raised.

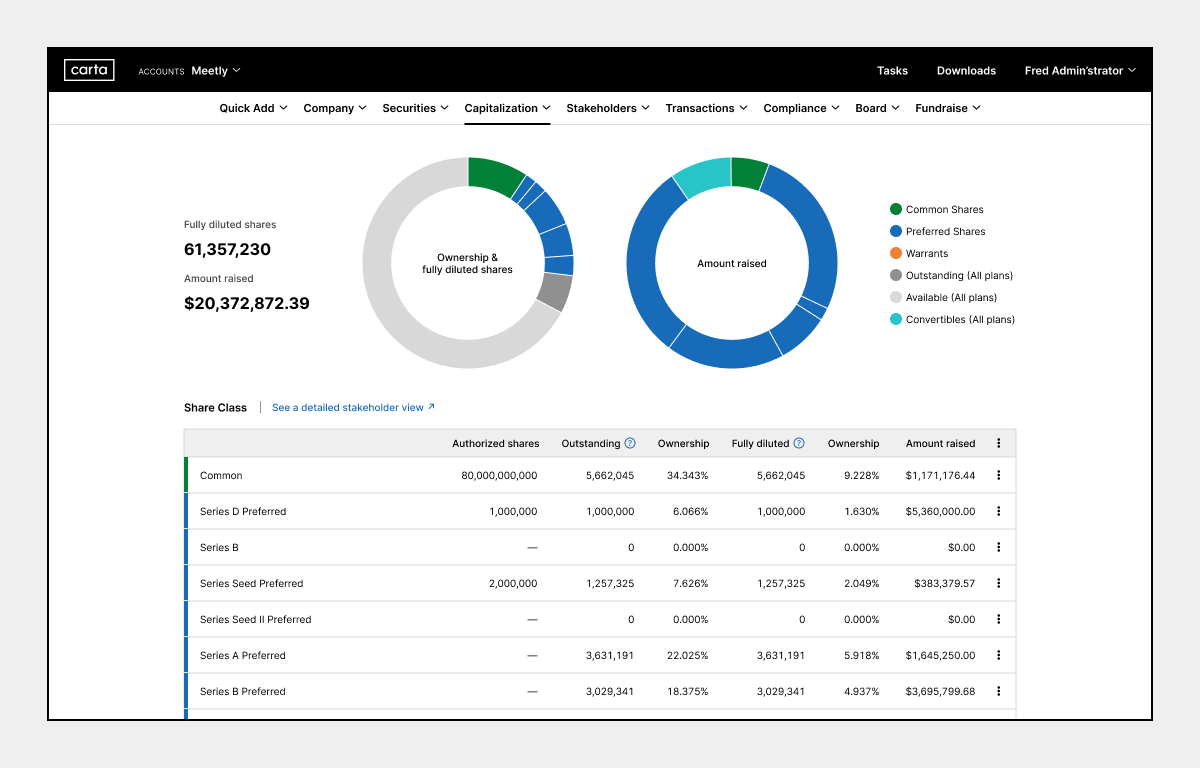

Cap table example

While there’s no standard format, here’s an example of what a cap table could look like:

How to create a cap table

Now that you understand the components, you can build your first cap table. Creating a cap table involves compiling and organizing your existing equity ownership information into a structured format that is easy to understand and maintain.

There are multiple ways to create and manage a cap table, but the best option for you depends on your company’s stage and ownership structure. For a founder in the “seed and setup” phase, the goal is to create a clean, professional record from day one.

This process sets the foundation for all future equity management. Getting it right from the start will save you from headaches and costly mistakes down the road.

The initial setup

Gather all the current equity and ownership information and legal documents to create a complete and up-to-date picture of your company’s ownership structure. Accuracy here is everything, as this data forms the basis of your entire cap table. Any missing or inaccurate information can lead to complications down the line during fundraising or audits.

You will need:

Total authorized shares: The maximum amount of shares the company can issue.

Issued and outstanding equity (stock, shares, convertibles): The number of shares currently allocated to stakeholders.

Shareholder details: Names, roles, and contributions of all equity holders.

Equity types: Details of issued securities including common and preferred stock, stock options, warrants, and convertible notes.

Funding rounds: Details of previous financing rounds, including valuations, total amount raised, and share price.

Option pool allocation: This includes the number of shares reserved for employee equity plans, issued and outstanding shares, exercised stock options, and more.

Any relevant documentation including incorporation documents will streamline this process.

Add founders’ equity

Next, you'll record the initial equity split between you and your co-founders. This section documents who gets what percentage of the company at its creation.

Documenting the initial co-founder equity split establishes ownership percentages and helps track dilution over time. To add founders’ equity, record the number of common shares assigned to each founder based on agreed ownership split, and include a column for any applicable vesting schedules.

If you receive restricted stock, it is important to file a timely 83(b) election with the IRS, and as part of your tax planning for small businesses, explore strategies like QSBS to potentially save on future taxes.

→ Data Desk: Learn more in Carta's Founder Ownership Report for 2025.

Add investor equity

If you've raised money from an angel investor or through a pre-seed round, add their investment to the cap table. This section will record the total investment amount, the total number of shares purchased by investors (or convertible notes or SAFEs), the price-per-share, the share class of the equity, and the voting rights and liquidation preferences agreed to with their equity.

A clean, accurate cap table shows potential investors that you are organized and diligent about managing your company's equity. It provides a clear record of fundraising, financial history, and company valuation.

On the other hand, a messy cap table can be a major red flag, as the timing of events like option pool increases and note conversions can have significant implications for valuation and founder dilution. When the market tightens, investors often use their leverage to negotiate for complex terms that can complicate your ownership structure. For example, as the market cooled, the use of investor-friendly deal terms spiked. The share of funding rounds with participating preferred stock, a term that can significantly complicate a cap table, more than tripled from 4.8% in late 2021 to 15.6% in early 2023, before falling back to 6.1% in Q3 2023.

Add an option pool

An option pool is a portion of your company's shares that you reserve for future employees as equity compensation. Creating one is a signal that you're planning to grow your team.

By including an option pool in your cap table, you ensure you have shares available to incentivize employees, consultants and advisors and have more certainty about future dilution.

Be strategic about the size of your option pool, as it's a resource that changes as your company grows. While every situation is different, benchmark data can provide a concrete starting point for your planning. For example, a median company valued at $25 million, a common proxy for the Series A stage, typically designates around 14% of its shares for its employee pool. As companies mature and raise more funding, they tend to expand their employee equity plans, with option pools at late-stage startups often nearing 20% of all equity.

Cap table management best practices

As your company grows, your cap table changes from a simple record into a strategic tool. Whether your business is an early-stage startup or a mature organization, regular cap table management helps you avoid costly errors, remain in compliance with regulations, and build trust with your stakeholders.

Following best practices will help you maintain a healthy cap table that supports your company's journey. Following these best practices ensures your cap table remains accurate, compliant, and ready for any opportunity, from a new funding round to an acquisition offer.

Maintain accurate records

Create a single source of truth: Your cap table must be the one and only undisputed record of ownership. This eliminates the confusion and risk that comes from managing multiple spreadsheets, legal documents, and email threads. That confusion isn't just an administrative headache; it has real financial consequences for your team. According to a 2022 report by Carta, 13% of employees didn't exercise their stock options because they were afraid of making a mistake or thought they already owned the shares. A single source of truth for equity prevents these costly errors.

Errors and omissions can lead to delays in fundraising, regulatory penalties, and disputes between stakeholders. Here’s what you should do to stave off such mistakes:

Regularly verify share ownership, equity types, and transaction history.

Reconcile cap table data with term sheets, stock certificates, and board resolutions.

Include all equity and convertible debt instruments in your cap table.

Use an organized format

Provide clarity: An organized cap table is easier to share with stakeholders, potential investors, and lawyers and prevents misunderstandings.

Use consistent layouts and labels on columns and rows.

Differentiate between share classes and associated rights or preferences.

Update your cap table regularly

Keep it live: A cap table is a dynamic, living document that changes frequently. It must be updated in real time with every new stock grant, transfer, or funding round to keep you investor-ready. This is where Carta's platform helps by automating these updates for you.

Record new issuances, grants, and transfers immediately after they occur.

Show changes in ownership percentage and share dilution after a funding round.

Review and update quarterly.

Plan for dilution

Model the future: Don't let fundraising rounds create surprises for your ownership stake. Use scenario modeling to understand exactly how new investments will impact the ownership percentages for you, your investors, and your employees. Carta's Scenario Modeling tools are built specifically for this purpose.

Model dilution scenarios when preparing to issue new shares during fundraising.

Communicate the impact of dilution to stakeholders.

Size your option pool appropriately to avoid frequent dilutive increases in the future.

Ensure compliance

Follow the rules: Equity is governed by a complex set of tax and legal regulations. Using a platform with built-in compliance for things like 409A valuations and financial reporting helps you avoid penalties and stay audit-ready at all times.

Use a cap table software with built-in compliance support.

Maintain documentation of board approvals and 409A valuations.

Understand the regulatory landscape and comply with reporting requirements.

Tools for cap table management

As a founder, you have two main choices for managing your cap table: a simple spreadsheet or dedicated cap table software. While a spreadsheet might seem sufficient at first, it quickly becomes a liability as your company grows.

Modern, professional software is designed to handle the complexities of equity management, saving you time and preventing expensive mistakes.

Cap table template

In the very early stages of a startup, cap tables often live in a spreadsheet because ownership is usually relatively simple and easy to track early on. But if you’re creating a cap table for the first time, starting from scratch can get complicated quickly.

Download Carta’s free cap table template for a useful starting point…but remember that Excel-based spreadsheets won’t scale with you as you grow.

Why spreadsheets don’t scale

Relying on a spreadsheet to manage your cap table is a common mistake for early-stage founders. While some companies begin by tracking their ownership in a spreadsheet, the path for growing venture capital-backed startups is clear. More than 50,000 companies now use dedicated platforms to manage over $3.0 trillion in equity, establishing a clear best practice for scalable and accurate cap table management.

As you hire employees, raise funds, and issue more equity, the risk of a small formula error or an outdated version causing a major problem increases. Managing your cap table on a spreadsheet can lead to common errors and confusion.

Spreadsheets | Cap table software |

Manual updates required | Automatically updates with each transaction |

High risk of human error | Reduces errors with built-in checks |

Difficult to share and track versions | Centralized, single source of truth |

Lacks built-in compliance | Includes compliance and reporting tools |

Does not scale with company growth | Scales from incorporation to IPO |

Carta began over a decade ago with the simple solution of fixing cap tables and taking them off manual spreadsheets. If your cap table still lives in a spreadsheet, you have to be diligent about using consistent names, updating your version whenever something happens, and sending the updated version to relevant stakeholders, like your lawyer.

Cap table software

Cap table software is the modern standard for serious founders who want to manage their equity professionally. It automates workflows, provides a secure portal for all stakeholders, and saves you time and legal fees—request a demo to see how it works.

Carta is the equity management platform trusted by over 50,000 companies, from new startups to mature companies.

Free cap table software

Starting with cap table software early in your company’s lifecycle can save you time and money as your business scales. For very early-stage companies, Carta Launch offers our professional platform for free, allowing you to get started the right way from day one. With Carta’s Launch plan, startups with up to 25 stakeholders that have raised less than $1 million can get free cap table management.

Frequently asked questions about cap tables

How do I create a cap table?

Start by listing all shareholders in your company, including founders, investors, and employees. For each, record the number of shares they own, the type of shares, and any other issuances like option grants or convertible notes. Next, calculate the total shares outstanding and determine each person's ownership percentage. Organize this information into a table, updating it whenever new equity is issued, options are exercised, or ownership changes.

Can an LLC have a cap table?

Yes, while LLCs issue “membership units” instead of shares, a cap table is still needed to track ownership percentages and capital accounts. Carta for LLCs is specifically designed to handle the unique equity structures of limited liability companies.

Do all companies have a cap table?

Any company with more than one owner or that plans to issue equity to investors or employees needs a cap table. It's the only way to maintain a clear and accurate record of who owns what.

Is a cap table a public document?

No; for private companies, the cap table is a highly confidential document. It is typically shared only with key stakeholders like board members, investors, and lawyers during specific events like fundraising or legal reviews.

Does a cap table include equity grants for service providers and advisors?

Yes, a cap table should include equity grants for service providers and advisors, tracking their ownership alongside founders, employees, and investors to reflect the company’s complete equity structure.

→ Learn more about advisory shares.

How do I prepare my cap table for due diligence or audits?

Ensure your cap table is accurate and up-to-date by verifying all equity issuances, transfers, option grants, and conversions with supporting legal documents, and clearly document ownership percentages, vesting schedules, and any outstanding convertible securities.

What is the impact of issuing stock options on cap table ownership?

Establishing an option pool from which to issue stock options increases the fully diluted share count, which reduces the ownership percentage of existing shareholders if the options are exercised, even though current share counts remain unchanged until exercise.

How does a cap table reflect an employee's stock vesting schedule?

A cap table typically notes both the total shares granted to an employee, the vesting schedule, and the number of shares vested to date, often in separate columns, providing clear tracking of what is earned versus unvested and subject to future vesting events.

How do I handle multiple share classes in a cap table?

List each share class separately, recording the number of shares, holders, and specific rights for each, and calculating ownership percentages and fully diluted shares for each class as well as in total.

How do I use cap table analytics to inform my growth strategy?

Cap table analytics reveals ownership distribution, potential dilution from future fundraising or option grants, and identifies capacity for new equity incentives. This enables more informed decisions during investor negotiations, employee compensation, and planning for future capital needs.

Can I add historical stock purchase plans and equity grants in a cap table?

Yes, you should include historical stock purchase plans and equity grants in your cap table to maintain an accurate record of all ownership changes and provide a complete view of your company’s equity history.

What is the best way to share cap table data with investors securely?

The best way to share your cap table with investors is to use reputable cap table management software with controlled access, or share encrypted files via secure platforms, ensuring only authorized recipients can view or download sensitive information.

How do funding milestones reflect on a cap table?

Funding milestones are reflected on a cap table as new share issuances or classes to new investors, updating ownership percentages and valuations to show the impact of each financing round on all shareholders.

How can I use a cap table software to forecast exit values?

A cap table software with scenario modeling features can forecast exit values by modeling different exit scenarios, calculating payouts to each shareholder class based on ownership, preferences, and dilution, and providing clarity on potential returns from acquisitions, mergers, or IPOs.

How does cap table software help in raising new capital?

Cap table software helps in raising new capital by clearly displaying current ownership, modeling dilution from new investments, generating up-to-date reports for investors, and ensuring all equity data is accurate and easily accessible for decision-making.

What features should I look for in cap table management software?

Look for features such as accurate equity tracking, support for multiple share classes, vesting and option management, scenario modeling, compliance tools, secure document storage, permission controls, investor reporting, and an intuitive interface.

How do I choose the right cap table software for my startup?

Choose the right cap table software for your startup by assessing your needs for equity tracking, ease of use, support for multiple share classes and vesting, scenario modeling, compliance features, integration with legal and HR systems, data security, scalability, and customer support.

DISCLOSURE: This communication is on behalf of eShares, Inc. dba Carta, Inc. ("Carta"). This communication is for informational purposes only, and contains general information only. Carta is not, by means of this communication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services nor should it be used as a basis for any decision or action that may affect your business or interests. Before making any decision or taking any action that may affect your business or interests, you should consult a qualified professional advisor. This communication is not intended as a recommendation, offer or solicitation for the purchase or sale of any security. Carta does not assume any liability for reliance on the information provided herein. © 2026 Carta. All rights reserved. Reproduction prohibited.